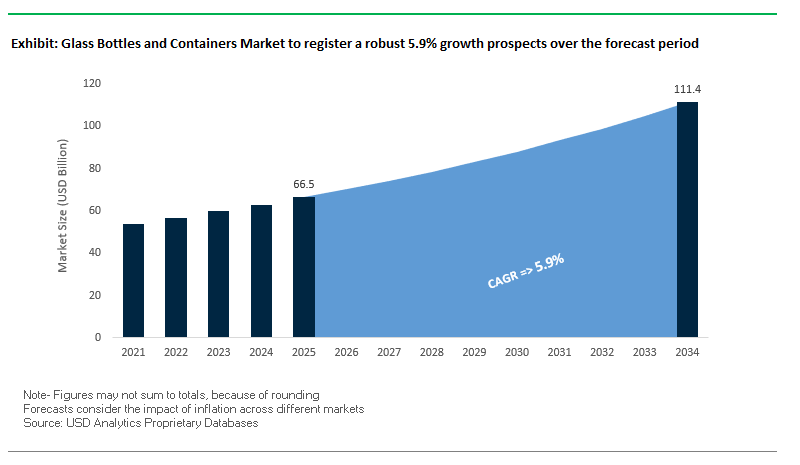

Market Overview: Global Glass Bottles and Containers Market to Surpass $111.4 Billion by 2034

The global glass bottles and containers market is valued at $66.5 billion in 2025 and is projected to reach $111.4 billion by 2034, expanding at a CAGR of 5.9%. Glass packaging continues to dominate premium beverage categories, food storage applications, and pharmaceutical packaging due to its chemical inertness, recyclability, and brand-enhancing qualities. For buyers and industry professionals, glass offers unmatched advantages in terms of sustainability, safety, and consumer perception, making it a resilient choice amid packaging innovation trends.

Lightweighting technology has reduced the weight of wine and juice bottles by 12% since 2021, lowering costs and carbon emissions. Meanwhile, high recycled content is driving circular economy adoption, with industry-government collaborations ensuring standardized measurement methodologies. Premiumization is also a critical driver, as spirits and wine producers increasingly choose glass to reinforce brand image, with 44% of alcoholic beverage packaging in 2024 utilizing glass formats. Additionally, the demand for non-reactive packaging in food and pharma ensures steady growth across multiple verticals.

Key Insights for Industry Professionals:

- Lightweighting Reduces Costs and Emissions: Average glass bottles are now 12% lighter compared to 2021.

- High Recycled Content Drives Circularity: UK glass manufacturers are setting benchmarks for measuring recycled content.

- Premiumization in Alcoholic Beverages: 44% of unit packaging in beer, wine, and spirits relied on glass in 2024.

- Non-Reactive Advantage in Pharma & Food: Glass ensures purity and safety, making it indispensable in sensitive applications.

Market Analysis: Recent Strategic Developments in Glass Bottles and Containers

The glass bottles and containers industry has undergone significant strategic and operational changes in 2024–2025, reflecting a mix of sustainability commitments, facility expansions, and optimization measures.

In September 2025, O-I Glass announced it would end production at its Portland, Oregon facility, affecting 90 employees as part of broader optimization under its “Fit to Win” strategy. Despite this, the company reported 4% growth in Q2 2025 sales volume in the Americas, attributed to efficiency gains. Meanwhile, Verallia posted strong financial results in August 2025, with profitability boosted by higher volumes and cash generation, signaling resilience in European demand.

Innovation and sustainability remain at the forefront. Ardagh Glass Packaging won Clear Choice Awards in May 2025 for innovative designs, including refillable milk bottles and heritage-inspired ale bottles. In April 2025, Ardagh also powered its California facility with a solar field, underscoring its commitment to clean energy. Expansion continues globally, as Vitro SAB de CV invested $70 million in March 2025 to build a new furnace in Toluca, Mexico, while Verallia completed its €230 million acquisition of Vidrala’s Italian operations in July 2024, strengthening its European footprint.

Other notable shifts include Krones’ July 2025 acquisition of Netstal Maschinen AG, giving beverage producers access to integrated PET solutions, indirectly complementing the glass industry by promoting hybrid portfolios. Collectively, these moves emphasize how the market is balancing sustainability, capacity expansion, and operational efficiency to stay competitive.

Trends and Opportunities Transforming the Glass Bottles and Containers Market

Strategic Investment in Domestic Production Capacity and Supply Chain Resilience

The glass bottles and containers market is witnessing a wave of large-scale capital investments aimed at strengthening domestic production capacity and regional supply chain resilience. Driven by geopolitical risks, rising shipping costs, and growing consumer demand for locally sourced sustainable packaging, manufacturers are committing significant resources to expand operations within key markets such as North America and Europe.

In the U.S., Anchor Glass Container Corporation secured a $100 million recapitalization package to enhance its production capabilities and support ongoing expansion. This move reflects the industry’s broader response to fortify domestic manufacturing infrastructure. Similarly, Arglass is investing over $230 million in its Valdosta, Georgia campus to build a second state-of-the-art furnace capable of producing more than 350 million containers annually by mid-2025. These initiatives directly address the rising demand for glass packaging across food, beverage, and pharmaceutical applications while reducing reliance on global imports.

In Europe, innovation in lightweight wine bottles demonstrates the region’s dual focus on sustainability and supply chain efficiency. A major glass producer launched a 390g lightweight wine bottle in France, showcasing how advanced engineering can reduce material use and transport emissions while maintaining premium aesthetics. Collectively, these investments are repositioning glass as a strategically resilient and future-ready packaging format.

Accelerated Adoption of High-Level Cullet in Furnaces to Reduce Carbon Footprint

Sustainability imperatives are pushing glass manufacturers to increase the proportion of cullet (recycled glass) in their production processes. Using cullet reduces both the energy intensity of furnaces and overall greenhouse gas emissions, aligning with corporate ESG strategies and regulatory expectations. According to the U.S. Environmental Protection Agency, using recycled glass significantly lowers energy demand compared to virgin raw materials.

One of the world’s leading packaging manufacturers recently introduced a lightweight wine bottle with up to 80% recycled content, far exceeding Europe’s current average of 50%. Meanwhile, Verallia has established a network of 19 dedicated cullet treatment centers worldwide to secure high-quality recycled inputs for production. These initiatives underline the industry’s push toward a circular economy model, where material reuse reduces environmental impact and supports compliance with tightening carbon reduction targets.

With consumer brands and governments demanding measurable sustainability outcomes, high-cullet furnaces are becoming the industry standard, simultaneously reducing costs, lowering emissions, and strengthening the environmental credentials of glass packaging.

Development of Lightweighting Technologies for Premium Segments

Lightweighting represents a major growth opportunity, particularly in premium beverage and personal care segments where glass aesthetics and durability are non-negotiable. By leveraging advanced coatings, nanoscale strengthening, and digital simulation technologies, manufacturers can deliver bottles that are both lighter and stronger.

For example, O-I Glass launched a 390g lightweight wine bottle with a 25% lower carbon footprint compared to conventional 500g bottles. In addition, collaborations involving “virtual twin” simulations are enabling the development of external coatings that reduce surface micro-cracks, improving durability on high-speed production lines. These breakthroughs not only reduce raw material use and transport costs but also allow brands to align their packaging with ambitious climate targets.

Nanotechnology-driven surface treatments further enhance glass resistance to breakage, enabling producers to pursue aggressive lightweighting strategies without compromising performance. As brands increasingly demand eco-efficient premium packaging, lightweight glass containers offer a direct route to sustainability, cost optimization, and differentiation in competitive markets.

Capitalizing on Regulatory Shifts Targeting Single-Use Plastics

Global regulatory frameworks targeting single-use plastics are positioning glass as a preferred packaging alternative across beverages, food, and cosmetics. The EU Single-Use Plastics Directive and India’s nationwide ban on plastic disposables are directly accelerating substitution toward glass containers. As governments enforce recyclability mandates and penalize non-compliant packaging through higher EPR fees, glass emerges as a compliance-ready, recyclable, and safe alternative.

Market data highlights that brands switching to glass packaging are consistently outperforming competitors reliant on plastic. A consumer survey revealed that 92% of shoppers consider sustainability in their purchasing decisions, with many willing to pay a premium for eco-friendly options. For CPG companies, glass provides not only a regulatory-safe pathway but also a marketing advantage, as it communicates premium quality, product purity, and environmental responsibility.

Competitive Landscape: Global Leaders Shaping Glass Bottles and Containers

The glass bottles and containers market is highly concentrated, led by multinational giants investing in lightweighting, recycled content, and renewable energy to maintain competitive advantage.

O-I Glass: Driving Growth with Fit to Win Strategy

O-I Glass is one of the largest global suppliers of glass containers for beverages, food, and pharmaceuticals. Its “Fit to Win” strategy emphasizes production footprint optimization and modernization. In Q2 2025, O-I achieved 4% volume growth in the Americas despite weak European demand. It leads in lightweighting, having introduced a 75cl eco-designed wine bottle 25% lighter than traditional formats, validated by the Carbon Trust. With its MAGMA modular system and operations in over 20 countries, O-I continues to push for higher efficiency and lower carbon impact.

Verallia: Expanding European Footprint with Vidrala Acquisition

Verallia, a leading European producer, completed its €230 million acquisition of Vidrala’s Italian glass business in July 2024, adding 225 kilotons of annual capacity. In August 2025, it reported recovery in profitability and cash flow, aided by higher volumes. Its “Verallia Green” product line, featuring high recycled content, aligns with brand and government sustainability goals. Strong financial positioning through bond issuance further supports Verallia’s expansion and eco-friendly innovation strategy.

Ardagh Group: Innovating with ECO Series and Clean Energy Investments

Ardagh Group combines sustainability with design innovation. In May 2025, its ECO Series™ lightweight bottles and refillable solutions won Clear Choice Awards. Its April 2025 initiative to power its California facility with solar energy demonstrates its leadership in renewable-powered manufacturing. With a global portfolio spanning metal and glass, Ardagh offers integrated design, decoration, and packaging solutions, reinforcing its status as a leading partner for premium food and beverage brands.

Vidrala: Streamlining Operations to Focus on Core European Markets

Vidrala specializes in lightweight glass bottles for food and beverages, particularly wine and spirits. In July 2024, it divested its Italian operations to Verallia, allowing it to refocus on core markets in Spain, Portugal, and Central Europe. Its strategy emphasizes carbon neutrality and furnace innovation, with investments in alternative fuels and efficiency improvements. Vidrala’s niche strength lies in producing high-quality, sustainable bottles tailored to premium beverage brands.

NSG Group: Expanding Specialty Glass for Food and Pharma

Nippon Sheet Glass (NSG Group) is traditionally known for automotive and architectural glass but has expanded into specialty glass for food and pharmaceuticals. In July 2025, it opened a new production line in St Helens, UK, reinforcing local supply chains. In August 2025, NSG reported strong Q1 2026 results, driven by specialty glass demand. Recognized by CDP with a “Supplier Engagement Leader” and Climate A- rating, NSG aligns its strategy with sustainability while expanding its high-value specialty offerings.

Glass Bottles and Containers Market Share Insights

Bottles Dominate Market Share by Product Type in Glass Bottles and Containers Industry

In 2025, glass bottles command 65% of the glass bottles and containers market, reinforcing their status as the undisputed leader in this segment. Their dominance stems from the global beverage industry, where glass is irreplaceable for beer, wine, spirits, and premium juices due to its inertness, impermeability, and superior brand image. Glass bottles not only protect carbonation and flavor but also provide a premium identity that is vital for consumer perception in alcohol and luxury beverage categories. Jars follow with 20%, serving as the preservation standard for jams, sauces, pickles, and baby food, where product visibility and trust are paramount. Vials and ampoules represent a high-value niche, primarily supporting pharmaceuticals and high-end cosmetics, where sterility and compatibility are critical. Other decorative and specialty containers, while small in share, play a strategic role in luxury branding. Collectively, this distribution highlights how bottles dominate volumes through beverages, jars anchor food preservation, and vials drive precision packaging for high-value industries.

Beverages Drive Market Share by Application in Glass Bottles and Containers Industry

By application, beverages account for 55% of the glass bottles and containers market in 2025, making this sector the anchor of the industry. Alcoholic beverages such as spirits, wine, and craft beer, along with premium juices and waters, overwhelmingly rely on glass due to its unmatched ability to protect taste and project brand heritage. Food packaging follows with 20%, where glass jars and bottles preserve flavor integrity and deliver the premium, “natural” image that consumers increasingly associate with quality. Pharmaceuticals represent a safety-critical application, driven by Type I borosilicate glass used for injectables and sensitive drug formulations, where regulatory standards dictate glass as the only viable option. Cosmetics and perfumes remain a luxury-driven segment, where glass bottles and jars symbolize weight, exclusivity, and sensory appeal. This segmentation underscores how the beverage sector anchors demand, food applications sustain tradition, and pharmaceuticals and cosmetics add value through safety and luxury positioning.

United States: Lightweighting and Premiumization Driving Glass Packaging Innovation

The U.S. glass bottles and containers market is experiencing significant transformation driven by sustainability and premiumization trends. Companies such as O-I Glass are investing in lightweighting technology to produce lighter glass containers, reducing transportation costs and carbon emissions, which is critical for addressing environmental concerns. Recycling infrastructure improvements are another key focus, with initiatives by the Glass Packaging Institute (GPI) enhancing the availability of recycled glass cullet, lowering energy consumption and reducing dependence on virgin materials. The demand for high-quality, aesthetically appealing glass packaging is increasing, particularly in the craft beverage and gourmet food segments, as premium products require packaging that preserves integrity while offering a luxury feel. Regulatory advantages, such as the FDA’s GRAS (generally recognized as safe) classification for glass, further enhance its appeal by ensuring chemical safety, making it a preferred choice for health-conscious consumers and brands prioritizing product safety.

Germany: Circular Economy Leadership and Advanced Pharmaceutical Glass Production

Germany’s glass bottles and containers industry is at the forefront of sustainable packaging, driven by the German Packaging Act (VerpackG) and preparations for the EU Packaging and Packaging Waste Regulation (PPWR). Manufacturers are leading in lightweighting innovations, with companies like Stoelzle Glass Group producing high-quality, low-weight glass for pharmaceutical, cosmetic, and spirits applications, reducing carbon footprints in production and transport. Germany is also a global hub for pharmaceutical glass, with Gerresheimer AG developing sustainable glass vials for injectable drugs, meeting the rising demand for safe, reliable packaging in advanced medicines. The market emphasizes a circular economy, with many manufacturers incorporating 100% recycled glass cullet into production, strengthening the country’s leadership in environmentally responsible glass packaging.

China: Rising Demand for Premium Glass and Sustainability Initiatives

China’s glass bottles and containers market is growing rapidly due to rising disposable incomes, urbanization, and increasing domestic demand in alcoholic beverage, food, and beverage sectors. There is a strong focus on premium, aesthetically sophisticated glass packaging, particularly for cosmetics, perfumery, and high-end spirits, driven by the expanding middle-class consumer base. Government policies promoting sustainability, including plastic bans and waste management regulations, are compelling manufacturers to adopt eco-friendly and reusable packaging alternatives. These regulatory initiatives, combined with rising consumer awareness, are fostering a market environment where premium quality and environmental responsibility go hand in hand, encouraging manufacturers to innovate in both design and material usage.

India: “Make in India” Driving Capacity Expansion and Specialty Glass Production

India’s glass bottles and containers market is being shaped by the “Make in India” initiative, attracting capital investments and strengthening domestic manufacturing capabilities. Leading players such as AGI Greenpac and Hindustan National Glass have expanded production capacities to meet rising domestic demand. Technological upgrades and R&D investment are enabling the production of high-end specialty glass for cosmetic and perfumery sectors, with a focus on exports to the U.S. and Europe. Shifting consumer preferences towards health, hygiene, and premium products are driving demand for glass packaging, particularly for food and pharmaceutical applications. Growth in the alcoholic beverage segment, especially in premium Indian Made Foreign Liquor (IMFL), is further propelling the adoption of 100% glass packaging solutions.

Brazil: Bioplastics Integration and Circular Economy Reinforcing Sustainability

Brazil’s glass bottles and containers market is increasingly aligned with sustainability initiatives, particularly in integrating bioplastics and eco-friendly alternatives. Green polyethylene derived from sugarcane ethanol is being leveraged to reduce dependence on fossil fuels. Regulatory oversight by Anvisa ensures that glass packaging meets strict food contact safety standards, encouraging the production of high-quality, safe containers. The Brazilian government’s focus on circular economy practices, including anticipated decrees for mandatory recycling and potential bans on single-use items, is incentivizing companies to adopt sustainable packaging strategies. Programs like “eureciclo,” which award Packaging Recycling Certificates, are reinforcing environmentally responsible practices in the glass packaging sector.

Japan: Lightweighting and Recycling Technologies Enhance Efficiency and Safety

Japan’s glass bottles and containers market is emphasizing lightweighting and high-quality production to address environmental and operational challenges. Companies like Toyo Glass are developing eco-friendly, lightweight glass packaging that reduces energy consumption during manufacturing and transportation. The market operates under the strict Japanese Sanitation Act, driving a focus on highly hygienic and safe packaging solutions that minimize contamination risks. Additionally, Japan has developed an extensive glass recycling infrastructure, with over 18 facilities converting bottles and containers into cullets and powder for new production. These measures strengthen the country’s commitment to sustainability, product safety, and operational efficiency in glass packaging.

Glass Bottles and Containers Market Report Scope

Glass Bottles and Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$66.5 Billion

|

|

Market Size (2034)

|

$111.4 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Type (Bottles, Jars, Vials & Ampoules, Other Containers), By Color (Flint (Clear), Amber, Green, Other Colors), By Application (Beverages, Food Packaging, Pharmaceuticals, Cosmetics & Perfumes, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Owens-Illinois (O-I), Ardagh Group S.A., Verallia S.A., Vitro S.A.B. de C.V., Vidrala S.A., Gerresheimer AG, Stoelzle Glass Group, Hindusthan National Glass & Industries Limited (HNG), AGI Greenpac, Consol Glass (Pty) Ltd., PGP Glass Private Limited, Nihon Yamamura Glass Co., Ltd., Zignago Vetro S.p.A., Anchor Glass Container Corporation, Saverglass S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Bottles and Containers Market Segmentation

By Product Type

- Bottles

- Jars

- Vials & Ampoules

- Other Containers

By Color

- Flint

- Clear

- Amber

- Green

- Other Colors

By Application

- Beverages

- Food Packaging

- Pharmaceuticals

- Cosmetics & Perfumes

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Glass Bottles and Containers Market

- Owens-Illinois (O-I)

- Ardagh Group S.A.

- Verallia S.A.

- Vitro S.A.B. de C.V.

- Vidrala S.A.

- Gerresheimer AG

- Stoelzle Glass Group

- Hindusthan National Glass & Industries Limited (HNG)

- AGI Greenpac

- Consol Glass (Pty) Ltd.

- PGP Glass Private Limited

- Nihon Yamamura Glass Co., Ltd.

- Zignago Vetro S.p.A.

- Anchor Glass Container Corporation

- Saverglass S.A.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global glass bottles and containers market, providing an in-depth analysis of market dynamics, strategic developments, and technological breakthroughs shaping the industry. The study reviews historic data from 2021 to 2024 and presents forward-looking forecasts through 2034, highlighting trends such as lightweighting, high recycled content adoption, premiumization, and regulatory-driven material substitution. The analysis reviews innovations in production processes, cullet utilization, and specialty glass solutions for pharmaceuticals, food, beverages, and cosmetics, while showcasing sustainability initiatives and operational optimization strategies. This report highlights the competitive landscape, tracking investments, mergers, and capacity expansions among 15+ leading companies globally. Designed for industry professionals, investors, and procurement specialists, this report is an essential resource for understanding supply chain resilience, strategic growth opportunities, and market positioning, enabling stakeholders to make informed decisions in the glass packaging sector.

Scope Highlights

- Segmentation: By Product Type (Bottles, Jars, Vials & Ampoules, Other Containers), By Color (Flint/Clear, Amber, Green, Other Colors), By Application (Beverages, Food Packaging, Pharmaceuticals, Cosmetics & Perfumes, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024 and forecast from 2025 to 2034

- Company Analysis: Profiles and strategic insights for 15+ major players including O-I Glass, Ardagh Group, Verallia, Vitro, Vidrala, Gerresheimer AG, and others

Methodology

The study employs a comprehensive research methodology combining primary and secondary sources to ensure accuracy and relevance for industry professionals. Data collection included interviews with key stakeholders, surveys with manufacturers, suppliers, and distributors, as well as analysis of company filings, investor presentations, and regulatory documents. USDAnalytics applied quantitative modeling to evaluate market size, growth trends, and segment performance, while qualitative analysis captured technological breakthroughs, sustainability initiatives, and premiumization strategies. Forecasting models were developed using historical trends, capacity expansions, and global consumption patterns, accounting for regional regulatory frameworks and market disruptions. Competitive benchmarking and SWOT analyses of leading players provide actionable insights, ensuring a robust understanding of global supply chains, production capacities, and emerging opportunities in glass bottles and containers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.