Alcoholic Beverage Packaging Market Overview: Market Size, Growth, and Key Insights

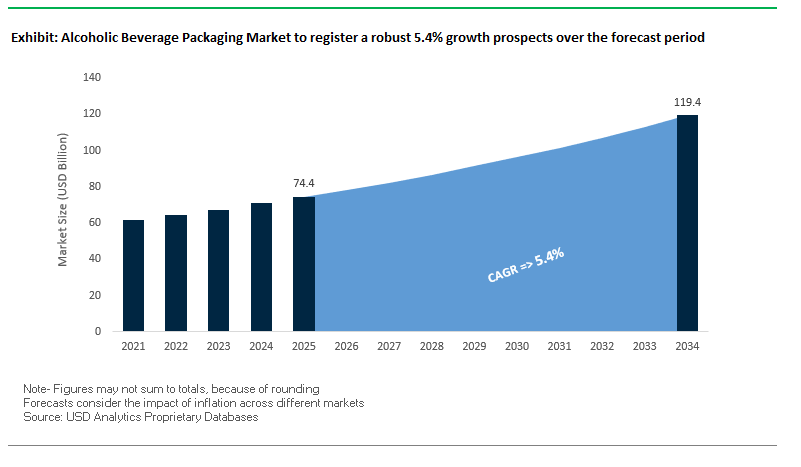

The Global Alcoholic Beverage Packaging Market is projected to reach $74.4 billion in 2025 and expand further to $119.4 billion by 2034, growing at a CAGR of 5.4% during the forecast period. The sector is undergoing a transformation driven by shifting consumer preferences, sustainability regulations, and advancements in design technology. Packaging has evolved beyond containment and protection; it has become a strategic branding tool, shaping consumer perception, purchase behavior, and sustainability narratives.

Glass continues to dominate the premium beverage space due to its non-reactive qualities and perception of luxury, while aluminum cans are rapidly growing across craft beers and ready-to-drink cocktails owing to their portability and recyclability. At the same time, sustainability and smart packaging are reshaping the industry, as companies integrate recycled content and interactive features into their packaging portfolios.

Key Insights for Industry Professionals

- Glass Bottles Remain Premium Standard: Over half of alcoholic beverages are packaged in glass, highlighting consumer trust in quality and heritage appeal.

- Aluminum Cans on Growth Trajectory: Rising adoption in craft beer and RTD cocktails due to convenience, portability, and design flexibility.

- Sustainability at Core: Glass and aluminum remain infinitely recyclable; one aluminum can re-enters the market in as little as 60 days.

- Smart Packaging: Increasing integration of AR labels, QR codes, and thermochromic inks for consumer engagement and brand authenticity.

Market Analysis: Recent Developments and Strategic Shifts

The alcoholic beverage packaging industry has been marked by significant developments that underscore its innovation, sustainability focus, and global expansion strategies. In August 2025, Crown Holdings achieved a critical milestone when its net-zero targets were validated by the Science Based Targets initiative (SBTi), reinforcing its position as a sustainability leader. Similarly, in July 2025, Crown reported robust Q2 results, highlighting the resilience of demand in beverage cans.

Ball Corporation has strengthened its innovation leadership. In May 2025, the company won four EMBANEWS Awards in Brazil for sustainable packaging breakthroughs, including a braille-embossed lid to enhance accessibility. Around the same time, Ball entered a joint venture in March 2025 to accelerate its aluminum cup business, aligning with global momentum toward circular economy models.

On the glass packaging front, Verallia showcased industrial strength in May 2025 by announcing the production of more than 16 billion bottles and jars in 2024, cementing its role as a leading European glass provider. O-I Glass, meanwhile, released its Design Book 3 in October 2024, reflecting the increasing role of creativity and aesthetics in differentiating beverage brands.

In April 2025, SIG strategically partnered with Namaqua Wines to bring carton packaging into the low-alcohol wine space, signaling diversification in formats beyond glass and cans. DS Smith also contributed to the sustainability agenda in November 2024 by investing $25 million into its Polish operations, expanding eco-friendly solutions across Central and Eastern Europe.

Key Trends and Strategic Opportunities Driving the Alcoholic Beverage Packaging Market

Strategic Adoption of Lightweighting and Alternative Formats to Reduce Carbon Footprint

The alcoholic beverage packaging market is witnessing a significant strategic shift towards lightweighting and alternative packaging formats, particularly for glass bottles, which are a major contributor to carbon emissions. Leading producers are investing heavily in reducing bottle weight while maintaining product integrity. For example, Diageo has successfully reduced Baileys bottles by 28 grams and Johnnie Walker Blue Label bottles by 16%, collectively saving over 1,600 tonnes of glass and significantly cutting carbon emissions. The Ellen MacArthur Foundation emphasizes that glass production and transport are major contributors to a beverage company’s carbon footprint, highlighting the importance of these lightweighting initiatives. Companies such as Anheuser-Busch InBev (AB InBev) are targeting 100% of their products in recyclable or high-recycled-content packaging by 2025, reinforcing the industry’s push for more sustainable packaging solutions. This trend is both a regulatory response and a consumer-driven imperative, reflecting a broader movement towards eco-efficient and carbon-conscious beverage packaging.

Integration of Smart and Connected Packaging for Consumer Engagement and Traceability

Alcoholic beverage brands are increasingly embedding NFC tags, QR codes, and other digital technologies into packaging to enhance consumer engagement, ensure product authenticity, and provide traceability. With estimates suggesting that 25-40% of global spirits consumption is counterfeit, NFC-enabled caps allow consumers to verify authenticity instantly, mitigating safety and financial risks. QR codes are also being used to create dynamic brand experiences, linking consumers to cocktail recipes, virtual masterclasses, and interactive content, effectively transforming bottles into data-rich marketing channels. Additionally, new EU regulations mandating ingredient transparency are accelerating the adoption of digital labeling, enabling brands to meet compliance requirements without cluttering physical labels, demonstrating a convergence of consumer engagement and regulatory compliance in smart alcoholic beverage packaging.

Development of a Scalable, High-Barrier Paper-Based Bottle

There is a compelling opportunity to commercialize paper-based bottles that meet oxygen barrier requirements for spirits and wines, offering a sustainable alternative to glass. Frugalpac’s “Frugal Bottle,” primarily made from recycled paperboard, achieves a carbon footprint up to six times lower than traditional glass bottles, addressing both manufacturing and transport emissions. Technological advancements, including ultra-thin recyclable liners and innovative pulp-molding processes, are enabling high-performance protection for oxygen-sensitive beverages. Trials by Diageo and adoption by wineries across Europe and the U.S. validate the commercial feasibility of paper-based bottles. U.S. wine producers investing millions in dual-format bottling systems further demonstrate the growing market acceptance of sustainable, high-barrier paper packaging solutions for alcoholic beverages.

Standardization and Adoption of Refillable and Reusable Packaging Systems

The industry is also exploring cross-brand, standardized refillable and reusable packaging systems to move beyond single-use containers. Diageo’s partnership with ecoSPIRITS pilots a closed-loop refillable system using durable 4.5L ecoTOTE containers, designed for up to 150 uses and potentially eliminating up to 1,000 single-use bottles per unit. Collaborative efforts led by the Ellen MacArthur Foundation emphasize the need for standardized bottle formats and shared reverse logistics networks to enable large-scale adoption. Deposit return schemes, such as the one recently launched in Romania with a 77% return rate in three months, demonstrate both economic viability and environmental effectiveness, underscoring the potential for scalable, sustainable, and cost-efficient refillable beverage packaging systems.

Competitive Landscape: Leading Companies in Alcoholic Beverage Packaging

The competitive landscape of the global alcoholic beverage packaging market is shaped by leading players that combine industrial capacity, sustainability commitments, and innovative packaging solutions. Each company has developed unique strengths to address the evolving needs of premiumization, recyclability, and consumer engagement.

Crown Holdings, Inc.: Driving Decorative Innovation in Aluminum Packaging

Crown Holdings is a major global producer of metal packaging with 57 beverage can facilities worldwide. Its innovations include thermochromic inks and premium finishes to enhance shelf appeal. In addition, the company’s Twentyby30 program emphasizes material reduction and circularity, strengthening its position as a sustainability-focused partner for global beverage brands.

Ardagh Group S.A.: Advancing Lightweight and Sustainable Packaging Solutions

Ardagh Group provides infinitely recyclable glass and metal packaging, focusing on lightweighting through advanced design modeling. The company emphasizes decorative customization such as embossing and color variations for branding impact. Its strategic positioning revolves around sustainability and energy efficiency, aligning with eco-conscious beverage manufacturers.

Ball Corporation: Leading in Sustainable Aluminum Innovation

Ball Corporation continues to pioneer sustainable aluminum packaging solutions. With the development of its ReAl alloy and proprietary lightweight cans, Ball reduces material consumption while ensuring durability. The company has also gained recognition for its accessibility-driven innovations, such as braille-embossed lids, reinforcing its commitment to inclusive design.

Verallia S.A.: Championing Glass Packaging Circularity

Verallia, the third-largest global glass packaging producer, maintains leadership in the wine and spirits segment. Its production scale of 16 billion units in 2024 demonstrates industrial strength. Verallia is deeply committed to the circular economy, ensuring glass is endlessly recycled without quality loss. Its decorative capabilities help brands differentiate in a highly competitive retail environment.

O-I Glass, Inc.: Innovating Through Design-Driven Glass Packaging

O-I Glass leverages innovation and aesthetics to enhance the role of glass packaging. Its Drinktainer product line reimagines single-serve glass with wide-mouth containers to enhance aroma release and consumer experience. Additionally, its Catalyst Collection blends design and consumer psychology to deliver emotionally resonant glass packaging. O-I’s focus on sustainability and innovation reinforces its premium market positioning.

Alcoholic Beverage Packaging Market Share Insights

Bottles Dominate Market Share by Packaging Type in the Alcoholic Beverage Packaging Industry

Glass bottles command the largest share, at an estimated 65%, cementing their role as the unshakable icon of alcoholic beverage packaging. Their dominance is rooted in consumer perception of quality, purity, and brand heritage factors especially critical in spirits and wine, where packaging is directly tied to product value. Glass bottles also deliver functional advantages, including inertness that prevents flavor migration and excellent recyclability when cullet is integrated into production. Aluminum cans, with around 25%, represent the fastest-growing segment. Once considered a format for low-cost beer, cans are now widely used for craft beers, hard seltzers, and ready-to-drink (RTD) cocktails. Their recyclability, portability, and light-and-oxygen barrier performance are driving adoption among younger consumers and sustainability-conscious brands. Pouches, bags, and cartons remain convenience-driven niches, primarily for bag-in-box wines and value-tier products, where cost savings and lighter transport weights outweigh the lack of premium positioning. The “other” category, though small, plays an outsized role in branding innovation, with stainless steel kegs, ceramic bottles, and specialty formats differentiating craft and luxury brands.

Breweries Drive Market Share by End-User in the Alcoholic Beverage Packaging Industry

Large-scale breweries account for nearly 40% of end-user demand, driven by their massive production volumes and reliance on high-speed filling lines for glass bottles and aluminum cans. Their economies of scale and global logistics networks make them the most influential stakeholders in shaping packaging standards. Wineries remain the guardians of tradition, anchoring demand for glass bottles in premium segments while increasingly leveraging bag-in-box formats for casual consumption and export markets. Distilleries reinforce glass’s supremacy, relying almost exclusively on bespoke bottle shapes and closures to communicate premium identity and heritage making this the most conservative end-user group in packaging experimentation. Craft breweries and microbreweries, while smaller by volume, act as the innovation hub. Their early adoption of aluminum cans for premium beers broke longstanding consumer perceptions and opened new growth channels. Their frequent use of distinctive formats such as 16oz tallboys and elaborately designed labels underscores their influence on broader industry trends. Collectively, end-user segmentation reveals a mature but evolving industry, where tradition anchors demand but innovation in cans and alternative formats drives future growth.

United States: TTB Labeling Updates and Sustainability Drive Innovation in Alcoholic Beverage Packaging

The U.S. alcoholic beverage packaging market is witnessing significant transformation driven by evolving regulations and sustainability initiatives. The Treasury Department's Alcohol and Tobacco Tax and Trade Bureau (TTB) proposed new labeling rules in January 2025, including mandatory “Nutrition Facts” panels detailing calories, carbohydrates, and allergens. This regulatory shift requires companies to redesign packaging to ensure compliance and enhance consumer information.

Technological advancements and corporate initiatives are further shaping the market. In July 2024, Diageo and ecoSPIRITS introduced refillable ecoTOTE containers across 18 countries, reducing single-use packaging and promoting a circular economy. Brands like Ketel One Family Made Vodka have adopted AQR technology with QR codes on bottles to improve accessibility for visually impaired consumers. Sustainability remains central, with increasing adoption of recyclable metal and glass packaging, supported by investments from companies like Ball Corporation in automated aluminum production. State-level Extended Producer Responsibility (EPR) laws are also influencing design and waste management, driving innovation in packaging solutions that align with eco-conscious consumer trends.

Germany: Circular Economy Leadership and Recyclable Alcoholic Beverage Packaging

Germany’s alcoholic beverage packaging market is strongly influenced by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reuse by 2030. The Packaging Act (VerpackG) holds producers accountable for the entire lifecycle of their packaging, fostering the development of highly recyclable mono-material bottles and cans and robust collection systems for packaging waste.

Technological innovations, including lightweight glass and aluminum cans such as Toyo Seikan's 6.1g beverage can launched in 2024, are reducing material use while maintaining structural integrity. Corporate initiatives, including collaborations by Beiersdorf AG with packaging innovators, emphasize sustainable production practices. The growth of e-commerce in Germany is driving demand for durable and high-quality packaging capable of withstanding shipping, while a shift to recyclable and lightweight materials aligns with both regulatory requirements and consumer preference for environmentally friendly alcoholic beverage packaging.

China: Dual Carbon Goals and Technological Integration Drive Sustainable Packaging

China’s alcoholic beverage packaging market is experiencing rapid growth influenced by the government’s “dual carbon” goals targeting carbon peak and neutrality. Policies promoting eco-friendly and reusable materials are reshaping packaging design and production. Chinese manufacturers are integrating automation, AI, and “5G plus industrial internet” solutions to optimize production efficiency, enhance flexibility, and reduce material waste.

Sustainability is a major focus, with restrictions on non-degradable plastics driving demand for paper-based and recyclable alternatives. Corporate expansion highlights include Primega Group’s acquisition of China Wangmao Liquor Industry Group in August 2025, aimed at entering the premium Baijiu market while leveraging intelligent technologies for supply chain optimization. The rapid rise of domestic e-commerce platforms is boosting demand for sustainable, customizable packaging across diverse product categories, cementing China’s position as a strategic market for innovative alcoholic beverage packaging solutions.

India: Regulatory Support and Premiumization Boost High-Quality Alcoholic Packaging

India’s alcoholic beverage packaging market is supported by the “Make in India” initiative and “Zero Effect Zero Defect” missions, promoting quality domestic production and regulatory support. Packaging and labeling are governed by the Food Safety and Standards (Alcoholic Beverages) Regulations, 2018, alongside state-level excise laws, mandating statutory warnings, font sizes, and allergen disclosures.

Investments in infrastructure, including automated packaging lines and on-site production systems, are increasing efficiency for glass and aluminum containers. Premiumization trends are driving demand for high-quality packaging, especially among middle-class consumers preferring international brands, while advanced technologies such as QR codes and embedded sensors improve traceability and regulatory compliance. Multinational FMCG companies are expanding local production to shorten supply chains, aligning with growing consumer expectations for sustainable and innovative alcoholic beverage packaging solutions.

Brazil: Circular Economy Policies and Aluminum Innovation Reshape Alcoholic Beverage Packaging

Brazil’s alcoholic beverage packaging market is strongly influenced by the National Solid Waste Policy, which promotes a circular economy and the use of reusable, durable packaging solutions. Technological advancements, including AI and robotics, are enhancing efficiency, quality control, and the sophistication of production operations.

Sustainability is a key driver, with a 2025 ban on importing solid waste including plastics encouraging domestic recycling and eco-friendly material adoption. Strategic investments, such as Novelis Inc.’s Customer Solution Center in São José dos Campos, Brazil, focus on advancing aluminum can innovation and sustainable beverage packaging solutions. The growth of e-commerce is amplifying demand for protective and sustainable packaging for fragile products, positioning Brazil as a rapidly expanding market for eco-conscious and high-performance alcoholic beverage packaging.

Japan: Precision Manufacturing and Bio-Based Materials Transform Alcoholic Beverage Packaging

Japan’s alcoholic beverage packaging market is anchored in precision manufacturing and advanced technologies. AI-driven design and production processes enhance efficiency and accuracy, supporting high-quality packaging solutions. Regulatory updates by the Ministry of Health, Labour and Welfare (MHLW) in May 2025 revise the “Specifications and Standards for Foods, Additives, etc.,” imposing stricter requirements on food-contact packaging for alcoholic beverages.

Sustainability is emphasized through the adoption of bio-based materials, exemplified by LyondellBasell’s incorporation of bio-based polypropylene in Shiseido’s packaging. Continuous innovation is enhancing packaging functionality, with a focus on high dimensional stability and resistance to deformation, supporting high-performance applications. Japan’s market reflects the convergence of regulatory compliance, technological advancement, and sustainability trends, positioning it as a global leader in premium and eco-friendly alcoholic beverage packaging solutions.

Alcoholic Beverage Packaging Market Report Scope

Alcoholic Beverage Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$74.4 Billion

|

|

Market Size (2034)

|

$119.4 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Packaging Type (Bottles, Cans, Pouches & Bags, Cartons, Other), By Material (Glass, Metal, Plastic, Paper & Paperboard), By Application (Beer, Wine, Spirits, Cider, RTD Cocktails), By End-User (Breweries, Wineries, Distilleries, Craft Breweries, Microbreweries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Ball Corporation, Crown Holdings Inc., Ardagh Group S.A., O-I Glass, Inc., Trivium Packaging, AptarGroup, Inc., Mondi Group, Smurfit Kappa Group, Tetra Pak (Tetra Laval), WestRock Company, Gerresheimer AG, Sonoco Products Company, Silgan Holdings Inc., DS Smith Plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Alcoholic Beverage Packaging Market Segmentation

By Packaging Type

- Bottles

- Cans

- Pouches & Bags

- Cartons

- Others

By Material

- Glass

- Metal

- Plastic

- Paper & Paperboard

By Application

- Beer

- Wine

- Spirits

- Cider

- RTD Cocktails

By End-User

- Breweries

- Wineries

- Distilleries

- Craft Breweries

- Microbreweries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Alcoholic Beverage Packaging Market

- Amcor plc

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- O-I Glass, Inc.

- Trivium Packaging

- AptarGroup, Inc.

- Mondi Group

- Smurfit Kappa Group

- Tetra Pak (Tetra Laval)

- WestRock Company

- Gerresheimer AG

- Sonoco Products Company

- Silgan Holdings Inc.

- DS Smith Plc

* List Not Exhaustive

Methodology

USDAnalytics utilizes a comprehensive, multi-layered research methodology to provide actionable insights into the global Alcoholic Beverage Packaging Market. Our approach combines primary interviews with packaging engineers, sustainability officers, supply chain managers, and beverage brand executives, along with secondary analysis of corporate reports, regulatory filings, trade publications, and government databases. Market sizing from USD 74.4 billion in 2025 to USD 119.4 billion by 2034 at a 5.4% CAGR is assessed using both top-down and bottom-up approaches, factoring in packaging types (bottles, cans, pouches & bags, cartons, other), materials (glass, metal, plastic, paper/paperboard), applications (beer, wine, spirits, cider, RTD cocktails), and end-user segments (breweries, wineries, distilleries, craft breweries, microbreweries). USDAnalytics evaluates evolving trends such as lightweighting, sustainable materials, smart and connected packaging, refillable systems, and high-barrier paper bottles, while analyzing regional dynamics across the U.S., Germany, China, India, Brazil, and Japan. Competitive benchmarking encompasses key players such as Crown Holdings, Ball Corporation, Verallia, O-I Glass, and Ardagh Group, emphasizing innovation, sustainability leadership, and design-driven differentiation. This integrated methodology ensures industry professionals receive precise, forward-looking intelligence to optimize packaging efficiency, brand engagement, and regulatory compliance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.