Plastic Caps and Closures Market Size, Overview, and Growth Outlook (2025–2034)

Plastic Caps and Closures Market Set to Surge to $141.6 Billion by 2034 Amid Screw Closure Dominance and Sustainability Trends

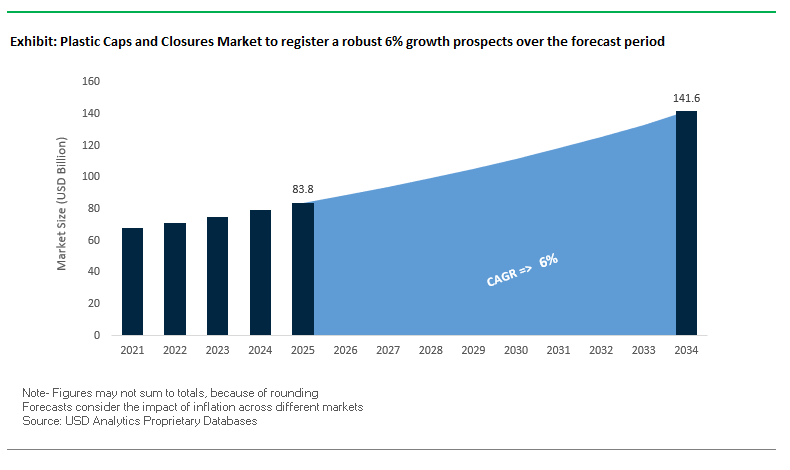

The global plastic caps and closures market is projected to grow from $83.8 billion in 2025 to $141.6 billion by 2034, representing a CAGR of 6%. Growth is primarily driven by the dominance of screw closures, the rise of tethered caps, and industry-wide initiatives in lightweighting and sustainability. The food and beverage sector remains the largest consumer, with high demand for secure, tamper-evident, and user-friendly solutions.

Key Insights for industry professionals and buyers:

- Screw Closures Lead the Market: Versatile and reliable, widely used for beverages, food, and personal care products.

- Lightweighting Reduces Costs and Environmental Impact: Many closures now use 20–30% less material, lowering production costs and carbon footprint.

- Tethered Caps Gain Traction: EU regulations and global adoption are driving the shift to caps that remain attached, enhancing recyclability.

- Food and Beverage Industry Drives Demand: Bottled water, soft drinks, sauces, and other products require secure, tamper-evident closures.

- Sustainability Fuels Innovation: Use of bio-based plastics, recycled materials, and advanced nanocoatings is shaping the future of closures.

Market Analysis: Plastic Caps and Closures Industry Accelerates Through Regulatory Compliance, Lightweighting, and Circular Economy Innovations

The plastic caps and closures market has been witnessing significant innovation driven by sustainability, lightweighting, and evolving regulatory standards. In September 2025, Siegwerk showcased circular packaging solutions at a flexible packaging summit, highlighting approaches applicable to closures. By July 2025, Closure Systems International (CSI) launched new closures for bottled water that enhance consumer experience while supporting sustainability goals.

Regulatory-driven design innovations continue to shape the industry. Tethered caps, mandated in regions like the European Union, are being increasingly adopted worldwide to improve recyclability. Developments such as Graphic Packaging International’s PaperSeal® Pressed MAP Tray in June 2025 demonstrate competitive pressure from paper-based alternatives in the food and beverage sector, prompting closure manufacturers to explore advanced materials and functional designs.

Material innovation and sustainability are also a focus. April 2025 saw Amcor collaborate with Nfinite Nanotechnology to develop nanocoated recyclable and compostable packaging with enhanced oxygen barrier properties. Additionally, industry leaders like PepsiCo and SACMI in early 2025 are advancing bio-based plastics, lightweight designs, and circular economy solutions, which are expected to impact the entire supply chain for plastic caps and closures. Earlier, in July 2024, CSI enhanced smart closure authentication technologies for traceability and anti-counterfeiting, showcasing the integration of digital solutions with packaging.

Emerging Trends and Strategic Opportunities in the Plastic Caps and Closures Market

Integration of Post-Consumer Recycled (PCR) Resin in Closure Manufacturing

The plastic caps and closures market is undergoing a major transformation as brand owners respond to global sustainability mandates and consumer demand for eco-friendly packaging. The European Union’s Single-Use Plastics Directive (SUPD), which came into effect in July 2024, mandates minimum recycled content in beverage bottles, indirectly influencing closures as brands aim for holistic compliance. Companies are increasingly extending recycled content integration to caps, recognizing that closures are an inseparable part of the package’s environmental footprint. Corporate commitments further amplify this trend: The Coca-Cola Company disclosed in its 2024 sustainability report that 28% of its global packaging mix contained recycled material, with a target to reach 30–35% recycled content in primary packaging—including closures—by 2035. Suppliers are innovating in parallel, with Closure Systems International (CSI) introducing its FDA-approved PolyCycle PCR resin, which supports brand owners in meeting Extended Producer Responsibility (EPR) requirements. These combined regulatory and corporate pressures are creating unprecedented momentum for PCR adoption in closure manufacturing.

Adoption of Lightweight and Mono-Material Closure Designs

Regulatory shifts are not only pushing for recycled content but also redefining the very design of plastic closures. The EU tethered cap mandate, effective July 2024, requires that caps remain attached to bottles after opening, forcing manufacturers to innovate with new tethered, user-friendly designs. This regulation has also accelerated efforts in lightweighting, reducing plastic per unit to minimize environmental impact and lower costs. Manufacturers are simultaneously focusing on recyclability by developing mono-material closures. TOPPAN, for instance, has introduced mono-material packaging innovations using PE and PP, eliminating the complexity of multi-polymer structures and streamlining recycling processes. Collaborative efforts like the “Every Bottle Back” initiative, spearheaded by PepsiCo, Coca-Cola, and Keurig Dr Pepper (KDP), emphasize material compatibility between bottles and closures, promoting a closed-loop recycling ecosystem. These shifts highlight how design, regulation, and collaboration are converging to drive sustainable closure innovation.

Development of Smart and Connected Closures

The transition from passive to intelligent closures represents a high-growth opportunity in the plastic caps and closures market. By embedding QR codes, NFC tags, or RFID technology, closures can deliver interactive consumer experiences while addressing critical industry needs. A GreyB report highlights that smart closures can authenticate products, track usage habits, and provide digital content, transforming closures into an active communication and engagement tool. In pharmaceuticals, this technology is gaining traction as a means to combat counterfeiting. Case studies demonstrate how RFID-enabled closures allow patients and pharmacists to instantly verify authenticity and access secure product information, enhancing patient safety. The convergence of smart packaging and closures not only strengthens supply chain transparency but also provides brands with new direct-to-consumer engagement platforms. As connected packaging becomes mainstream, smart closures are poised to become a core innovation in both consumer goods and healthcare markets.

Expansion of Biopolymer-Based Closures

Sustainability goals are also fueling the expansion of biopolymer-based closures, offering an alternative to fossil-based plastics and addressing end-of-life challenges. Companies like CJ Biomaterials and Tech-Long International are scaling production of polyhydroxyalkanoate (PHA)-based bottle caps, which biodegrade in as little as six months, offering significant advantages in markets where recycling systems are underdeveloped. Academic research published in MDPI has underscored that biopolymers such as PLA and starch-based materials, though limited by moisture sensitivity and mechanical strength, are being enhanced with nanofiller reinforcements. These advancements improve durability and broaden the range of applications for biopolymer closures. Ongoing investment in research and commercialization is driving performance improvements, ensuring that biopolymer closures can compete with conventional plastics in functionality while providing superior environmental benefits. This shift positions biopolymers as a vital solution for companies seeking to reduce reliance on fossil-based resins and align with global circular economy goals.

Competitive Landscape: Leading Companies Are Driving Innovation and Sustainability in the Plastic Caps and Closures Market

The plastic caps and closures market is dominated by companies focusing on lightweighting, sustainability, and innovative sealing solutions, catering to food, beverage, and personal care segments globally.

Berry Global Group, Inc.: Championing Fully Recyclable Tethered Caps and Post-Consumer Resin Solutions

Berry Global manufactures a wide range of closures including dispensing, child-resistant, and screw-on caps. In March 2024, it launched fully recyclable tethered beverage caps in response to EU regulations. The company focuses on recyclable, reusable, and compostable packaging, with post-consumer recycled (PCR) resin integrated into its products to meet sustainability targets.

AptarGroup, Inc.: Pioneering Bio-Based and E-Commerce Ready Dispensing Closures for Global Brands

Aptar designs innovative closures, including disc-top, flip-top, and spray pump solutions for food, beverage, personal care, and pharmaceutical products. In April 2024, Aptar introduced bio-based dispensing closures, and its Future Disc Top offers a fully recyclable, e-commerce-ready solution. The company combines consumer insights with advanced R&D to create functional and sustainable closures.

Silgan Holdings Inc.: Expanding High-Barrier, Lightweight Closures for Food and Beverage Safety

Silgan’s Dispensing and Specialty Closures segment delivers innovative closures for food, beverage, and personal care products. In May 2024, it launched lightweight, high-barrier closures to improve freshness and reduce material usage. Silgan emphasizes customized, high-performance, and sustainable closures for diverse consumer needs.

Amcor plc: Balancing High-Barrier Protection with Lightweight and Recyclable Closure Designs

Amcor offers a broad portfolio of closures for beverages, food, and personal care with a focus on sustainability and innovation. The company aims for 100% recyclable or reusable packaging by 2025, integrating Genesis™ tamper-evident and lightweight closures to reduce material usage while maintaining product safety and freshness.

Closure Systems International (CSI): Driving Smart, Anti-Counterfeit, and Lightweight Closure Innovations

CSI specializes in closures for beverage bottles, including water, soft drinks, and dairy. In July 2024, it enhanced smart closure authentication with QR codes and introduced lightweight closures to minimize plastic waste. CSI focuses on high-performance, sustainable closures compatible with high-speed production lines, ensuring consumer safety, product freshness, and traceability.

Plastic Caps and Closures Market Share Insights, 2025-2034

Screw-On Caps Retain the Largest Market Share by Product Type in the Plastic Caps and Closures Industry

Screw-on caps hold a commanding 32% share of the plastic caps and closures market, reflecting their unmatched versatility across beverage, food, pharmaceutical, and personal care applications. Their simplicity, compatibility with high-speed filling lines, and cost-effectiveness make them the default closure solution for mass-market packaging. Threaded caps, closely related, reinforce this dominance by providing secure sealing across jars and bottles, underpinning the entire closure infrastructure. Dispensing closures are the fastest-growing category, driven by consumer demand for controlled dosing in personal care, condiments, and cleaning products, where pumps, flip-tops, and sprayers provide added convenience. Tamper-evident and child-resistant closures, though specialized, are critical compliance-driven categories, mandated in pharmaceuticals and household chemicals to ensure safety. Tethered caps are emerging as a regulation-driven disruptor, with the EU SUPD mandate accelerating their adoption in beverage packaging worldwide, forcing global producers to invest in new mold designs and production lines. Legacy categories like non-threaded press-on and crown caps are declining, but remain embedded in niche beverage cultures such as craft beer, preserving their cultural and market relevance.

Beverages Account for the Largest Market Share by End-Use Industry in Plastic Caps and Closures

The beverage sector represents 41% of demand in the plastic caps and closures industry, reflecting the massive global production of bottled water, carbonated soft drinks, juices, and functional beverages. This segment is highly volume-intensive, making lightweighting and tethered-cap compliance the central focus of innovation and regulation-driven redesigns. The food industry follows as a mature, stable contributor, where closures must preserve freshness and prevent leakage across edible oils, sauces, and condiments. Pharmaceuticals, while smaller in unit volume, represent a high-value, compliance-driven market, demanding tamper-evidence, child resistance, and compatibility with sensitive formulations, thus commanding premium closure pricing. Personal care and cosmetics remain a major driver of value-added closures, where pumps, sprayers, and customized caps enhance both brand aesthetics and consumer convenience. Household and industrial chemicals, along with automotive applications, highlight the functional and safety-critical role of closures, where chemical resistance, controlled dispensing, and durability are paramount. Collectively, the segmentation shows how beverages dominate by scale, while pharmaceuticals and personal care set the pace for premiumization and compliance-led innovation.

European Union Plastic Caps and Closures Market Shaped by Tethered Caps and PPWR Regulations

The European Union plastic caps and closures market is undergoing a major transformation due to strict sustainability and safety regulations. Since July 2024, the Single-Use Plastics Directive requires all beverage containers up to three liters to feature tethered caps, ensuring that closures remain attached to bottles and are collected with them during recycling. This regulation directly impacts the design of caps, requiring manufacturers to rethink material durability and functionality while enhancing recyclability. The implementation of the Packaging and Packaging Waste Regulation (PPWR) in February 2025 further intensifies the shift, as it enforces higher recyclability standards and pushes for reusable packaging across EU member states.

From August 2026, the EU will ban food packaging with PFAS concentrations exceeding regulatory thresholds, compelling closure manufacturers to adopt safer material alternatives. Companies are redesigning closures to meet the PPWR’s 70% recyclability target for 2030, investing in mono-material solutions and eco-friendly polymers. However, industry groups like the Alliance For Sustainable Packaging are advocating for a pause in certain PPWR provisions, warning of potential unintended environmental consequences. Despite debates, EU-based companies are at the forefront of advancing tethered, tamper-evident, and fully recyclable closure systems.

United States Plastic Caps and Closures Market Driven by Transparency and Smart Packaging

The United States plastic caps and closures market is being shaped by a mix of federal safety standards and state-level sustainability laws. The Food and Drug Administration (FDA) enforces stringent food-contact safety regulations, ensuring closures prevent contamination and preserve product integrity. Additionally, the Drug Supply Chain Security Act (DSCSA) requires serialization and tracking, which is influencing closure design for pharmaceutical applications.

Sustainability is a central trend. Leading manufacturers like Kraft Heinz and Berry Global have introduced closures with higher percentages of post-consumer recycled (PCR) content, including the first fully recyclable ketchup cap made from a single recyclable plastic type. Meanwhile, states such as California and Washington are tightening restrictions on single-use plastics, with Washington’s ESHB 1293 set to restrict sales of certain plastic packaging, including closures, from January 2026. On the innovation front, brands are incorporating smart packaging technologies such as QR codes and NFC tags into closures to boost consumer engagement and provide real-time sustainability and recycling information. The rise of e-commerce packaging has also increased demand for robust, tamper-proof dispensing closures that can withstand shipping while reducing environmental impact.

China Plastic Caps and Closures Market Accelerated by Regulations and Industrial Clusters

The China plastic caps and closures market is adapting to new regulatory measures and industrial innovation. A regulation effective June 2025 aims to minimize excessive packaging and promote recycled materials, with a strong focus on the booming e-commerce delivery sector. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are working in tandem to reduce plastic pollution and enhance sustainability by encouraging the adoption of biodegradable materials.

China’s positive list system for food-contact materials and updated adhesive standards that came into force in February 2025 are reshaping closure production for food-grade applications. Industrial clusters in Guangdong, Zhejiang, and Shandong are driving cost efficiencies through integrated supply chains, making China a hub for high-volume closure manufacturing. Domestic innovation is focused on producing closures that are not only compliant with stricter regulations but also cost-competitive, recyclable, and suitable for global exports.

India Plastic Caps and Closures Market Boosted by EPR and Sustainable Innovation

The India plastic caps and closures market is guided by strict policies under the Plastic Waste Management Rules (2016, amended 2022), which mandate Extended Producer Responsibility (EPR). Manufacturers and brand owners are required to manage the full lifecycle of their packaging, including the collection and recycling of plastic closures. The Swachh Bharat Abhiyan (Clean India Mission) is reinforcing these efforts, emphasizing waste segregation and sustainability at the community level.

The Food Safety and Standards Authority of India (FSSAI) is engaging with food and beverage companies to push adoption of biodegradable and recyclable closures, aligning with India’s push for eco-friendly alternatives. Local startups are making notable contributions: in September 2024, Dharaksha Ecosolutions secured funding to scale packaging solutions made from agricultural waste, showing how innovation is addressing both waste reduction and sustainable packaging. These developments, combined with India’s massive demand for bottled beverages and pharmaceuticals, make the country a growth hotspot for eco-friendly, tamper-evident, and cost-effective closure solutions.

United Kingdom Plastic Caps and Closures Market Influenced by PPT and Recycling Initiatives

The United Kingdom plastic caps and closures market is being transformed by regulatory and fiscal measures. The Plastic Packaging Tax (PPT), in effect since April 2022, taxes plastic packaging that does not contain at least 30% recycled content, incentivizing manufacturers to redesign closures with more recycled material. Data from HM Revenue and Customs (2024–2025) shows that 51% of plastic packaging manufactured or imported already meets the recycled threshold, signaling industry-wide compliance.

Additional support comes from the government’s Smart Sustainable Plastic Packaging (SSPP) Challenge, a £60 million funding program that has financed over 80 projects to improve recyclability and reduce plastic waste. Upcoming policies, including a deposit return scheme for plastic bottles, will directly influence closure designs to ensure compatibility with reverse vending and recycling systems. UK-based companies are also advancing single-material closure innovations, designed to streamline recycling and reduce waste from complex multi-material formats.

Japan Plastic Caps and Closures Market Focused on Food Safety and Recycling Innovation

The Japan plastic caps and closures market is shaped by new food safety and waste reduction frameworks. The country’s positive list system for food-contact materials, which came into effect on June 1, 2025, is redefining closure design by mandating compliance with strict material safety standards. This policy is particularly important for beverage and pharmaceutical applications, where closures must ensure both safety and performance.

Japan is also driving innovations in sustainability. Companies like Suntory are leading bottle-to-bottle recycling programs, producing closures and bottles from mechanically recycled PET. Suntory has also introduced label-free bottles, simplifying recycling preparation for consumers. Beyond recycling, Japan is investing in high-performance, eco-friendly plastics for closures that meet the dual needs of durability and compostability. With strong government backing for circular economy initiatives, the Japanese market is becoming a hub for next-generation closure designs that balance functionality, compliance, and sustainability.

Plastic Caps and Closures Market Report Scope

Plastic Caps and Closures Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$83.8 Billion

|

|

Market Size (2034)

|

$141.6 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Product Type (Screw-on Caps, Dispensing Closures, Child-resistant Closures, Tamper-evident Closures, Threaded Caps, Non-threaded Caps, Tethered Caps), By Raw Material (PP, HDPE, LDPE, PET, Recycled Content Plastics, Bio-based Plastics, Others), By Technology (Injection Molding, Compression Molding, Others), By End-Use Industry (Beverages, Food, Personal Care & Cosmetics, Household Chemicals, Pharmaceuticals, Industrial Chemicals, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, AptarGroup, Inc., Berry Global, Inc., Bericap Holding GmbH, Guala Closures Group, Closure Systems International (CSI), Corvaglia Group, Alpla-Werke Alwin Lehner GmbH & Co KG, Plastic Closures Limited, Silgan Holdings Inc., Bormioli Pharma S.p.A., Comar, United Caps, Crown Holdings Inc., RPC Group (Berry Global, Inc.)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Caps and Closures Market Segmentation

By Product Type

- Screw-on Caps

- Dispensing Closures

- Child-resistant Closures

- Tamper-evident Closures

- Threaded Caps

- Non-threaded Caps

- Tethered Caps

By Raw Material

- PP

- HDPE

- LDPE

- PET

- Recycled Content Plastics

- Bio-based Plastics

- Others

By Technology

- Injection Molding

- Compression Molding

- Others

By End-Use Industry

- Beverages

- Food

- Personal Care & Cosmetics

- Household Chemicals

- Pharmaceuticals

- Industrial Chemicals

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Caps and Closures Market

Amcor plc

- AptarGroup, Inc.

- Berry Global, Inc.

- Bericap Holding GmbH

- Guala Closures Group

- Closure Systems International (CSI)

- Corvaglia Group

- Alpla-Werke Alwin Lehner GmbH & Co KG

- Plastic Closures Limited

- Silgan Holdings Inc.

- Bormioli Pharma S.p.A.

- Comar

- United Caps

- Crown Holdings Inc.

- RPC Group (Berry Global, Inc.)

* List Not Exhaustive

Methodology

The research methodology for the Plastic Caps and Closures Market combines both primary and secondary approaches to ensure robust data reliability and precise market insights. Primary research involved detailed interviews with industry executives, packaging engineers, sustainability specialists, and supply chain stakeholders across key regions, capturing firsthand perspectives on design innovation, regulatory compliance, and material adoption. Secondary research encompassed comprehensive analysis of company annual reports, regulatory databases, patents, sustainability disclosures, industry journals, and verified trade publications. Advanced data triangulation was applied to validate market sizing, CAGR, and growth forecasts, integrating factors such as material trends (PP, HDPE, LDPE, PET, bio-based and recycled plastics), technological adoption (injection and compression molding), and regulatory frameworks including EU SUPD, UK PPT, and global EPR mandates. Both top-down and bottom-up approaches were employed to ensure accuracy in regional and product-level projections, while market dynamics were contextualized against consumer trends, sustainability-driven innovations, and competitive strategies. This rigorous, multi-layered methodology ensures that USDAnalytics delivers fact-based, actionable insights aligned with real-world industry developments in plastic caps and closures.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.