Biodegradable Paper & Plastic Packaging Market Overview (2025–2034)

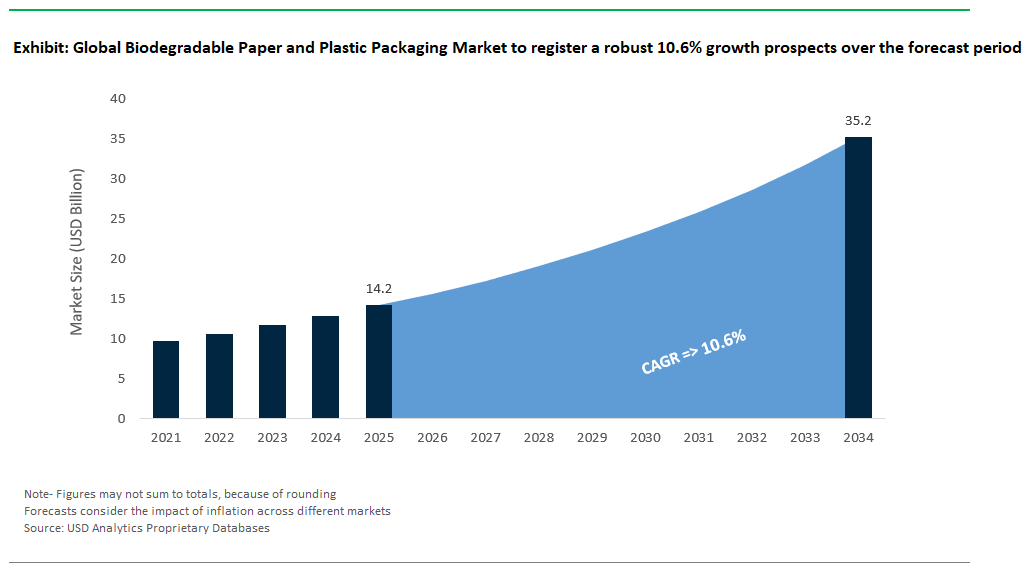

The Global Biodegradable Paper & Plastic Packaging Market is entering a dynamic phase of growth from 2025 through 2034, as regulatory mandates, corporate sustainability targets, and verified academic breakthroughs reshape packaging value chains worldwide. According to the latest industry announcements and policy developments, the market is projected to grow from USD 14.2 billion in 2025 to USD 35.2 billion by 2034, registering a strong CAGR of 10.6%. The momentum is led by a surge in investments from packaging producers, global brands, and material innovators, as well as a dramatic acceleration in the commercialization of eco-friendly packaging formats across food & beverages, e-commerce, retail, and healthcare sectors.

Drawing on rigorously sourced data from corporate disclosures, government policy shifts, and academic research, this report provides an authoritative evaluation of the global biodegradable paper & plastic packaging market By Biodegradable Paper Type (Corrugated Board, Boxboard / Cartonboard, Flexible Paper, Molded Pulp, Bagasse-based Packaging, Others), By Biodegradable Plastic Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS), Cellulose Acetate, Polycaprolactone (PCL), Others), By Packaging (Flexible Packaging, Rigid Packaging, Disposable Food Service Ware), By End-Use Industry (Food & Beverages, Beverages, Consumer Goods, Healthcare / Pharmaceuticals, E-commerce & Retail, Others).

This report delivers a comprehensive analysis of the global biodegradable paper & plastic packaging market, emphasizing breakthrough product launches, pioneering corporate projects, and the direct impact of policy reforms on packaging innovation. It investigates the evolution of biodegradable materials such as molded pulp, bagasse, PLA, PHA, and cellulose acetate across flexible and rigid packaging applications, alongside the rising use of disposable food service ware and sustainable retail packaging. The study examines how leading brands and packaging converters are scaling up next-generation materials, collaborating across supply chains, and driving adoption in food, beverage, healthcare, and retail industries. With verified segmentation and actionable insights, this report is an essential resource for manufacturers, investors, and policymakers committed to accelerating the mainstream adoption of biodegradable packaging worldwide.

Global Biodegradable Paper & Plastic Packaging Market Analysis: Corporate Initiatives & Policy Momentum

The global biodegradable paper and plastic packaging market is rapidly transforming, driven by intensifying regulatory mandates, surging brand sustainability commitments, and groundbreaking technological innovations. Once positioned largely as niche alternatives, biodegradable solutions are now scaling into mainstream packaging segments, offering high-performance, sustainable alternatives to conventional multi-material laminates and plastics. Recent developments across product launches, capacity expansions, partnerships, and regulatory shifts illustrate how the industry is converging around bio-based, compostable, and recyclable solutions that align with circular economy principles.

Innovative Product Launches: Expanding Functional Capabilities

Product innovation remains a primary growth engine, with manufacturers launching increasingly sophisticated solutions that combine environmental sustainability with critical packaging performance requirements.

- Mondi’s developments in mono-material barrier packaging, such as its recycle-ready solutions for flexible packaging made from PE or PP, exemplify how companies are creating highly protective yet recyclable alternatives to traditional multi-material plastic laminates.

- Amcor’s AmPrima™ Recycle-Ready Paper mailers, incorporating 30% bio-based PE coatings, cater to the booming e-commerce sector, where sustainability and durability must coexist.

- The partnership between BASF and Pulpex to co-develop biodegradable paper bottles for alcoholic beverages signals a leap forward in tackling hard-to-recycle liquid packaging applications traditionally reliant on multi-material plastics or glass.

Capacity Expansions: Highlighting Market Scalability

Substantial investments and capacity expansions indicate strong confidence in the market’s growth potential and the need to achieve cost efficiencies through scale.

- Stora Enso invested around €10 million in its Forshaga, Sweden site to expand production of sustainable barrier paperboard solutions, reflecting growing demand for eco-friendly food packaging in Europe.

- TotalEnergies Corbion operates a 75,000-tonne-per-year PLA plant in Thailand and plans further capacity in Europe, highlighting the rising need for biopolymer coatings used in flexible food wraps and beverage cartons.

- DS Smith, a leader in sustainable packaging, is optimizing paper-based solutions for a circular economy, including significant containerboard production at its Lucca, Italy paper mill.

Strategic Partnerships & M&A: Driving Biodegradable Packaging Innovation

Strategic partnerships and acquisitions are fueling rapid progress in biodegradable paper-plastic hybrid packaging solutions. Tetra Pak is developing paper-based barriers for beverage cartons, aiming to replace aluminum and synthetic polymers with renewable materials that significantly lower carbon footprints. Sealed Air is innovating compostable trays made from cellulose-based biopolymers, catering to the growing demand for sustainable foodservice packaging amid regulatory and brand pressures. Novamont’s MATER-BI® bioplastics support a wide range of biodegradable and compostable packaging, including products with potential marine-degradability, demonstrating the industry’s shift toward sustainable materials that perform across diverse end-of-life scenarios.

Regulations: Shaping Biodegradable Packaging Adoption

Regulatory policies worldwide are becoming a key driver of biodegradable packaging adoption. In the EU, the Packaging and Packaging Waste Regulation (PPWR) mandates compostable paper/plastic hybrids for applications like tea bags, fruit stickers, and lightweight carrier bags by February 2028, establishing clear compliance targets for brands and manufacturers. In the U.S., California’s SB 54 law requires all coated paper and paper-plastic hybrid packaging to be recyclable or compostable by 2032, reshaping the North American packaging landscape. Meanwhile, India’s ban on single-use plastic packaging is pushing retailers toward paper-based alternatives with suitable barrier coatings, spurring rapid changes across the sector.

Technological Advances: Improving Performance & Sustainability

Technological breakthroughs are solving key challenges that have limited the broader adoption of biodegradable packaging, such as moisture resistance, durability, and compostability. The Fraunhofer Institute is developing biobased coatings like bioORMOCER®, which provide excellent barriers against moisture and other elements for packaging use. At the same time, the University of Cambridge is researching enzyme-assisted degradation of PLA-based composites, aiming to enable faster and more efficient breakdown of plastic components, reducing their environmental footprint.

Commercial Adoption: Signaling Market Readiness

The growing commercial rollout of biodegradable paper-plastic hybrids demonstrates rising consumer acceptance and brand commitment to sustainability. McDonald’s switch to paper straws across European outlets highlights the foodservice industry’s move away from traditional plastics under consumer and regulatory pressure. Nestlé has introduced KitKat wrappers with high recycled plastic content and shifted products like Quality Street to paper packaging, showing how even high-volume, brand-critical products can transition to sustainable solutions without sacrificing quality or shelf appeal. Unilever’s launch of sustainable paperboard tubs for Ben & Jerry’s in the EU, featuring plant-based polyethylene coatings, underscores that biodegradable paper-plastic hybrids are viable for demanding applications like frozen desserts, where cold-chain stability and premium aesthetics are essential.

Market Dynamics in Biodegradable Paper & Plastic Packaging: Advances in Water-Soluble Films and Food-Saving Barriers

Trend: Water-Soluble Polymers Transforming Single-Dose Packaging

The global biodegradable paper and plastic packaging industry is evolving rapidly, owing to the rise of water-soluble polymers, revolutionizing single-dose and convenience packaging. Innovations like polyvinyl alcohol (PVA) and casein blends enable packaging that fully dissolves in water, eliminating microplastics and reducing environmental impact, a breakthrough highlighted by companies such as Lactips.

Demand for water-soluble packaging has surged across the detergent, food, and pharmaceutical sectors, driven by both sustainability goals and consumer preference for convenience. These materials reduce packaging weight compared to rigid plastics, lowering material use and logistics costs. Major brands like Unilever are prioritizing such lightweighting solutions as part of broader sustainability strategies.

Commercial adoption is booming. In detergents, pods from brands like Tide (P&G) and Seventh Generation have become mainstream, demonstrating consumer enthusiasm for convenient, water-soluble formats. The combination of environmental benefits, supply chain efficiency, and strong brand engagement is positioning water-soluble polymers as a game changer in single-dose packaging for both paper and plastic applications.

Opportunity: Nanocellulose Barriers Combatting Food Waste in Flexible Packaging

A significant growth opportunity in the global biodegradable paper and plastic packaging market lies in nanocellulose barrier coatings for flexible food packaging. This technology directly addresses the global food waste crisis, where nearly one-third of food produced is lost or wasted, often due to inadequate packaging, as reported by the FAO.

Research from Fraunhofer UMSICHT shows that nanocellulose offers far superior barrier properties compared to some conventional films and can significantly extend the shelf life of fresh produce, helping reduce spoilage. Importantly, these coatings are biodegradable and can be home-compostable, aligning with the growing demand for fully circular packaging and certifications like TÜV OK Compost.

Scaling prospects are strong. AI-optimized manufacturing is expected to lower production costs and increase efficiency, while global capacity for nanocellulose barriers is forecast to grow rapidly in response to rising demand. Potential food waste reduction is substantial, with estimates suggesting savings could rise from 1.8 million tonnes annually today to 22 million tonnes by 2030, driven by policies like the EU Farm-to-Fork Strategy. Strategic regions leading this innovation include Europe, supported by Horizon Europe funding, Japan, with companies like Oji Holdings investing in nanocellulose development, and the U.S. through programs like USDA BioPreferred promoting bio-based products.

Competitive Landscape: Leading Players in Biodegradable Paper & Plastic Packaging

The global biodegradable paper and plastic packaging market is growing rapidly in 2024, driven by escalating environmental regulations, brand commitments to sustainable packaging, and shifting consumer preferences. Biodegradable plastics such as PLA, PHA, PBAT blends, and starch-based materials are increasingly replacing traditional plastics in flexible and rigid applications, while biodegradable paper solutions are gaining ground in e-commerce, food service, and retail packaging. Leading companies are scaling capacity, launching innovative materials, and forming strategic partnerships to capture market share in this evolving landscape where sustainability and performance are equally crucial.

NatureWorks: Leading PLA Production for Sustainable Packaging

NatureWorks (USA) NatureWorks continues to lead the biodegradable plastics sector with its robust PLA production capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost regional capacity. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability, integrating Ingeo™ PLA biopolymer in the rigid capsule body, nonwoven filter, and multi-layer top lidding. Further expanding its portfolio, in February 2025, the company launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films. These initiatives underscore NatureWorks’ commitment to expanding PLA’s role beyond traditional single-use products into durable goods and complex packaging solutions.

TotalEnergies Corbion: Innovating High-Performance PLA Solutions

TotalEnergies Corbion (Netherlands) TotalEnergies Corbion has established itself as a key innovator in high-performance PLA, operating a 75,000 TPA facility in Thailand under its Luminy® brand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion and a drive to meet growing global demand. TotalEnergies Corbion's focus on technical enhancements positions it as a pivotal supplier in applications where both sustainability and functional performance are critical.

Novamont: Dominant in Starch-Based Biodegradable Plastics

Novamont (Italy) Novamont remains a dominant force in starch-based biodegradable plastics through its Mater-Bi® product line. As of October 2019, Novamont increased its Mater-Bi® compostable bioplastics production capacity by 40,000 tonnes at the Mater-Biopolymer plant in Patrica, Frosinone, complementing the existing 110,000 tonnes capacity at their Terni site. Following its acquisition of BioBag Group in 2023, Novamont significantly expanded its influence in the compostable packaging market. Novamont’s leadership in creating cost-effective, high-performance compostable solutions makes it a cornerstone of the European biodegradable packaging sector, particularly in flexible films and compostable bags for food, retail, and agricultural applications. However, recent developments from June 2025 indicate the Italian Competition Authority imposed fines totaling over €32 million on Novamont and its parent company Eni for abuse of a dominant position in the national markets for bioplastic raw materials used in bags.

BASF: Strengthening Biodegradable Plastics with PBAT/PLA Blends

BASF (Germany) BASF continues to strengthen its position in biodegradable plastics through its ecovio® PBAT/PLA blends, widely used in certified compostable bags and flexible packaging. The PBAT market was estimated at USD 1.74 billion in 2024, with Asia Pacific accounting for the largest revenue share. In February 2024, BASF launched its ChemCycling™ initiative in the US, converting plastic waste into new ISCC+ certified advanced recycled building blocks, further aligning its strategy with circular economy principles. BASF continues to demonstrate how global reach and advanced chemical innovation are propelling bioplastics into diverse and high-demand markets worldwide. Looking ahead to K 2025 (October 2025), BASF plans to showcase its commitment to #OurPlasticsJourney, highlighting a reduced Product Carbon Footprint (rPCF) portfolio and the use of biomass balance approach for biopolymers like ecovio® and ecoflex® BMB, further reinforcing its sustainable packaging solutions.

DS Smith: Innovating in Biodegradable Paper Packaging

DS Smith (UK) DS Smith is emerging as a significant player in biodegradable paper packaging, known for its molded fiber innovations tailored for e-commerce and retail applications. The company highlights its focus on "Plastic Replacement" within its packaging solutions. DS Smith's research underlines the positive impact of switching to fiber-based alternatives in e-commerce clothing packaging and the potential to replace unnecessary plastics in supermarket food and drink packaging. DS Smith reinforces its commitment to sustainable packaging and meeting the growing demand for plastic-free solutions in shipping and logistics.

Huhtamaki: Advancing Biodegradable Paper-Based Food Service Packaging

Huhtamaki (Finland) is at the forefront of biodegradable paper-based food service packaging with its offerings of paper cups and lids for various beverages. In January 2025, Huhtamaki India hosted the presentation of "Design for Recyclability Guidelines for Films & Flexible Packaging" as part of the CII-India Plastics Pact's (IPP) initiative, highlighting its commitment to driving a circular economy in India's flexible packaging sector. Huhtamaki's focus on innovative sustainable solutions, including its recyclable single-coated paper cups 'ProDairy' (February 2025), which reduce plastic content while maintaining performance, solidifies its role as a leader in the biodegradable paper packaging segment, catering to food service and retail industries worldwide.

Biodegradable Paper & Plastic Packaging Market Share Analysis

By Biodegradable Paper Type: Corrugated Board Leads Market, Bagasse-Based Packaging Grows Fastest

In 2025, corrugated board holds a 31.8% market share, maintaining its dominance as the preferred solution for e-commerce and retail packaging due to its strength, recyclability, and supply chain efficiency. Bagasse-based packaging is the fastest-growing segment, rapidly gaining adoption in the food service sector for disposable trays, plates, and clamshells as brands and restaurants seek plant-based, compostable alternatives. Molded pulp is also seeing increased demand in egg cartons and protective packaging for electronics, reflecting broader interest in sustainable, fiber-based formats.

.png)

By Biodegradable Plastic Type: PLA Dominates, PHA Delivers the Highest Growth Rate

Polyhydroxyalkanoates (PHA) deliver the fastest growth with a CAGR of 11.3%, driven by their marine-degradable properties and suitability for specialty packaging in food and personal care. PBAT continues to be widely used in flexible films, particularly in applications that require both compostability and flexibility. Polylactic acid (PLA) leads the biodegradable plastics segment in 2025, fueled by its widespread use in rigid food packaging and containers for perishable goods.

By Packaging Format: Flexible Packaging Leads Adoption, Disposable Food Service Ware Expands Most Rapidly

Flexible packaging dominates the market, accounting for 48.7% of total demand in 2025, supported by ongoing consumer preference for pouches, wraps, and resealable solutions across food, snack, and personal care sectors. Disposable food service ware is the fastest-growing format, as regulatory bans on single-use plastics drive adoption of biodegradable straws, cutlery, and takeaway containers. Rigid packaging remains strong, particularly in bottles, trays, and clamshells for food and consumer goods.

China Scaling Biodegradable Packaging for Food Delivery, Agriculture, and Retail

China continues to dominate the global biodegradable paper and plastic packaging industry, driven by substantial R&D investment, industrial expansion, and government mandates. The country invested more than $1.2 billion in bioplastics R&D between 2021 and 2025 as part of its 14th Five-Year Plan, fueling breakthroughs in PLA, PBAT, and PBS technologies. Chinese companies are leading the transition to sustainable packaging across key sectors: PLA and PBAT-based cutlery and bags now serve the booming food delivery industry, while PBS films are widely adopted for agricultural mulch applications. 2024 saw the rollout of Kingfa’s PBAT shopping bags for Alibaba and the massive expansion of BBCA Biochemical’s PLA production to reach an estimated capacity of over 1 million tons per year by early 2025, strengthening supply chains for both domestic and export markets. Recent industry news includes Sinopec’s partnership with Mengniu Dairy to supply biodegradable milk bottles, signaling rapid adoption by top consumer brands. In 2025, several provinces are further tightening "plastic ban" regulations, leading to a noticeable surge in demand for certified biodegradable alternatives for single-use items in retail and foodservice. Additionally, new state-backed research programs are focusing on developing advanced biodegradable materials for smart packaging and e-commerce logistics, aiming for broader market penetration. China’s innovation ecosystem, regulatory discipline, and manufacturing scale continue to set global benchmarks for cost-effective, certified biodegradable packaging solutions.

United States Accelerating Biodegradable Packaging with Innovation, Policy, and Capacity Scale-Up

The United States is rapidly expanding its role in the global biodegradable packaging industry, blending innovation, public investment, and regulatory ambition. The Department of Energy’s $118 million funding for PHA and PLA technology underscores a national push for compostable and marine-degradable packaging. Major market applications include NatureWorks’ PLA compostable coffee pods and Danimer’s PHA-based straws, which are now being adopted by major retailers and QSRs such as Starbucks. Breakthrough product launches like TIPA Corp’s home-compostable snack wrappers in 2023 and the commissioning of Danimer Scientific’s new 30,000-ton PHA plant in Kentucky demonstrate the move from pilot to industrial scale. Policy is also driving adoption: California’s SB 54 law requires all packaging in the state to be 100% recyclable or compostable by 2032, establishing a new national and international benchmark. In 2025, several major U.S. consumer product companies are anticipated to announce significant increases in their use of bioplastic packaging, driven by both brand sustainability commitments and the evolving state-level regulations. There's also a heightened focus on developing advanced sorting and composting infrastructure to support the large-scale adoption of certified biodegradable packaging, with federal grants targeting these initiatives. The United States’ blend of investment, startup innovation, and policy momentum is rapidly transforming both supply and demand for biodegradable paper and plastic packaging.

Germany Advancing Compostable Packaging through Bioeconomy Funding and Regulatory Leadership

Germany continues to advance the biodegradable packaging sector with world-class research, generous government funding, and rigorous standards. The federal government’s €3.6 billion bioeconomy investment powers leading-edge projects across materials and applications. BASF’s “Ecoflex” PBAT is a cornerstone for compostable films, while German innovation has expanded the use of PLA blends in automotive and specialty applications. Südzucker’s 2024 launch of sugar-based biodegradable films highlights progress in food-safe, sustainable alternatives. German manufacturers are also expanding their global reach. Novamont, for example, doubled Mater-Bi production in 2023 to meet rising EU demand. The EU’s Packaging and Packaging Waste Regulation (PPWR), which became legally binding in February 2025 and will apply from August 2026, includes mandates for specific compostable packaging (e.g., fresh produce stickers, tea/coffee bags), prompting widespread industry reform and innovation. BASF’s launch of compostable coffee capsules with TÜV certification signals the country’s ongoing commitment to both convenience and sustainability. For 2025, German packaging companies are actively re-designing their product portfolios to comply with the PPWR's upcoming recycled content and recyclability targets, leading to increased adoption of advanced bioplastics and bio-coated paper solutions. Furthermore, collaborative projects between German research institutes and industry players are intensifying, focusing on developing next-generation biodegradable coatings for paper and cardboard packaging to enhance their barrier properties for food applications. Germany’s combination of technical leadership, investment, and policy rigor cements its status as Europe’s benchmark market for sustainable paper and plastic packaging.

Italy Scaling Compostable Bioplastics for Food, Cosmetics, and Furniture Packaging

Italy is a global pioneer in compostable bioplastic packaging, supported by strategic investment, innovative applications, and policy mandates. Novamont has invested over €350 million in R&D, supplying mandated compostable fruit and vegetable bags for retail and developing Bio-on’s PHA-based packaging for luxury cosmetics. Italy is also expanding the scope of bioplastics with breakthrough launches, such as IKEA’s bioplastic furniture collaboration with Novamont in 2024 and the opening of TotalEnergies Corbion’s 100,000-ton PLA plant in Thailand, which serves global demand, including Italy. These developments, paired with a well-developed composting infrastructure, enable Italy to support large-scale deployment of compostable packaging across sectors. National regulations, such as mandatory compostable bags for fresh produce, continue to drive the transition toward certified biodegradable packaging, positioning Italy as a European leader in the food, retail, and consumer goods space. In 2025, regional authorities in Italy are expected to launch new incentive programs for businesses to adopt certified compostable packaging for a wider range of food service applications, building on existing successes. There's also a growing trend of Italian organic food producers actively marketing their products in home-compostable bioplastic packaging, further boosting consumer awareness and adoption.

Netherlands Driving Biodegradable Packaging Adoption with Plant-Based Innovations and EU Policy

The Netherlands is a key hub for advanced biodegradable packaging solutions in Europe, supported by strong R&D and a favorable policy environment. With €250 million in EU Horizon grants fueling innovation, Dutch companies are at the forefront of plant-based alternatives like Avantium’s PEF, now piloted in beverage bottles for Coca-Cola in 2024. Corbion’s PLA is widely adopted for flexible food packaging, meeting both brand and regulatory needs. The country’s leadership in renewable packaging is amplified by the EU Single-Use Plastics Directive, which has accelerated PEF and PLA adoption across beverage, foodservice, and personal care sectors. In 2025, the Netherlands is focusing on developing robust circular systems for advanced bioplastics, including pilots for chemical recycling of PEF and comprehensive collection schemes for compostable packaging in urban areas. Several new collaborative projects between Dutch startups and established packaging companies are launching, aiming to bring innovative bio-based barrier coatings and fully biodegradable flexible films to market. The Netherlands’ integration of technology, brand partnerships, and policy support positions it as a European benchmark for plant-based and biodegradable packaging.

Thailand Leading Biodegradable Packaging Exports for Food, Retail, and Agriculture

Thailand is rising as a major global producer and exporter of biodegradable paper and plastic packaging, investing $1 billion through its BCG (Bio-Circular-Green) Economy Fund. Local manufacturers like PTT MCC are providing PLA for global brands such as Unilever, while innovative applications like compostable rice-starch bags are rapidly gaining ground. Thailand is expanding supply through new capacity: Total Corbion PLA continues to operate its large-scale PLA plant (75,000 tons/year), further solidifying Thailand’s export leadership. In 2024, SCG Packaging launched sugarcane-based pulp trays, offering new sustainable solutions for food packaging and logistics. For 2025, Thailand is actively promoting its capabilities as a bioplastics manufacturing hub to attract further foreign investment, particularly from Japanese and European companies seeking diversified supply chains. The government is also expected to introduce new standards for marine-biodegradable plastics to support sustainable aquaculture and fishing industries, driving innovation in related packaging and equipment. Thailand’s commitment to R&D, capacity growth, and affordable pricing ensures continued dominance in the Asia-Pacific sustainable packaging market.

Brazil Scaling Sugarcane-Based Biodegradable Packaging for Cosmetics and Amazon Conservation

Brazil is driving the adoption of biodegradable packaging in South America, powered by significant investments by Braskem for sugarcane-based polyethylene (bio-PE), including strategic partnerships to expand global bio-polyolefin capacity. Partnerships with L’Oréal for sustainable cosmetic jars and a focus on biodegradable alternatives for Amazon-region logistics and packaging mark Brazil’s push toward both market leadership and conservation. National policies such as the “Plastic Free Amazon” law are creating incentives and mandates for rapid adoption, positioning Brazil as a key innovator and regional exporter in the global biodegradable packaging industry. In 2025, Braskem is anticipated to announce further commercial agreements for its bio-PE in various packaging applications, including food and beverage. There's also a growing domestic market demand for bio-based packaging driven by consumer awareness and local sustainability campaigns, particularly in major urban centers, pushing retailers to adopt more eco-friendly options.

India Building Biodegradable Packaging Capacity for Food, Retail, and E-Commerce

India’s biodegradable paper and plastic packaging market is experiencing robust growth, supported by $150 million in R&D investments under the “Make in India” initiative. Key players like Reliance are commercializing bio-PET for food packaging, while starch-based pouches address the demands of e-commerce and retail. The upcoming 50,000-ton PLA plant from Zhejiang Hisun and Indian Oil, slated for completion and initial operations in late 2025, will significantly boost domestic capacity and reduce import reliance. India’s government has rolled out new EPR (Extended Producer Responsibility) rules to incentivize brand adoption of certified biodegradable packaging, accelerating the market’s transition toward more sustainable materials. For 2025, the Indian government is expected to issue clearer guidelines and standards for industrial and home composting of biodegradable packaging, aiming to streamline waste management. Major e-commerce players are increasing their investment in sustainable logistics, including expanded use of biodegradable and compostable packaging for last-mile delivery, particularly in Tier 1 and Tier 2 cities. India’s scale, policy incentives, and growing infrastructure make it a promising player in the global shift to compostable and biodegradable packaging.

Biodegradable Paper & Plastic Packaging Market Report Scope

Biodegradable Paper & Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.2 Billion

|

|

Market Size (2034)

|

$35.2 Billion

|

|

Market Growth Rate

|

10.6%

|

|

Segments

|

By Biodegradable Paper Type (Corrugated Board, Boxboard / Cartonboard, Flexible Paper, Molded Pulp, Bagasse-based Packaging, Others), By Biodegradable Plastic Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS), Cellulose Acetate, Polycaprolactone (PCL), Others), By Packaging (Flexible Packaging, Rigid Packaging, Disposable Food Service Ware), By End-Use Industry (Food & Beverages, Beverages, Consumer Goods, Healthcare / Pharmaceuticals, E-commerce & Retail, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor Plc (Switzerland/Australia), Mondi Group (Austria/UK), International Paper Company (U.S.), Tetra Pak International SA (Switzerland), WestRock Company (U.S.), Stora Enso (Finland/Sweden), Smurfit Kappa Group Plc (Ireland), DS Smith Plc (UK), Novamont S.p.A. (Italy), BASF SE (Germany), NatureWorks LLC (U.S.), Danimer Scientific (U.S.), TotalEnergies Corbion (Netherlands), Braskem S.A. (Brazil), Kruger Inc. (Canada), Riverside Paper Co. Inc. (U.S.), SmartSolve Industries (U.S.), Ultra Green Sustainable Packaging (U.S.), Özsoy Plastik (Turkey), Hosgör Plastik (Turkey), Eurocell S.r.l (Italy), SEE (Sealed Air Corporation) (U.S.), Alpla Group (Austria), Constantia Flexibles (Austria), Huhtamaki Oyj (Finland), Karat Packaging Inc. (U.S.), Pakka (Switzerland), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Paper and Plastic Packaging Market Segmentation

By Biodegradable Paper Type

- Corrugated Board

- Boxboard / Cartonboard

- Flexible Paper

- Molded Pulp

- Bagasse-based Packaging

- Others

By Biodegradable Plastic Type

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Starch Blends / Thermoplastic Starch (TPS)

- Polybutylene Succinate (PBS)

- Cellulose Acetate

- Polycaprolactone (PCL)

- Others

By Packaging

- Flexible Packaging

- Rigid Packaging

- Disposable Food Service Ware

By End-Use Industry

- Food & Beverages

- Fresh Produce

- Dairy & Dairy Alternatives

- Bakery & Confectionery

- Meat, Poultry & Seafood

- Ready-to-Eat Meals & Food Service

- Beverages

- Consumer Goods

- Healthcare / Pharmaceuticals

- E-commerce & Retail

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Paper and Plastic Packaging Market

- Amcor Plc (Switzerland/Australia)

- Mondi Group (Austria/UK)

- International Paper Company (US)

- Tetra Pak International SA (Switzerland)

- WestRock Company (US)

- Stora Enso (Finland/Sweden)

- Smurfit Kappa Group Plc (Ireland)

- DS Smith Plc (UK)

- Novamont S.p.A. (Italy)

- BASF SE (Germany)

- NatureWorks LLC (US)

- Danimer Scientific (US)

- TotalEnergies Corbion (Netherlands)

- Braskem S.A. (Brazil)

- Kruger Inc. (Canada)

- Riverside Paper Co. Inc. (US)

- SmartSolve Industries (US)

- Ultra Green Sustainable Packaging (US)

- Özsoy Plastik (Turkey)

- Hosgör Plastik (Turkey)

- Eurocell S.r.l (Italy)

- SEE (Sealed Air Corporation) (US)

- Alpla Group (Austria)

- Constantia Flexibles (Austria)

- Huhtamaki Oyj (Finland)

- Karat Packaging Inc. (US)

- Pakka (Switzerland)

* List Not Exhaustive

Methodology

The Global Biodegradable Paper & Plastic Packaging Market 2025–2034 report is developed using a rigorous and multi-pronged research methodology that integrates both primary and secondary research. Primary research encompasses in-depth interviews with industry leaders—including packaging converters, biopolymer manufacturers, material science researchers, and regulatory experts—to capture first-hand insights on technology adoption, market challenges, and regional developments. Secondary research draws on company annual reports, patent analyses, government policy documents, peer-reviewed scientific publications, and reputable industry journals to ensure data robustness and context. Market sizing and forecast models apply a combination of top-down and bottom-up approaches, considering capacity expansions, end-use industry consumption patterns, and regulatory-driven demand shifts across over 25 countries. All data points undergo triangulation and validation through proprietary intelligence from USDAnalytics, ensuring the report delivers precise, actionable insights. Advanced analytics and scenario modeling further support the forecast horizon, enabling stakeholders to anticipate both baseline and disruptive growth trajectories in the biodegradable paper and plastic packaging market.

Research Coverage

- Geographic Scope: Global coverage spanning North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with detailed country-level insights across 25+ countries.

- Segmentation: Comprehensive segmentation by Biodegradable Paper Type (Corrugated Board, Boxboard/Cartonboard, Flexible Paper, Molded Pulp, Bagasse-based Packaging, Others), Biodegradable Plastic Type (PLA, PHA, PBAT, TPS, PBS, Cellulose Acetate, PCL, Others), Packaging Format (Flexible Packaging, Rigid Packaging, Disposable Food Service Ware), and End-Use Industry (Food & Beverages, Beverages, Consumer Goods, Healthcare/Pharmaceuticals, E-commerce & Retail, Others).

- Competitive Landscape: Profiles and strategic developments of more than 25 leading players in the biodegradable paper and plastic packaging markets.

- Key Themes: Innovations in paper-plastic hybrid solutions, impact of emerging regulations (e.g., EU PPWR, US SB 54), supply chain integration, material cost trends, and technology breakthroughs such as nanocellulose barriers and water-soluble polymers.

- Market Dynamics: Analysis of drivers, challenges, regional trends, technological evolution, sustainability initiatives, and investment activity shaping market growth through 2034.

- Historical Data (2021–2024) and Forecast Data (2025–2034)

Deliverables

- Comprehensive Market Report (PDF, Excel): Including market data tables, charts, narrative analysis, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-Level Revenue and Volume Projections (2025–2034)

- Competitive Benchmarking and Detailed Company Profiles

- Regulatory Framework Analysis and Emerging Policy Tracker

- Executive Summary and Key Analyst Takeaways

- Post-Sale Analyst Support for Custom Queries

Table of Contents

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Biodegradable Paper & Plastic Packaging Market Overview (2025–2034)

2.1. Introduction to Biodegradable Paper & Plastic Packaging

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Current Market Size (2025)

2.2.2. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Market Drivers

2.3.1. Regulatory Mandates and Policy Developments

2.3.2. Corporate Sustainability Targets and Brand Commitments

2.3.3. Advancements in Material Science and Production Technologies

2.4. Market Challenges and Restraints

3. Global Biodegradable Paper & Plastic Packaging Market Analysis: Corporate Initiatives & Policy Momentum

3.1. Innovative Product Launches: Expanding Functional Capabilities

3.1.1. Mono-Material Barrier Packaging (Mondi)

3.1.2. Recycle-Ready Paper Mailers with Bio-Based Coatings (Amcor AmPrima™)

3.1.3. Biodegradable Paper Bottles for Alcoholic Beverages (BASF & Pulpex Partnership)

3.2. Capacity Expansions: Highlighting Market Scalability

3.2.1. Stora Enso: Investment in Sustainable Barrier Paperboard

3.2.2. TotalEnergies Corbion: PLA Production Expansion

3.2.3. DS Smith: Optimizing Paper-Based Solutions

3.3. Strategic Partnerships & M&A: Driving Biodegradable Packaging Innovation

3.3.1. Tetra Pak: Developing Paper-Based Barriers for Beverage Cartons

3.3.2. Sealed Air: Innovating Compostable Trays from Cellulose-Based Biopolymers

3.3.3. Novamont: MATER-BI® Bioplastics for Biodegradable and Compostable Packaging

3.4. Regulations: Shaping Biodegradable Packaging Adoption

3.4.1. EU Packaging and Packaging Waste Regulation (PPWR) Mandates

3.4.2. U.S. California’s SB 54 Law for Packaging Recyclability/Compostability

3.4.3. India’s Ban on Single-Use Plastic Packaging

3.5. Technological Advances: Improving Performance & Sustainability

3.5.1. Biobased Barrier Coatings (Fraunhofer Institute – bioORMOCER®)

3.5.2. Enzyme-Assisted Degradation of PLA-Based Composites (University of Cambridge)

3.6. Commercial Adoption: Signaling Market Readiness

3.6.1. McDonald’s Switch to Paper Straws

3.6.2. Nestlé’s Transition to Sustainable Packaging (KitKat, Quality Street)

3.6.3. Unilever’s Sustainable Paperboard Tubs (Ben & Jerry’s)

4. Market Dynamics in Biodegradable Paper & Plastic Packaging: Advances in Water-Soluble Films and Food-Saving Barriers

4.1. Trend: Water-Soluble Polymers Transforming Single-Dose Packaging

4.1.1. Innovations in PVA and Casein Blends

4.1.2. Surging Demand Across Detergent, Food, and Pharmaceutical Sectors

4.1.3. Commercial Adoption and Brand Prioritization

4.2. Opportunity: Nanocellulose Barriers Combatting Food Waste in Flexible Packaging

4.2.1. Addressing Global Food Waste Crisis with Enhanced Barrier Properties

4.2.2. Biodegradability and Home-Compostability of Nanocellulose Coatings

4.2.3. Scaling Prospects and Regional Leadership in Innovation

5. Competitive Landscape: Leading Players in Biodegradable Paper & Plastic Packaging

5.1. Overview of Competitive Environment

5.2. Company Profiles & Strategies (Overview)

5.2.1. NatureWorks: Leading PLA Production for Sustainable Packaging

5.2.2. TotalEnergies Corbion: Innovating High-Performance PLA Solutions

5.2.3. Novamont: Dominant in Starch-Based Biodegradable Plastics

5.2.4. BASF: Strengthening Biodegradable Plastics with PBAT/PLA Blends

5.2.5. DS Smith: Innovating in Biodegradable Paper Packaging

5.2.6. Huhtamaki: Advancing Biodegradable Paper-Based Food Service Packaging

5.2.7. Other Key Players (Detailed profiles in Chapter 9)

6. Biodegradable Paper & Plastic Packaging Market Segmentation Analysis

6.1. By Biodegradable Paper Type

6.1.1. Corrugated Board

6.1.2. Boxboard / Cartonboard

6.1.3. Flexible Paper

6.1.4. Molded Pulp

6.1.5. Bagasse-based Packaging

6.1.6. Others

6.2. By Biodegradable Plastic Type

6.2.1. Polylactic Acid (PLA)

6.2.2. Polyhydroxyalkanoates (PHA)

6.2.3. Polybutylene Adipate Terephthalate (PBAT)

6.2.4. Starch Blends / Thermoplastic Starch (TPS)

6.2.5. Polybutylene Succinate (PBS)

6.2.6. Cellulose Acetate

6.2.7. Polycaprolactone (PCL)

6.2.8. Others

6.3. By Packaging

6.3.1. Flexible Packaging

6.3.2. Rigid Packaging

6.3.3. Disposable Food Service Ware

6.4. By End-Use Industry

6.4.1. Food & Beverages

6.4.1.1. Fresh Produce

6.4.1.2. Dairy & Dairy Alternatives

6.4.1.3. Bakery & Confectionery

6.4.1.4. Other Food & Beverages

6.4.2. Beverages

6.4.3. Consumer Goods

6.4.4. Healthcare / Pharmaceuticals

6.4.5. E-commerce & Retail

6.4.6. Others

7. Geographic Analysis: Biodegradable Paper & Plastic Packaging Market Outlook by Country (2021-2034)

7.1. Asia Pacific

7.1.1. China: Scaling Biodegradable Packaging for Food Delivery, Agriculture, and Retail

7.1.2. Japan: Driving Innovation in High-Performance Biopolymer Films

7.1.3. India: Building Biodegradable Packaging Capacity for Food, Retail, and E-Commerce

7.1.4. South Korea: Advancing Sustainable Biopolymer Packaging Solutions

7.1.5. Thailand: Leading Biodegradable Packaging Exports for Food, Retail, and Agriculture

7.1.6. Rest of Asia Pacific

7.2. Europe

7.2.1. Germany: Advancing Compostable Packaging through Bioeconomy Funding and Regulatory Leadership

7.2.2. Italy: Scaling Compostable Bioplastics for Food, Cosmetics, and Furniture Packaging

7.2.3. Netherlands: Driving Biodegradable Packaging Adoption with Plant-Based Innovations and EU Policy

7.2.4. UK: Strong Growth Driven by Sustainable Packaging Demand

7.2.5. France: Increasing Adoption Due to Stringent Regulations

7.2.6. Spain: Significant Market Expansion Led by Polysaccharide and PLA Adoption

7.2.7. Rest of Europe

7.3. North America

7.3.1. United States: Accelerating Biodegradable Packaging with Innovation, Policy, and Capacity Scale-Up

7.3.2. Canada: Steady Growth Driven by Sustainable Packaging Demand

7.3.3. Mexico: Rapid Expansion Fueled by Sustainable Packaging and F&B Sector Demand

7.4. South America

7.4.1. Brazil: Scaling Sugarcane-Based Biodegradable Packaging for Cosmetics and Amazon Conservation

7.4.2. Argentina: Emerging Market with Potential in Flexible Packaging

7.4.3. Rest of South America

7.5. Middle East & Africa

7.5.1. Saudi Arabia: Developing Market for Lignin-based Biopolymers

7.5.2. UAE: Rapidly Growing Demand for Sustainable Packaging

7.5.3. Rest of Middle East & Africa

8. Biodegradable Paper & Plastic Packaging Market Size Outlook by Region (2025-2034)

8.1. North America Biodegradable Paper & Plastic Packaging Market Size Outlook to 2034

8.1.1. By Biodegradable Paper Type

8.1.2. By Biodegradable Plastic Type

8.1.3. By Packaging

8.1.4. By End-Use Industry

8.2. Europe Biodegradable Paper & Plastic Packaging Market Size Outlook to 2034

8.2.1. By Biodegradable Paper Type

8.2.2. By Biodegradable Plastic Type

8.2.3. By Packaging

8.2.4. By End-Use Industry

8.3. Asia Pacific Biodegradable Paper & Plastic Packaging Market Size Outlook to 2034

8.3.1. By Biodegradable Paper Type

8.3.2. By Biodegradable Plastic Type

8.3.3. By Packaging

8.3.4. By End-Use Industry

8.4. South America Biodegradable Paper & Plastic Packaging Market Size Outlook to 2034

8.4.1. By Biodegradable Paper Type

8.4.2. By Biodegradable Plastic Type

8.4.3. By Packaging

8.4.4. By End-Use Industry

8.5. Middle East & Africa Biodegradable Paper & Plastic Packaging Market Size Outlook to 2034

8.5.1. By Biodegradable Paper Type

8.5.2. By Biodegradable Plastic Type

8.5.3. By Packaging

8.5.4. By End-Use Industry

9. Company Profiles: Leading Players in the Biodegradable Paper & Plastic Packaging Market

9.1. NatureWorks

9.2. TotalEnergies Corbion

9.3. Novamont

9.4. BASF

9.5. DS Smith

9.6. Huhtamaki

9.7. Mondi

9.8. Amcor

9.9. TIPA Corp

9.10. Stora Enso

9.11. Sealed Air

9.12. Kingfa

9.13. BBCA Biochemical

9.14. PTT MCC Biochem

9.15. Braskem

9.16. Reliance

9.17. Others (as applicable)

10. Research Methodology

10.1. Data Collection Approach (Primary & Secondary Research)

10.2. Market Sizing and Forecasting Model

10.3. Data Validation and Triangulation

10.4. Proprietary Intelligence & Tools (USDAnalytics)

11. Report Scope & Deliverables

11.1. Report Scope

11.2. Deliverables

12. Disclaimer