Biodegradable Paper Packaging Materials Market Overview (2025–2034)

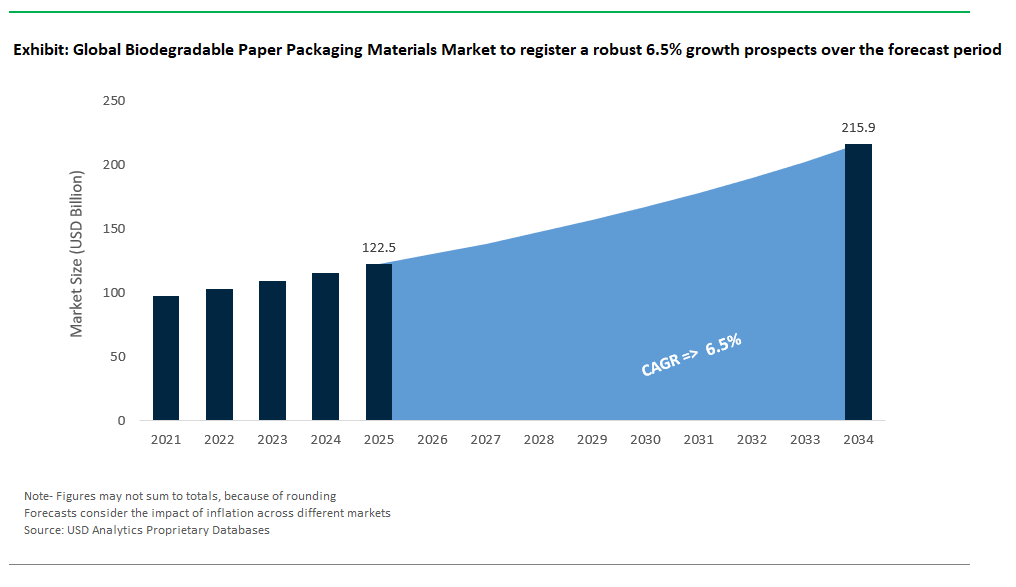

The Global Biodegradable Paper Packaging Materials Market is set to advance steadily between 2025 and 2034, driven by verified momentum from corporate sustainability initiatives, evolving government regulations, and innovative academic research focused on sustainable packaging solutions. Based on direct industry announcements and regulatory updates, the market is projected to grow from USD 122.5 billion in 2025 to USD 215.9 billion by 2034, reflecting a CAGR of 6.5%. Growth is underpinned by the expanding role of biodegradable paper packaging in food & beverages, e-commerce, retail, personal care, and healthcare sectors, as brands intensify their transition away from plastics and align packaging strategies with global climate and waste-reduction goals.

Backed by USDAnalytics’ proprietary research, the newest report presents an in-depth review and future projections for the global Biodegradable Paper Packaging Materials Market, covering developments in 21 countries and profiling upwards of 20 major players- By Material Type (Virgin Fiber-based Paper & Paperboard, Recycled Fiber-based Paper & Paperboard, Agricultural Residue-based Paper & Paperboard, Coated Paper & Paperboard), By Packaging Type (Flexible Paper Packaging, Rigid Paper Packaging), By End-Use Industry (Food & Beverages, E-commerce & Retail, Personal Care & Cosmetics, Homecare, Healthcare & Pharmaceuticals, Others).

This report provides a comprehensive analysis of the global biodegradable paper packaging materials market, spotlighting breakthrough product developments, large-scale corporate projects, and policy reforms accelerating sustainable material adoption through 2034. It investigates advances in agricultural residue-based papers, innovations in coatings that enhance recyclability and barrier properties, and the rising shift toward high-performance recycled fiber solutions. The study also explores the strategic moves of packaging manufacturers expanding capacity, investing in eco-friendly technologies, and forming alliances to serve the evolving demands of food, e-commerce, cosmetics, and pharmaceutical applications. Equipped with verified segmentation and practical insights, this report serves as an essential guide for paper manufacturers, converters, brand owners, and policymakers committed to leading the global transition toward sustainable packaging materials.

Global Biodegradable Paper Packaging Materials Market Analysis: Verified Corporate, Policy & Research Developments

The global biodegradable paper packaging materials market is rapidly evolving as sustainability becomes a non-negotiable priority across industries, driven by tightening regulations, technological breakthroughs, and strong commercial adoption by major brands. Historically limited to niche applications, biodegradable paper packaging is increasingly penetrating mainstream markets, offering a credible alternative to plastics and multi-material laminates. Recent innovations, capacity expansions, and collaborations underscore how the industry is aligning to meet both environmental imperatives and performance demands in diverse packaging applications.

Innovative Product Launches: Elevating Functionality and Scope

Product innovation remains at the forefront of market momentum, with companies launching biodegradable paper materials that deliver both sustainability and performance. Mondi’s FunctionalBarrier Recyclable exemplifies the new generation of paper solutions designed for recycling, offering a fiber-based alternative to plastic laminates in applications like dry food packaging while ensuring barrier protection. Stora Enso’s EcoFiber™ Barrier, a nanocellulose-coated paper, addresses grease and oil resistance in fast-food applications, bridging the performance gap that historically limited paper’s use in demanding foodservice contexts. Meanwhile, companies like DS Smith are innovating with coated papers designed from recycled fibers, supporting sustainable packaging for e-commerce and other sectors.

Capacity Expansions: Signaling Scaling for Mainstream Adoption

Substantial investments in capacity and technology are transforming biodegradable paper packaging from niche materials into scalable industrial solutions.

- Stora Enso’s €97 million investment at Skoghall Mill expands packaging board production, driven by strong demand for sustainable food packaging materials across Europe.

- Billerud is increasing production of innovative paper solutions like FibreForm®, reflecting rising interest in molded biodegradable paper pulp for luxury packaging where sustainability is a key brand differentiator.

- UPM’s new biorefinery in Germany will produce bio-based barrier chemicals, emphasizing the importance of sustainable raw materials for biodegradable coatings used in moisture- and grease-resistant paper packaging.

Strategic Partnerships and Acquisitions: Driving Innovation in Biodegradable Packaging

Strategic partnerships and acquisitions are reshaping the biodegradable packaging industry, combining expertise in paper, biopolymers, and sustainable coatings to unlock new growth opportunities. Tetra Pak is developing 100% paper-based beverage cartons with innovative plant-based barriers, aiming to replace aluminum foil in liquid packaging while ensuring recyclability and high performance. Novamont’s work with MATER-BI® coatings shows how global companies are creating advanced bioplastics to tackle environmental issues like ocean pollution, expanding biodegradable paper applications into areas such as coastal tourism and seafood packaging. Meanwhile, Sealed Air’s acquisition of AFP, Inc., a specialist in diverse packaging solutions, highlights the industry’s focus on scaling sustainable packaging to meet growing retailer and consumer demand, particularly in protective and custom-fabricated packaging segments.

Regulatory Drivers: Propelling Rapid Market Adoption

Global regulatory initiatives are significantly accelerating the adoption of biodegradable paper packaging.

- The European Union’s Packaging and Packaging Waste Regulation (PPWR) sets binding targets for compostable packaging in applications like tea and coffee bags, fruit and vegetable labels, and lightweight plastic carrier bags by February 2028, creating clear market pathways for sustainable products.

- California’s SB 54 legislation requires 100% compostable paper takeout containers by 2032, indicating that the U.S. policy is pushing brands to update their packaging portfolios for sustainability.

- India’s nationwide actions to reduce plastic pollution are driving demand for biodegradable solutions, with e-commerce giants like Flipkart and Amazon committed to removing single-use plastics from their packaging.

Technological Breakthroughs: Enhancing Performance and Environmental Impact

Technological innovation is overcoming the limitations that once constrained biodegradable paper’s broader adoption. The Fraunhofer Institute, among other research bodies, is exploring advanced bio-based coatings that could deliver enhanced moisture and oil resistance for paper packaging, with research focusing on materials that can degrade responsibly in various environments, including marine contexts. Research into intelligent, sustainable packaging solutions, such as enzyme-responsive indicators being explored by universities, is aiming to merge environmental responsibility with added consumer value by providing real-time food spoilage information and enabling packaging to degrade appropriately.

Commercial Adoption: Confirming Market Readiness for Biodegradable Paper Packaging

Global brands are increasingly adopting biodegradable paper packaging, signaling strong confidence in its performance and market viability. McDonald’s switch to paper straws in multiple regions reflects how major fast-food chains are moving away from traditional plastics, though challenges remain in recycling infrastructure and material design for such products. Nestlé’s pilot shift of KitKat wrappers to recyclable paper packaging shows that iconic consumer brands are embracing sustainable alternatives without compromising brand identity or functionality. Unilever’s rollout of plant-based polyethylene-coated paper tubs for Ben & Jerry’s ice cream in both the EU and U.S. underscores that biodegradable paper packaging can meet the demands of challenging applications like frozen foods, where barrier performance and consumer appeal are critical.

Biodegradable Paper Packaging Materials Market Dynamics: Bio-Based Coatings and E-Commerce Growth

Trend: Bio-Based Barrier Coatings Replacing PFAS and Petrochemical Alternatives

The global biodegradable paper packaging industry is undergoing a major shift as regulations tighten and performance demands rise, driving the replacement of PFAS and petrochemical coatings with advanced bio-based barriers. Patent activity in bio-barrier technologies is surging, reflecting significant R&D investment in materials like starch-chitosan blends and cellulose nanofibers. This innovation push is essential, as regions including the EU, U.S., Canada, Japan, and Australia enforce or propose strict bans on PFAS in food packaging, with many deadlines approaching by 2025 and beyond.

Bio-based coatings are rapidly matching the performance of synthetic alternatives, with new solutions like protein-lipid hybrids offering strong water resistance for demanding packaging uses. Importantly, costs are declining as pilot production scales up and economies of scale reduce the price premium of bio-based barriers, making widespread adoption increasingly viable across the packaging industry.

Opportunity: E-Commerce Standardization Spurs Growth in Paper-Based Packaging

A significant opportunity for biodegradable paper packaging is emerging in the e-commerce sector, where standardized packaging formats are driving a major shift from plastic materials to engineered paper solutions. As of 2024, replacing plastic mailers and void fill with paper-based alternatives offers a vast market potential, with millions of tons of plastic targeted for elimination.

Consumer preferences are a strong catalyst: surveys show many online shoppers are deeply concerned about plastic packaging and are willing to choose more sustainable options. This trend is pushing retailers and brands to adopt eco-friendly solutions. Beyond consumer demand, paper packaging offers clear environmental and logistical advantages. Optimized paper cushioning designs can lower logistics emissions compared to plastic bubble wrap, as confirmed by life cycle assessments focused on sustainable alternatives.

Adoption is growing fast, with a rising number of top global retailers implementing paper-based e-commerce packaging, signaling an industry-wide shift toward sustainability. As e-commerce continues to expand, standardized, sustainable paper packaging is poised to reshape supply chains, delivering environmental benefits and giving brands a competitive edge in the evolving biodegradable packaging market.

Competitive Landscape of the Global Biodegradable Paper Packaging Materials Market

The global biodegradable paper packaging materials market is gaining remarkable momentum in 2024, driven by regulatory bans on single-use plastics, rising sustainability commitments from major brands, and growing consumer demand for eco-friendly packaging alternatives. Innovations in bio-based barrier coatings, molded fiber solutions, compostable papers, and 3D-moldable papers are reshaping both functional and luxury packaging sectors. As paper packaging evolves to meet demanding performance and environmental standards, leading companies are expanding capacities, forming strategic alliances, and launching new products that replace plastics across e-commerce, food service, electronics, and high-end retail applications. The competitive landscape reflects a dynamic race among innovators to define the future of sustainable packaging.

DS Smith: Leading in Molded Fiber Packaging and Plastic Replacement

DS Smith (UK) DS Smith has solidified its leadership in molded fiber packaging, serving the booming e-commerce sector with sustainable alternatives to plastics. The company achieved its target in 2023/24 of replacing, avoiding, or reducing over 1.2 billion pieces of plastic since setting this target in 2020/21, through alternative corrugated solutions. In 2024, DS Smith received WorldStar Global Packaging Awards for innovations, including a fully recyclable corrugated cardboard packaging solution for vehicle chassis and a mono-material, plastic-free packaging for navigation systems. These initiatives underscore DS Smith’s strategic focus on replacing plastic in high-volume packaging applications while supporting brand commitments to recyclability and sustainability.

Huhtamaki: Global Force in Sustainable Food Service Packaging

Huhtamaki (Finland) remains a global force in food service packaging, offering paper cups and containers designed for hot and cold food applications. In January 2025, Huhtamaki India hosted the presentation of "Design for Recyclability Guidelines for Films & Flexible Packaging" as part of the CII-India Plastics Pact's (IPP) initiative, highlighting its commitment to driving a circular economy in India's flexible packaging sector. The company also launched recyclable single-coated paper cups for dairy products in February 2025, designed to contain less than 10% plastic content and be fully recyclable in Europe. Huhtamaki’s expertise in bio-based, compostable, and recyclable solutions positions it as a key supplier to global brands seeking alternatives to plastic in the food and beverage sector.

Stora Enso: Pioneering Bio-Based Barrier-Coated Paper Technologies

Stora Enso (Sweden) Stora Enso is pioneering bio-based barrier-coated paper technologies, developing moisture- and oil-resistant coatings that enable paper to replace plastics in demanding food and beverage packaging applications. Stora Enso offers a range of paperboard materials, including Cupforma Natura™ and CKB™, which can be combined with bio-based PE Green coatings. Its partnership with Pulpex for paper bottle development, announced in May 2021, aims for large-scale industrial production of renewable and recyclable paper bottles and containers, with major brands like Coca-Cola, PepsiCo, and Unilever being part of the Pulpex global partner consortium. Stora Enso’s innovations are redefining the performance boundaries of paper packaging and solidifying its role as a sustainability leader in the industry.

UFP Technologies: Niche Leader in Molded Pulp for Medical & Electronics

UFP Technologies (USA) UFP Technologies is carving a niche in molded pulp solutions for protective packaging, primarily for the medical market, also serving electronics. The company reported a 13.1% increase in net sales for the full year 2023, reaching $400.1 million, compared to $353.8 million in 2022, with strong growth in its MedTech sales (up 21.0% in 2023). UFP Technologies’ ability to deliver molded pulp solutions with precise protective properties positions it strongly in sectors where environmental concerns and high-performance packaging needs intersect.

Sappi: Advancing Sustainable Paper Coatings and Barriers

Sappi (South Africa) Sappi is a significant player in sustainable paper coatings, leveraging its innovation in water-based, biodegradable barriers for food and consumer goods packaging. Sappi offers functional flexible packaging papers that provide integrated barriers against oxygen, water vapor, grease, and mineral oil, eliminating the need for additional coatings or laminations. These innovative papers are designed for various applications, including food and non-food packaging, and are recyclable in the paper waste stream, supporting sustainable packaging solutions. Sappi’s expertise in biodegradable barrier technologies is key to enabling paper to replace plastic in applications requiring grease, moisture, and oxygen resistance.

WestRock: Expanding Fiber-Based Packaging Portfolio

WestRock (USA) WestRock is expanding its fiber-based packaging portfolio, offering solutions that aim to be recyclable, compostable, or reusable. WestRock's 2025 target is to make 100% of its products recyclable, compostable, or reusable. The company recently formed Smurfit Westrock in July 2024, a strategic combination between Smurfit Kappa Group plc and WestRock Company, creating a global leader in sustainable paper-based packaging. This combination aims to bring together complementary portfolios and capabilities, enhancing offerings in corrugated and consumer packaging solutions. WestRock’s focus on fiber-based retail and food packaging solutions positions it as a major player in helping global brands meet recyclability and compostability goals.

BillerudKorsnäs: Redefining Packaging with FibreForm® Technology

BillerudKorsnäs (Sweden) BillerudKorsnäs is redefining packaging with its FibreForm® technology, a unique 3D-moldable paper used in premium applications. This technology allows for deep embossing and intricate designs, providing a tactile and visually appealing alternative to plastic for luxury brands. BillerudKorsnäs’ FibreForm® is utilized in various premium applications, showcasing how sustainability and luxury can coexist in modern packaging solutions.

Smurfit Kappa: Leadership in Corrugated and E-commerce Packaging

Smurfit Kappa (Ireland) Smurfit Kappa maintains its leadership in corrugated and e-commerce packaging, actively promoting paper as the ultimate biodegradable packaging material. Smurfit Kappa's corrugated boxes are designed to be highly versatile, customizable, and inherently biodegradable, disappearing within months if they end up in nature. The company emphasizes its commitment to sustainable innovation, ensuring its continued prominence in global paper-based packaging solutions across e-commerce, retail, consumer goods, and industrial sectors.

Segmentation Analysis: Biodegradable Paper Packaging Materials Market

By Material Type: Virgin Fiber-Based Paper Leads, Agricultural Residue-Based Materials Grow Fastest

In 2025, virgin fiber-based paper and paperboard dominate with a 39.4% market share, prized by brands for premium packaging that delivers high print quality and shelf appeal, especially in cosmetics and luxury goods. Agricultural residue-based paper and paperboard are the fastest-growing segment (CAGR 7.1%), propelled by sustainability initiatives and increasing use of byproducts such as sugarcane bagasse for food trays and molded pulp solutions. Recycled fiber-based packaging maintains wide adoption, serving the booming e-commerce and secondary packaging markets with cost-effective, circular economy solutions.

By Packaging Type: Rigid Paper Packaging Commands the Market, Flexible Paper Packaging Rises Rapidly

Rigid paper packaging leads the segment in 2025, underpinned by surging demand for boxes, cartons, and clamshells in e-commerce and food service. Flexible paper packaging is the fastest-growing type with a CAGR of 7.3%, as brands increasingly swap plastic films for paper-based pouches, wraps, and bags in snacks, frozen foods, and single-use applications.

By End-Use Industry: Food & Beverages Dominate, Healthcare & Pharmaceuticals Expand Most Rapidly

Food & beverages remain the primary end-use industry, accounting for 41.8% of demand in 2025, supported by the widespread adoption of coated paper, molded pulp, and compostable trays for packaging perishable and prepared foods. Healthcare and pharmaceuticals represent the fastest-growing sector, as demand spikes for biodegradable blister packs, medicine sachets, and sterile coated papers. E-commerce and retail are also growing swiftly, driven by Amazon and other retailers’ shift to eco-friendly corrugated and recycled packaging.

.png)

Sweden Leading the EU in Biodegradable Paper Packaging Innovation and Market Share

Sweden continues to solidify its position as the EU’s leading producer of biodegradable paper packaging, accounting for approximately 25% of the region’s market share. The Swedish packaging sector is at the forefront of R&D, with a major focus on developing water-based barrier coatings that replace plastics in food, retail, and e-commerce applications. BillerudKorsnäs, a sustainability champion, has recently launched FiberForm®, an advanced 3D-moldable paper that enables high-performance, plastic-free packaging for a wide range of products. In 2025, BillerudKorsnäs is further expanding the commercial applications of FiberForm®, particularly in collaboration with major European food brands, aiming to displace conventional plastic trays and containers. Supportive government policy, including tax incentives for brands that adopt plastic-free packaging, further accelerates industry growth and encourages commercial innovation. Swedish policymakers are currently exploring additional incentives for packaging made from sustainably managed forest resources, bolstering the competitive advantage of fiber-based solutions. Sweden’s leadership in sustainable fiber technology and rapid commercialization makes it a critical supplier and model for best practices across the EU and global markets.

Finland Driving Export Growth and Fiber-Based Packaging Leadership in Europe and Asia

Finland stands out as a major exporter and producer of biodegradable paper packaging materials, with a production capacity of 1.2 million tons per year and around 40% of output destined for EU and Asian markets. Finnish companies are pushing the envelope with recyclable and compostable solutions: Stora Enso’s EcoFiber™ paperboard, designed for food packaging, addresses both recyclability and food safety, while Kemira’s innovations in biodegradable wet-strength additives enhance product durability for demanding applications. By mid-2025, Stora Enso expects to see significant uptake of its new barrier board solutions, specifically designed to meet the upcoming EU regulations on fresh produce packaging. Kemira is also launching a new generation of bio-based wet-strength agents, offering even higher performance and lower environmental impact for pulp and paper mills. Finland’s competitive edge is rooted in world-class forest resources, advanced pulping technologies, and a strong export-oriented supply chain, making it a top global source for next-generation fiber-based packaging.

Germany Setting Industry Standards for Paper-Based Packaging and Compostable Coatings

Germany continues to act as Europe’s innovation hub for biodegradable paper packaging, with more than 50 patents filed annually for advanced paper coatings and conversion technologies. The country’s policy environment, driven by the EU Packaging and Packaging Waste Regulation (PPWR), mandates paper-based packaging for e-commerce and has accelerated the development and adoption of plastic-free solutions. Leading companies like Syntegon have created fully paper-based snack packaging that replaces plastic laminates, while BASF’s Ecovio® PS 1606 offers compostable coatings to improve packaging end-of-life options. In 2025, the German government, in collaboration with industry associations, is rolling out new certification standards for home-compostable paper packaging, aiming to increase consumer confidence and streamline waste collection. Furthermore, there's a concerted effort to scale up industrial composting facilities to handle the growing volume of certified compostable paper and board. Germany’s focus on research, technical standards, and regulatory compliance cements its role as a trendsetter for sustainable packaging throughout Europe.

The United States is Experiencing Rapid Growth and Brand Adoption in Biodegradable Paper Packaging

The United States is witnessing a surge in biodegradable paper packaging, with the market projected to grow at an 18% CAGR from 2023 to 2028. Industry giants such as WestRock and International Paper are leading the way, supplying innovative solutions to major consumer brands. Notable recent developments include McDonald’s transition to 100% paper-based sandwich wraps and Amazon’s large-scale adoption of curbside-recyclable paper mailers. By mid-2025, McDonald's aims for full compliance with its global paper-based packaging targets for wraps and bags, while Amazon is reportedly targeting over 75% of its U.S. shipments to utilize paper-based or easily recyclable mailers by year-end, further reducing reliance on plastic. Strong consumer demand for plastic-free, recyclable, and compostable packaging is driving rapid adoption across the foodservice, e-commerce, and retail sectors. The market’s momentum is further supported by evolving FTC Green Guides, which, in their anticipated 2025 updates, are expected to provide clearer definitions and stricter enforcement for "compostable" and "biodegradable" claims, encouraging greater transparency and verified sustainability efforts from brands.

Japan Pioneering Nano-Fibrillated Cellulose and Regulatory Push for Plastic-Free Packaging

Japan is at the technological forefront of biodegradable paper packaging, especially in the area of nano-fibrillated cellulose (NFC). The government’s 2025 mandate for plastic-free e-commerce packaging has spurred rapid innovation. Oji Holdings has developed transparent paper films for food packaging, offering both sustainability and shelf appeal. Electronics brands like Sony have adopted NFC-based packaging, reducing reliance on plastics in consumer electronics. In June 2025, Toyo Seikan Group Holdings, exhibiting as "Nano Cellulose Japan" at Expo 2025 Osaka, is showcasing the "New ECOCRYSTAL Cup," a barrier paper container utilizing Japan's first cellulose nanocrystals for enhanced oxygen barrier properties, marking a significant commercialization milestone for NFC in food packaging. Supported by progressive policy from the Ministry of Environment and a culture of continuous innovation, Japan is set to expand its influence in high-value, biodegradable packaging solutions for food, retail, and electronics.

India Scaling Production and Adoption of Bagasse-Based Biodegradable Packaging

India’s biodegradable paper packaging industry is on a steep growth trajectory, with production rising 30% year-over-year between 2023 and 2024. The sector is increasingly focused on bagasse (sugarcane waste)-based materials, which offer a renewable, compostable alternative to traditional paper and plastic packaging. Key market movers include Tata Packers, which recently introduced oil-resistant paper food containers, and leading food delivery platforms like Zomato and Swiggy, now using 100% compostable paper packaging for millions of orders nationwide. By late 2025, it's anticipated that over 60% of all food delivery orders from major platforms in India’s metropolitan areas will be delivered in certified compostable paper or bagasse-based packaging, a direct result of ongoing regulatory pressure and consumer preference. Supportive regulations from the Central Pollution Control Board (CPCB) and government investment in sustainable packaging infrastructure are driving rapid market adoption and innovation. The Plastic Waste Management (Amendment) Rules, 2025, effective July 1, 2025, mandate producers, importers, and brand owners to provide specific product information on plastic packaging, including for biodegradable plastics, via QR codes or other means, enhancing accountability and tracking.

China Dominating Global Biodegradable Paper Packaging Supply and Production Capacity

China is the world’s largest producer of biodegradable paper packaging, manufacturing over 3 million tons annually and supplying approximately 60% of global demand. The country’s vast scale is underpinned by leading players like Nine Dragons Paper, which operates the world’s largest recycled paper facility. Nine Dragons Paper and other major Chinese paper manufacturers are slated to bring significant new production lines for food-grade, barrier-coated paperboard online by early to mid-2025, further solidifying China's export dominance in specialized biodegradable paper packaging. Policy measures are accelerating adoption. Alibaba, for example, requires that half of all shipments use paper-only packaging by 2025. Alibaba's 2025 paper-only packaging mandate is seeing high compliance rates due to stringent internal auditing and a growing ecosystem of compliant suppliers, setting a precedent for other major e-commerce platforms. China’s supply chain efficiency, low-cost manufacturing, and rapid plant expansions have cemented its role as the leading source of both commodity and high-performance biodegradable paper packaging for export markets worldwide.

Brazil: Leveraging Sustainable Pulp and Molded Fiber Innovation for Global Packaging

Brazil holds a unique advantage as the world’s largest supplier of certified sustainable pulp, with fast-growing eucalyptus plantations supporting the biodegradable packaging sector. The country is experiencing strong growth in molded fiber packaging for electronics, as brands like Apple switch to Brazilian eucalyptus-fiber solutions. Klabin, a market leader, has recently developed waterproof paper using plant-based waxes, opening new opportunities for food and electronics packaging. In 2025, Brazil's molded fiber packaging market is projected to grow significantly, driven by increased demand from the electronics and food service sectors. Klabin is actively pursuing new partnerships for its waterproof paper solutions, particularly for liquid and semi-liquid food applications, leveraging its sustainable pulp base. Supportive government policies and a deep resource base make Brazil an increasingly strategic partner for global brands seeking sustainable, compostable paper packaging materials.

Biodegradable Paper Packaging Materials Market Report Scope

Biodegradable Paper Packaging Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$122.5 Billion

|

|

Market Size (2034)

|

$215.9 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Material Type (Virgin Fiber-based Paper & Paperboard, Recycled Fiber-based Paper & Paperboard, Agricultural Residue-based Paper & Paperboard, Coated Paper & Paperboard), By Packaging Type (Flexible Paper Packaging, Rigid Paper Packaging), By End-Use Industry (Food & Beverages, E-commerce & Retail, Personal Care & Cosmetics, Homecare, Healthcare & Pharmaceuticals, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company (U.S.), Mondi Group (Austria/UK), Stora Enso (Finland/Sweden), WestRock Company (U.S.), Smurfit Kappa Group Plc (Ireland), DS Smith Plc (UK), Huhtamaki Oyj (Finland), Tetra Pak International SA (Switzerland), Kruger Inc. (Canada), Amcor Plc (Switzerland/Australia) , Novamont S.p.A. (Italy) , NatureWorks LLC (U.S.) , Notpla (UK) , Solenis LLC (U.S.) , Kemin Industries Inc. (U.S.) , Be Green Packaging LLC (U.S.), Ecoware (India), Pakka Ltd. (formerly Yash Pakka Ltd.) (India), Chuk (Brand of Yash Pakka Ltd.) (India), BioPak (Part of Duni Group/Huhtamaki Oyj) (Sweden/Finland) , Sulapac (Finland) , Reynolds Group Holdings Limited (U.S.) , Oji Holdings Corporation (Japan), BillerudKorsnäs AB (now Billerud) (Sweden), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, AfricaMarket Report Scope

|

Biodegradable Paper Packaging Materials Market Segmentation

By Material Type

- Virgin Fiber-based Paper & Paperboard

- Kraft Paper

- Corrugated Board

- Boxboard

- Specialty Papers

- Molded Pulp

- Recycled Fiber-based Paper & Paperboard

- Recycled Kraft Paper

- Recycled Corrugated Board

- Recycled Boxboard

- Recycled Molded Pulp

- Agricultural Residue-based Paper & Paperboard

- Bagasse-based Materials

- Bamboo-based Materials

- Straw-based Materials

- Coated Paper & Paperboard

- Paper/Board with PLA Coatings

- Paper/Board with PBAT Coatings

- Paper/Board with Starch-based Coatings

- Paper/Board with Water-dispersible/Soluble Coatings

- Paper/Board with Seaweed-based Coatings (e.g., Notpla)

By Packaging Type

- Flexible Paper Packaging

- Rigid Paper Packaging

By End-Use Industry

- Food & Beverages

- E-commerce & Retail

- Personal Care & Cosmetics

- Homecare

- Healthcare & Pharmaceuticals

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Paper Packaging Materials Market

- International Paper Company (US)

- Mondi Group (Austria/UK)

- Stora Enso (Finland/Sweden)

- WestRock Company (US)

- Smurfit Kappa Group Plc (Ireland)

- DS Smith Plc (UK)

- Huhtamaki Oyj (Finland)

- Tetra Pak International SA (Switzerland)

- Kruger Inc. (Canada)

- Amcor Plc (Switzerland/Australia)

- Novamont S.p.A. (Italy)

- NatureWorks LLC (US)

- Notpla (UK)

- Solenis LLC (US)

- Kemin Industries Inc. (US)

- Be Green Packaging LLC (US)

- Ecoware (India)

- Pakka Ltd. (formerly Yash Pakka Ltd.) (India)

- Chuk (Brand of Yash Pakka Ltd.) (India)

- BioPak (Part of Duni Group/Huhtamaki Oyj) (Sweden/Finland)

- Sulapac (Finland)

- Reynolds Group Holdings Limited (US)

- Oji Holdings Corporation (Japan)

- BillerudKorsnäs AB (now Billerud) (Sweden)

* List Not Exhaustive

Methodology

The Global Biodegradable Paper Packaging Materials Market 2025–2034 report is built upon a rigorous, multi-layered research methodology designed to ensure high accuracy and actionable insights. The research process integrates both primary and secondary sources. Primary research includes direct interviews and structured discussions with executives at paper mills, converters, coatings specialists, end-use brand owners, material scientists, and regulatory officials to gather firsthand intelligence on market trends, technological advances, and regulatory implications. Secondary research leverages exhaustive analysis of company disclosures, government policy updates, scientific publications, patent filings, industry trade reports, and authoritative databases to validate and contextualize market findings.

Market size estimates use a hybrid approach, combining top-down macroeconomic modeling—based on global fiber production trends, sustainability regulations, and industry output statistics—with bottom-up data aggregation from key market participants, capacity expansions, and material usage rates across over 25 countries. Forecasts from 2025 to 2034 undergo triangulation and stress testing against proprietary data models from USDAnalytics and scenario analyses that account for regulatory shifts, technological breakthroughs, and geopolitical or economic volatility. The result is a robust, credible forecast and strategic insights for decision-makers across the biodegradable paper packaging value chain.

Research Coverage

- Geographic Scope: Global, including detailed country-level analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa, covering more than 25 individual countries.

- Segmentation: Extensive segmentation by Material Type (Virgin Fiber-based Paper & Paperboard, Recycled Fiber-based Paper & Paperboard, Agricultural Residue-based Paper & Paperboard, Coated Paper & Paperboard), Packaging Type (Flexible Paper Packaging, Rigid Paper Packaging), and End-Use Industry (Food & Beverages, E-commerce & Retail, Personal Care & Cosmetics, Homecare, Healthcare & Pharmaceuticals, Others).

- Competitive Analysis: Comprehensive profiles of over 25 leading global and regional companies, detailing product portfolios, capacity investments, strategic collaborations, sustainability initiatives, and recent innovations in biodegradable paper packaging.

- Key Themes: Examination of technological breakthroughs in bio-based barrier coatings, sustainability-driven capacity expansions, PFAS replacement trends, regulatory catalysts (e.g., EU PPWR, California SB 54), circular economy initiatives, and emerging applications in sectors like e-commerce, luxury goods, and healthcare.

- Market Dynamics: In-depth analysis of market drivers, restraints, policy impacts, technological innovations, supply chain developments, cost structures, and evolving consumer behavior influencing the biodegradable paper packaging landscape through 2034.

- Data Horizon: Historical data spanning 2021–2024 and forward-looking projections for 2025–2034.

Deliverables

- Comprehensive Market Report (PDF & Excel): Includes narrative analysis, data tables, and insightful visuals covering market dynamics, competitive intelligence, and segment forecasts.

- Country-Level Market Forecasts and Strategic Insights

- Segment-Level Revenue and Volume Projections (2025–2034)

- Detailed Company Profiles and Competitive Benchmarking

- Regulatory Landscape Analysis and Policy Tracker

- Executive Summary with Analyst Commentary and Strategic Recommendations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requests