Market Overview: Sustainability and Paperization Defining Future Growth

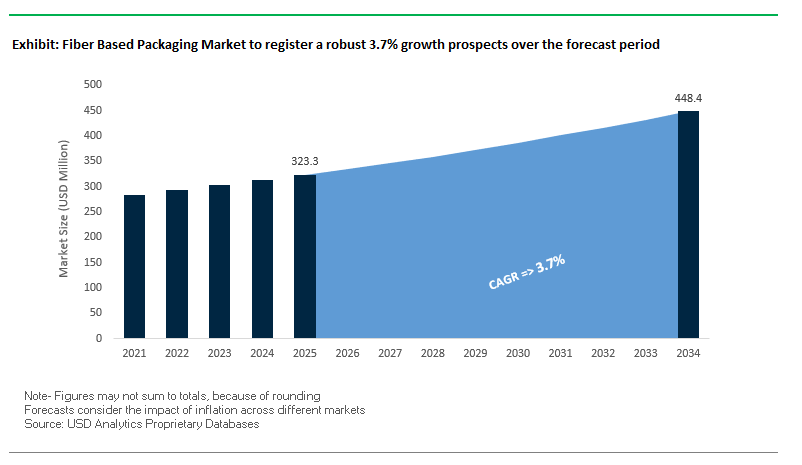

The Global Fiber-Based Packaging Market is projected to grow from USD 323.3 million in 2025 to USD 448.3 million by 2034, advancing at a CAGR of 3.7%. This industry is undergoing significant transformation, driven by regulatory mandates, consumer awareness, and corporate commitments to phase out single-use plastics. Fiber-based packaging spans corrugated boxes, cartons, molded pulp, and flexible wraps, all of which are being reengineered to enhance durability, functionality, and sustainability.

One of the defining trends is “paperization”, where brands replace plastics and foams with renewable and recyclable paper-based alternatives. Coupled with bio-based barrier coatings that enhance resistance to grease, moisture, and oxygen, fiber packaging is increasingly suitable for food, beverage, and personal care applications. Moreover, governments enforcing plastic bans and extended producer responsibility (EPR) regulations are accelerating adoption.

Digital printing is becoming integral to the sector, enabling high-resolution graphics, QR codes, and smart features that enhance traceability and consumer engagement. At the same time, advances in molded pulp and composite fiber packaging are expanding applicability in electronics, healthcare, and temperature-sensitive logistics.

Key Insights for Industry Professionals:

- Market size forecast: USD 323.3M (2025) → USD 448.3M (2034), CAGR 3.7%.

- Paperization trend replacing plastics with recyclable fiber packaging.

- Bio-based coatings improving barrier properties for food and pharma use.

- Plastic bans and EPR regulations driving faster adoption by global brands.

- Digital printing and smart features integrating marketing with supply chain traceability.

Market Analysis: Recent Developments in the Fiber-Based Packaging Industry

The Fiber-Based Packaging Industry is experiencing robust momentum, marked by mergers, innovation, and capacity expansion to meet global sustainability targets.

In August 2025, International Paper announced the divestment of its Global Cellulose Fibers business for USD 1.5 billion, refocusing on its core sustainable packaging solutions. The same month, Graphic Packaging International launched its PaperSeal® Pressed MAP tray, a recyclable food packaging innovation, while Huhtamaki Oyj priced EUR 300 million in notes to refinance debt and fund sustainable packaging growth.

Also in August 2025, Smurfit Kappa and WestRock finalized their all-stock merger, creating a global leader in corrugated and paperboard packaging, strengthening capabilities in e-commerce and retail packaging. Earlier in May 2025, DS Smith announced it had exceeded its 2025 target of replacing over 1 billion plastic units with fiber-based alternatives, a landmark achievement in its “Now and Next” sustainability strategy.

In April 2025, Graphic Packaging received child-resistant certification for its CleanClose™ paperboard detergent pod packaging, underscoring the rising importance of safety and compliance in FMCG packaging. In January 2025, DS Smith introduced TailorTemp, a fiber-based temperature-controlled solution for cold chain logistics in pharmaceuticals and biotech, demonstrating the expansion of fiber packaging into high-value applications.

Game-Changing Trends and Growth Opportunities in the Fiber-Based Packaging Market

Advanced Functional Coatings for PFAS-Free Oil and Grease Resistance

A defining trend in the fiber-based packaging market is the rapid adoption of PFAS-free functional coatings that provide oil, water, and grease resistance without relying on harmful fluorochemicals. This shift is being propelled by strict regulations, such as New York State’s ban on intentionally added PFAS in food-contact fiber packaging since December 2022, which covers pizza boxes, pastry packaging, and sandwich wrappers. To meet compliance and consumer expectations for safer materials, manufacturers are pivoting toward bio-based polymers, plant-derived waxes, and cellulose-based coatings. Companies like Lotus Nano are leading innovation in this space, offering PFAS-free, food-contact safe coatings that meet durability requirements for fast-food wrappers and dairy packaging. R&D efforts are equally strong, with firms developing water-based dispersion coatings that are fully compostable while maintaining structural integrity. This creates a significant growth avenue, particularly in the foodservice sector, where demand for plastic-free, recyclable, and compostable fiber packaging is surging. Ultimately, PFAS-free barrier innovations are redefining the value chain by giving packaging manufacturers a compliant, high-performance alternative that aligns with both regulatory mandates and consumer preferences.

Digital Printing Driving High-Impact, Short-Run E-Commerce Packaging

The adoption of digital printing technologies for fiber-based packaging is transforming the way brands engage with e-commerce and direct-to-consumer (D2C) markets. Unlike conventional offset printing, digital solutions eliminate the need for costly printing plates, enabling small-batch or even single-unit production with lead times as short as two to five days. Industry leaders like Stora Enso have already rolled out digitally printed corrugated boxes designed for agile supply chains and personalized branding. This trend is being fueled by the explosive rise of e-commerce, where packaging is no longer just a protective layer but also a primary marketing channel that delivers brand identity directly to the consumer’s doorstep. Companies offering on-demand digital printing services empower small and medium-sized D2C brands to create personalized, versioned, and promotional packaging without the constraints of high-volume orders. The growth potential is enormous, as digital printing reduces material waste, supports rapid prototyping, and enhances customer engagement. For packaging suppliers, this trend also shifts their role from being mere providers to strategic partners, helping brands optimize inventory, reduce waste, and elevate their consumer experience with agile, high-graphics packaging.

Expansion of Molded Fiber Packaging for Complex, Non-Food Applications

While molded fiber packaging is widely recognized for egg cartons and food trays, there is a high-value growth opportunity in developing molded fiber solutions for electronics, cosmetics, and industrial applications. The demand for sustainable alternatives to plastic foams and rigid plastics is rising, particularly in protective packaging for high-end products. Manufacturers are experimenting with advanced fiber blends and precision forming technologies to create molded pulp inserts with smoother finishes, higher resolution designs, and superior cushioning properties. Companies are already delivering custom-designed molded fiber packaging for electronics, offering impact protection while being fully recyclable. This creates strong appeal for premium consumer goods companies seeking sustainable packaging solutions that do not compromise performance or aesthetics. The commercialization of advanced molded fiber will not only diversify revenue streams for packaging manufacturers but also foster collaboration between fiber-based material scientists, product designers, and global brands. By scaling this innovation, the industry can unlock new sectors where sustainability, durability, and branding converge, making molded fiber a credible replacement for plastics in non-food categories.

Designing Fiber-Based Composites Compatible with Chemical Recycling

Another compelling opportunity lies in making fiber-based composite packaging compatible with chemical recycling technologies, a breakthrough that could address one of the sector’s largest sustainability challenges. Multi-material packaging, such as paperboard with plastic linings, often escapes traditional recycling streams due to the difficulty of separating components. Chemical recycling provides a solution by breaking down plastics into monomers while recovering fiber, enabling true circularity for composite packaging. Companies are piloting new processes to separate fiber and plastic layers using innovative mechanical-chemical hybrid techniques such as spindle screen friction separation. At the same time, studies show that pyrolysis and depolymerization methods can convert composite plastics into valuable petrochemical feedstock, creating both economic and environmental benefits. This compatibility is set to become a major differentiator, allowing packaging manufacturers to offer fiber-based composites that are not just recyclable in theory but actually recoverable in practice. By embracing this innovation, the fiber-based packaging market can position itself at the forefront of sustainable materials science, creating scalable solutions for brand owners under increasing pressure to meet circular economy goals.

Competitive Landscape: Key Players Driving Fiber-Based Packaging Innovation

The Global Fiber-Based Packaging Market is highly competitive, with leading companies investing in new technologies, mergers, and sustainability programs to strengthen market presence.

International Paper focuses on core sustainable packaging solutions

International Paper remains a leader with its vast network of mills and conversion facilities. In August 2025, it sold its Global Cellulose Fibers business for USD 1.5B, streamlining operations to concentrate on corrugated and containerboard solutions. Its portfolio includes corrugated boxes, cartons, and specialty papers. Strategic investments, such as its USD 250M mill conversion in Alabama, demonstrate its commitment to reinforcing its supply capabilities.

Smurfit Kappa expands global reach through WestRock merger

Smurfit Kappa, now merged with WestRock, has created a global paper-based packaging powerhouse. Known for corrugated e-commerce and retail solutions, it offers innovative displays, boxes, and protective inserts. The merger enhances its global footprint and portfolio scale, positioning it to meet surging demand for sustainable and lightweight packaging while optimizing supply chains.

Graphic Packaging pioneers food-safe and child-resistant fiber solutions

Graphic Packaging International continues to lead in food and FMCG packaging. In August 2025, it launched its PaperSeal® MAP tray, providing recyclable solutions for the food industry, and earlier secured child-resistant certification for CleanClose™ detergent pod cartons. Its ongoing Waco, Texas paperboard facility expansion will significantly increase fiber packaging capacity, reinforcing its focus on safety, performance, and circularity.

DS Smith surpasses plastic replacement targets with circular design

DS Smith is a sustainability-focused leader, recognized in May 2025 for eliminating over 1 billion pieces of plastic from the market. Its innovations include TailorTemp fiber cold chain packaging for pharmaceuticals, replacing EPS foam. With its Circular Design Metrics, DS Smith partners with FMCG brands to enhance recyclability and reduce waste, reinforcing its leadership in circular economy packaging solutions.

Huhtamaki Oyj strengthens fiber packaging with U.S. acquisition

Huhtamaki Oyj is a global specialist in fiber-based food packaging, with offerings spanning paper cups, molded fiber egg cartons, and compostable containers. In early 2025, it acquired Zellwin Farms in the U.S., expanding its installed capacity in fiber-based egg packaging. Its strategy emphasizes compostable and recyclable packaging, backed by a multi-year efficiency program and strong investment in fiber innovation.

Fiber Based Packaging Market Share Insights

Corrugated Boxes Hold the Largest Market Share by Product Type in Fiber-Based Packaging

Corrugated boxes account for 55% of the fiber-based packaging market, making them the undisputed workhorse of the global supply chain. Their strength, stackability, and low cost position them as the default solution for transport, logistics, and particularly e-commerce packaging. The ongoing boom in online retail has made corrugated boxes indispensable for last-mile delivery, where durability and branding opportunities converge. Advances in lightweight fluting, recycled fiber integration, and high-graphic digital printing ensure that corrugated boxes continue to evolve to meet sustainability mandates while maintaining cost efficiency. Their dominance reflects not only sheer shipping volume but also their versatility across B2B and B2C sectors, securing their place as the backbone of fiber-based packaging demand.

E-Commerce Emerges as the Fastest-Growing End-Use in Fiber-Based Packaging

E-commerce now represents 25% of the fiber-based packaging market, making it the fastest-growing end-use sector. Every online purchase—from apparel and electronics to groceries—requires corrugated shipping containers or mailers, creating a continuous surge in demand. The need for right-sized, durable, and sustainable boxes has fueled innovation in automated packaging systems, recycled paper integration, and digital print customization for branding. Unlike traditional retail packaging, e-commerce prioritizes protective strength and customer experience through unboxing, making it a driver of structural as well as graphic design innovation. This segment’s rise is reshaping the entire fiber-based packaging supply chain, as converters and brands adapt to support omnichannel retail with scalable, cost-effective, and sustainable corrugated solutions.

United States Fiber-Based Packaging Market Accelerating Through EPR Regulations and Sustainable Innovations

The U.S. fiber-based packaging market is driven by a fragmented regulatory environment at federal, state, and local levels. With seven states, including Maryland in 2025, implementing Extended Producer Responsibility (EPR) laws, manufacturers are financially incentivized to adopt recyclable, fiber-based materials that reduce environmental impact. Technological advancements are reshaping the industry, with innovations like new barrier coatings for paper and paperboard replacing plastics. The Department of Energy’s $52 million fund in 2025 toward cellulose-based films underscores public sector support for next-generation fiber-based packaging substrates.

Corporate investments are also driving market growth, exemplified by the December 2024 partnership between Nexgen Packaging and Seaman Paper, focusing on plastic-free, paper-based solutions for retail, apparel, and footwear sectors. Key applications are concentrated in e-commerce and food and beverage industries, where the demand for durable, lightweight corrugated boxes and molded fiber inserts is rising. Leading brands like Coca-Cola and PepsiCo pushing for 100% recyclable or compostable packaging by 2025 further accelerate adoption. Sustainability remains a central focus, with recycled fiber solutions generating the highest revenue in 2024, reinforced by indirect demand from government-backed semiconductor initiatives that require protective fiber-based packaging.

Germany Fiber-Based Packaging Market Driven by Circular Economy Leadership and Regulatory Compliance

Germany’s fiber-based packaging market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR), which mandates full recyclability or reusability by 2030. The national Packaging Act further tightens recyclability requirements, prompting a shift from complex laminates to single-polymer or fiber-based structures. Germany’s well-established Extended Producer Responsibility (EPR) system incentivizes manufacturers to develop recyclable packaging through modulated fees.

Technological innovation is reshaping the market, with companies like ILLIG showcasing award-winning Dry Fiber Systems that produce cups, trays, and lids from cellulose fibers with high drawing depth and integrated barrier properties. Key applications are concentrated in the food, beverage, and FMCG sectors, driven by consumer demand for high-quality, sustainable packaging. Investments in R&D, such as pilot systems for trial runs, ensure efficient implementation of fiber-based packaging concepts. This combination of stringent regulations, technological innovation, and sustainability focus positions Germany as a global leader in fiber-based packaging solutions.

China Fiber-Based Packaging Market Expanding Through Government Initiatives and Advanced Manufacturing

China’s fiber-based packaging market is being shaped by governmental initiatives like the “dual carbon” goal and the 2024 Action Plan for Promoting Large-Scale Equipment Updates, encouraging recycling and sustainable materials adoption. Regulatory reforms targeting excessive packaging, effective since September 2023, influence fiber-based cartons, mailers, and e-commerce packaging.

Technological advancements, including AI-driven automation and “5G plus industrial internet” integration, are enhancing production efficiency and flexibility. Domestic manufacturing is a key focus, with local companies expanding capacity to substitute imported solutions. For instance, Valmet is constructing an OptiConcept M board line for Anhui Linping, scheduled to go online by 2025. Key applications include e-commerce, food and beverage, and quick-service restaurants, with nationwide surveys indicating that 68% of shoppers prefer paper wrappers for online grocery deliveries when performance is comparable to plastic. These developments reinforce China’s position as a rapidly expanding and innovative fiber-based packaging hub.

India Fiber-Based Packaging Market Fueled by Circular Economy Initiatives and Automation

India’s fiber-based packaging market is experiencing rapid growth due to government policies promoting a circular economy and sustainable packaging practices. Recent GST reductions have temporarily disrupted FMCG companies, prompting industry calls for a grace period to avoid wastage of pre-printed packaging materials. Technological advancements, including automated production systems, are enabling the creation of cost-effective and high-performance packaging solutions. Companies like Naini Papers and PrimeFiber are driving innovation in specialty packaging papers through strategic partnerships.

Corporate investments, such as the 2025 collaboration between Naini Papers and PrimeFiber Global Paper Solutions, are strengthening India’s domestic specialty paper segment. Key applications span food and beverage, personal care, and e-commerce sectors, with the demand for high-quality, recyclable, and compostable fiber-based packaging growing steadily. The expanding domestic market and low capital requirements for fabrication units are attracting new entrants, positioning India as a key growth market for sustainable fiber-based packaging solutions.

Japan Fiber-Based Packaging Market Advancing Through High-Performance Technology and Consumer Sustainability Demand

Japan’s fiber-based packaging market is at the forefront of innovation, driven by advanced manufacturing and sustainability-focused regulations. The Plastic Resource Circulation Act, effective since April 2022, promotes environmentally friendly design and reduces single-use plastics. Nippon Molding’s installation of the PulPac Modula machine in 2025 exemplifies the industry’s adoption of dry-molded fiber technology, significantly reducing water and energy consumption compared to conventional methods.

High-performance coatings and lamination techniques are enhancing barrier properties, enabling fiber-based alternatives to traditional plastics. The market is responding to consumer concerns over ocean litter, with a growing preference for sustainable packaging. Functional innovation, including improved dimensional stability and moisture resistance, addresses high-performance application needs. Collaborative industry efforts, such as Nippon Molding’s initiative to produce responsible fiber-based packaging, are driving further adoption and innovation across Japan’s packaging ecosystem.

Brazil Fiber-Based Packaging Market Expanding Through Sustainability Laws and Local Innovation

Brazil’s fiber-based packaging market is shaped by the National Solid Waste Policy and 2024 legislation targeting single-use disposable items, requiring all packaging to be returnable, recyclable, or compostable by 2030. This regulatory push encourages manufacturers to adopt sustainable fiber-based solutions. Technological advancements, including robotics and AI integration, are enhancing production efficiency and quality control. Notable developments include biodegradable films derived from sugarcane bagasse.

Corporate investments are increasing to meet local demand, with facilities focusing on eco-friendly, high-performance packaging. Key applications are concentrated in food and beverage and cosmetics sectors, supported by a growing processing industry. Sustainability remains central, with the adoption of paper-based packaging with bio-based coatings. Research collaborations, such as the EMBRAPA-UIC smart packaging project that uses nanofiber mats and natural pigments to indicate fish freshness, exemplify Brazil’s commitment to innovation and advanced, responsible fiber-based packaging solutions.

Fiber Based Packaging Market Report Scope

Fiber Based Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$323.3 Million

|

|

Market Size (2034)

|

$448.3 Million

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Product Type (Corrugated Boxes, Folding Cartons, Liquid Cartons, Bags & Sacks, Sacks, Other Packaging Products), By Material Source (Virgin Fiber, Recycled Fiber), By End-Use Industry (Food & Beverages, Personal Care, Home Care, Pharmaceuticals, Industrial, E-commerce, Other End-Use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, DS Smith plc, WestRock Company, Sonoco Products Company, Graphic Packaging Holding Company, Rengo Co., Ltd., Billerud AB, Pactiv Evergreen Inc., Amcor plc, Greif, Inc., Sealed Air Corporation, Berry Global Group, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fiber Based Packaging Market Segmentation

By Product Type

- Corrugated Boxes

- Folding Cartons

- Liquid Cartons

- Bags & Sacks

- Sacks

- Other Packaging Products

By Material Source

- Virgin Fiber

- Recycled Fiber

By End-Use Industry

- Food & Beverages

- Personal Care

- Home Care

- Pharmaceuticals

- Industrial

- E-commerce

- Other End-Use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fiber Based Packaging Market

- International Paper Company

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- DS Smith plc

- WestRock Company

- Sonoco Products Company

- Graphic Packaging Holding Company

- Rengo Co., Ltd.

- Billerud AB

- Pactiv Evergreen Inc.

- Amcor plc

- Greif, Inc.

- Sealed Air Corporation

- Berry Global Group, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive, multi-faceted research methodology to deliver an authoritative analysis of the Global Fiber-Based Packaging Market. The approach combined extensive primary research, including interviews with packaging manufacturers, FMCG brand managers, sustainability officers, and supply chain experts, with secondary research drawing from company reports, regulatory filings, press releases, and industry publications. Quantitative forecasting models were applied to estimate market growth across product types, material sources, and end-use industries, while qualitative insights highlighted trends such as paperization, PFAS-free coatings, digital printing, and molded fiber innovations. Regional market dynamics in the U.S., Germany, China, India, Japan, and Brazil were analyzed with a focus on regulations, government initiatives, circular economy policies, and technological adoption. USDAnalytics also assessed innovations in chemical recycling-compatible composites, high-barrier fiber films, and e-commerce-specific packaging solutions, ensuring a holistic, data-driven outlook that equips industry professionals with actionable insights for strategic planning, operational efficiency, and investment decisions in the evolving fiber-based packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.