Water-Soluble Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Water-Soluble Packaging Market Set to Reach $6.3 Billion by 2034 Driven by Sustainability and Regulatory Compliance

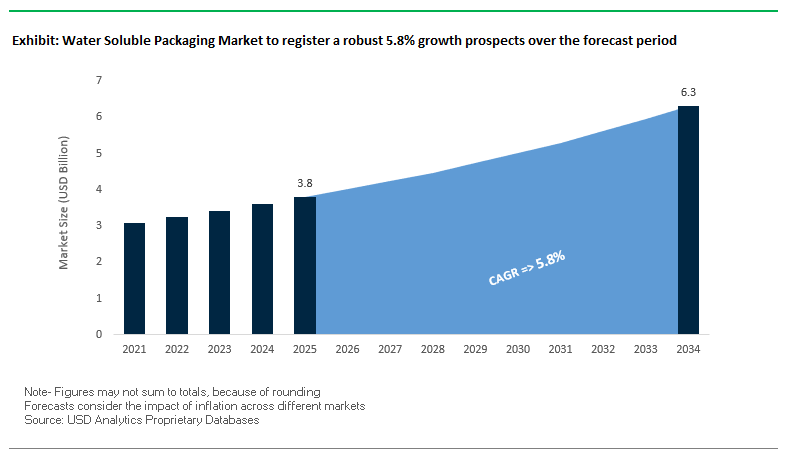

The global water-soluble packaging market is projected to grow from $3.8 billion in 2025 to $6.3 billion by 2034, at a CAGR of 5.8%. Water-soluble packaging, typically made from polyvinyl alcohol (PVOH), dissolves in water to leave a non-toxic and biodegradable residue, making it an essential solution for reducing plastic waste. This market is critical to home care, industrial, and agricultural sectors, where precise dosing, consumer convenience, and environmental safety are increasingly prioritized.

Key Insights for industry professionals and buyers:

- Regulatory pressures such as bans on single-use plastics are driving the adoption of water-soluble alternatives globally.

- Advances in polymer technology are enhancing film strength, barrier properties, and solubility customization, enabling applications beyond traditional sectors.

- Single-dose formats like pods and capsules improve user safety, convenience, and product efficiency, particularly in laundry, dishwasher, and agricultural products.

- Marine-safe and fully biodegradable films are becoming a focus to prevent microplastic pollution and meet environmental standards.

- Material innovation and consumer trends are creating opportunities for market expansion into food, cosmetics, and specialty chemical applications.

Market Analysis: Innovations and Strategic Expansions Are Accelerating the Global Water-Soluble Packaging Industry

The water-soluble packaging market is evolving rapidly due to technological innovations, sustainability initiatives, and market consolidation. In August 2025, Klöckner Pentaplast won the German Packaging Award for its kp 100% Tray2Tray® innovation, reflecting its commitment to environmentally friendly packaging solutions. The same month, Aquapak Polymers Ltd highlighted research showing 86% of FMCG brands are willing to invest in sustainable packaging, signaling strong market validation for eco-friendly materials. Additionally, studies in August 2025 demonstrated composite antimicrobial films with high bactericidal activity and excellent biodegradability.

In July 2025, Ecopol S.p.A. expanded operations in North America with a new facility in Georgia to serve the detergent and home care markets, meeting growing demand for water-soluble films. Mondi Group introduced SolmixBag, a water-soluble bag for construction materials designed to dissolve during mixing, enhancing convenience and reducing waste. Earlier in June 2024, Grove Bags launched ExIce, a water-soluble storage solution for frozen cannabis, improving preservation and preventing condensation.

Other notable developments include October 2024 collaborations between Newwen and Parrdekopper on reusable transport boxes with RFID tracking and Cortec Corporation’s August 2025 launch of Eco Works 100, a 100% USDA-certified biobased, compostable packaging film. These advances underscore the market’s focus on sustainable innovation, operational efficiency, and environmental compliance across multiple industries.

Trends and Opportunities Defining the Water-Soluble Packaging Market

Strategic Development of Bio-Based and Marine-Safe Polymer Formulations

The water-soluble packaging market is undergoing a material transformation, as producers increasingly focus on bio-based polymers derived from renewable resources such as polysaccharides, proteins, and plant-based polyesters. Academic research underscores the potential of biomass sources like seaweed-derived alginate and carrageenan, which can be processed into films that reduce reliance on petroleum feedstocks and significantly lower carbon footprints. These materials not only align with global decarbonization goals but also address the rising demand from consumers and regulators for non-toxic, natural, and renewable packaging alternatives.

A critical advancement is the shift towards marine-safe biodegradability. Unlike conventional plastics that persist in oceans for centuries, water-soluble packaging made from renewable polymers is designed to safely degrade in marine environments within weeks. Companies such as Notpla have commercialized seaweed-based edible bottles that naturally break down in 4–6 weeks, while Evoware in Indonesia has developed edible films for food packaging that either dissolve in water or biodegrade harmlessly in marine ecosystems. These innovations position water-soluble packaging as a credible response to the plastic pollution crisis, particularly in coastal and island economies where marine litter is a pressing issue.

Precision Engineering for Controlled Dissolution and Barrier Properties

A second major trend is the precision engineering of dissolution triggers to extend water-soluble packaging into diverse applications. Manufacturers now customize solubility parameters by adjusting film thickness, temperature thresholds, and agitation response, enabling tailored solutions. For instance, hot-water-soluble films are optimized for dishwasher and laundry pods, while cold-water-soluble films are being deployed in hospitality toiletries and amenity kits. This functionality ensures product safety until the precise moment of use, enhancing reliability and consumer confidence.

Simultaneously, multi-layer co-extrusion technology is advancing the barrier properties of water-soluble packaging. While single-layer films are vulnerable to moisture and gas permeability, co-extruded structures combine multiple polymer layers to deliver enhanced mechanical strength and resistance to oxygen, light, and water vapor. Technical studies confirm that these engineered films rival traditional non-soluble laminates, making them viable for protecting sensitive consumer goods, agrochemicals, and healthcare products without compromising performance or shelf life.

Addressing the Hospitality and Healthcare Sectors’ Need for Hygienic Unit-Dose Solutions

A significant opportunity for the water-soluble packaging industry lies in addressing infection control and hygiene challenges across healthcare and hospitality. In hospitals, contaminated linens or medical waste can be sealed in water-soluble laundry bags that dissolve directly in the wash cycle, preventing direct contact with pathogens. This innovation eliminates the need for manual sorting and has been formally validated by the UK’s National Health Service (NHS) as a best practice for infection prevention.

Beyond infection control, the packaging also offers operational efficiency by streamlining workflows in laundry management and waste handling. In hospitality, where hygiene has become a top priority in the post-pandemic era, unit-dose water-soluble films for cleaning chemicals and guest amenities minimize cross-contamination risks while ensuring accurate dosing. This dual functionality of hygiene and efficiency is positioning water-soluble packaging as a disruptive solution in institutional and commercial environments.

Enabling Sustainable and Precision Agriculture through Water-Soluble Pods

The agriculture sector represents another high-growth opportunity, particularly through the use of water-soluble pods for agrochemicals. These pre-measured pods dissolve directly into sprayer tanks, eliminating the need for workers to handle hazardous pesticides and fertilizers. This innovation enhances farmworker safety, reducing exposure to concentrated chemicals while improving ease of use.

Sustainability benefits are equally important. By replacing bulky, non-recyclable chemical jugs, water-soluble agrochemical packaging reduces plastic waste generation on farms. Moreover, the precision dosing enabled by these pods prevents over-application, minimizes chemical runoff, and conserves resources, directly supporting sustainable farming practices. Industry reports emphasize that this packaging format not only saves time and reduces waste but also aligns with the global push toward climate-smart agriculture, where efficiency, safety, and environmental responsibility intersect.

Competitive Landscape: Leading Companies Are Driving Sustainability and Advanced Technology in Water-Soluble Packaging

The water-soluble packaging market is dominated by key global players leveraging materials expertise, manufacturing excellence, and sustainable innovation to meet growing demand for eco-friendly solutions.

MonoSol (a Kuraray Company): Global Leader in PVOH-Based Water-Soluble Films

MonoSol specializes in PVOH films used in unit-dose detergents, agrochemicals, and personal care products. In August 2025, the company announced headquarters relocation to Portage, Indiana, reflecting its strategic growth plans. MonoSol’s core strengths include deep expertise in PVOH chemistry, brand recognition, and a global manufacturing network, enabling it to deliver innovative solutions across regions.

Aquapak Polymers Ltd.: Pioneering Marine-Safe Water-Soluble Polymers

Aquapak Polymers develops Hydropol™, a patented, water-soluble, biodegradable, and marine-safe polymer. In August 2025, the company highlighted consumer willingness to pay more for sustainable packaging and partnered with N Brown and Finisterre to replace single-use garment bags. Its strategy focuses on high-quality, compliant, and innovative packaging solutions for global markets.

Sekisui Chemical Co., Ltd.: Driving Sustainability with Vision 2030 Strategic Plan

Sekisui Chemical offers water-soluble films across construction, automotive, and specialty applications. Under Vision 2030, the company is advancing CO2-derived e-SAF technology and emphasizing innovation and sustainability. Sekisui’s core strengths include brand recognition, vertical integration, and expertise in materials science, ensuring comprehensive solutions for diverse end-use applications.

Mitsubishi Chemical Corporation: Innovating Eco-Friendly Specialty Films for Detergent Capsules

Mitsubishi Chemical provides HI-SELON™ PVOH films for detergent capsules and other applications. The company is actively investing in sustainable materials, including BioPTMG, a polyol derived from bio-feedstocks. Its strengths lie in expertise across advanced materials, sustainable innovation, and a vertically integrated business model, supporting global customer needs.

Cortec Corporation: Leading Industrially Compostable Water-Soluble Films

Cortec Corporation offers EcoSol® films for detergents, cleaners, and agricultural products. In August 2025, it introduced Eco Works 100, a 100% USDA-certified biobased, industrially compostable packaging film. Cortec focuses on sustainable material development, brand strength, and global manufacturing capabilities, ensuring its leadership in environmentally friendly packaging solutions.

Water Soluble Packaging Market Share Insights, 2025-2034

Pods & Capsules Dominate Market Share by Product Type in the Water-Soluble Packaging Industry

Pods & capsules represent the largest product type in the water-soluble packaging market, commanding around 45% share due to their role as the consumer-facing innovation driver. Their dominance originates from the laundry and dishwasher detergent sectors, where precise dosing, reduced chemical handling, and enhanced user convenience have redefined household cleaning habits. The ability to completely dissolve in water while ensuring packaging-free waste disposal aligns perfectly with sustainability expectations and circular economy goals. Additionally, expansion into bath care, agrochemicals, and other consumer applications continues to solidify this segment’s market-leading position. The success of pods highlights how convenience, safety, and functionality converge to transform packaging into a value-added feature rather than a mere container.

Household & Industrial Chemicals Lead Market Share by End-Use in the Water-Soluble Packaging Industry

Household and industrial chemicals command about 50% of the overall water-soluble packaging market, reflecting the overwhelming influence of detergent pods and related applications. This end-use category has scaled into a multi-billion-dollar product line, driven by single-dose laundry pods, dishwasher tablets, and cleaning agents that leverage dissolvable film technology to deliver consistent dosing, ease of handling, and consumer safety. The industrial side is equally important, where water-soluble formats eliminate worker exposure to hazardous cleaning chemicals while maintaining efficiency in controlled environments. This leadership underscores how consumer convenience and occupational safety together dictate packaging innovation, establishing household and industrial chemicals as the undisputed core of the industry.

European Union: PPWR, EPR Regulations, and Horizon Europe Driving Water-Soluble Adoption

The European Union water-soluble packaging market is strongly influenced by regulatory shifts and funding support aimed at reducing packaging waste and promoting sustainable alternatives. The Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025, is a cornerstone, mandating reduced packaging waste and encouraging manufacturers to switch to recyclable and reusable solutions. In line with this, Denmark will introduce Extended Producer Responsibility (EPR) on October 1, 2025, pushing companies to adopt recyclable and waste-reducing packaging.

The EU’s sustainability agenda is also backed by Horizon Europe, which provides significant funding for bio-based and compostable packaging innovations. Companies like Mondi Group are leveraging this by launching solutions such as SolmixBag, a water-soluble paper bag that dissolves in cement mixtures, addressing waste issues in construction. Additionally, the EU’s goal to cut packaging waste by 15% by 2040 compared to 2018 levels ensures long-term demand for water-soluble packaging films and bags across industrial and consumer sectors.

United States: EPA Regulations, EPR Laws, and Growth in Home-Delivery Packaging

The United States water-soluble packaging market is driven by regulatory encouragement and consumer trends toward sustainability. The U.S. Environmental Protection Agency (EPA) actively supports the use of water-soluble packaging (WSP), particularly for hazardous products like pesticides, where it reduces handler exposure and eliminates container waste. The EPA’s streamlined approval process allowing WSP to be added to pesticide registrations via notification—has accelerated manufacturer adoption.

Beyond agrochemicals, the rise of e-commerce and home delivery services is fueling demand for water-soluble unit-dose packaging in laundry pods, dish detergent tablets, and specialty consumer goods. Several states, including Maine, Maryland, and Washington, have implemented EPR laws, further driving industry compliance. Innovation is strong, with products like Grove Bags’ ExIce, a water-soluble storage solution for cannabis that dissolves without leaving microplastic residue, showcasing the move toward eco-friendly, application-specific packaging solutions.

China: Government Mandates, Expanding Domestic Capacity, and Safety Standards

The China water-soluble packaging market is expanding rapidly under strict environmental mandates. Under the 14th Five-Year Plan, effective June 1, 2025, express delivery companies must prioritize eco-friendly, reduced, and reusable packaging—boosting adoption in the booming e-commerce sector. This is coupled with strong government incentives for remanufacturing and green technologies, making water-soluble packaging a strategic growth area.

Domestic manufacturers are scaling up production to meet demand from consumer goods, agriculture, and food sectors, while regulatory oversight by the State Administration for Market Regulation (SAMR) ensures compliance. The introduction of GB 4806.1 food contact standards, which require a “complete barrier” to ensure safety, is pushing manufacturers toward advanced water-soluble films and pouches that meet both performance and safety benchmarks.

India: EPR, Plastic Ban, and Standards for Compostable Packaging

The India water-soluble packaging market is being transformed by strict regulations and sustainability-driven reforms. The Plastic Waste Management (Amendment) Rules, 2024, implemented on April 1, 2025, impose Extended Producer Responsibility (EPR) on manufacturers, brand owners, and importers, driving adoption of eco-friendly packaging formats. Additionally, India’s 2022 ban on single-use plastics has created opportunities for water-soluble packaging as a viable replacement across consumer and industrial applications.

The Food Safety and Standards Authority of India (FSSAI) is also ensuring secure packaging in food sectors, which supports the adoption of unit-dose water-soluble packs. To further standardize eco-friendly adoption, the Bureau of Indian Standards (BIS) introduced mandatory certification for compostable carry bags under IS 17088, ensuring that water-soluble and compostable solutions meet compliance. These regulations, combined with growing consumer awareness, are setting the stage for significant growth in India’s water-soluble packaging adoption.

Japan: Plastic Resource Circulation Strategy and Corporate Innovation in Water-Soluble Films

The Japan water-soluble packaging market is advancing under the Plastic Resource Circulation Strategy, which mandates that by 2025 all plastic packaging must be reusable or recyclable. This is reinforced by the Plastic Resource Circulation Promotion Law, which specifically targets 12 categories of single-use plastics for redesign or reduction. Together, these regulations are pushing industries toward water-soluble and compostable packaging alternatives.

Japanese companies are leading innovation, with Kao Corporation launching a stick-shaped powdered laundry detergent wrapped in water-soluble film, showcasing scalable applications in household goods. Additionally, the Ministry of Health, Labor and Welfare (MHLW) has established a positive list system (effective June 1, 2025) for food-contact materials, ensuring only safe materials are used. These initiatives make Japan a hub for both regulatory compliance and high-tech product innovation in water-soluble packaging.

Brazil: National Solid Waste Policy and Growth in Unit-Dose Packaging

The Brazil water-soluble packaging market is supported by the National Solid Waste Policy (PNRS), which emphasizes responsible waste disposal, recycling, and reduction. This regulatory framework is encouraging businesses to adopt eco-friendly alternatives like water-soluble films and pouches.

A key trend in Brazil is the rising use of unit-dose packaging for household cleaning products, which not only reduces large plastic container usage but also aligns with consumer demand for convenience. As sustainability regulations tighten and waste reduction gains priority, water-soluble packaging adoption is expected to accelerate across both consumer goods and industrial applications in Brazil.

Water Soluble Packaging Market Report Scope

Water Soluble Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.8 Billion

|

|

Market Size (2034)

|

$6.3 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (Bags & Pouches, Pods & Capsules, Films, Other Products), By Material (PVA, Polymers, Surfactants, Fibers, Other Materials), By Solubility (Cold Water Soluble, Hot Water Soluble), By End-Use Industry (Pharmaceuticals, Household & Industrial Chemicals, Agriculture, Food & Beverages, Water Treatment, Textile)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsubishi Chemical Group Corporation, Kuraray Co., Ltd., Sekisui Chemical Co., Ltd., Mondi Group, Aquapak Polymers Ltd., Amcor plc, Aicello Corporation, Cortec Corporation, Arrow GreenTech Ltd., TIPA Corp., Ecopol S.p.A., Jiangmen Proudly Water-soluble Plastic Co., Ltd., AMC (UK) Ltd., Noble Industries, Sphere, Monosol, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Soluble Packaging Market Segmentation

By Product Type

- Bags & Pouches

- Pods & Capsules

- Films

- Other Products

By Material

- PVA

- Polymers

- Surfactants

- Fibers

- Other Materials

By Solubility

- Cold Water Soluble

- Hot Water Soluble

By End-Use Industry

- Pharmaceuticals

- Household & Industrial Chemicals

- Agriculture

- Food & Beverages

- Water Treatment

- Textile

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Soluble Packaging Market

- Mitsubishi Chemical Group Corporation

- Kuraray Co., Ltd.

- Sekisui Chemical Co., Ltd.

- Mondi Group

- Aquapak Polymers Ltd.

- Amcor plc

- Aicello Corporation

- Cortec Corporation

- Arrow GreenTech Ltd.

- TIPA Corp.

- Ecopol S.p.A.

- Jiangmen Proudly Water-soluble Plastic Co., Ltd.

- AMC (UK) Ltd.

- Noble Industries

- Sphere

- Monosol, LLC

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to deliver in-depth insights into the global water-soluble packaging market. Our approach combines extensive primary research with industry stakeholders—including packaging manufacturers, FMCG companies, agricultural and home-care product suppliers, and regulatory bodies—alongside secondary data sources such as government regulations, trade publications, patent filings, and company reports. The analysis covers key market dynamics, including sustainability-driven adoption, polymer innovations, unit-dose applications, marine-safe materials, and regulatory frameworks across North America, Europe, China, India, Japan, and Brazil. USDAnalytics evaluates segmentation by product type, material, solubility, and end-use industry, providing actionable insights for strategic planning, product development, operational efficiency, and environmental compliance. We also assess technological advancements such as multi-layer co-extrusion films, controlled dissolution, and bio-based polymer formulations, highlighting growth opportunities in household, industrial, agricultural, healthcare, and hospitality sectors. This methodology ensures that decision-makers gain a comprehensive understanding of market trends, competitive positioning, and future prospects in water-soluble packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.