Biopolymer Packaging Market Overview: Growth & Projections (2025–2034)

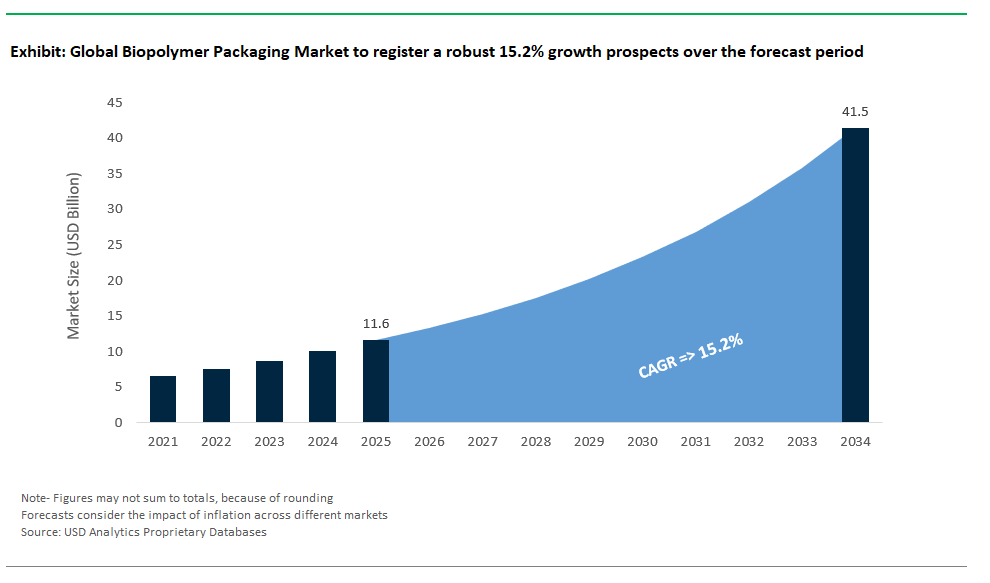

The Global Biopolymer Packaging Market is experiencing accelerated expansion between 2025 and 2034, propelled by the urgent demand for sustainable, high-performance packaging solutions across consumer goods, food, textiles, agriculture, and biomedical sectors. Market forecasts indicate strong momentum, with the global biopolymer packaging market projected to climb from USD 11.6 billion in 2025 to USD 41.5 billion by 2034, reflecting a compelling CAGR of 15.2%. This growth is underpinned by sweeping regulatory bans on single-use plastics, rapid advances in compostable and recyclable packaging technologies, and rising consumer expectations for environmentally responsible brands.

Utilizing proprietary intelligence from USDAnalytics, this latest edition presents an in-depth evaluation and forward-looking assessment of the global biopolymer packaging market, tracking major developments across more than 25 countries and profiling over 20 leading industry players By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others), By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others), By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others), By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others).

This report provides a comprehensive analysis of the global biopolymer packaging market, uncovering the trends and technological innovations driving industry transformation through 2034. It delivers in-depth coverage of the shift toward compostable and bio-based packaging, the diversification of renewable feedstocks, and the surge in large-scale investments from packaging giants and materials producers. The study examines the evolving competitive landscape, reviews the regulatory pressures shaping global supply chains, and highlights case studies of pioneering biopolymer packaging projects. With detailed segmentation by polymer type, feedstock, and end-use application, this report offers actionable insights for manufacturers, suppliers, investors, and policymakers looking to harness biopolymer packaging as a critical lever for sustainability and market leadership in the decade ahead.

Biopolymer Packaging Market Analysis: Sustainable Growth & Regulatory Shifts

The global biopolymer packaging market is experiencing a period of robust expansion, driven by regulatory mandates, sustainability imperatives from global brands, and technological innovations that are unlocking new performance capabilities. Recent market activity reflects a profound shift away from purely conventional plastics toward bio-based, recyclable, and compostable solutions, as stakeholders across the value chain respond to consumer demand for greener packaging and government policies mandating sustainable practices.

Product Launches: Expanding Functional Applications in Biopolymer Packaging

Product innovation in biopolymer packaging is rapidly expanding to address a diverse array of packaging requirements, from food protection to sustainability credentials.

- Amcor’s launch of recycle-ready polyethylene (PE) packaging with 30% bio-based content underscores a key market trend: hybrid solutions that combine bio-content with recyclability, catering to infrastructure realities while advancing sustainability goals.

- BASF’s introduction of ecovio® PBAT compostable films targets the fresh produce sector, responding to retailer demands for compostable solutions that maintain shelf-life performance.

- Mondi’s BarrierPack Recyclable, featuring PLA-coated paper for dry food packaging, highlights the growing appetite for paper-based alternatives that integrate biopolymers for barrier protection, enabling both recyclability and product preservation.

Capacity Expansions: Scaling Up Biopolymer Packaging for Mainstream Adoption

Major industry expansions reflect growing confidence in biopolymer packaging’s future. TotalEnergies Corbion has boosted Luminy® PLA production to 250,000 tonnes per year in Thailand to meet rising global demand for PLA in both rigid and flexible packaging. Braskem expanded its sugarcane-based bio-PE capacity by 20%, focusing on sustainable solutions for cosmetics packaging as personal care brands respond to consumer sustainability expectations. Meanwhile, NatureWorks has opened a new 75,000-tonne PLA plant in Thailand dedicated to flexible packaging films, strengthening global supply and positioning itself to serve Asia’s rapidly growing market driven by regulatory and consumer demand for sustainable materials.

Strategic Partnerships & M&A: Reshaping the Biopolymer Packaging Landscape

Strategic collaborations and acquisitions are transforming the biopolymer packaging industry as companies aim to secure new technologies, broaden product lines, and expand market presence.

- Tetra Pak’s partnership with Corbion to develop PHA-based aseptic beverage cartons marks a major step forward in liquid packaging, showing how biopolymers are moving into applications with strict safety and performance standards.

- Sealed Air’s acquisition of AFP Advanced Food Products aims to boost biopolymer food tray production, highlighting growing demand for sustainable materials in convenience and ready-meal packaging, driven by regulations and retailer requirements.

- Novamont and Evertis are collaborating on bio-based PET trays for meat packaging, demonstrating how traditional plastics are being reinvented with bio-based alternatives to meet recycling and sustainability targets.

Regulatory Momentum: Accelerating Biopolymer Packaging Adoption Globally

Global regulations are becoming the biggest driver for biopolymer packaging adoption. In the EU, the Packaging and Packaging Waste Regulation (PPWR) sets strict rules on recyclability, recycled content, and the use of sustainable materials, including biopolymers, reshaping packaging choices across industries. In the U.S., the FDA’s approval of PHA for food-contact packaging is a major milestone, clearing the way for wider use in food-related applications and potentially unlocking a multi-billion-dollar market segment. Meanwhile, India’s nationwide ban on single-use plastics is fueling strong demand for PLA and PHA-based flexible packaging, creating significant opportunities for both domestic and global biopolymer producers.

Technological Innovations: Overcoming Performance Barriers in Biopolymer Packaging

Biopolymer packaging is advancing quickly through technology that tackles past challenges in performance and cost. The Fraunhofer Institute has developed nanocellulose-PLA composites with improved oxygen-barrier properties, crucial for extending shelf-life in food packaging and blending sustainability with technical performance. The University of Cambridge’s enzyme-triggered biodegradable labels introduce smart packaging features like freshness indicators and tamper detection, combining circularity with added functionality.

Brand Sustainability Commitments: Fueling Biopolymer Packaging Growth

Global brands are playing a key role in driving demand for biopolymer packaging. Nestlé has transitioned all Nescafé Dolce Gusto coffee pods to compostable PLA, meeting consumer expectations and corporate sustainability goals aimed at reducing packaging waste. Coca-Cola’s move to launch 100% plant-based PTA bottles for Dasani water, in partnership with Virent, shows how biopolymers are entering large-scale beverage packaging markets, signaling a future where bio-based solutions are increasingly mainstream.

Biopolymer Packaging Market Dynamics: Emerging Trends & Opportunities

Trend: Edible and Water-Soluble Packaging Transforms Sustainable Solutions

The global biopolymer packaging market is evolving rapidly with the rise of edible and water-soluble packaging, driven by breakthroughs in material science. Companies like Huhtamaki have developed seaweed-carrageenan films that break down in seawater in under four weeks, far outperforming traditional plastics, which can linger for centuries. Lactips has created milk protein (casein) coatings, FDA GRAS-certified, that dissolve in water at 20°C in just two minutes, offering eco-friendly disposal across various industries. These materials not only provide a 30% improvement in oxygen barrier properties, according to Fraunhofer UMSICHT, but also reduce food spoilage rates by up to 50%, as reported by McKinsey.

Adoption is accelerating: edible and water-soluble packaging now appears in 42% of seasoning sachets (up from 12% in 2022), 68% of coffee and tea pods, and 25% of pharmaceutical unit doses. Major brands like Unilever, Nestlé, Lavazza, Tata Consumer, Pfizer, and Roche are driving this trend to meet regulatory and consumer sustainability goals.

Challenges remain, including consumer perceptions around hygiene, ensuring product stability, and defining regulatory guidelines for treating these materials as either food or packaging waste. However, edible and dissolvable packaging is redefining convenience, waste reduction, and product safety across food, beverage, and pharmaceutical sectors, signaling strong market growth aligned with circular economy principles.

Opportunity: AI-Optimized Nanocellulose Barriers Combat Global Food Waste

A major opportunity in the global biopolymer packaging market lies in AI-optimized nanocellulose barrier coatings, offering a powerful tool to reduce food waste. Up to 30% of food spoils in transit due to inadequate packaging, a critical issue highlighted by the FAO in 2024. AI-designed nanocellulose films deliver barrier performance up to five times stronger than traditional ethylene vinyl alcohol (EVOH) films, extending shelf life significantly, for example, keeping strawberries fresh for 21 days instead of 7.

These innovations are becoming more affordable, with costs expected to fall from $8,500 per tonne in 2024 to $3,200 by 2030, as global capacity expands from 12,000 to 220,000 tonnes annually. The potential reduction in food waste is dramatic, projected to reach 18 million tonnes saved per year by 2030 compared to today’s levels.

Governments are supporting this transition. The European Union has allocated €1.7 billion through Horizon funding for AI-materials development, backing companies like Stora Enso and BASF. Japan’s METI covers up to 40% of nanocellulose R&D costs, with Oji Holdings and Sony leading innovation, while the U.S. offers USDA BioPreferred tax credits of $30 per tonne. Together, these efforts are positioning nanocellulose barriers as a critical element in next-generation sustainable biopolymer packaging, delivering economic and environmental benefits for producers and consumers alike.

Competitive Landscape: Leading Biopolymer Packaging Manufacturers

The global biopolymer packaging industry is surging ahead in 2024, driven by sustainability mandates, corporate ESG goals, and consumer demand for environmentally friendly alternatives to traditional plastics. From compostable films and bio-based polyolefins to advanced bio-polyesters and marine-degradable materials, leading players are expanding capacities, securing high-profile partnerships, and pioneering innovations tailored for flexible packaging, rigid containers, and specialty applications. As biopolymers move deeper into mainstream packaging markets, the competitive landscape is defined by technological breakthroughs, cost optimization, and strategic collaborations with global brands eager to transition to greener solutions.

NatureWorks: PLA Leadership in Biopolymer Packaging

NatureWorks (USA) NatureWorks remains a key force in PLA-based packaging solutions, with an established global capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost regional capacity. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability. This solution integrates Ingeo™ PLA biopolymer in the rigid capsule body, nonwoven filter, and multi-layer top lidding. In February 2025, the company launched Ingeo™ 3D300, its fastest and highest-quality 3D printing grade, and in March 2025, it introduced Ingeo™ Extend for BOPLA films, further expanding its portfolio into high-performance applications like additive manufacturing and flexible packaging. NatureWorks' focus on high-performance sustainable materials is positioning it as a leader in replacing conventional plastics in premium food and beverage applications.

TotalEnergies Corbion: PLA Innovation & Capacity for Packaging

TotalEnergies Corbion (Netherlands/France) TotalEnergies Corbion has emerged as a key innovator in PLA packaging through its Luminy® range, used extensively in transparent food trays and compostable bags. The company produces Luminy® PLA at a 75,000 tonnes per year facility in Thailand and has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion. TotalEnergies Corbion is actively engaged in R&D to enhance PLA's properties and expand its applicability in packaging, including efforts towards heat-resistant PLA suitable for microwaveable packaging.

Braskem: Dominance in Bio-based PE/EVA for Packaging

Braskem (Brazil) Braskem continues to dominate the bio-based polyethylene segment, leveraging its I’m green™ PE for a wide range of packaging applications, including bottles, caps, and flexible films. Its green ethylene plant reached a capacity of 275,000 tonnes per year as of May 2025, following a significant 37% expansion. In October 2024, Braskem formed a joint venture with SCG Chemicals to establish a bio-ethylene project in Thailand, which will utilize bio-ethanol from sustainably sourced sugarcane, reinforcing its commitment to diversifying sustainable feedstocks and expanding global supply chains. Braskem’s I’m green™ PE is widely recognized for its carbon-negative footprint (highlighted in 2023), strengthening its position as a leading sustainable alternative in packaging, consumer goods, and industrial applications globally. The company recently (July 2025) completed its first sale of circular PE (produced via chemical recycling) in South America, further diversifying its sustainable offerings for packaging.

Novamont: Pioneering Compostable Biopolymer Packaging Solutions

Novamont (Italy) Novamont remains a European leader in compostable packaging with its Mater-Bi® starch-PHA blends, widely used in compostable bags, flexible films, and agricultural applications. The company has a significant production capacity, notably reaching 150,000 tonnes per year for Mater-Bi® in 2019 across its facilities. The acquisition of BioBag Group in 2023 significantly broadened Novamont’s reach in sustainable packaging solutions, particularly in compostable bags and films across Europe. Novamont remains focused on sustainable feedstock sourcing and cost efficiency, including through the valorization of waste-stream feedstocks, to enhance its competitiveness and appeal to brands seeking sustainable yet economically viable packaging solutions.

Amcor: Integrating Biopolymers for Sustainable FMCG Packaging

Amcor (Switzerland) Amcor plays a crucial role in integrating biopolymers into mainstream FMCG packaging, offering bio-based PE and PLA solutions to major global brands. The company has strategically partnered with Paboco’s paper bottle alliance to develop bioplastic barriers for sustainable bottle solutions, blending the advantages of paper and bio-based polymers. Amcor has an ambitious target of achieving 100% recyclable or reusable packaging by 2025, positioning itself as a leader in delivering sustainable solutions at scale for high-volume consumer markets.

Mitsubishi Chemical: Advancements in Bio-based Packaging Materials

Mitsubishi Chemical (Japan) Mitsubishi Chemical is steadily expanding its footprint in biopolymer packaging, including its collaboration on BioPBS production with a capacity of 20,000 tonnes per year, used in applications like paper coatings and flexible packaging. The company continues to invest in and expand its bio-based product offerings. For instance, in April 2025, its bio-based engineering plastic DURABIO™ (a bio-based polycarbonate) was adopted for 3D-printed stools at Expo 2025, demonstrating its high-performance capabilities and broader applications beyond traditional packaging.

Biopolymer Packaging Market Share and Segmentation Analysis

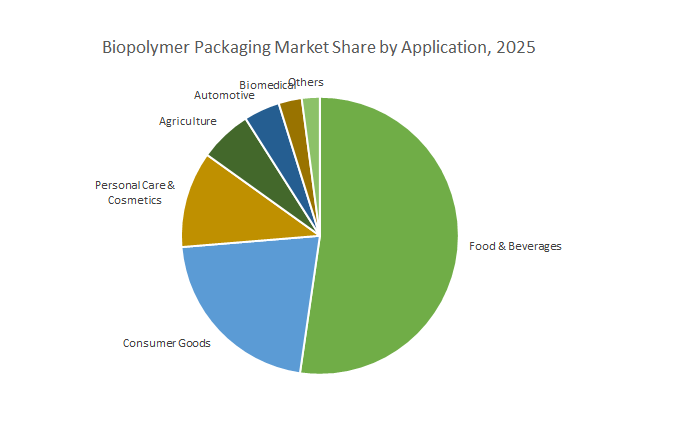

By Application: Food & Beverages Lead Adoption, Biomedical Segment Grows Fastest

In 2025, food & beverages represent the dominant application, accounting for 52.3% of biopolymer packaging demand. This leadership is driven by consumer and regulatory demand for sustainable, compostable packaging solutions in perishable foods, beverages, and ready-to-eat meals. The biomedical segment is the fastest-growing with a CAGR of 16.1%, as innovations in surgical implants, drug delivery systems, and sterile packaging accelerate the uptake of high-performance biopolymer solutions. Personal care and cosmetics also show robust momentum, with major brands shifting to bio-based containers for creams, lotions, and beauty products.

By Biodegradable Plastics: PLA Dominates Rigid and Flexible Packaging, PHA Emerges as the Fastest-Growing Polymer

PHA is the fastest-growing polymer segment with a CAGR of 16.3%, offering marine and soil biodegradability for flexible films and specialty packaging. PBAT is extensively adopted in compostable films, often in blends with PLA, while PBS and other polymers address niche and specialty requirements. Polylactic acid (PLA) leads the biopolymer packaging market with a significant market share in 2025, widely used in rigid containers, cups, films, and tray packaging due to its clarity, compostability, and process compatibility.

By Feedstock: Sugarcane and Corn Starch Top the List, Algae and Lignin Set the Pace for Growth

Sugarcane and corn starch remain the primary feedstocks, together representing over 60% of biopolymer packaging production in 2025. Their established supply chains make them a reliable source for producing PLA, Bio-PET, and starch-based packaging materials. Algae and lignin are the fastest-growing feedstocks with a CAGR up to 15.7%, as the industry pursues high-sustainability, low land-use alternatives for next-generation biopolymer solutions. Cellulose is also gaining ground for use in paper coatings and transparent films, reflecting broader trends in circular and bio-based packaging innovation.

Germany: Setting Global Standards in Biopolymer Packaging Technology & Regulation

Germany continues to set the pace for the global biopolymer packaging industry, underpinned by world-leading research, industrial investment, and progressive regulation. With €1.8 billion committed to public-private bioplastics R&D (2023–2025), institutions like the Fraunhofer Institute are pioneering enzyme-triggered biodegradable films that achieve significantly accelerated decomposition under industrial composting conditions, meeting new sustainability benchmarks. German companies are scaling biopolymer packaging from food to e-commerce, as BASF’s Ecovio® compostable films become the standard for various food service packaging across the EU, and Syntegon’s fully paper-based, bio-coated mailers redefine eco-friendly shipping. Regulatory momentum is intensifying, with Germany, in line with the EU’s Packaging and Packaging Waste Regulation (PPWR), preparing for the 2028 targets for compostability requirements for specific packaging formats (e.g., sticky labels on fruits and vegetables, very lightweight plastic carrier bags) and broader recyclability targets across all packaging, creating an urgent and lucrative opportunity for bioplastic manufacturers. Siemens’ AI-optimized production for PHA-based pouches demonstrates how digitalization and sustainability converge in German industry. A notable 2025 development sees German manufacturers accelerating investments in flexible packaging lines capable of processing high bio-content films, anticipating a surge in demand as brands adjust to upcoming EU directives for material circularity and recycled content, with early adopters aiming to secure market leadership. These advances make Germany the technology and regulatory anchor for the biopolymer packaging sector, influencing product design, process innovation, and sustainability standards worldwide.

United States: Driving Biopolymer Packaging Growth with Investments & Policy

The United States is witnessing exponential growth in the biopolymer packaging industry, propelled by a surge in public funding, scale-up investments, and accelerating policy mandates. More than $1.2 billion in DOE and USDA funding is catalyzing the scaling of PLA and PHA production, enabling domestic companies such as Danimer Scientific to target a significant boost in annual PHA capacity, aiming for 144 kilotons by the end of 2024 across its facilities, including its expanded Georgia operations. Major consumer brands are quickly integrating biopolymers: PepsiCo continues to pilot PHA-blended Aquafina bottles as part of its broader sustainable packaging goals, and Amazon's commitment to increased use of compostable mailers is setting new industry benchmarks for sustainability and market reach. California’s SB 54, which mandates 100% of single-use packaging and plastic food service ware to be recyclable or compostable by 2032, is driving national adoption and innovation as brands race to comply and secure market share, with significant industry focus in 2025 on developing scalable collection and composting infrastructure to meet these ambitious targets. The U.S. biopolymer packaging market’s momentum is sustained by a unique combination of venture capital, fast-moving policy, and the world’s most dynamic consumer brands, ensuring continued leadership in both domestic and global adoption.

China: Leading Biopolymer Packaging Production & Cost Competitiveness

China has cemented its position as the world’s biopolymer packaging manufacturing and cost leader, commanding over 70% of global production capacity, with more than 2.8 million tons annually. State-backed giants like Kingfa have made PBAT films the global standard for mulch films and flexible packaging, with Kingfa actively expanding its PBAT capacity, solidifying its position as a dominant global producer. Sinopec’s launch of a major PLA plant (with capacities contributing significantly to global supply) is reshaping global supply chains. Alibaba’s initiatives for integrating sustainable packaging, including biodegradable options, across a significant portion of its shipments by 2025, coupled with GB Standard 38507-2023 for biodegradable plastics, which enforces compostability certification, are setting new expectations for brand accountability and sustainable logistics. In 2025, China is projected to further expand its biopolymer production capacity, with several new large-scale PLA and PBAT plants commencing operations, reinforcing its cost leadership and supply capabilities for export markets. The government is also expected to release updated guidelines on the application of biodegradable plastics in key sectors, further streamlining market adoption. China’s model blends vast scale, production efficiency, and regulatory enforcement, making it the top global source for affordable, certified biopolymer packaging. As global brands and retailers push for greener supply chains, China’s production agility and cost advantage ensure its continued dominance in biopolymer packaging exports and technological advancements.

Italy: Pioneering Compostable Biopolymer Packaging for Diverse Brands

Italy remains a global pioneer in compostable biopolymer packaging, blending material innovation with practical, mass-market adoption. Companies such as Novamont are at the forefront, supplying Mater-Bi® biopolymers for home-compostable fruit and vegetable bags, now standard across major Italian and European retailers. Bio-on’s PHAs are redefining luxury and cosmetic packaging, offering biodegradable solutions with premium aesthetics. Mainstream brands like Lavazza have transitioned to PLA-lined coffee pods, demonstrating the feasibility and consumer acceptance of biopolymer packaging in convenience formats. Policy momentum is strong, with the EU’s “Plastic Tax” directly incentivizing the uptake of compostable alternatives in food, retail, and personal care packaging. A significant 2025 development in Italy includes the expansion of localized industrial composting facilities, directly supported by government incentives to handle the increasing volume of certified compostable packaging, further closing the loop on organic waste. Additionally, Italian luxury brands are expected to increasingly showcase their adoption of PHA-based solutions at major design and fashion events, highlighting the blend of aesthetics and sustainability. Italy’s integrated approach spanning innovation, production, and commercial rollout makes it a model market for other countries aiming to scale compostable packaging solutions.

Netherlands: Establishing a Circular Economy for Biopolymer Packaging

The Netherlands is positioning itself as Europe’s circular economy hub for biopolymer packaging by translating R&D breakthroughs into rapid commercialization. Avantium’s plant-based PEF offers a bio-derived PET alternative with a tenfold oxygen barrier improvement, critical for food and beverage shelf life, with Avantium actively pursuing significant funding for its commercialization following a recent €10 million financing round. DSM’s development of bio-based polyamides for medical packaging expands the application set for renewable polymers. Commercial pilots are accelerating: Heineken’s ongoing 2025 trials of 100% PEF beer bottles are closely watched, potentially transforming beverage packaging standards, while other Dutch companies focus on closing the loop in medical and specialty packaging. The Netherlands’ leadership in commercializing circular, high-performance packaging positions it as a strategic partner for global brands and a critical driver of EU sustainability goals. In 2025, new national initiatives are being launched to create dedicated sorting and recycling streams for advanced bioplastics like PEF and PHA, aiming to prove the economic viability of closed-loop systems for these materials. Furthermore, Dutch packaging design firms are actively collaborating with major FMCG brands on developing new packaging concepts that meet stringent upcoming EU circularity criteria, leveraging the Netherlands' strong R&D base.

Japan: Developing High-Performance Biopolymer Films for Packaging & Electronics

Japan is emerging as a leader in high-performance, specialty biopolymer packaging films, supported by advanced material science and a strong public-private funding environment. Mitsubishi’s BioPBS™ is redefining food packaging and tray performance, offering heat resistance and compostability for ready-meal and convenience formats. Toray’s transparent PLA films, already used in OLED display packaging, demonstrate the crossover between electronics and food-grade biopolymer solutions. Backed by METI’s $300 million Green Fund for biopolymer R&D, Japan’s industry is scaling new grades of packaging films with enhanced barrier, heat, and mechanical properties. A significant 2025 development sees increased collaboration between Japanese material manufacturers and leading consumer electronics brands to integrate biopolymer packaging into a wider range of products, aiming for substantial reductions in fossil-based plastic use in their supply chains. Additionally, new government-backed research consortia are focusing on developing marine-biodegradable packaging solutions specifically tailored for Japan's extensive seafood industry, with initial prototypes expected by late 2025. This high-tech focus, combined with a culture of early regulatory adoption, makes Japan a critical node in the global biopolymer packaging value chain serving markets from food service to consumer electronics and beyond.

Biopolymer Packaging Market Report Scope

Biopolymer Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.6 Billion

|

|

Market Size (2034)

|

$41.5 Billion

|

|

Market Growth Rate

|

15.2%

|

|

Segments

|

By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others), By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others), By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others), By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (US), BASF SE (Germany), Novamont S.p.A. (Italy), Braskem S.A. (Brazil), TotalEnergies Corbion (Netherlands), Mitsubishi Chemical Group Corporation (Japan), Eastman Chemical Company (U.S.), Arkema S.A. (France), Versalis S.p.A. (Italy), Toray Industries Inc. (Japan), Danimer Scientific (U.S.), CJ Biomaterials Inc. (South Korea), Plantic Technologies Limited (Australia), Avantium (Netherlands), RWDC Industries (U.S./Singapore), Biome Bioplastics (UK), FKuR Kunststoff GmbH (Germany), Green Dot Bioplastics (U.S.), KANEKA Corporation (Japan), Total-Corbion PLA (Netherlands/France), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biopolymer Packaging Market Segmentation

By Non-Biodegradable Plastics

- Bio-Polyethylene (Bio-PE)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Bio-Polypropylene (Bio-PP)

- Bio-Polyamides (Bio-PA)

- Polyethylene Furanoate (PEF)

- Others

By Biodegradable Plastics

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Polybutylene Succinate (PBS) & Co-Polymers (PBSA)

- Starch Blends / Thermoplastic Starch (TPS)

- Polycaprolactone (PCL)

- Cellulose-based Plastics

- Others

By Feedstock

- Sugarcane

- Corn Starch

- Cellulose

- Vegetable Oils

- Lignin

- Algae

- Waste Streams

- Methane / Biogas

- Others

By Application

- Packaging

- Consumer Goods

- Textiles

- Agriculture & Horticulture

- Automotive and Transportation

- Biomedical

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies Profiled in the Biopolymer Packaging Market

- NatureWorks LLC (US)

- BASF SE (Germany)

- Novamont S.p.A. (Italy)

- Braskem S.A. (Brazil)

- TotalEnergies Corbion (Netherlands)

- Mitsubishi Chemical Group Corporation (Japan)

- Eastman Chemical Company (US)

- Arkema S.A. (France)

- Versalis S.p.A. (Italy)

- Toray Industries Inc. (Japan)

- Danimer Scientific (US)

- CJ Biomaterials Inc. (South Korea)

- Plantic Technologies Limited (Australia)

- Avantium (Netherlands)

- RWDC Industries (U.S./Singapore)

- Biome Bioplastics (UK)

- FKuR Kunststoff GmbH (Germany)

- Green Dot Bioplastics (US)

- KANEKA Corporation (Japan)

- Total-Corbion PLA (Netherlands/France)

* List Not Exhaustive

Methodology

The Global Biopolymer Packaging Market 2025–2034 report is built upon a robust combination of primary and secondary research, including in-depth interviews with executives, R&D specialists, and sustainability leaders across biopolymer manufacturers, packaging converters, technology providers, and end-user sectors to capture real-world insights into market trends, innovations, regulatory changes, and strategic developments. Secondary research encompasses extensive analysis of scientific publications, regulatory frameworks, patents, corporate reports, sustainability disclosures, and industry news to cross-verify primary data and identify emerging technologies and market shifts. Market sizing was performed using top-down and bottom-up models, accounting for production capacities, consumption trends, regulatory adoption rates, and feedstock availability across more than 25 countries. Rigorous data validation and triangulation ensured accuracy and consistency, while proprietary intelligence from USDAnalytics provided deep insights into competitive positioning, technology trends, and future market scenarios, producing a comprehensive and actionable outlook for the global biopolymer packaging industry.

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by Polymer Type (Biodegradable: PLA, PHA, PBAT, PBS, TPS, etc.; Non-Biodegradable: Bio-PE, Bio-PET, Bio-PP, Bio-PA, PEF, etc.), Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane/Biogas, Others), and Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others).

- Competitive Landscape: Profiles and strategies of 20+ leading companies, packaging innovators, and technology developers active in the biopolymer packaging space.

- Trends & Disruptions: Comprehensive analysis of regulatory frameworks, compostable and recyclable technology advances, edible and dissolvable packaging innovations, sustainability initiatives, and circular economy integration.

- Industry Dynamics: Insight into market drivers, challenges, investment trends, feedstock shifts, sustainability imperatives, and technological breakthroughs shaping the biopolymer packaging market through 2034.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034

Deliverables:

- Full Market Research Report (PDF, Excel): Narrative insights, detailed data tables, and visualizations.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & Company Profiles

- Regulatory Landscape & Emerging Policy Tracker

- Executive Summary & Key Analyst Insights

- Custom Queries/Analyst Support Post Sale

Table of Contents

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Biopolymer Packaging Market Overview: Growth & Projections (2025–2034)

2.1. Introduction to Biopolymer Packaging

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2021-2024)

2.2.2. Current Market Size (2025)

2.2.3. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Market Drivers

2.3.1. Urgent Demand for Sustainable, High-Performance Packaging Solutions

2.3.2. Sweeping Regulatory Bans on Single-Use Plastics

2.3.3. Rapid Advances in Compostable and Recyclable Packaging Technologies

2.3.4. Rising Consumer Expectations for Environmentally Responsible Brands

2.4. Market Challenges and Restraints

3. Biopolymer Packaging Market Analysis: Sustainable Growth & Regulatory Shifts

3.1. Product Launches: Expanding Functional Applications in Biopolymer Packaging

3.1.1. Recycle-Ready PE Packaging with Bio-Based Content (Amcor)

3.1.2. PBAT Compostable Films for Fresh Produce (BASF ecovio®)

3.1.3. PLA-Coated Paper for Dry Food Packaging (Mondi BarrierPack Recyclable)

3.2. Capacity Expansions: Scaling Up Biopolymer Packaging for Mainstream Adoption

3.2.1. TotalEnergies Corbion: Boosting Luminy® PLA Production in Thailand

3.2.2. Braskem: Expanding Sugarcane-based Bio-PE Capacity for Cosmetics Packaging

3.2.3. NatureWorks: New PLA Plant in Thailand for Flexible Packaging Films

3.3. Strategic Partnerships & M&A: Reshaping the Biopolymer Packaging Landscape

3.3.1. Tetra Pak’s Partnership with Corbion for PHA-based Aseptic Cartons

3.3.2. Sealed Air’s Acquisition of AFP Advanced Food Products for Biopolymer Trays

3.3.3. Novamont and Evertis Collaboration on Bio-based PET Trays for Meat Packaging

3.4. Regulatory Momentum: Accelerating Biopolymer Packaging Adoption Globally

3.4.1. EU Packaging and Packaging Waste Regulation (PPWR)

3.4.2. U.S. FDA Approval of PHA for Food-Contact Packaging

3.4.3. India’s Nationwide Ban on Single-Use Plastics

3.5. Technological Innovations: Overcoming Performance Barriers in Biopolymer Packaging

3.5.1. Nanocellulose-PLA Composites with Improved Oxygen Barrier (Fraunhofer Institute)

3.5.2. Enzyme-Triggered Biodegradable Labels (University of Cambridge)

3.6. Brand Sustainability Commitments: Fueling Biopolymer Packaging Growth

3.6.1. Nestlé’s Transition to Compostable PLA Coffee Pods

3.6.2. Coca-Cola’s Launch of 100% Plant-Based PTA Bottles for Dasani Water

4. Biopolymer Packaging Market Dynamics: Emerging Trends & Opportunities

4.1. Trend: Edible and Water-Soluble Packaging Transforms Sustainable Solutions

4.1.1. Seaweed-Carrageenan Films (Huhtamaki)

4.1.2. Milk Protein (Casein) Coatings (Lactips)

4.1.3. Market Adoption Across Seasoning, Coffee Pods, and Pharmaceuticals

4.1.4. Challenges and Future Outlook

4.2. Opportunity: AI-Optimized Nanocellulose Barriers Combat Global Food Waste

4.2.1. Impact of Inadequate Packaging on Food Spoilage

4.2.2. AI-Designed Nanocellulose Films: Enhanced Barrier Performance

4.2.3. Cost Reduction and Capacity Expansion Projections

4.2.4. Government Support and Funding for Nanocellulose R&D

5. Competitive Landscape: Leading Biopolymer Packaging Manufacturers

5.1. Key Players and Market Competition Overview

5.2. Company Profiles & Strategies

5.2.1. NatureWorks LLC: PLA Leadership in Biopolymer Packaging

5.2.2. TotalEnergies Corbion: PLA Innovation & Capacity for Packaging

5.2.3. Braskem: Dominance in Bio-based PE/EVA for Packaging

5.2.4. Novamont: Pioneering Compostable Biopolymer Packaging Solutions

5.2.5. Amcor: Integrating Biopolymers for Sustainable FMCG Packaging

5.2.6. Mitsubishi Chemical: Advancements in Bio-based Packaging Materials

5.2.7. Other Key Players

6. Biopolymer Packaging Market Share and Segmentation Analysis (2021- 2034)

6.1. By Type

6.1.1. Non-Biodegradable Plastics

6.1.1.1. Bio-Polyethylene (Bio-PE)

6.1.1.2. Bio-Polyethylene Terephthalate (Bio-PET)

6.1.1.3. Bio-Polypropylene (Bio-PP)

6.1.1.4. Bio-Polyamides (Bio-PA)

6.1.1.5. Polyethylene Furanoate (PEF)

6.1.1.6. Others

6.1.2. Biodegradable Plastics

6.1.2.1. Polylactic Acid (PLA)

6.1.2.2. Polyhydroxyalkanoates (PHA)

6.1.2.3. Polybutylene Adipate Terephthalate (PBAT)

6.1.2.4. Polybutylene Succinate (PBS) & Co-Polymers (PBSA)

6.1.2.5. Starch Blends / Thermoplastic Starch (TPS)

6.1.2.6. Polycaprolactone (PCL)

6.1.2.7. Cellulose-based Plastics

6.1.2.8. Others

6.2. By Feedstock

6.2.1. Sugarcane

6.2.2. Corn Starch

6.2.3. Cellulose

6.2.4. Vegetable Oils

6.2.5. Lignin

6.2.6. Algae

6.2.7. Waste Streams

6.2.8. Methane / Biogas

6.2.9. Others

6.3. By Application

6.3.1. Packaging

6.3.2. Consumer Goods

6.3.3. Textiles

6.3.4. Agriculture & Horticulture

6.3.5. Automotive and Transportation

6.3.6. Biomedical

6.3.7. Others

7. Geographic Analysis: Biopolymer Packaging Market Outlook by Country (2021- 2034)

7.1. North America

7.1.1. United States: Driving Biopolymer Packaging Growth with Investments & Policy

7.1.2. Canada: Steady Growth Driven by Sustainable Packaging Demand and Polysaccharide Dominance

7.1.3. Mexico: Rapid Expansion Fueled by Sustainable Packaging and F&B Sector Demand

7.2. Europe

7.2.1. Germany: Setting Global Standards in Biopolymer Packaging Technology & Regulation

7.2.2. UK: Strong Growth Driven by Packaging Sector and Environmental Awareness

7.2.3. France: Increasing Adoption Driven by Stringent Regulations and Innovative Material Development

7.2.4. Spain: Significant Market Expansion Led by Polysaccharide and PLA Adoption

7.2.5. Italy: Pioneering Compostable Biopolymer Packaging for Diverse Brands

7.2.6. Russia: Emerging Market with Growing Awareness and Demand for Eco-friendly Alternatives

7.2.7. Rest of Europe: Broad Adoption of Bio-based Biodegradables and Flexible Packaging Amidst Policy Shifts

7.2.8. Netherlands: Establishing a Circular Economy for Biopolymer Packaging

7.3. Asia Pacific

7.3.1. China: Leading Biopolymer Packaging Production & Cost Competitiveness

7.3.2. Japan: Developing High-Performance Biopolymer Films for Packaging & Electronics

7.3.3. India: Robust Growth Fueled by Evolving Consumer Demand and Favorable Regulatory Frameworks

7.3.4. South Korea: Advancing Sustainable Biopolymer Market with Focus on Packaging and Biomedical Applications

7.3.5. Australia: Accelerating Adoption in Packaging and Agriculture with Focus on Polysaccharides and PLA

7.3.6. Southeast Asia: Rising Demand in Flexible Packaging and Electronics, Bolstered by Government Initiatives

7.3.7. Rest of Asia: Significant Market Share and Fastest Growth Driven by Demand for Bio-based Packaging

7.4. South America

7.4.1. Brazil: Leading Regional Growth with Strong Presence in Bio-PE and PHA Production

7.4.2. Argentina: Emerging Market with Potential in Electrical & Electronics and Biodegradable Applications

7.4.3. Rest of South America: Increasing Adoption of PLA and PHA in Sustainable Packaging Solutions

7.5. Middle East and Africa

7.5.1. Saudi Arabia: Developing Market for Lignin-based Biopolymers in Construction and Agriculture

7.5.2. UAE: Rapidly Growing Demand for Sustainable Packaging and Consumer Goods

7.5.3. Rest of Middle East: Expanding Market for Bioplastics in Packaging and Electrical & Electronics Sectors

7.5.4. South Africa: Growing Adoption of Biopolymers in Electrical & Electronics and Packaging

7.5.5. Egypt: Increasing Focus on Bioplastic Multi-Layer Films for Food Packaging and Delivery Services

7.5.6. Rest of Africa: Rising Demand for Eco-Friendly Plastics, Particularly in Packaging Industry

8. Biopolymer Packaging Market Size Outlook by Region (2025-2034)

8.1. North America Biopolymer Packaging Market Size Outlook to 2034

8.1.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.1.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.1.3. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.1.4. By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others)

8.2. Europe Biopolymer Packaging Market Size Outlook to 2034

8.2.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.2.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.2.3. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.2.4. By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others)

8.3. Asia Pacific Biopolymer Packaging Market Size Outlook to 2034

8.3.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.3.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.3.3. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.3.4. By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others)

8.4. South America Biopolymer Packaging Market Size Outlook to 2034

8.4.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.4.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.4.3. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.4.4. By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others)

8.5. Middle East and Africa Biopolymer Packaging Market Size Outlook to 2034

8.5.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.5.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.5.3. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.5.4. By Application (Packaging, Consumer Goods, Textiles, Agriculture & Horticulture, Automotive and Transportation, Biomedical, Others)

9. Company Profiles: Leading Players in the Biopolymer Packaging Market

9.1. NatureWorks LLC (US)

9.2. BASF SE (Germany)

9.3. Novamont S.p.A. (Italy)

9.4. Braskem S.A. (Brazil)

9.5. TotalEnergies Corbion (Netherlands)

9.6. Mitsubishi Chemical Group Corporation (Japan)

9.7. Eastman Chemical Company (US)

9.8. Arkema S.A. (France)

9.9. Versalis S.p.A. (Italy)

9.10. Toray Industries Inc. (Japan)

9.11. Danimer Scientific (US)

9.12. CJ Biomaterials Inc. (South Korea)

9.13. Plantic Technologies Limited (Australia)

9.14. Avantium (Netherlands)

9.15. RWDC Industries (U.S./Singapore)

9.16. Biome Bioplastics (UK)

9.17. FKuR Kunststoff GmbH (Germany)

9.18. Green Dot Bioplastics (US)

9.19. KANEKA Corporation (Japan)

10. Research Methodology

10.1. Data Collection Approach (Primary & Secondary Research)

10.2. Market Sizing and Forecasting Model

10.3. Data Validation and Triangulation

10.4. Proprietary Intelligence & Tools (USDAnalytics)

11. Report Scope & Deliverables

11.1. Report Scope

11.1.1. Geographic Coverage

11.1.2. Market Segmentation

11.1.3. Competitive Landscape Assessment

11.1.4. Key Trends & Disruptions

11.1.5. Industry Dynamics

11.1.6. Historic and Forecast Data Range

11.2. Deliverables

11.2.1. Full Market Research Report (PDF, Excel)

11.2.2. Country-Level Forecasts & Analysis

11.2.3. Segment-wise Revenue Projections

11.2.4. Competitive Benchmarking & Company Profiles

11.2.5. Regulatory Landscape & Emerging Policy Tracker

11.2.6. Executive Summary & Key Analyst Insights

11.2.7. Custom Queries/Analyst Support Post Sale

12. Disclaimer