Starch-Based Packaging Market Size, Overview, and Growth Outlook (2025–2034)

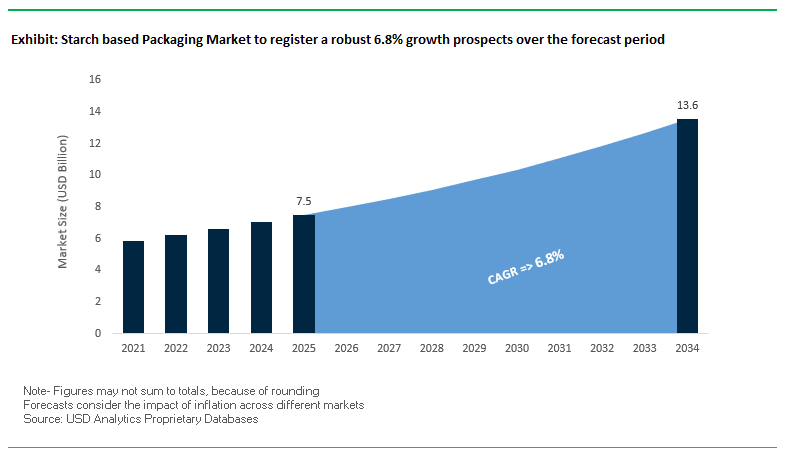

Starch-Based Packaging Market Poised for Robust Growth from $7.5 Billion in 2025 to $13.6 Billion by 2034 Driven by Sustainability and Regulatory Push

The global starch-based packaging market is projected to grow from $7.5 billion in 2025 to $13.6 billion by 2034, achieving a CAGR of 6.8%. Leveraging renewable and biodegradable materials derived from corn, potato, and cassava, starch-based packaging is emerging as a key eco-friendly alternative to conventional plastics, particularly amid stringent single-use plastic bans and environmental regulations.

Key Insights for Industry Professionals:

- Government regulations and single-use plastic bans are major drivers in Europe, North America, and other markets.

- Material performance enhancements are enabling starch-based packaging to compete with conventional plastics in strength, flexibility, and moisture resistance.

- Circular economy adoption is promoted by compostable packaging that returns nutrients to soil, particularly in foodservice and e-commerce applications.

- Diverse end-use applications now include films, disposable cutlery, trays, and protective void-fill materials.

- Corporate sustainability strategies are increasingly aligned with starch-based packaging to enhance brand image and reduce environmental impact.

The industry is actively advancing R&D, material innovation, and bio-based formulations to address both environmental responsibility and commercial applicability, positioning starch-based packaging as a core segment in sustainable packaging markets.

Market Analysis: Strategic Developments in Starch-Based Packaging Reflect Focus on Innovation, Circular Economy, and Regulatory Compliance

The starch-based packaging market is experiencing significant growth driven by technological innovation, sustainability, and expanding applications. In August 2025, Constantia Flexibles partnered with Syntegon to showcase high-performance mono-material pouches, signaling a strong industry pivot toward recyclable and eco-friendly materials. The same month, an academic review highlighted the use of advanced additives such as nanoparticles and essential oils to enhance mechanical and antimicrobial properties of starch-based films, reflecting the continuous focus on material performance.

Innovation in functional applications is also shaping market dynamics. In July 2025, a U.S. university study on controlled-release insecticide formulations demonstrated trends in designing advanced starch-based packaging for agrochemical applications. In May 2025, Tate & Lyle launched a clean-label starch portfolio for sauces and dressings in Europe, addressing demand for reduced synthetic ingredients. In April 2025, Roquette introduced plant-based coating systems for pharmaceuticals and nutraceuticals, extending starch applications beyond traditional food packaging.

Capacity expansion and product development are crucial for market scaling. In March 2025, Ingredion expanded its modified starch plant in India to meet growing demand from snack and bakery segments. February 2025 saw Cargill introduce thermoplastic starch (TPS) pellets for biodegradable cutlery and mulch films, highlighting high-value end-use applications. In January 2025, ADM launched low-glycemic starches for diabetic-friendly foods and partnered with a pharmaceutical company for binder-grade starch, reflecting the diverse industrial applications driving market adoption.

Trends and Opportunities Reshaping the Starch-Based Packaging Market

Enhancement of Material Properties for Broader Application

One of the most significant trends in the starch-based packaging market is the targeted improvement of material performance to overcome the inherent limitations of starch as a standalone polymer. Traditionally, starch films have suffered from brittleness, poor mechanical strength, and weak barrier properties, restricting their use in demanding packaging applications. However, recent scientific breakthroughs have demonstrated that reinforcing starch with cellulose nanofibers and other natural fillers dramatically improves tensile strength and elasticity. These composites not only maintain biodegradability but also make starch-based films suitable for packaging food, beverages, and consumer goods that require more robust protection.

Another critical area of advancement is barrier enhancement. To protect packaged goods from moisture and oxygen—two of the most damaging factors for product shelf life—researchers are blending starch with other biopolymers and nanoparticles. These new composites reduce water vapor permeability and oxygen transmission rates to levels comparable with certain petroleum-based plastics, ensuring starch packaging can effectively compete with conventional solutions. This dual improvement in mechanical resilience and functional barrier performance positions starch packaging as a serious contender in mainstream applications.

Strategic Partnerships for Integrated Biopolymer Production

The starch-based packaging industry is also seeing a surge in strategic partnerships and collaborations designed to scale up biopolymer production and ensure supply security. For example, Danimer Scientific partnered with a global chemical company in December 2020 to co-develop biodegradable coatings for the paper and board sector. Such collaborations highlight the industry’s move toward farm-to-packaging models, where agricultural outputs are directly integrated into the value chain, ensuring steady availability of starch-derived materials.

Another noteworthy development is the use of agricultural byproducts as feedstock. Companies like UKHI are pioneering the transformation of crop waste into functional starch-based polymers, effectively creating a regenerative bioeconomy. This approach not only reduces costs and carbon footprint but also enhances resilience against supply chain volatility tied to fossil fuel-based plastics. The ability to leverage localized, renewable raw materials further strengthens the sustainability credentials of starch packaging, aligning with global efforts to reduce dependency on petrochemicals.

Development of Home-Compostable Certified Packaging Solutions

One of the most immediate opportunities in starch-based packaging is the creation of home-compostable certified solutions, addressing the lack of widespread industrial composting infrastructure. Unlike PLA and other bioplastics that require high-temperature industrial composting, starch-based materials can be engineered to break down under typical household composting conditions. Companies such as EcoBharat are already producing cornstarch-based products certified to decompose within 180 days in a home compost pit, providing consumers with a clear, accessible end-of-life option for single-use items.

The key challenge lies in balancing performance with compostability. Innovations like BASF’s ecovio®, which combines starch polymers with PBAT, demonstrate that it is possible to achieve mechanical performance comparable to polypropylene (PP) while maintaining certified compostability. These materials are already being used in rigid and flexible packaging, including bags, trays, and films, proving that functional home-compostable solutions can deliver both durability and sustainability.

Replacement of Petrochemical Coatings with Starch-Based Barriers

Another high-potential opportunity is the replacement of petroleum-based coatings on paper and board with starch-based barrier systems. Conventional plastic coatings such as PE and PET provide moisture, oil, and grease resistance but render paper packaging non-recyclable or non-compostable. In contrast, starch-based coatings are bio-based, biodegradable, and recyclable, making them a truly circular alternative. For instance, Cargill™ Barrier Coatings, launched as a starch-derived solution, are designed to deliver strong grease and oil resistance while allowing full recyclability of paper packaging.

This innovation supports the broader “paperization” trend, where brands are shifting from plastic to paper-based formats. A technical review of starch-based coatings highlights their adaptability, noting that they can be engineered for different food categories, from dry snacks to takeaway containers. By enabling the creation of fully sustainable paper packaging systems, starch-based coatings not only address consumer demand for plastic-free options but also align with tightening regulatory frameworks on single-use plastics.

Competitive Landscape: Leading Companies Are Driving Starch-Based Packaging Growth Through Innovation, Sustainability, and Advanced Materials

The starch-based packaging industry is shaped by companies leveraging materials science, sustainable solutions, and manufacturing expertise to deliver high-performance, environmentally responsible packaging.

Ingredion Incorporated: Expanding Global Capacity to Deliver High-Performance Starch-Based Packaging

Ingredion develops advanced starches for food, beverage, and industrial applications, including sustainable barrier starches for paper and board with grease and oil resistance. In March 2025, the company expanded its modified starch plant in India, supporting the growing snack and bakery segments. Ingredion’s strengths lie in extensive R&D capabilities, a diverse starch portfolio, and a robust supply chain, with a strategic focus on innovative, sustainable ingredient solutions for global customers.

Cargill, Incorporated: Pioneering Thermoplastic Starch Solutions for Biodegradable Packaging

Cargill produces a range of starches, including TPS pellets for cutlery, mulch films, and paper packaging applications. In February 2025, it introduced thermoplastic starch pellets for biodegradable applications. Cargill’s strengths include a global supply chain, strong R&D capabilities, and bio-based material expertise, with a strategy aimed at sustainable innovation and responsible food development.

Mondi Group: Leveraging Paper-Based and Starch-Coated Packaging for Eco-Friendly Alternatives

Mondi offers paper-based pouches and bio-based coatings incorporating starch as a sustainable alternative to plastics. In June 2025, it partnered with Saga Nutrition to launch paper-based pet food pouches. Mondi’s strengths lie in sustainability-focused R&D, customizable packaging solutions, and material innovation, guided by its “Growing with Purpose” strategy to provide functional, environmentally responsible packaging.

BASF SE: Enabling High-Performance Biopolymer Solutions to Enhance Starch-Based Packaging

BASF provides key materials such as ecoflex® and ecovio® biopolymers often blended with starch to produce compostable films and packaging formats. The company invests heavily in R&D for bio-based polymers and performance improvement, focusing on high-performance barrier films for food and beverage applications. BASF’s strengths include chemical manufacturing expertise, extensive material portfolios, and vertically integrated operations, with a strategic emphasis on innovation and sustainability across the supply chain.

Starch based Packaging Market Share Insights, 2025-2034

Bags & Pouches Hold the Largest Market Share by Product Type in Starch-Based Packaging

Bags and pouches command 30% of the starch-based packaging industry, leading the segment due to their ability to directly replace conventional single-use plastic bags—the most heavily legislated packaging type worldwide. Compostable starch-based shopping bags, bakery bags, and produce pouches align with regulatory bans and consumer preference for eco-friendly alternatives, ensuring steady market growth. Their cost-effectiveness, relative ease of production, and strong consumer acceptance make them the most scalable starch-based application. While trays, containers, and loose-fill have carved out important niches in foodservice and protective packaging, starch-based bags and pouches dominate because they address the largest and most visible pain point in global plastic pollution: the disposable bag.

Food & Beverages Dominate Market Share by End-Use Industry in Starch-Based Packaging

Food and beverages account for nearly 75% of the starch-based packaging market, making this sector the overwhelming growth driver. The dominance stems from a convergence of regulatory restrictions on EPS foam trays, consumer demand for sustainable food packaging, and the natural fit of starch-based materials for short-life, single-use applications. Compostable trays, clamshells, and pouches made from starch-based biopolymers are increasingly replacing polystyrene and PET in quick-service restaurants, grocery retail, and fresh produce packaging. The sector’s focus on reducing foodservice waste aligns perfectly with starch-based materials’ compostability, enabling a closed-loop end-of-life solution. While personal care, healthcare, and agriculture represent emerging niches, the volume and regulatory urgency of the food and beverage industry make it the uncontested anchor of this market.

European Union: PPWR, Compostability, and Emerging Marine-Safe Films

The European Union starch-based packaging market is heavily influenced by the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates the inclusion of recycled content in all packaging plastics by 2030. For starch-based solutions, this regulatory push translates into increased investments in compostable and recyclable systems supported by advanced recycling and recovery infrastructure. Alongside PPWR, the Ecodesign for Sustainable Products Regulation (ESPR) is promoting the adoption of mono-material flexible packaging that can be easily recycled or composted, positioning starch-based packaging as a strong substitute for multi-layer plastics.

The region is also preparing for the rollout of Digital Product Passports, which will provide detailed information on biodegradability, material composition, and compliance. Southern European countries such as Italy and Spain are pioneering compostable food containers and films, driven by local composting infrastructure investments and partnerships with startups. Innovations such as marine-safe film technology and dual-layered cellulose packaging are gaining commercial traction in perishable food sectors. The VTT Technical Research Centre of Finland is further advancing the space with pilot roll-to-roll production that supports smart starch-based packaging integration in electronics and active food packaging.

United States: Policy-Driven Adoption and Nanomaterial Integration

The United States starch-based packaging market is strongly shaped by regulatory frameworks, particularly the U.S. Environmental Protection Agency’s 2030 recycling goal and the Break Free from Plastic Pollution Act (2021). These initiatives are driving a shift away from single-use plastics and stimulating demand for compostable, starch-based alternatives. The Act’s extended producer responsibility provisions are expected to accelerate the transition to starch-based solutions, especially in foodservice items, single-use cutlery, and consumer goods packaging.

On the innovation side, U.S. companies and research institutions are focusing on nanotechnology integration to improve starch-based packaging performance. Incorporating cellulose nanofibers and montmorillonite enhances barrier properties, tensile strength, and durability, making bioplastics competitive with petroleum-based plastics. There is also strong demand for BPI-certified compostable products, ensuring compliance with municipal composting systems. Meanwhile, the Association of Plastic Recyclers (APR) is influencing the design of starch-based packaging through guidance on inks, adhesives, and films, encouraging recyclability without compromising product safety.

China: Advanced Research and Premium Packaging Trends

The China starch-based packaging market is developing rapidly under the “14th Five-Year Plan” and new environmental regulations effective June 1, 2025, mandating eco-friendly, reusable packaging across logistics and express delivery. This has opened significant opportunities for starch-based packaging in the e-commerce and retail sectors, where sustainability and cost efficiency are key drivers.

China’s premium consumer market is also fueling the adoption of high-end starch-based packaging with oxygen barrier films, UV stabilization, and advanced printing finishes. Government incentives for green technology adoption and investments in remanufacturing capacity further strengthen the sector. Academic research plays a central role: a Jiangnan University team has developed starch-based active films incorporating nano-ZnO and montmorillonite to deliver antibacterial properties and extended fruit preservation, highlighting China’s leadership in functional, value-added biodegradable packaging.

India: EPR Enforcement and Growing Retail Applications

The India starch-based packaging market is driven by the Plastic Waste Management (Amendment) Rules, 2024, effective April 2025, which impose strict Extended Producer Responsibility (EPR) mandates. By July 1, 2025, all plastic packaging, including starch-based, must be traceable via barcodes or QR codes, ensuring transparency and accountability across the value chain. While MSMEs are exempt from direct EPR obligations, larger manufacturers and importers supplying raw materials are expected to shoulder compliance responsibilities.

Demand is growing significantly in e-commerce, organized retail, and food packaging sectors, where traceability, hygiene, and sustainability are increasingly critical. The government’s regulatory emphasis is pushing manufacturers toward scaled adoption of starch-based flexible packaging for food delivery, dairy products, and personal care applications. This shift is aligned with India’s push to modernize its packaging sector and reduce plastic dependency while strengthening supply chain accountability.

Japan: Plastic Resource Circulation Laws and Food Safety Compliance

The Japan starch-based packaging market is undergoing transformation under the Plastic Resource Circulation Strategy, which mandates all packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective the same year, requires reduction or redesign of 12 single-use plastic categories, directly benefiting starch-based compostable solutions. These policies are complemented by Japan’s 2030 goal of doubling renewable material use and strict enforcement of waste segregation at collection.

Food safety regulations are also evolving, with the Ministry of Health, Labor and Welfare’s (MHLW) “positive list” system for synthetic food packaging coming into effect on June 1, 2025. This system outlines which materials are approved for food contact safety, pushing starch-based packaging producers to meet strict biocompatibility standards. Together, these regulatory pressures are driving the adoption of bio-based, recyclable, and compostable starch-based packaging formats in both food and electronics industries.

Brazil: Reverse Logistics and Digital Tracking Platforms

The Brazil starch-based packaging market is underpinned by the National Solid Waste Policy (PNRS), which emphasizes recycling, reuse, and reverse logistics. The enactment of Law No. 15,088 in January 2025, banning imports of plastic waste, has further boosted domestic demand for sustainable materials such as starch-based packaging.

To strengthen accountability, the government supports reverse logistics systems where producers are responsible for post-consumer collection and recycling. A landmark initiative is the Recircula Brasil Platform, introduced by the Brazilian Agency for Industrial Development and the Brazilian Association of the Plastics Industry. This platform enables tracking and certification of plastic waste, ensuring verified reintroduction into production and promoting transparency across the starch-based packaging supply chain. As demand for sustainable food and consumer packaging grows, Brazil is positioning itself as a leading Latin American market for compostable, traceable, and regulation-compliant starch-based packaging.

Starch based Packaging Market Report Scope

Starch based Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.5 Billion

|

|

Market Size (2034)

|

$13.6 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Source (Corn Starch, Potato Starch, Tapioca Starch, Wheat Starch, Others), By Product Type (Bags & Pouches, Films & Wraps, Trays & Containers, Bottles, Molded Shapes, Loose-fill Packaging), By End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Home & Industrial Chemicals, Healthcare & Pharmaceuticals, Agriculture)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Novamont S.p.A., Roquette Frères, Corbion N.V., BioBag International AS, Innovia Films, NatureWorks LLC, Solanyl Biopolymers, AVEBE, BASF SE, TIPA Corp., Toray Industries, Inc., Futamura Chemical Co., Ltd., Plantic Technologies, VTT Technical Research Centre of Finland, EcoBharat

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Starch based Packaging Market Segmentation

By Source

- Corn Starch

- Potato Starch

- Tapioca Starch

- Wheat Starch

- Others

By Product Type

- Bags & Pouches

- Films & Wraps

- Trays & Containers

- Bottles

- Molded Shapes

- Loose-fill Packaging

By End-Use Industry

- Food & Beverages

- Personal Care & Cosmetics

- Home & Industrial Chemicals

- Healthcare & Pharmaceuticals

- Agriculture

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Starch based Packaging Market

- Novamont S.p.A.

- Roquette Frères

- Corbion N.V.

- BioBag International AS

- Innovia Films

- NatureWorks LLC

- Solanyl Biopolymers

- AVEBE

- BASF SE

- TIPA Corp.

- Toray Industries, Inc.

- Futamura Chemical Co., Ltd.

- Plantic Technologies

- VTT Technical Research Centre of Finland

- EcoBharat

* List Not Exhaustive

Methodology

The Starch-Based Packaging Market report by USDAnalytics has been prepared using a meticulous research methodology combining both primary and secondary sources to ensure accuracy, relevance, and actionable insights for industry professionals. Primary research involved interviews and consultations with R&D specialists, packaging engineers, supply chain managers, and sustainability officers from leading companies such as Ingredion, Cargill, BASF, Mondi Group, and Roquette, focusing on innovations in starch-based polymers, compostable solutions, and barrier enhancements. Secondary research included a comprehensive review of company reports, regulatory frameworks, trade publications, scientific journals, and market news to analyze trends in material performance, circular economy adoption, regional policy impacts, and technological advancements. Market sizing and forecasts were developed through a combination of top-down and bottom-up approaches, incorporating factors such as product type, end-use industry, raw material sources, and regional market drivers including EU PPWR, U.S. EPA regulations, India’s EPR mandates, China’s 14th Five-Year Plan, Japan’s Plastic Resource Circulation Strategy, and Brazil’s reverse logistics initiatives. Data triangulation and cross-validation ensured precision in estimating market potential, competitive landscape, and growth opportunities, providing a holistic view of the global starch-based packaging industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.