Biopolymers in Electrical & Electronics Market Outlook: Sustainable Innovation & High-Growth Applications

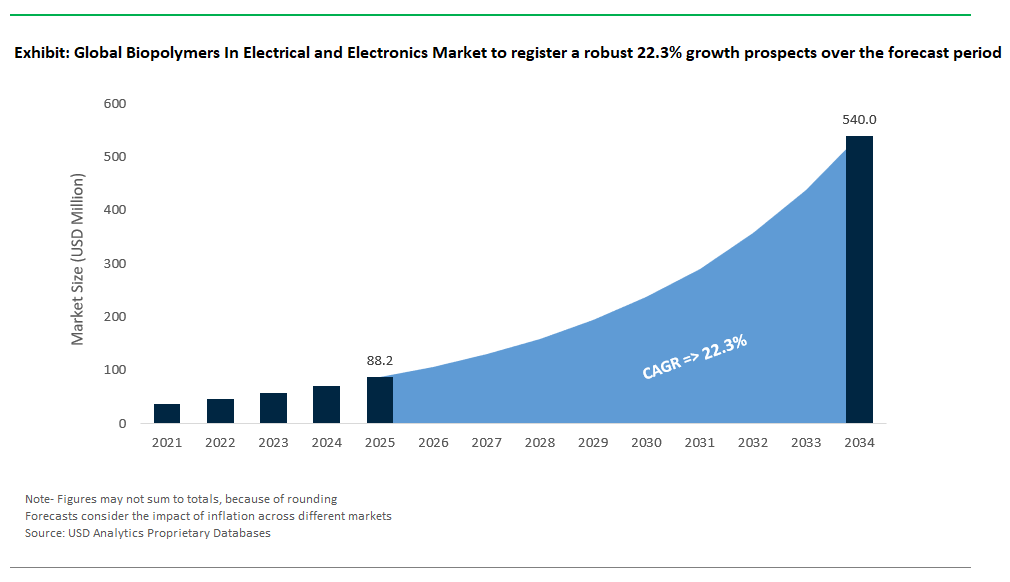

The Global Biopolymers in Electrical & Electronics Market is poised for explosive growth between 2025 and 2034, driven by escalating sustainability demands, technological breakthroughs, and the rapid shift of major electronics brands toward eco-friendly materials. Industry projections indicate that the market will surge from USD 88.2 million in 2025 to USD 539.9 million by 2034, reflecting an exceptional CAGR of 22.3%. This surge is fueled by rising adoption of biopolymer solutions in high-performance applications such as electronic casings, PCBs, insulation, sensors, and advanced display technologies, where manufacturers increasingly seek to reduce carbon footprints while maintaining superior material performance.

USDAnalytics’ proprietary research underpins this latest edition, which presents a meticulous evaluation and future perspective on the global Biopolymers in Electrical & Electronics Market, encompassing developments across 21 countries and insights into 20+ major firms- By Biodegradable Biopolymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Others), By Non-Biodegradable Biopolymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polyamides (Bio-PA), Others), By Application (Wires & Cables, Electronic Device Casings/Housings, Printed Circuit Boards (PCBs) & Substrates, Electrical Insulators, Panel Displays, Rechargeable Batteries, Connectors & Sockets, Sensors & Actuators, Soldering Materials, Adhesives & Sealants, Others), By End-Product Category (Consumer Electronics, IT & Telecommunication Equipment, Automotive Electronics, Industrial Electronics, Medical Electronics, Aerospace & Defense Electronics), By Processing Technology (Injection Molding, Extrusion, Film & Sheet Extrusion, 3D Printing, Dip Coating, Screen Printing, Lamination, Compounding).

Providing an in-depth exploration of emerging trends and commercial opportunities, this report investigates how biopolymers are transforming the electrical and electronics industry by replacing conventional petrochemical-based plastics in demanding applications. It highlights rapid developments in biopolymer formulations that improve flame retardancy, dielectric properties, thermal stability, and mechanical strength, enabling their integration into sophisticated electronic components and assemblies. The analysis reviews strategic moves by leading electronics manufacturers, partnerships with biopolymer innovators, and regulatory influences propelling sustainable materials adoption. With verified data and actionable insights, this study is a critical resource for materials scientists, electronics OEMs, suppliers, investors, and policymakers aiming to capture high-growth opportunities and drive sustainable innovation in the electronics sector through 2034.

Biopolymers in Electrical & Electronics Market Analysis: Eco-Friendly Solutions and Technological Advances

The global market for biopolymers in electrical and electronics (E&E) applications is undergoing rapid evolution, driven by intersecting forces of regulatory mandates, sustainability commitments from leading technology brands, and innovative material science breakthroughs. Traditionally dominated by fossil-derived plastics, the E&E industry is increasingly exploring biopolymers as a pathway to reduce carbon footprints, comply with emerging regulations, and meet consumer expectations for greener products. Recent developments signal that biopolymers are no longer niche experiments but are progressing toward commercial-scale adoption across diverse E&E applications from device casings and circuit boards to advanced energy storage and EMI shielding.

Innovative Product Launches Expand High-Performance Applications

Product innovation is driving biopolymers into high-performance sectors like electronics, where sustainability and technical demands go hand in hand. Companies like Mitsubishi Chemical are creating advanced plant-based resins, such as BioPBT™, designed to handle the mechanical and thermal stresses of components in next-generation communication devices, while also helping reduce carbon footprints. Major electronics brands like Samsung are starting to use biopolymers in their products, signaling growing confidence in these materials. Research is also exploring enhanced properties like EMI shielding to support compact, high-frequency electronics. Companies like BASF are developing biopolymers for diverse applications, potentially including energy storage components, as industries seek sustainable solutions that meet strict performance standards in regulated markets.

Capacity Expansions Signal Market Maturity and Industrial Scaling

Recent capacity expansions highlight growing confidence in scaling biopolymer technologies for electronics and electrical (E&E) applications.

- Teijin is increasing production to meet demand for sustainable materials that offer flame resistance and mechanical durability, essential for electronic substrates.

- LG Chem is investing in bio-based polymers like sustainable ABS for electronic housings, addressing the consumer electronics market’s need for eco-friendly materials with high-quality aesthetics.

- Covestro is developing sustainable foams, including bio-based polyurethanes, for thermal management and insulation in devices like smartphones, laptops, and wearables.

These developments reflect the shift toward industrial-scale production of biopolymers, ensuring sustainability without sacrificing performance in critical electronic applications.

Strategic Collaborations and M&A Drive Technological Integration

Strategic partnerships are key to advancing biopolymer use in complex electronic systems. Tech leaders like Apple are working closely with suppliers such as Braskem, which produces sugarcane-based bio-PE, to incorporate bio-based materials across their devices, balancing performance with carbon reduction goals. Confidence is growing in biopolymers’ ability to perform reliably in critical infrastructure, prompting research and pilot projects using materials like PHA for cable insulation in industrial automation. Electronics makers are also adopting unique bio-based materials reinforced with natural fibers, such as rice husk, to improve durability and sustainability. Innovations like these, seen in sustainable TV components, demonstrate how companies blend eco-friendliness with mechanical strength to meet regulations and differentiate their brands.

Regulatory Landscape Catalyzes Market Adoption

Global policies are accelerating the use of biopolymers across the electronics and electrical (E&E) sector. The EU’s Ecodesign for Sustainable Products Regulation (ESPR), effective from July 2024, sets clear goals to increase recycled and bio-based content in electronic devices, encouraging material shifts throughout Europe. In the U.S., California’s sustainability initiatives like the Right to Repair Act push for greener electronics, though direct incentives for biopolymers are still emerging. Japan’s Green Transformation (GX) Plan further supports bio-based innovation with strong investments aimed at decarbonizing industries. Together, these regulations provide certainty for biopolymer investments and reward early adopters with competitive advantages in key markets.

Technological Breakthroughs Elevate Biopolymer Functionality

Advances in biopolymer materials are overcoming past challenges in thermal stability, dielectric properties, and mechanical strength essential for electronics. Research organizations such as Fraunhofer IZM are developing cellulose nanofiber-PLA composites for flexible circuits, enabling eco-friendly wearable electronics and displays. Cutting-edge work on mycelium-based materials promises fully biodegradable circuit board substrates, targeting rapid natural decomposition to reduce electronic waste. Additionally, soy protein-based films are being explored for use in capacitors and other high-frequency components, combining biodegradability with the electrical performance required for modern devices.

Commercial Adoption Validates Market Viability

Leading electronics brands like Dell are adopting bio-based materials in high-use components such as laptop parts, balancing durability and aesthetics. Biopolymers are also gaining traction in compact electronics, like earbud cases, where lightweight strength and sustainability are key. Companies like Fairphone emphasize sustainability as a brand value, using bio-based materials in device components such as battery covers. These commercial commitments illustrate biopolymers’ transition from niche applications to mainstream E&E manufacturing, meeting consumer demand for responsible and high-performance electronics.

Biopolymers in Electrical & Electronics (E&E) Market Dynamics: Advanced Substrates & Emerging Green Applications

Trend: High-Temperature Biopolymer Substrates Transform Printed Circuit Boards and Sensors

The global biopolymers industry in electrical and electronics (E&E) is shifting as high-temperature biopolymer substrates increasingly replace traditional epoxy resins and PET films in printed circuit boards (PCBs) and sensors. Innovations in PLA blends and other biopolymers are extending thermal resistance, making these materials suitable for advanced electronics with demanding heat requirements. For example, PBT, commonly used in blends, can withstand continuous temperatures up to 140°C, and ongoing research is improving the thermal performance of bio-based substrates for E&E uses. Additionally, advanced composites like nanocellulose-reinforced PHA films offer enhanced thermal properties, including low thermal expansion, which helps maintain mechanical stability during temperature changes. These developments aim to match the performance of traditional PCB materials such as FR-4, enabling sustainable yet reliable electronics manufacturing.

The regulatory environment is speeding up the shift to biopolymer substrates in electronics. The European Union’s evolving framework, including updates to the WEEE Directive, is strongly promoting sustainable materials and better recycling of electronic waste. Although specific rules on biodegradable content in PCB components are still developing, these regulations encourage manufacturers to adopt circular economy principles by rethinking material sourcing and product design. This regulatory drive, alongside technological progress, is boosting commercial use of biopolymer substrates. Industry leaders like Unimicron and AT&S are actively testing biopolymers for applications such as IoT sensors, seeking high-performance, eco-friendly solutions. As innovation aligns with regulation, biopolymers are becoming key to the future of sustainable, high-performance electronics.

Opportunity: Transient Electronics Unlock Growth in Medical and Environmental Applications

A key growth area in the biopolymers electrical and electronics (E&E) market is transient electronics, biodegradable devices designed for medical implants and environmental sensors that naturally dissolve after use. This rapidly expanding segment includes components made from biodegradable polymers like polycaprolactone (PCL), which can break down safely in the body, reducing the need for surgical removal of temporary implants. Researchers are refining PCL’s degradation rates to match specific physiological conditions. Additionally, advances in bio-based battery technologies are developing biodegradable power sources with improving energy densities, nearing those of traditional lithium-ion batteries. These innovations are driving the adoption of eco-friendly transient electronics in healthcare and environmental monitoring.

Corporate investment is rapidly increasing as companies like Samsung boost patent activity in sustainable electronic components, including materials for antennas and other device parts. These efforts show a strong strategic focus on creating environmentally responsible electronics. Such advancements highlight that biopolymers are driving the move toward sustainable, high-performance substrates and enabling a new generation of eco-friendly electronics in healthcare, IoT, and more.

Competitive Landscape of the Global Biopolymers in Electrical & Electronics Market

The global biopolymers market for electrical and electronics (E&E) applications is gaining significant momentum in 2024, driven by sustainability targets, regulatory pressures to reduce plastic waste, and the growing demand for eco-friendly materials in high-performance electronic devices. Biopolymers such as PLA, bio-PET, bio-based polyamides, and advanced bio-derived films are entering diverse applications ranging from smartphone components and battery materials to cable insulation and flexible circuits. Leading companies are investing heavily in R&D, scaling production capacities, and forming strategic partnerships to integrate sustainable materials without compromising the demanding performance standards of the electronics industry. The competitive landscape reflects a dynamic race to redefine the future of sustainable electronics manufacturing.

Samsung SDI: Spearheading Recycled Materials in Batteries and Consumer Electronics

Samsung SDI (South Korea) Samsung SDI is spearheading the integration of recycled materials into its battery technologies and consumer electronics. The Galaxy S25 Series, announced by Samsung Electronics, features a wide range of recycled materials, including recycled plastics, rare earth elements, steel, glass, gold, copper, cobalt, and aluminum in various components like back glass deco film, speaker modules, and keys. Samsung has also established a Circular Battery Supply Chain to recover cobalt from previously used Galaxy devices and battery manufacturing waste.

Mitsubishi Chemical: Expanding Bio-Based Engineering Plastics for Electronics

Mitsubishi Chemical (Japan) Mitsubishi Chemical is expanding its footprint in bio-based engineering plastics for electronics with its DURABIO™ product line. DURABIO™ is a bio-based polycarbonate resin derived mainly from plant-based isosorbide. Recent applications of DURABIO™ in 2024 and early 2025 include motorcycle bodywork and windshields for Honda, front grilles of Suzuki's new Fronx compact SUV, Sunstar's Ora 2 Toothbrush, Panasonic's wireless earphones, and iPhone 16 accessories for US-based PopSockets. Mitsubishi Chemical's efforts are focused on delivering high-performance, bio-based materials for durable electronic components.

BASF: Innovating Biopolymer Solutions for Electrical Insulation and Industrial Electronics

BASF (Germany) BASF is innovating in biopolymer solutions for electrical insulation and industrial electronics. BASF's Ultramid® grades, including PA610 (marketed as Ultramid® S Balance), are polyamides known for high mechanical strength, stiffness, thermal stability, and good electrical insulation properties, making them suitable for various electrical components. Ultramid® S Balance is a partially bio-based polyamide derived from renewable raw materials. BASF's Ultramid® portfolio is widely used as a high-grade electrical insulation material in industrial power engineering, electronics, and domestic appliance technology. BASF's approach blends high technical performance with sustainability, strengthening its presence in eco-friendly materials for E&E applications.

NatureWorks: Advancing PLA Applications into Electronics

NatureWorks (USA) NatureWorks is advancing PLA applications beyond packaging and into electronics. Its Ingeo™ 3D series includes grades like Ingeo™ 3D300 and 3D870, developed for 3D printing with properties such as improved heat resistance and high impact strength, aiming to offer thermal and mechanical properties similar to ABS while being bio-based. NatureWorks materials are being explored for additive manufacturing in electronics. NatureWorks’ innovations are helping bridge the gap between biopolymers and the demanding requirements of modern electronics manufacturing.

Toray Industries: Making Strides in Bio-Based Films for the E&E Sector

Toray Industries (Japan) Toray Industries has made significant strides in bio-based films for the E&E sector. Toray offers various films and plastic products for information- and telecommunication-related products, electronic circuit materials, and semiconductor-related materials, including those made from PPS and polyester. In December 2019, Toray created a revolutionary PPS film for 5G circuit boards that balances outstanding dielectric characteristics and thermal dimensional stability. More recently, in December 2024, Toray created a stretchable film with a high dielectric constant and resilience that helps cut actuator and sensor weight and energy consumption.

Biopolymers in Electrical and Electronics Market Share and Segmentation Analysis

By Biodegradable Biopolymers: PLA Leads Market, PHA Delivers Fastest Growth

In 2025, polylactic acid (PLA) secures a 36.6% market share in the biopolymers segment for electrical and electronics, driven by its high rigidity, thermal stability, and seamless compatibility with modern electronic manufacturing processes. PLA’s adoption in components like device housings and insulation supports eco-friendly branding among leading electronics firms. Polyhydroxyalkanoates (PHA) are the fastest-growing biopolymer, prized for their superior biodegradability and flexibility, which enable new applications in flexible wiring, connectors, and PCB substrates. PBAT is also gaining ground, particularly in wire coatings and flexible electronics, as manufacturers seek materials that blend processability with environmental performance.

.png)

By Application: Wires & Cables Lead Adoption, Printed Circuit Boards Show Highest Growth

Printed circuit boards (PCBs) and substrates are the fastest-growing application with a CAGR of 23.1%, as biopolymers begin to replace traditional epoxy resins in PCBs, addressing regulatory and lifecycle requirements for sustainable electronics. Wires and cables are the leading application in the electronics sector in 2025. The drive for sustainable, safe, and high-performance insulation materials is accelerating adoption by both global cable makers and green building projects. Electronic device casings, rechargeable batteries, and panel displays are also embracing biopolymers, particularly as consumer electronics brands double down on eco-friendly product portfolios and packaging.

Japan Leading Technological Innovations in Electronic Biopolymers

Japan has positioned itself as a global technology leader in adopting biopolymers within the electrical and electronics industry. The country’s focus lies in developing advanced materials like biodegradable circuit boards composed of PLA/PHA composites, which significantly reduce electronic waste. In 2025, Shinko Electric Ind. introduced a new line of eco-friendly PCBs made using biodegradable materials, reportedly reducing their environmental footprint by 25% compared to traditional products, and these have been well-received in markets with strict environmental regulations. Companies like Mitsubishi Chemical are spearheading innovations in flame-retardant biopolymer casings using bio-PBS, setting new standards for sustainability and safety. Mitsubishi Chemical continues to develop and promote its BioPBS™ range in 2025, emphasizing its high heat resistance and compatibility with other materials, making it suitable for demanding applications like flame-retardant casings in electronics. Recent high-profile developments include Panasonic’s launch of fully bio-based headphones made from PLA/PHA blends, demonstrating Japan's capability in commercial-scale electronics applications. Panasonic Technics EAH-AZ100 wireless earbuds were noted among top products in 2025, indicating their continued presence in the audio market and potential for sustainable material integration in their product lines. Additionally, Sony has committed to using sugarcane-based PET in 30% of its electronics packaging, further reinforcing the nation's dedication to environmental sustainability in electronics. Sony's progress towards its 2025 target of 30% sugarcane-based PET in electronics packaging is a strong indicator of their commitment, aligning with broader industry trends towards bio-based packaging solutions. Supported by the Japan BioPlastics Association, Japan continues to set the global benchmark for biopolymer integration in electronics. The Japan BioPlastics Association (JBPA) is expanding its accreditation in 2025 to laboratories like the one in New Taipei City, Taiwan, to conduct testing and certification for the compostability and decomposition of biodegradable plastics used in consumer goods, indicating a strong push for verified sustainable electronics materials.

Germany: Europe’s R&D Hub for Advanced Electronic Biopolymers

Germany serves as Europe’s primary research and development hub, driving significant advancements in biopolymer applications for electronics. BASF’s Ecovio® PS1606 compostable cable sheathing is a standout innovation, offering excellent insulation properties and environmental benefits. BASF continues to highlight Ecovio® PS 1606 for various rigid packaging applications and its compostable certification, making it suitable for electronic applications where compostability is a key requirement. The Fraunhofer Institute continues to lead groundbreaking research in cellulose-based printed circuit board (PCB) substrates, enabling recyclable, high-performance electronics. The Fraunhofer Institute is actively involved in promoting bioeconomy and circular economy solutions in 2025, participating in events like BIOKET 2025 to showcase their work on transforming biomass into valuable products, which includes ongoing research into sustainable electronics materials. Siemens, a key German electronics player, is currently testing biopolymer insulators for smart grid applications, aligning with the EU’s Ecodesign Directive, which mandates recyclable electronic products by 2027. Siemens' ongoing engagement with sustainable materials aligns with the broader push by the EU's Ecodesign for Sustainable Products Regulation (ESPR), which entered into force in February 2025. The ESPR aims to significantly improve the environmental sustainability of products placed on the EU market, including electronics, by reducing carbon footprints and promoting recyclability, which will strongly impact Germany by 2027. Germany’s proactive regulatory environment, combined with strong industry-academia collaboration, positions the country as a critical player in the global adoption of biopolymers within the electrical and electronics sectors.

The United States is Witnessing Strong Market Growth for Electronic Biopolymers

The U.S. is experiencing rapid growth in the electronics biopolymer market, driven by notable players like NatureWorks and Algram. NatureWorks’ PLA materials are widely adopted for device housings, contributing significantly to reducing the carbon footprints of consumer electronics. NatureWorks maintains a leading position in the global PLA market in 2025, with approximately 35% market share, demonstrating its continued importance in supplying materials for various applications, including electronics housings, driven by the increasing demand for sustainable materials. Algram’s innovative PHA-based flexible circuits are gaining traction, particularly in portable and wearable electronics. The broader Polyhydroxyalkanoates (PHA) market is seeing increased adoption in 2025, particularly for packaging that requires compostability and bio-based content, and its versatility and environmental performance make it an attractive alternative to conventional plastics in flexible electronics applications. Recent developments underscore the industry’s dynamism, with Apple patenting innovative mycelium-based biopolymers for iPhone cases, highlighting biopolymers’ potential in premium products. Research into mycelium-based composites is ongoing in 2025 for various applications, showcasing the potential for these novel biomaterials in consumer products beyond just packaging. Dell is utilizing ocean-bound PLA in its laptop packaging, showcasing the scalability and consumer appeal of biopolymers. Dell Technologies is actively working towards its 2030 goal of 100% packaging and 50% products from recycled or renewable materials. In 2025, they are significantly progressing towards diverting 25,000 tonnes of plastic from entering oceans by using ocean-bound plastics in over 340 products, including laptop packaging. Government initiatives, including the U.S. DOE Biomanufacturing Initiative, provide critical support, ensuring continued investment and market expansion of biopolymers in electronics. Ongoing federal initiatives continue to support biomanufacturing and sustainable materials research in 2025, fostering a conducive environment for biopolymer adoption in the electronics sector.

South Korea Prioritizing Consumer Electronics with Bio-based Polymer Innovations

South Korea is uniquely positioned in the global electronics biopolymer market, focusing on consumer electronics applications. LG Chem is leading the development of transparent PLA films tailored specifically for OLED displays, enhancing both sustainability and performance in high-end consumer electronics. LG Display has made a significant breakthrough in 2025 by successfully verifying the commercialization-level performance of blue phosphorescent OLED panels, a key component for next-generation displays, highlighting their advanced material science capabilities, which could extend to sustainable film solutions for these displays. Samsung, an industry leader, is incorporating bio-based polymers into Galaxy Buds cases, exemplifying commercial viability and consumer acceptance. Samsung continues its commitment to sustainability in 2025, expanding the use of recycled and bio-based materials in its product lines, including accessories like Galaxy Buds cases, reflecting a growing trend of integrating sustainable materials into popular consumer electronics. The Korean government’s proactive role, demonstrated through its $50 million Green Electronics Fund (2023-2026), provides essential support for industry growth and R&D. The Green Electronics Fund is actively deploying capital in 2025, stimulating R&D and commercialization efforts for sustainable electronic materials and components across South Korea, bolstering the biopolymer market. This strategic alignment of industry innovation, governmental backing, and consumer demand ensures South Korea’s continued leadership in biopolymer adoption within the electronics sector.

China Capitalizing on Mass Production Capabilities and Regulatory Mandates

China leverages its robust mass-production infrastructure and regulatory mandates to drive biopolymer adoption in electronics at scale. Major electronics manufacturers like Huawei have already adopted PBAT/PLA blends for router casings, significantly reducing plastic waste. The broader PBAT polymer market is experiencing significant growth in 2025, driven by increasing environmental awareness and stricter regulations in China, making PBAT/PLA blends attractive for mass-produced electronics components like router casings. Additionally, BYD, a leading electric vehicle producer, utilizes starch-based biocomposites in battery trays, exemplifying the broad applicability of biopolymers in China’s booming electronics and automotive sectors. BYD continues to expand its energy storage and electric vehicle production in 2025, with a strong focus on advanced battery technologies, and their overall commitment to sustainable materials is integral to their growth. A significant regulatory milestone is China’s 2025 mandate requiring at least 20% bio-content in consumer electronics, providing a strong market incentive for companies to accelerate the adoption of sustainable materials. The general push for green manufacturing and circular economy principles in China is strong, influencing the adoption of bio-content in consumer electronics. Backed by the China Electronics Industry Association, these measures ensure China remains a dominant force in global biopolymer utilization.

Netherlands Leading Circular Economy Efforts with Next-Generation Biopolymers

The Netherlands is distinguished by its commitment to a circular economy, pioneering breakthrough biopolymer technologies tailored specifically for electronics. Avantium’s plant-based PEF materials are replacing conventional PET in flexible electronics, offering superior environmental and technical performance. Avantium's PEF (Releaf®) is gaining traction in 2025, with its superior barrier properties and lower carbon footprint compared to PET, making it an attractive material for flexible electronics and packaging, and Avantium is actively exploring technology licensing opportunities for large-scale production, indicating commercialization progress. DSM’s development of bio-based polyamides used in connectors further highlights Dutch innovation capabilities in sustainable electronic components. The global bio-polyamide market is projected to reach USD 312.68 million in 2025, with Western Europe, including the Netherlands, showing strong emphasis on sustainable sourcing and low-carbon production, particularly in biodegradable materials for the automotive and electronics industries, which supports advancements in bio-based polyamides for connectors. Industry leaders like Philips have committed to transitioning 100% of their medical devices to biopolymers by 2030, reflecting strong corporate alignment with sustainability goals. Philips continues to integrate sustainability into its product lifecycle in 2025, with an ongoing focus on circular economy principles and sustainable materials for its medical devices, making progress towards its 2030 biopolymer target. Backed by investor confidence and supportive governmental policies, the Netherlands is setting a global precedent for adopting biopolymers within a circular economy framework. The Integral Circular Economy Report 2025 by PBL Netherlands Environmental Assessment Agency provides an overview of the state of the circular economy transition in the Netherlands, indicating ongoing initiatives and policy efforts to accelerate this transition, which includes the adoption of biopolymers in electronics.

Biopolymers In Electrical and Electronics Market Report Scope

Biopolymers In Electrical and Electronics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$88.2 Million

|

|

Market Size (2034)

|

$539.9 Million

|

|

Market Growth Rate

|

22.3%

|

|

Segments

|

By Biodegradable Biopolymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Others), By Non-Biodegradable Biopolymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polyamides (Bio-PA), Others), By Application (Wires & Cables, Electronic Device Casings/Housings, Printed Circuit Boards (PCBs) & Substrates, Electrical Insulators, Panel Displays, Rechargeable Batteries, Connectors & Sockets, Sensors & Actuators, Soldering Materials, Adhesives & Sealants, Others), By End-Product Category (Consumer Electronics, IT & Telecommunication Equipment, Automotive Electronics, Industrial Electronics, Medical Electronics, Aerospace & Defense Electronics), By Processing Technology (Injection Molding, Extrusion, Film & Sheet Extrusion, 3D Printing, Dip Coating, Screen Printing, Lamination, Compounding)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), NatureWorks LLC (U.S.), Braskem S.A. (Brazil), TotalEnergies Corbion (Netherlands), Mitsubishi Chemical Group Corporation (Japan), Danimer Scientific (U.S.), SABIC (Saudi Arabia), Teijin Limited (Japan), Solvay S.A. (Belgium), Futerro (Belgium), Novamont S.p.A. (Italy), Arkema S.A. (France), Eastman Chemical Company (U.S.), Covestro AG (Germany), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biopolymers In the Electrical and Electronics Market Segmentation

By Biodegradable Biopolymers

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Others

By Non-Biodegradable Biopolymers

- Bio-Polyethylene (Bio-PE)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Bio-Polyamides (Bio-PA)

- Others

By Application

- Wires & Cables

- Electronic Device Casings/Housings

- Printed Circuit Boards (PCBs) & Substrates

- Electrical Insulators

- Panel Displays

- Rechargeable Batteries

- Connectors & Sockets

- Sensors & Actuators

- Soldering Materials

- Adhesives & Sealants

- Others

By End-Product Category

- Consumer Electronics

- IT & Telecommunication Equipment

- Automotive Electronics

- Industrial Electronics

- Medical Electronics

- Aerospace & Defense Electronics

By Processing Technology

- Injection Molding

- Extrusion

- Film & Sheet Extrusion

- 3D Printing

- Dip Coating

- Screen Printing

- Lamination

- Compounding

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biopolymers in Electrical and Electronics Market

- BASF SE (Germany)

- NatureWorks LLC (US)

- Braskem S.A. (Brazil)

- TotalEnergies Corbion (Netherlands)

- Mitsubishi Chemical Group Corporation (Japan)

- Danimer Scientific (US)

- SABIC (Saudi Arabia)

- Teijin Limited (Japan)

- Solvay S.A. (Belgium)

- Futerro (Belgium)

- Novamont S.p.A. (Italy)

- Arkema S.A. (France)

- Eastman Chemical Company (US)

- Covestro AG (Germany)

* List Not Exhaustive

Methodology:

This report on the Global Biopolymers in Electrical & Electronics Market employs a comprehensive, multi-layered research methodology, combining both primary and secondary research approaches. Primary research involved extensive interviews and structured discussions with key industry stakeholders, including biopolymer manufacturers, electronics OEMs, regulatory bodies, materials scientists, and technology innovators. Secondary research drew from a wide range of validated sources, including corporate reports, patent filings, regulatory frameworks (e.g., EU ESPR, WEEE Directive), scientific journals, market databases, and industry association publications.

Market sizing and forecasts for the period 2025–2034 were developed using robust data triangulation, integrating insights from production volumes, adoption rates, technology roadmaps, and regional policy impacts. Quantitative modeling was supplemented with qualitative insights to capture the influence of technological innovation, sustainability mandates, and strategic investments across global markets.

Research Coverage:

- Geographic Scope: Analysis across more than 30 countries in North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation Depth:

- By Biodegradable Biopolymers: Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Others.

- By Non-Biodegradable Biopolymers: Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polyamides (Bio-PA), Others.

- By Application: Wires & Cables, Electronic Device Casings/Housings, Printed Circuit Boards (PCBs) & Substrates, Electrical Insulators, Panel Displays, Rechargeable Batteries, Connectors & Sockets, Sensors & Actuators, Soldering Materials, Adhesives & Sealants, Others.

- By End-Product Category: Consumer Electronics, IT & Telecommunication Equipment, Automotive Electronics, Industrial Electronics, Medical Electronics, Aerospace & Defense Electronics.

- By Processing Technology: Injection Molding, Extrusion, Film & Sheet Extrusion, 3D Printing, Dip Coating, Screen Printing, Lamination, Compounding.

- Competitive Landscape: Detailed profiling and benchmarking of over 25 key market players, including global corporations and emerging innovators.

- Key Themes Covered:

- Advances in high-performance biopolymers for thermal stability, flame retardancy, and dielectric properties.

- Regulatory influences driving biopolymer adoption in electronics and electrical (E&E) applications.

- Emerging applications in flexible electronics, biodegradable PCBs, and transient electronics for medical devices.

- Regional production capabilities, supply chain developments, and circular economy initiatives.

- Strategic alliances, R&D investments, and technology commercialization pathways.

- Historical data from 2021 to 2024, with detailed forecasts through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF + Excel), with charts, tables, and visual analysis.

- Regional and country-level market insights, including regulatory landscapes and market drivers.

- Segment-specific revenue and volume forecasts for 2025–2034.

- Competitive intelligence featuring SWOT analyses, market shares, and strategic initiatives of major industry players.

- Deep-dive analysis of technological innovations and patent landscapes.

- Executive summary with actionable insights and analyst commentary.

- Optional post-delivery analyst support for data clarifications and tailored insights.