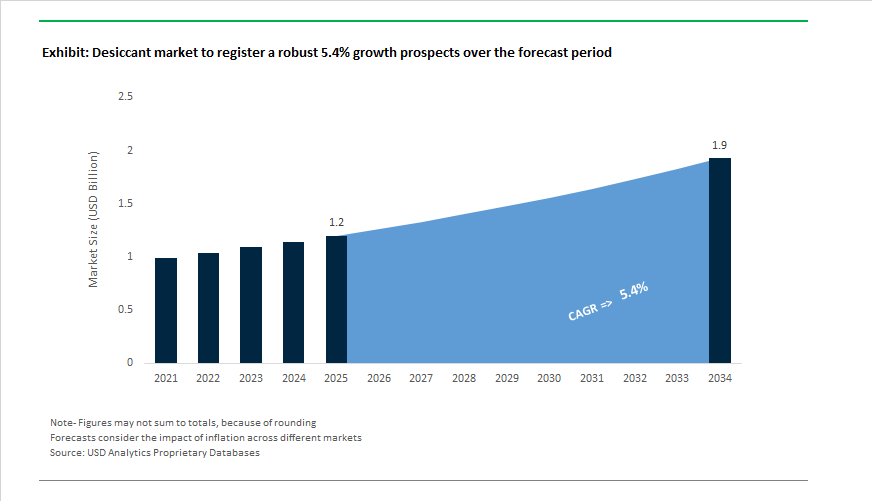

Desiccant Market to Reach $1.9 Billion by 2034 at 5.4% CAGR Fueled by Smart Moisture Control and Bio-Based Adsorbents

The Desiccant Market is projected to grow from $1.2 billion in 2025 to $1.9 billion by 2034, registering a CAGR of 5.4%. Expansion is being driven by rising demand for moisture control solutions in pharmaceuticals, electronics, EV logistics, and high-value industrial exports. Molecular sieves, silica gel, activated alumina, clay desiccants, and specialty polymer-based adsorbents are increasingly integrated into supply chains that require humidity stabilization during storage and transport. The market is also experiencing structural change as sustainability regulations, digital monitoring technologies, and regional supply diversification reshape production and procurement strategies.

Industry consolidation and capacity expansion began accelerating in March 2024, when W. R. Grace & Co. inaugurated its expanded CDMO facility in South Haven, Michigan, increasing site capacity by 25% and integrating high-purity moisture-control solutions for pharmaceutical drug stability. In April 2024, Zeochem, a subsidiary of the Swiss CPH Group, acquired Sorbead India and Swambe Chemicals, significantly strengthening its footprint in South Asia. The acquisition expanded Zeochem’s portfolio of specialty molecular sieves and chromatography gels, directly serving India’s growing petrochemical refining and API manufacturing base. During 2024, operations commenced at the Gothenburg Biorefinery through the St1 and SCA partnership, increasing the availability of wood-derived residues that are being evaluated for next-generation activated carbon desiccants. Through 2024–2025, Clariant scaled global production of Desi Pak® ECO, the first large-scale plastic-free desiccant packet using bentonite clay and bio-based paper, targeting sustainable logistics in textiles and machinery exports.

Technological innovation intensified through September 2025, when BASF’s Dahej and Mangalore plants achieved REDcert2 certification, enabling biomass-balanced specialty materials production aligned with low-carbon construction value chains. In October 2025, Honeywell completed the spin-off of its Advanced Materials business into Solstice Advanced Materials, restructuring its specialty chemical and desiccant portfolio into a standalone entity before its broader 2026 corporate realignment. Late 2025 also saw the debut of AI-integrated smart desiccant monitoring systems at major exhibitions, with embedded humidity sensors and digital indicators enabling real-time tracking of cargo conditions for semiconductors and precision electronics. Between 2025 and 2026, Clariant reported record adoption of Container Dri® II cargo desiccants for global EV shipments, addressing condensation risks that threaten sensitive electronic control units during long-haul maritime transport. In January 2026, Wacker Chemie implemented price increases of up to 25% for platinum-dependent silicone specialties, affecting the cost structure of advanced silicone-based desiccants used in medical and electronics applications. BASF added a new specialty materials production line in Mangalore in February 2026, reinforcing India’s role in diversified global supply chains. That same month, the Dahej PCPIR project secured approximately ₹360 crore in funding to expand chemical intermediates and specialty desiccant production capacity supporting pharmaceutical and green energy exports.

Trends and Opportunities in the Global Desiccant Market

Purity-Engineered Desiccants for Semiconductor Fabs and Battery Dry Rooms

- Advanced electronics and battery manufacturing are placing unprecedented demands on desiccant performance. The production of sub-5 nanometer semiconductor nodes and high-energy-density lithium-ion batteries requires ultra-dry environments, with permissible moisture levels often below 10 to 100 parts per million to avoid hydrofluoric acid formation and electrode degradation. By 2025, next-generation desiccant dehumidification systems such as the Fisair DFLOW platform were consistently achieving dew points as low as minus 70 degrees Celsius in battery dry rooms. These systems rely on high-purity silica gel rotors engineered for near-zero dust generation, a critical requirement in cleanroom environments where particulate contamination can trigger catastrophic cell failure or shorten electric vehicle battery cycle life.

- Beyond ambient humidity control, chemical inertness during material handling is becoming equally important. In August 2025, process technology leaders emphasized the growing role of vacuum drying systems integrated with desiccant-managed airlocks for cathode precursor preparation. Maintaining moisture thresholds below 300 parts per million during lithium hydroxide and related precursor drying prevents surface reactions with carbon dioxide, preserving crystal morphology and electrochemical performance of cathode active materials. As gigafactory scale-up accelerates, desiccant specifications are increasingly written directly into battery process qualification protocols rather than treated as auxiliary equipment.

Smart Monitoring and RFID-Enabled Desiccant Systems for Supply Chain Assurance

- The desiccant market is also moving toward active quality assurance through digital integration. Pharmaceutical, semiconductor, and high-value electronics supply chains are embedding intelligence into desiccant systems to enable real-time monitoring of humidity exposure across global logistics networks. In May 2025, Powercast Corporation received the Best New Product award at RFID Journal LIVE! for its battery-free, energy-harvesting RFID sensor platform. These passive sensors can be embedded directly into desiccant packaging, logging humidity and temperature data without onboard power and allowing logistics operators to verify dry-chain compliance using standard handheld readers.

- Semiconductor manufacturers are deploying similar approaches at scale. Clariant has expanded the use of color-change humidity indicator cards compliant with JEDEC J-STD-033 standards. When combined with digital identifiers and tracking systems, these smart desiccants enable continuous monitoring of moisture exposure for surface-mount devices throughout storage and transit. Any breach in seal integrity triggers immediate alerts, reducing the risk of latent moisture-related failures during reflow soldering and final device assembly.

Hydrogen Purification and Drying for the Net-Zero Energy Transition

- The rapid scale-up of green hydrogen production and distribution is opening a high-value growth avenue for advanced desiccants and molecular sieves. Hydrogen streams must be dried to extremely low moisture levels to protect electrolyzers, fuel cells, and pipeline infrastructure from corrosion and performance loss. Arkema has positioned its Siliporite® molecular sieve portfolio as a core material for hydrogen electrolyzer drying systems. These desiccants are engineered to withstand high-pressure cyclic loading while ensuring compliance with ISO 14687 hydrogen purity specifications required for fuel cell electric vehicles.

- Process optimization is further amplifying this opportunity. In late 2025, Honeywell UOP reported that upgrading pressure swing adsorption units with high-performance adsorbents can increase hydrogen recovery by between 2% and 33 %, depending on cycle design. These advanced molecular sieves also enable removal of oxygen impurities down to 1 part per million by volume, a critical requirement for green hydrogen used in mobility, refining, and chemical synthesis. As hydrogen infrastructure expands globally, desiccants are becoming a core efficiency lever rather than a balance-of-plant component.

Sustainable and Bio-Based Desiccants for Circular Packaging Systems

- Sustainability regulation is creating parallel growth opportunities in packaging and consumer goods. Under the European Union Packaging and Packaging Waste Regulation, brands are under pressure to reduce plastic content and carbon intensity across packaging systems, including moisture-control solutions. In response, 2025 saw increased industrial focus on extracting highly dispersible bio-silica from rice husk ash. This approach converts agricultural waste into functional desiccant materials with a carbon footprint approximately 50% lower than conventional precipitated silica, while delivering comparable moisture adsorption performance for food, pharmaceutical, and cosmetic packaging.

- In addition, starch- and cellulose-based desiccant sachets derived from corn and tapioca are gaining traction as biodegradable alternatives to plastic-heavy packets. These bio-polymer desiccants align with zero-plastic and compostable packaging mandates and are finding adoption across the rapidly expanding green building materials market and sustainable consumer goods sector. As circular economy principles become embedded in procurement criteria, bio-based desiccants are moving from pilot applications to scalable commercial solutions within the global desiccant market.

Desiccant Market Share and Segmentation Insights

Market Share by Type : Silica Gel Leads While Molecular Sieves Enable Precision Drying

Silica gel holds 35% of the global desiccant market in 2025, driven by its non-toxicity, chemical inertness, and reliable performance across wide humidity ranges, making it the preferred choice for pharmaceutical packaging, electronics protection, and food preservation. Molecular sieves follow as a high-performance segment, valued for exceptional adsorption at ultra-low humidity and selective molecular separation in industrial gas drying and solvent purification. Activated alumina maintains strong demand in compressed air systems and natural gas processing due to its mechanical strength. Bentonite clay serves cost-sensitive logistics and agricultural storage, while calcium chloride addresses high-capacity moisture control in cold-chain shipping despite forming brine upon saturation. Activated charcoal offers dual moisture and odor adsorption for specialty packaging. Metal-organic frameworks remain a niche but fast-evolving category, attracting attention for electronics manufacturing and advanced energy systems requiring highly controlled humidity environments.

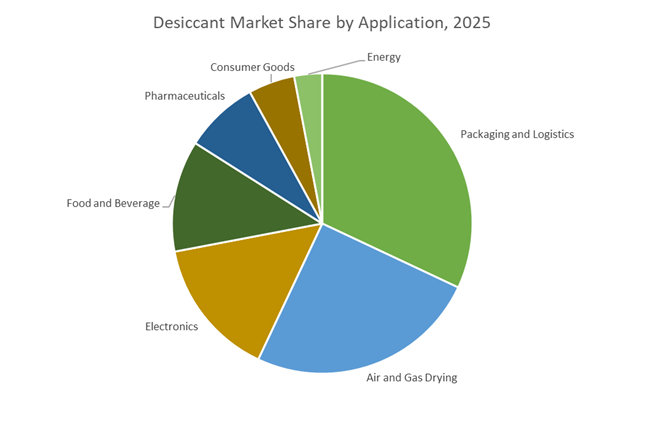

Market Share by Application : Packaging and Logistics Dominate as Electronics and Pharma Drive High-Value Demand

Packaging and logistics account for 32% of desiccant consumption, protecting machinery, textiles, and consumer goods from moisture damage during storage and global transport through container desiccants and moisture-control packets. Air and gas drying represents a major industrial segment, using desiccants in compressed air systems, HVAC, and natural gas dehydration to prevent corrosion and equipment failure. Electronics rely heavily on miniaturized desiccants to safeguard semiconductors, circuit boards, and optical devices from oxidation. Food and beverage applications utilize food-grade desiccants to preserve crispness and prevent clumping in spices, dried fruits, and powders. Pharmaceuticals demand regulatory-compliant desiccant canisters and packets to stabilize hygroscopic drugs throughout shelf life. Consumer goods and energy applications complete the landscape, with desiccants supporting moisture-sensitive retail products, transformer breathers, battery manufacturing, and critical infrastructure requiring long-term humidity control.

Competitive Landscape of the Desiccant Market

The Desiccant Market is being reshaped by active packaging innovation, pharma-grade moisture control, molecular sieve dehydration, and integrated oxygen–moisture protection, as industries prioritize shelf-life extension, electronics reliability, and ultra-dry manufacturing environments across food, pharmaceuticals, EV batteries, and industrial gas processing.

Clariant AG drives sustainable active packaging with Desi Pak ECO and bentonite security

Clariant commands a leading position in consumer-facing and food-contact desiccants through its Functional Minerals division and Active Packaging portfolio. Its flagship Desi Pak® ECO leverages natural bentonite clay and plastic-free bio-based paper, supporting low-carbon moisture absorption for e-commerce, textiles, and packaged foods. In late 2025, Clariant expanded its Mediterranean bentonite mining operations to secure a 20-year supply of premium raw materials, strengthening long-term cost stability. The company further deepened its Asia footprint by opening a Sustainability Center in Indonesia in early 2026, tailoring humidity-control solutions for Southeast Asia. Clariant’s core advantage lies in regulatory leadership, with FDA- and EU-compliant desiccants that set benchmarks for food safety, packaging performance, and sustainable moisture management.

W.R. Grace advances silica desiccants with ML-driven pore optimization for pharma and LNG

W.R. Grace dominates the synthetic silica segment, supplying SYLOID® and SYLOSIV® desiccants across pharmaceutical packaging, insulated glass, and industrial gas drying. In early 2026, the company showcased machine-learning workflows to optimize pore-size distribution, enabling application-specific adsorption performance for demanding environments. Grace’s strategic focus on pharma-grade precision targets the fast-growing pharmaceutical stability market, delivering ultra-pure silica gels that prevent oxidative degradation in tablets and biologics. The company also plays a critical role in LNG processing, where its desiccants prevent corrosion and freeze-up during liquefaction. With advanced materials science and predictive manufacturing, W.R. Grace continues to expand high-performance moisture control across healthcare, energy infrastructure, and specialty industrial applications.

Honeywell UOP leads molecular sieve dehydration for EV batteries and semiconductor fabs

Honeywell UOP sets the global standard for molecular sieves and synthetic zeolites, serving petrochemical, electronics, and advanced manufacturing markets. Its Molsiv™ MB masterbatch, launched in 2025–2026, delivers seven-times higher moisture-loading capacity in thermoplastics versus calcium oxide, accelerating adoption in smart packaging and engineered plastics. Deep integration with Honeywell Connected Plant software enables real-time monitoring of desiccant bed performance, supporting predictive maintenance and optimized replacement cycles. Honeywell’s technical leadership in dehydration to below 0.1 ppm is mission-critical for EV battery gigafactories and semiconductor cleanrooms. To meet rising Asian demand, the company expanded molecular sieve production in 2026, directly supporting regional electronics and battery manufacturing growth.

BASF SE strengthens industrial adsorbents through Verbund integration and Sorbead platforms

BASF leverages its Verbund manufacturing strategy to deliver activated alumina and specialty adsorbents with unmatched supply security. Its Sorbead® aluminosilicate desiccants are widely used in compressed air systems and gas drying, offering high water capacity and mechanical strength. In February 2026, BASF consolidated logistics hubs in India and Malaysia to accelerate delivery across its Industrial Solutions segment, while commissioning a new Mangalore dispersions line to support desiccant-enhanced coatings and sealants. Vertical integration into chemical precursors allows BASF to buffer raw-material volatility and maintain pricing stability. This end-to-end control positions BASF as a preferred supplier for large-scale industrial dehydration, process reliability, and moisture-sensitive infrastructure projects worldwide.

Mitsubishi Gas Chemical pioneers dual-action PharmaKeep for oxygen and moisture control

Mitsubishi Gas Chemical differentiates through dual-action desiccant chemistry that combines moisture absorption with oxygen scavenging. Its PharmaKeep™ platform protects pharmaceuticals from both hydrolysis and oxidation, extending shelf life for biologics and medical devices. In late 2025, MGC introduced a canister-style PharmaKeep engineered for high-speed automated bottling lines, accelerating adoption in global pharma manufacturing. By 2026, MGC’s oxygen-absorbing desiccants had become essential components in premium drug packaging systems. Guided by its KAITEKI Vision 35 strategy, the company prioritizes medicine and food quality preservation, positioning dual-function adsorbents as a strategic growth pillar across healthcare logistics, sterile packaging, and advanced medical applications.

Arkema accelerates specialty desiccants for electronics and green energy after portfolio reshaping

Arkema has repositioned itself as a pure-play Specialty Materials leader, divesting its Intermediates business in late 2025 to focus on high-growth adsorbents through its CECA platform. The company projects 12% annual growth in advanced electronics for 2026, driven by desiccant demand from 5G and IoT infrastructure. Arkema is also investing in bio-based molecular sieves and renewable sourcing to decarbonize traditional zeolite production. Its strength in bonding and assembly materials enables integrated solutions where desiccants are embedded directly into adhesives and coatings for construction and automotive applications. This systems-level approach allows Arkema to capture value across electronics protection, energy efficiency, and next-generation moisture-control architectures.

United States: Pharma-Grade Precision and Energy-System Drying Drive Demand

The U.S. desiccant market is evolving through a convergence of pharmaceutical compliance, HVAC transformation, and energy infrastructure investment. In March 2024, W. R. Grace & Co. expanded its fine chemicals facility in South Haven, Michigan, lifting capacity by 25% to support high-purity silica-based desiccants and adsorbents. This expansion directly addresses FDA-aligned requirements for moisture-sensitive Active Pharmaceutical Ingredients, where even marginal humidity exposure can degrade product stability and shelf life. The move underscores how pharmaceutical-grade desiccants are transitioning from commodity consumables to validated, compliance-critical components within regulated drug manufacturing and packaging workflows.

Beyond pharmaceuticals, the U.S. Environmental Protection Agency’s AIM Act allowance allocations for 2026 are reshaping HVAC and refrigeration ecosystems. The accelerated phase-down of high-GWP refrigerants has increased adoption of low-GWP alternatives that require advanced molecular sieve desiccants for effective moisture removal. These materials are now integral to preventing acid formation and compressor failure in next-generation systems. Parallel to this, electronics logistics protection has emerged as a growth vector. Technology hubs in Texas and California reported a 12% rise in IoT-enabled smart desiccants during 2025. These systems embed humidity sensors and real-time alerts to protect high-value semiconductor shipments, reflecting the market’s shift toward data-driven moisture control solutions. Energy infrastructure is reinforcing this trajectory, with Porocel Corporation expanding activated alumina production in Arkansas to serve hydrogen purification and drying needs tied to federally backed clean energy programs.

China: AI-Driven Efficiency and Battery Manufacturing Set New Performance Benchmarks

China’s desiccant industry is advancing through large-scale digitalization and tight integration with strategic manufacturing sectors. By late 2025, chemical clusters across Jiangsu and Zhejiang deployed AI-driven process controls in silica gel manufacturing, reducing energy intensity by approximately 15% while achieving tighter pore-size distribution. This level of precision is critical for electronic-grade desiccants used in semiconductors and advanced electronics, where uniform adsorption performance directly affects yield and reliability. The emphasis on smart factory optimization reflects a broader national objective to elevate functional material quality while lowering production costs and emissions.

Capacity and capability expansion is also evident at the specialty chemical level. In November 2025, BASF commissioned a high-performance production line in Nanjing, integrating Controlled Free Radical Polymerization to support additives and dispersants for moisture-barrier coatings and premium desiccants. The most powerful demand catalyst, however, is electric vehicle battery manufacturing. Under China’s 2026 Green Battery Initiative, gigafactories must maintain moisture levels below 1% relative humidity. This requirement has driven rapid deployment of rotor-based desiccant systems capable of delivering ultra-low dew points of minus 40 degrees Celsius. Domestic suppliers are scaling molecular sieve wheel production, embedding desiccants deeper into China’s battery value chain and reinforcing long-term structural demand.

India: Localization, Cold Chain Expansion, and Food Safety Standards Reshape Usage

India’s desiccant market is increasingly defined by localization strategies and infrastructure-led consumption. In 2025, Desicca Chemicals Pvt. Ltd. upgraded its Maharashtra facility to exceed British and American Chemical Society benchmarks for adsorption capacity. This move targets India’s expanding generic pharmaceutical sector, where localized production of compliant desiccants reduces import dependency and strengthens supply chain resilience. As Indian drug manufacturers scale exports, demand is rising for desiccants that meet stringent global pharmacopoeia expectations.

Infrastructure development is amplifying this momentum. The PM Gatishakti master plan has prioritized the construction of 100 new cold-storage warehouses, directly increasing consumption of calcium chloride and silica gel desiccants for agricultural preservation and food logistics. Regulatory reform is reinforcing qualitative shifts in product selection. In late 2025, the Bureau of Indian Standards introduced revised moisture-control guidelines for food packaging, incentivizing non-toxic, food-grade bentonite clay desiccants over cobalt-based indicators. This change is gradually redefining procurement norms across packaged food, nutraceuticals, and export-oriented agri-products, positioning India as a fast-growing market for safer and regulation-aligned moisture control solutions.

Germany: Sustainability Mandates and Advanced Materials Innovation

Germany’s desiccant market reflects Europe’s broader sustainability and circular economy agenda, combined with advanced materials research. In 2025, Clariant accelerated its EcoTain initiative by launching bio-based bentonite desiccants under the DESI PAK brand. These products deliver an estimated 40% lower carbon footprint compared with synthetic alternatives and are increasingly specified by luxury goods exporters and automotive OEMs seeking to decarbonize packaging and logistics without compromising moisture protection.

Innovation is extending beyond conventional adsorbents. BASF disclosed in its 2025 research briefing the use of AI platforms such as QKnows to accelerate discovery of Metal-Organic Frameworks. These materials are being piloted in 2026 for high-capacity atmospheric water harvesting and industrial gas drying, signaling a potential leap in adsorption efficiency. Regulatory pressure is also reshaping product design. From January 2026, German packaging laws mandate that desiccant canisters contain at least 30% recyclable material. This has prompted companies like TROPACK to transition toward mono-material housings and biodegradable sachets, aligning functional performance with circular economy compliance.

Comparative Snapshot: Desiccant Market Dynamics by Country

Desiccant Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Technology or Regulation Shift

|

Strategic Outcome

|

|

United States

|

Pharma compliance and HVAC transition

|

Smart desiccants and molecular sieves

|

High-value, validated applications

|

|

China

|

EV battery manufacturing and AI factories

|

Ultra-low dew point rotor systems

|

Scale-driven performance leadership

|

|

India

|

Pharma localization and cold chain build-out

|

Food-grade and pharma-grade desiccants

|

Import substitution and volume growth

|

|

Germany

|

Sustainability mandates and advanced R&D

|

Bio-based adsorbents and MOFs

|

Low-carbon differentiation

|

Desiccant Market Report Scope

Desiccant market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Silica Gel, Molecular Sieves, Activated Alumina, Activated Charcoal, Bentonite Clay, Calcium Chloride, Metal-Organic Frameworks), By Form (Beads and Pellets, Powder, Packets and Sachets, Canisters and Stoppers, Desiccant Sheets and Cards), By Application (Pharmaceuticals, Electronics, Food and Beverage, Packaging and Logistics, Air and Gas Drying, Energy, Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

W. R. Grace & Co., Clariant AG, BASF SE, Honeywell International Inc., Evonik Industries AG, Mitsubishi Chemical Group Corporation, Arkema S.A., Porocel Corporation, Fuji Silysia Chemical Ltd., Hengye Inc., Desicca Chemicals Pvt. Ltd., Tropack Packmittel GmbH, Aptar CSP Technologies, Calgon Carbon Corporation, Shin-Etsu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Desiccant Market Segmentation

By Type

- Silica Gel

- Molecular Sieves

- Activated Alumina

- Activated Charcoal

- Bentonite Clay

- Calcium Chloride

- Metal-Organic Frameworks

By Form

- Beads and Pellets

- Powder

- Packets and Sachets

- Canisters and Stoppers

- Desiccant Sheets and Cards

By Application

- Pharmaceuticals

- Electronics

- Food and Beverage

- Packaging and Logistics

- Air and Gas Drying

- Energy

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Desiccant Industry

- W. R. Grace & Co.

- Clariant AG

- BASF SE

- Honeywell International Inc.

- Evonik Industries AG

- Mitsubishi Chemical Group Corporation

- Arkema S.A.

- Porocel Corporation

- Fuji Silysia Chemical Ltd.

- Hengye Inc.

- Desicca Chemicals Pvt. Ltd.

- Tropack Packmittel GmbH

- Aptar CSP Technologies

- Calgon Carbon Corporation

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive