Synthetic Zeolites Market 2025–2034: $9.2 Billion to $12.1 Billion at 3.1% CAGR Driven by FCC Catalyst Innovation, Green Hydrogen Purification, and SAF Conversion Technologies

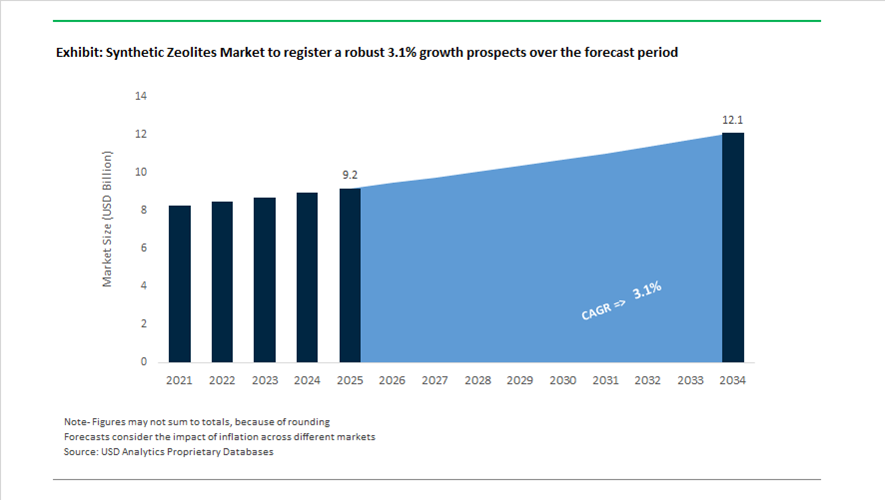

The global synthetic zeolites market is valued at $9.2 billion in 2025 and is projected to reach $12.1 billion by 2034, expanding at a CAGR of 3.1%. Demand is anchored in fluid catalytic cracking (FCC) catalysts, hydroprocessing catalysts, molecular sieves, pressure swing adsorption (PSA) systems, and advanced depolymerization catalysts used across refining, petrochemicals, hydrogen purification, LNG processing, and circular polymer recycling. While refinery throughput growth remains moderate, high-value applications in sustainable aviation fuel (SAF), renewable diesel, green hydrogen purification, and chemical recycling are reshaping the performance requirements of zeolite frameworks. Multi-zeolite architectures, tailored pore-size distribution, improved acidity control, and enhanced thermal stability are central to next-generation catalyst design.

Refining and petrochemical catalyst demand strengthened in 2024. In January 2024, ExxonMobil commissioned a $2 billion expansion at its Baytown complex, including significant upgrades to FCC units that rely heavily on synthetic zeolite catalysts for improved conversion efficiency. In February 2024, W.R. Grace confirmed that China Coal Shaanxi Energy & Chemical Group doubled its UNIPOL polypropylene license capacity to 600 kilotons per year, supported by advanced catalyst systems incorporating zeolitic structures. In August 2024, BASF launched a new FCC catalyst with multi-zeolite architecture engineered to increase butylene yield and naphtha octane, giving refiners flexibility between fuels and petrochemicals. In late 2024, Honeywell was selected to supply adsorption-based purification systems for the Rovuma LNG project in Mozambique, deploying high-performance zeolite molecular sieves to remove water, CO₂, and hydrocarbon contaminants before liquefaction. In 2024, Honeywell’s Ecofining technology became fully operational at the St1 Gothenburg biorefinery, producing approximately 200,000 tons annually of SAF and renewable diesel using zeolite-supported processing systems.

Portfolio realignment and integration intensified during 2025 and 2026. In early 2025, BASF started up its first commercial loopamid facility in Shanghai, applying advanced chemical recycling technologies that likely incorporate zeolite-based depolymerization catalysts to convert textile waste into nylon 6. During 2024 and 2025, Arkema expanded its Siliporite molecular sieve portfolio with new grades optimized for PSA purification of green hydrogen, targeting removal of trace CO and moisture from electrolytic hydrogen streams. In September 2025, Technip Energies announced a definitive agreement to acquire Ecovyst’s Advanced Materials & Catalysts business, including Zeolyst International, with closing expected in Q1 2026. This transaction integrates high-margin zeolite synthesis directly into Technip’s technology licensing and engineering platform. In early 2026, Albemarle confirmed the pending sale of a controlling stake in Ketjen and finalized its exit from the Eurecat joint venture, streamlining its portfolio toward lithium energy storage while stepping away from downstream zeolite-based catalyst services. In January 2026, Honeywell’s eFining technology received recognition as an Energy Transition Solution of the Year, leveraging advanced zeolite catalysts to convert methanol into SAF with greenhouse gas reductions of up to 88% compared to conventional jet fuel. These refinery upgrades, hydrogen purification expansions, SAF conversion platforms, and catalyst portfolio realignments are defining the structural trajectory of the synthetic zeolites market through 2034.

Synthetic Zeolites Market Trends and Opportunities: Petrochemical Reorientation, Green Detergents, and Carbon Capture Innovation

FCC Catalyst Innovation Driving Petrochemical Feedstock Flexibility and Olefin Yield Optimization

The Synthetic Zeolites market is undergoing a strategic transformation as refineries pivot from fuel-centric operations toward petrochemical feedstock optimization, driven by declining internal combustion engine (ICE) demand and rising consumption of light olefins such as propylene and butylene. Advanced fluid catalytic cracking (FCC) catalysts, enriched with high-performance zeolite structures such as ZSM-5 and Y-type zeolites, are enabling refiners to maximize value extraction from heavier feedstocks.

This transition is evident in large-scale refinery upgrades. In early 2025, Sinopec expanded FCC turnaround projects across five major facilities, implementing petrochemical-focused catalyst systems designed to comply with China 6 emission standards while increasing olefin yields. These next-generation catalysts, often comprising up to 50% synthetic zeolite content, enable efficient conversion of heavy gas oils into high-value intermediates, reinforcing the shift toward crude-to-chemicals (C2C) strategies.

ZSM-5 additives, typically deployed at 3% to 10% loading, are central to this evolution due to their shape-selective catalytic properties, which suppress undesired byproducts and enhance propylene selectivity. This molecular-level control is positioning synthetic zeolites as critical enablers of refinery margin optimization, particularly in Asia and the Middle East where petrochemical integration is accelerating.

Phosphate-Free Detergent Regulations Accelerating Global Adoption of Zeolite 4A Builders

Regulatory pressure on phosphate and phosphonate builders is significantly reshaping the demand landscape for synthetic zeolites, particularly in the home care and detergent formulations market. Global bans and restrictions aimed at mitigating eutrophication and aquatic toxicity are driving the widespread adoption of Zeolite 4A as a sustainable water-softening agent.

In February 2026, reinforced regulatory alignment between the European Union and U.S. Environmental Protection Agency (EPA) further strengthened phosphate-free detergent mandates, solidifying Zeolite 4A’s position as the industry-standard builder chemical. This regulatory clarity is creating stable, long-term demand for synthetic aluminosilicates in both developed and emerging markets.

From a performance perspective, Zeolite 4A delivers rapid ion-exchange kinetics, achieving approximately 95% calcium removal within five minutes, making it highly suitable for low-temperature, short-cycle washing programs that reduce household energy consumption. This aligns with broader sustainability trends in consumer products.

Additionally, export dynamics are reinforcing market expansion. Data from India’s Department of Chemicals and Petrochemicals indicates growing international demand for synthetic detergent intermediates, with exports reaching approximately $6.87 million, highlighting the increasing role of emerging economies as key suppliers of eco-friendly zeolite-based formulations.

Synthetic Zeolites as High-Performance Adsorbents in Carbon Capture and CCUS Technologies

A major growth opportunity for the Synthetic Zeolites market lies in their application as advanced adsorbents in Carbon Capture, Utilization, and Storage (CCUS) systems, where their tunable pore structures enable high selectivity for CO₂ separation. This positions synthetic zeolites as critical materials in the global transition toward low-carbon industrial processes and decarbonization technologies.

Commercial deployment is gaining momentum. In 2024, Zeochem AG expanded its supply of Zeolite 13X adsorbents for EU-backed carbon capture projects, demonstrating the scalability of zeolite-based solutions beyond traditional gas drying applications. Similarly, Honeywell UOP is advancing its DACSIV carbon capture technology, leveraging engineered zeolite frameworks optimized for selective CO₂ adsorption over nitrogen in post-combustion environments.

Beyond capture, synthetic zeolites are enabling carbon utilization pathways. Research published in early 2026 highlights the effectiveness of zeolite-supported catalysts (e.g., Ru/ZSM-5) in CO₂ methanation, achieving over 95% methane selectivity. This supports the development of Power-to-Gas systems, where captured carbon is converted into synthetic fuels using renewable hydrogen. These advancements are positioning synthetic zeolites at the center of carbon circularity and sustainable energy ecosystems.

Circular Economy Opportunity: Sustainable Zeolite Production from Industrial Waste Streams

The transition toward circular and sustainable manufacturing is unlocking new growth pathways through the synthesis of zeolites from industrial waste streams, including coal fly ash, blast furnace slag, and rice husk ash. This approach reduces dependence on virgin raw materials while addressing waste management challenges, aligning with global green chemistry and resource efficiency goals.

Recent research demonstrates the technical and economic viability of this approach. Studies from 2025 confirm that Class F fly ash can be converted into high-purity Na-X and Na-P1 zeolites via hydrothermal synthesis within 24 hours, significantly reducing production costs compared to conventional sodium silicate-based methods. This cost advantage is particularly relevant for large-scale environmental applications, including wastewater treatment and soil remediation.

From an environmental perspective, waste-derived zeolite production reduces reliance on energy-intensive bauxite mining, lowering the overall carbon footprint of the manufacturing process. Pilot projects in China and India are already leveraging these bio-based zeolites for applications such as ammonium removal in agricultural runoff, supporting compliance with increasingly stringent water quality regulations.

This circular synthesis model is emerging as a high-impact innovation pathway, enabling manufacturers to combine cost efficiency, sustainability, and regulatory compliance, while expanding the application scope of synthetic zeolites across environmental and industrial sectors.

Synthetic Zeolites Market Share and Segmentation Insights

Zeolite A Leads Synthetic Zeolites Market with Strong Detergent Builder Demand

Zeolite A accounted for 32.80% of the synthetic zeolites market in 2025, driven by its dominant role as a phosphate-free detergent builder in laundry formulations. Its uniform 4Å pore structure enables efficient calcium ion exchange, improving water softening and detergent performance. The global shift toward phosphate-free detergents has significantly increased demand for zeolite A across developed and emerging markets. The 2025 market trend emphasizes the regulatory-driven phosphate replacement, where detergent manufacturers rely on optimized zeolite A grades compatible with modern formulations, including cold water detergents and enzyme-based systems.

Detergent Builders Segment Drives High-Volume Synthetic Zeolite Consumption

Detergent builders accounted for 42.80% of synthetic zeolites market demand in 2025, reflecting their essential role in enhancing cleaning efficiency and formulation performance in household and industrial detergents. Zeolites replace phosphates by softening water and improving surfactant effectiveness, making them indispensable in modern detergent systems. The scale of global detergent production ensures sustained high-volume demand. The 2025 trend centers on the compact and concentrated detergent shift, where zeolite particle size, morphology, and bulk density are optimized for unit-dose pods and high-active formulations, ensuring rapid dispersion, compatibility, and consistent performance.

Consumer Chemicals Segment Leads End-Use Demand with Global Detergent Production Scale

Consumer chemicals accounted for 42.80% of synthetic zeolites market demand in 2025, driven primarily by their use in laundry detergents, dishwashing products, and household cleaners. The widespread adoption of zeolite-based formulations in phosphate-restricted markets underpins strong consumption. Continuous innovation in detergent chemistry further supports demand for high-performance zeolites. The 2025 industry focus highlights performance-enhanced zeolite grades, where manufacturers optimize particle size distribution, ion exchange capacity, and compatibility with enzymes and bleach systems, enabling improved cleaning efficiency while meeting sustainability and cost targets in consumer chemical formulations.

Synthetic Zeolites Market Competitive Landscape

The synthetic zeolites market in 2026 is driven by molecular engineering, low-template synthesis, and ultra-stable frameworks like USY and ZSM-5. Key players are advancing high-performance zeolite catalysts for FCC units, hydrogen purification, and bio-refinery applications aligned with decarbonization and circular feedstock strategies.

BASF Advances Nano-Engineered Zeolite Catalysts with X3D® Technology and Verbund Integration

BASF leads the synthetic zeolites market through advanced catalyst engineering and integrated Verbund production systems. Its ECMS division contributed to a Group EBITDA of €6.6 billion in 2025, reflecting strong catalyst demand. The Zhanjiang Verbund site enhances localized production of zeolite-based catalysts for Asia-Pacific petrochemical expansion. BASF’s X3D® technology embeds nano-zeolites into hierarchical structures, improving diffusion efficiency and reducing coke formation in FCC processes. The company is targeting CO2 emissions of 17.2–18.2 million metric tons in 2026, aligning zeolite innovation with decarbonization goals. Its portfolio supports emission control, refining efficiency, and sustainable chemical production.

Honeywell UOP Strengthens Molecular Sieve Leadership Through Spin-Off and Hydrogen Purification Expansion

Honeywell UOP is transforming into a specialty chemicals pure-play following the 2026 spin-off of its Advanced Materials business. The new entity is expected to generate $3.8 billion in annual revenue with EBITDA margins above 25%. Expansion of zeolite production capacity in China supports growing demand in natural gas processing and hydrogen purification markets. Its MOLSIV™ molecular sieves are critical for PSA systems, enabling high-purity hydrogen production for fuel cells. The $1.81 billion acquisition of Air Products’ LNG business integrates zeolite dehydration technologies into global LNG value chains. Honeywell’s focus on high-selectivity adsorbents strengthens its position in clean energy applications.

Clariant Scales Zeolite Catalysts for Bio-Based Feedstock Conversion and Emission Control Applications

Clariant is positioning itself as a leader in sustainable transition catalysis using advanced zeolite frameworks. Its partnership with Vertimass enables conversion of bio-alcohols into SAF through CADO technology. The company’s CHA-structured zeotypes and ZSM-5 analogs are widely used in MTO processes and NOx reduction systems. Clariant achieved a 17.8% EBITDA margin in 2025, driven by high-margin catalyst solutions. Its Pentasil and Beta zeolite powders are industry standards for VOC abatement and industrial emission control. The company’s focus on bio-refinery catalysts aligns with global decarbonization and circular economy initiatives.

Arkema Expands High-Purity Molecular Sieves for Ethylene Dehydration and Hydrogen Processing

Arkema is strengthening its position in synthetic zeolites through its Siliporite® molecular sieve portfolio. The Siliporite® 3A OPX range is optimized for cracked gas dehydration in ethylene plants, reducing coking and improving operational efficiency. Arkema’s zeolites are also used in isomerization and alkylation processes to meet stringent fuel standards. Its PHYG adsorbents support hydrogen production by protecting catalyst beds in SMR and PSA units. The company is integrating zeolite materials into advanced composites and bio-based applications, expanding its functional materials portfolio. Its focus on energy and chemical sector integration drives demand for high-performance adsorbents.

Tosoh Strengthens High-Silica Zeolite Leadership for Refining, Emission Control, and Hydrogen Economy

Tosoh is a global leader in high-silica zeolites, leveraging its integrated production capabilities and Zeolyst partnership. Its Eco-Business segment focuses on zeolite applications in automotive emission control and VOC capture systems. Government certification of its low-carbon ammonia projects supports expansion in hydrogen-related technologies. Tosoh’s HSZ materials offer superior hydrothermal stability, making them ideal for FCC and heavy oil processing. The company is also developing complementary materials such as polymer electrolytes for water electrolysis. Its diversified portfolio supports refining efficiency, environmental compliance, and hydrogen economy growth.

India Synthetic Zeolites Industry Anchored in CCU Testbeds and Refinery Expansion

India’s synthetic zeolites industry is increasingly shaped by carbon capture deployment and downstream petrochemical optimization. In May 2025, the Department of Science and Technology launched five Carbon Capture and Utilisation testbeds, with a flagship initiative at Indian Institute of Technology Bombay focusing on engineered zeolite frameworks for catalyst-driven CO2 capture. This program positions synthetic zeolites as a core material platform for indigenous clean-tech scale-up, particularly in emissions-intensive cement manufacturing. Complementing academic pilots, a public-private CCU plant in Ballabhgarh, Haryana, commissioned in partnership with JK Cement, demonstrated the feasibility of zeolite adsorption systems capturing two tonnes of CO2 per day for conversion into value-added building materials.

Refining and fuel-transition policies are reinforcing structural demand. Indian Oil Corporation’s plan to raise national refining capacity to 106 million tonnes per annum by 2031 is accelerating procurement of ZSM-5 and FCC catalysts to maximize propylene yields. Parallelly, under the National Green Hydrogen Mission, zeolite-enabled methanol-to-jet pathways are being integrated at refinery clusters to meet ICAO CORSIA requirements from 2026 onward. In consumer chemicals, rising phosphate bans across Asia-Pacific are supporting steady exports of Zeolite 4A detergent intermediates, reinforcing India’s role as a regional supply node for environmentally compliant builders.

China Synthetic Zeolites Industry Driven by High-Purity Electronics and Water Compliance

China’s synthetic zeolites market is transitioning from volume-driven applications toward high-purity and environmentally critical use cases. The Ministry of Industry and Information Technology’s 2025–2026 roadmap prioritizes OLED-grade synthetic zeolites for moisture-sensitive encapsulation, directly supporting domestic semiconductor self-sufficiency targets. At the industrial scale, BASF integrated advanced zeolite catalyst units into its Zhanjiang Verbund site by late 2025, lowering the carbon intensity of petrochemical intermediate production while improving catalyst lifecycle efficiency.

Environmental regulation is a second structural driver. Stricter 2025 water quality norms issued by the Ministry of Ecology and Environment have accelerated adoption of Zeolite Y and mordenite for ammonium and heavy metal removal across Yangtze River Delta industrial zones. In energy chemicals, newly commissioned coal-to-olefins plants in 2025 are deploying SAPO-34 zeolites to enhance olefin selectivity while cutting energy consumption by an estimated 12%. Together, these shifts indicate a deliberate policy-led migration toward performance-critical zeolite frameworks rather than bulk commodity grades.

United States Synthetic Zeolites Industry Centered on Biofuels and Direct Air Capture

The United States synthetic zeolites industry is being reshaped by renewable fuels and carbon management technologies. In October 2025, Honeywell UOP introduced Biocrude Upgrading technology, using specialized zeolite catalysts to convert agricultural and forestry residues into drop-in e-SAF and marine fuels. This development aligns zeolite demand directly with decarbonization pathways for hard-to-abate transport sectors. In parallel, Honeywell’s DACSIV platform achieved a scaling milestone in late 2025, deploying modular synthetic zeolite adsorbents for Direct Air Capture across multiple Permian Basin sites.

Regulatory pressure in water treatment is reinforcing municipal demand. Updated 2025 directives from the Environmental Protection Agency on arsenic and MTBE contamination have expanded the use of ammonium-exchanged Zeolite Y, which demonstrates stable arsenate removal across wide pH ranges. In renewable fuels, W. R. Grace & Co., in partnership with Advanced Refining Technologies, is supplying zeolite-based catalysts for renewable diesel production from waste cooking oils, strengthening the circular feedstock ecosystem.

Japan Synthetic Zeolites Industry Advancing Membranes and Hydrogen Combustion

Japan’s synthetic zeolites landscape is defined by materials science leadership and energy efficiency gains. In 2025, researchers at Nagoya Institute of Technology developed ionic liquid-modified ZSM-5 membranes exhibiting superior H2O permselectivity for CO2 conversion reactors, positioning zeolites as functional membranes rather than passive adsorbents. Industrial deployment is already underway, with Japanese firms commercializing nano-sheet zeolite membranes that reduce energy consumption in alcohol dehydration by roughly 30% compared to conventional distillation.

Policy alignment with carbon neutrality is reinforcing catalyst demand. Under Japan’s 2025 carbon-neutral R&D grants, Chabazite zeolites are being advanced for selective catalytic reduction systems in hydrogen combustion engines. Companies such as Mitsui are actively scaling membrane-based separation technologies, consolidating Japan’s position at the high end of the synthetic zeolite value chain where purity, selectivity, and lifecycle efficiency outweigh volume considerations.

Comparative Snapshot: Synthetic Zeolites Industry by Country

Synthetic Zeolites Market County Level Snapshot

|

Country

|

Primary Demand Anchor

|

Dominant Zeolite Types

|

Structural Market Direction

|

|

India

|

CCU pilots, refinery expansion, SAF

|

ZSM-5, FCC, Zeolite 4A

|

Indigenous scale-up and regional exports

|

|

China

|

Electronics purity, water treatment, CTO

|

SAPO-34, Zeolite Y, Mordenite

|

Policy-driven shift to high-performance grades

|

|

United States

|

Biofuels, DAC, water compliance

|

Zeolite Y, specialty DAC adsorbents

|

Decarbonization-led catalyst demand

|

|

Japan

|

Membranes, hydrogen engines

|

ZSM-5 membranes, CHA

|

High-selectivity, energy-efficient applications

|

Synthetic Zeolites Market Report Scope

Synthetic Zeolites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.2 Billion

|

|

Market Size (2034)

|

$12.1 Billion

|

|

Market Growth Rate

|

3.1%

|

|

Segments

|

By Type (Zeolite A, Zeolite X, Zeolite Y, Zeolite ZSM-5, Beta Zeolites, Mordenite and Chabazite), By Application (Catalysts, Adsorbents and Molecular Sieves, Detergent Builders, Environmental Remediation, Agriculture), By End-Use Industry (Oil and Gas, Chemical and Petrochemical, Consumer Chemicals, Medical and Healthcare, Construction and Building Materials)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International Inc., BASF SE, W. R. Grace & Co., Clariant AG, Arkema Group, Tosoh Corporation, Albemarle Corporation, Zeolyst International, Ecovyst Inc., Zeochem AG, KNT Group, Zhejiang Longsheng Group, Anten Chemical Co., Ltd., National Aluminium Company Limited, Haldor Topsoe A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Synthetic Zeolites Market Segmentation

By Type

- Zeolite A

- Zeolite X

- Zeolite Y

- Zeolite ZSM-5

- Beta Zeolites

- Mordenite and Chabazite

By Application

- Catalysts

- Adsorbents and Molecular Sieves

- Detergent Builders

- Environmental Remediation

- Agriculture

By End-Use Industry

- Oil and Gas

- Chemical and Petrochemical

- Consumer Chemicals

- Medical and Healthcare

- Construction and Building Materials

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Synthetic Zeolites Industry

- Honeywell International Inc.

- BASF SE

- W. R. Grace & Co.

- Clariant AG

- Arkema Group

- Tosoh Corporation

- Albemarle Corporation

- Zeolyst International

- Ecovyst Inc.

- Zeochem AG

- KNT Group

- Zhejiang Longsheng Group

- Anten Chemical Co., Ltd.

- National Aluminium Company Limited

- Haldor Topsoe A/S

*- List not Exhaustive