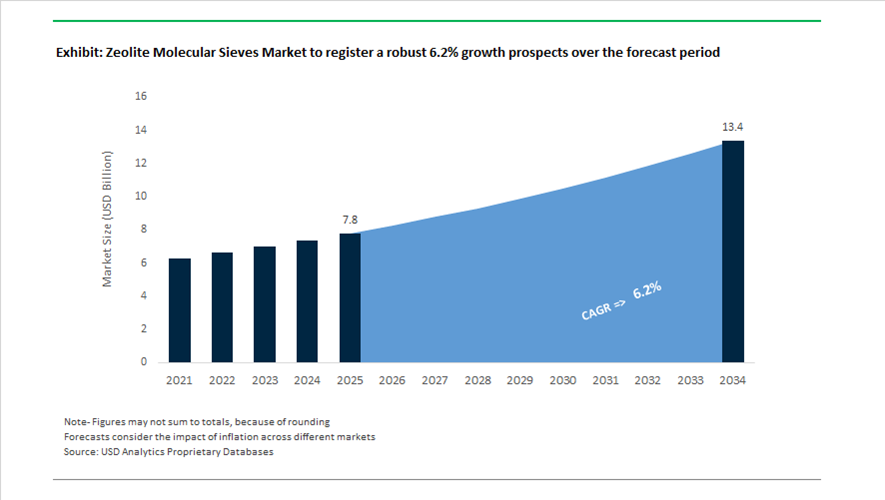

Zeolite Molecular Sieves Market Overview 2025–2034: $7.8 Billion to $13.4 Billion at 6.2% CAGR Driven by Advanced Catalysis, Direct Air Capture, and Green Hydrogen Infrastructure

The Zeolite Molecular Sieves market is valued at $7.8 billion in 2025 and is projected to reach $13.4 billion by 2034, expanding at a CAGR of 6.2%. Zeolite molecular sieves—crystalline aluminosilicates with highly ordered microporous structures—are critical in fluid catalytic cracking (FCC), petrochemical refining, gas separation, dehydration, environmental remediation, and emerging carbon capture technologies. Market expansion is being propelled by increasing refinery complexity, the global transition toward sustainable fuels, expansion of polypropylene capacity, and deployment of direct air capture (DAC) systems. Simultaneously, innovation in nano-structured and 3D-printed zeolite architectures is improving mass transfer efficiency and catalytic selectivity.

Strategic consolidation and capacity expansion reshaped the competitive landscape beginning in 2024. In January 2024, Zeochem acquired Sorbead India, strengthening its footprint in Asia across pharmaceutical-grade and packaging desiccant molecular sieves. In February 2024, China Coal Shaanxi Energy & Chemical Group doubled its license for Grace’s UNIPOL polypropylene process technology, expanding capacity to 600 kilotons per year and reinforcing demand for high-performance zeolite catalysts. In August 2024, BASF launched the Fourtiva™ FCC catalyst utilizing Multiple Frameworks Topology (MFT), integrating distinct zeolite structures to enhance butylene yield and improve naphtha octane. Throughout 2024–2025, Albemarle positioned Ketjen Corporation as an independent catalyst-focused subsidiary, intensifying development of customized zeolite systems capable of processing heavier, sulfur-rich refinery feedstocks aligned with energy transition requirements.

Environmental and decarbonization technologies accelerated in 2025. Honeywell UOP commercially rolled out DACSIV™, a zeolite-based adsorbent engineered for high-selectivity CO₂ capture in Direct Air Capture installations, supporting negative emission infrastructure. In July 2025, W.R. Grace introduced next-generation SYLOBEAD® adsorbents for high-purity gas separation, targeting sulfur and moisture removal in natural gas while minimizing CO₂ formation. In May 2025, Evonik launched nano-zeolite additives designed to enhance catalytic kinetics and energy efficiency in specialty chemical and energy storage applications. Tosoh Corporation announced a major expansion of zeolite production capacity in September 2025 to address growing demand across Asian refining and environmental markets.

Advanced manufacturing and green hydrogen integration are defining the 2026 outlook. BASF is scheduled to start up its commercial-scale 3D-printed catalyst plant in Ludwigshafen in Q1 2026, leveraging proprietary X3D technology to create structured zeolite catalysts with optimized flow distribution and increased accessible surface area. In February 2026, Topsoe upgraded its financial guidance, citing strong momentum in zeolite-enabled green ammonia and sustainable aviation fuel (SAF) technologies, including participation in the Yanbu Green Hydrogen Project. Parallel R&D efforts are exploring hybrid adsorbent systems that integrate traditional zeolite frameworks with bio-based materials to enhance sustainability metrics.

The zeolite molecular sieves market is advancing toward high-selectivity CO₂ adsorbents, multi-framework FCC catalysts, nano-zeolite additives, 3D-printed structured catalysts, and hydrogen-integrated ammonia systems. Demand from petrochemical upgrading, polypropylene expansion, gas purification, and carbon removal infrastructure will sustain mid-single-digit growth through 2034.

Trends and Opportunities in the Zeolite Molecular Sieves Market

Strategic Technology Shifts Driving High-Performance, Application-Specific Zeolite Demand

The zeolite molecular sieves market is transitioning from bulk separation applications toward embedded, performance-critical roles across hydrogen mobility, advanced electronics cooling, decentralized gas generation, and battery manufacturing. Between 2024 and 2026, demand is increasingly shaped by purity thresholds, energy efficiency mandates, and space-constrained system design, elevating zeolites from commodity adsorbents to mission-critical functional materials.

Trend 1: Integration of On-Board Hydrogen Purification for Fuel Cell Mobility

The commercialization of Fuel Cell Electric Vehicles (FCEVs) is driving the integration of zeolite-based Pressure Swing Adsorption systems directly into vehicle architectures. These compact PSA modules are essential to protect platinum catalysts from trace contaminants introduced during refueling.

To comply with the International Organization for Standardization ISO 14687:2019 hydrogen fuel quality standard, automotive OEMs are deploying Zeolite 5A and Zeolite 13X to achieve hydrogen purity levels of 99.97%. Technical evaluations conducted during 2024–2025 show that refueling with inadequately purified grey or blue hydrogen can reduce fuel cell efficiency by up to 15% within the first 1,000 operating hours, making on-board purification economically unavoidable.

Recent industrial pilots demonstrate that lithium-exchanged zeolites deliver CO₂ adsorption capacities of 2.5 mmol/g at 25°C, materially outperforming silica gel and activated carbon. This higher adsorption density allows for smaller and lighter PSA modules, a decisive advantage for long-haul hydrogen trucks and fuel-cell bus fleets where weight and packaging constraints directly affect vehicle range and payload economics.

Trend 2: Ultra-Low Dew Point Desiccants for High-Density Electronics Cooling

The rapid expansion of AI-driven high-performance computing and direct-to-chip liquid cooling is creating a specialized demand for 3A zeolite molecular sieves as permanent moisture control agents within dielectric coolant loops.

Modern data center cooling systems require dew points below −70°C to prevent dielectric fluid breakdown and micro-arcing. The 3 Å pore diameter of Zeolite 3A selectively adsorbs water molecules with a kinetic diameter of 2.6 Å, while excluding larger molecules found in synthetic hydrocarbon and fluorinated dielectric fluids. This molecular selectivity ensures long-term coolant integrity without fluid loss or contamination.

Manufacturers such as Zeochem have commercialized ultra-stable 3A zeolites capable of withstanding thousands of regeneration cycles, enabling service lifetimes of 5 to 10 years without desiccant replacement. This durability materially reduces Total Cost of Ownership for hyperscale facilities operated by firms such as Google and Microsoft, where unplanned cooling downtime carries multi-million-dollar operational risk.

Opportunity 1: Decentralized Oxygen Generation via Zeolite Vacuum Swing Adsorption

The push for resilient, decentralized infrastructure is accelerating the adoption of zeolite-based Vacuum Swing Adsorption oxygen generators across healthcare, mining, and industrial sites.

Oxygen concentrators utilizing Lithium-X (LiX) zeolites now deliver continuous oxygen streams at 90–95% purity, leveraging the zeolite’s high nitrogen selectivity. These systems are replacing pressurized cylinder logistics in remote mining operations and rural hospitals, where transport costs and supply disruptions materially inflate oxygen availability risks.

Government-backed “oxygen security” initiatives in India and Southeast Asia are prioritizing modular PSA and VSA plants built on synthetic zeolites with surface areas approaching 1,000 m²/g. Compared with cryogenic separation, these systems deliver 30–40% lower energy consumption for small-to-medium capacity installations, making them structurally advantaged in decentralized and emergency response scenarios.

Opportunity 2: Dynamic VOC Absorption in Lithium-Ion Battery Giga-Factories

Lithium-ion battery manufacturing generates substantial volumes of volatile organic compounds, particularly N-Methyl-2-pyrrolidone (NMP) during electrode coating. This has created a high-value opportunity for zeolite-based rotor concentrators within giga-factory exhaust systems.

Benchmark sustainability deployments show that dual-rotor zeolite concentrators achieve 99.5% VOC removal efficiency. In large-scale installations, including those implemented by TSMC and other electronics leaders, zeolite-coated fiberglass rotors reduce pressure drop by 10% and cut exhaust fan power demand by 17.7% compared with ceramic fiber systems.

By concentrating VOC streams up to 20×, zeolite rotors dramatically improve the economics of thermal oxidation and solvent recovery. For a typical battery giga-factory, this translates into annual savings of over 480 MWh of electricity and a reduction of approximately 266 metric tons of CO₂ emissions, directly supporting corporate Net-Zero manufacturing commitments and tightening environmental compliance margins.

Zeolite Molecular Sieves Market Share and Segmentation Insights

Raw Material Type Market Share: Synthetic Zeolite Leads with Tailored Pore Structure and Catalytic Precision

Synthetic zeolite dominates the zeolite molecular sieves market with a 72.80% share in 2025, driven by its precisely engineered pore size distribution, uniform crystal structure, and tunable surface chemistry. These properties make synthetic zeolites essential for high-value applications in catalysis, gas separation, and adsorption processes. Natural zeolites serve lower-cost applications with less stringent performance requirements. A key trend is zeolite structure engineering, where advanced synthesis and computational design enable customized frameworks such as ZSM-5 and zeolite Y with optimized acid site distribution and pore architecture, improving efficiency in petrochemical refining and industrial separation processes.

Application Market Share: Adsorbents and Separation Leads with Industrial Gas Purification and PSA Optimization

Adsorbents and separation account for 42.80% of the zeolite molecular sieves market in 2025, supported by their critical role in gas separation, dehydration, and purification across industrial processes. Applications include oxygen and nitrogen separation, natural gas drying, and chemical stream purification. Catalysts, detergent builders, environmental remediation, and agriculture represent additional demand segments. A key growth driver is pressure swing adsorption optimization, where advanced zeolite adsorbents are engineered for higher working capacity, faster adsorption kinetics, and improved durability under cyclic pressure conditions, enabling energy-efficient separation processes in hydrogen purification and biogas upgrading.

Zeolite Molecular Sieves Market Competitive Landscape

The Zeolite Molecular Sieves market in 2026 is driven by pore-level engineering, with advanced ZSM-5, Beta, and SAPO-11 structures enabling superior hydrothermal stability, adsorption selectivity, and catalytic efficiency, alongside growing adoption of circular catalyst regeneration services to reduce Scope 3 emissions and optimize refining performance.

Honeywell UOP Leads LNG and SAF Transformation with Integrated Zeolite Adsorption and Ecofining™ Technologies

Honeywell UOP dominates high-value zeolite molecular sieves applications through its integrated adsorption and process licensing capabilities. Its Rovuma LNG project deployment utilizes advanced zeolite systems for CO2, water, and hydrocarbon removal across 18 Mtpa capacity. The Ecofining™ platform is accelerating SAF production using proprietary zeolite catalysts for waste oil conversion. Capacity expansion in Asia-Pacific supports rising demand for ULSD compliance and FCC propylene maximization. Honeywell’s bundled licensing model ensures optimal reactor kinetics and adsorbent performance. This integration strengthens its leadership across natural gas processing and renewable fuel technologies.

BASF Advances Emission Control and Digitalized Zeolite Manufacturing with Cu-SSZ-13 Catalysts

BASF is reinforcing its position through advanced zeolite catalysts targeting emission control and sustainable chemical production. Its Cu-SSZ-13 SCR catalyst delivers superior NOx and N2O reduction for Euro 7 and China 6 standards at lower temperatures. The Zhanjiang Verbund site integrates digitalized manufacturing for high-purity zeolite powders in Asia. BASF reported €6.6 billion EBITDA in 2025, supporting reinvestment into green catalyst innovation. The company is expanding applications into carbon-neutral plastics and electrospun membrane technologies. This strategy aligns zeolite performance with regulatory and sustainability-driven industrial demand.

Arkema CECA Expands Molecular Sieve Capacity for LNG, Bioethanol Dehydration, and Gas Purification

Arkema, via CECA Molecular Sieves, is scaling production to meet surging demand in gas separation and biofuel processing markets. Expansion at the Honfleur facility strengthens supply of Siliporite® molecular sieves for LNG dehydration. Its 3A zeolites enable selective water removal in ethanol dehydration, maximizing biofuel yield. The Airsiev® 13X portfolio supports PSA/VSA systems for hydrogen purification and air separation. Arkema’s focus on energy-efficient adsorption reduces regeneration energy in TSA systems. This positions the company as a preferred partner in industrial gas and sustainable fuel applications.

W. R. Grace Drives FCC Performance with ZSM-5 Additives and Circular Catalyst Recycling Solutions

W. R. Grace leads the refining catalyst segment through advanced zeolite-based FCC additives and circular catalyst services. Its ZAVANTI™ ZSM-5 additive enhances propylene yield and activity retention in modern FCC units. Growth in Middle East and Asia is driven by hydrocracking demand for heavy crude processing. The Valleyfield Innovation Hub continues to develop multi-pollutant additives reducing SOx and NOx emissions. Grace is expanding closed-loop recycling programs to recover and reuse spent zeolite catalysts. This circular approach improves refinery efficiency while aligning with global sustainability mandates.

Clariant Strengthens High-Silica Zeolite Portfolio for SAF, Emission Control, and Fuel Upgrading

Clariant is advancing high-silica zeolite innovation for fuel upgrading, emission control, and sustainable aviation fuel synthesis. Its SAPO-11 and ZSM-22 zeolites enable precise hydroisomerization with up to 86.5% selectivity for iso-alkanes. The award-winning HySat™ platform reflects its broader shift toward chromium-free and environmentally compliant catalyst systems. Beta and Pentasil zeolites are increasingly used in VOC and N2O emission control retrofits. Clariant’s customizable SiO2/Al2O3 ratios deliver superior thermal and acid resistance for demanding industrial applications. This technical flexibility supports its leadership in next-generation catalytic materials.

China Zeolite Molecular Sieves Market: Green Manufacturing Mandates, Synthetic Zeolite A Dominance, and EV Catalyst Demand Surge

China continues to dominate the global zeolite molecular sieves market, driven by its 2025–2026 industrial action plan for specialty chemicals and non-ferrous materials, emphasizing green manufacturing, smart production systems, and high-purity material development. The Ministry of Industry and Information Technology (MIIT) is targeting a 5% annual increase in industrial added value, with a strong focus on ultra-high purity zeolites for semiconductor manufacturing, EV supply chains, and advanced petrochemical processing. Capacity expansion by global players such as Honeywell UOP, particularly in propylene-rich cracking catalysts and high-performance adsorbents, is reinforcing China’s leadership in refinery-integrated zeolite applications.

Regulatory shifts are accelerating structural demand changes, with updated Clean Production Standards (2026) driving the phase-out of phosphate-based detergent builders, leading to a surge in demand for Synthetic Zeolite A, which now accounts for ~60% of global consumption. Additionally, China’s stringent Guo VI emission standards are triggering large-scale adoption of zeolite-based selective catalytic reduction (SCR) catalysts in heavy-duty vehicles, creating non-discretionary replacement cycles. Innovation remains a priority under the 14th Five-Year Plan, with funding directed toward hierarchical zeolite structures (micro- and mesoporous systems) to enhance diffusion efficiency in complex catalytic reactions, positioning China at the forefront of next-generation zeolite material science and industrial scalability.

India Zeolite Molecular Sieves Market: PLI-Driven API Growth, PCPIR Investments, and Water Treatment Applications

India is emerging as a high-growth market for zeolite molecular sieves, supported by Production Linked Incentive (PLI) schemes, expanding petrochemical infrastructure, and increasing demand for purification technologies in pharmaceuticals and water treatment. The commissioning of 38 greenfield bulk drug projects has established a domestic capacity of 56,800 MT per annum, significantly boosting demand for zeolite-based molecular sieves used in API purification, solvent drying, and gas separation processes. This aligns with India’s broader ambition to become a global hub for pharmaceutical intermediates and specialty chemicals.

Strategic developments such as Zeochem’s acquisition of Sorbead India and Swamble Chemicals have strengthened local supply chains, enhancing availability of high-performance molecular sieves for pharma, food packaging, and industrial gas applications. Investment under the pharmaceutical PLI scheme has reached ₹4,814 crore, with additional focus on zeolite-based oxygen concentrator materials, highlighting the growing role of zeolites in healthcare infrastructure resilience. Furthermore, massive investments of ₹3,49,192 crore in PCPIRs are driving demand for ZSM-5 and Y-type zeolite catalysts in refinery and petrochemical complexes. Rapid urbanization is also fueling adoption of natural zeolites such as clinoptilolite for ammonium removal in municipal wastewater treatment, positioning India as a key market for environmental and industrial zeolite applications.

Germany Zeolite Molecular Sieves Market: Sustainable Fuel Catalysis, FCC Innovation, and Carbon Footprint Compliance

Germany leads the European zeolite molecular sieves market, with a strong focus on circular economy applications, sustainable fuel production, and advanced catalytic technologies. A major development is the strategic partnership between Clariant and Vertimass (March 2026) to scale CADO (Catalytic Alcohol-to-Olefins) technology, leveraging advanced zeolite catalysts to convert bio-based alcohols into sustainable aviation fuels and transport fuels. This underscores Germany’s leadership in green fuel innovation and decarbonized chemical processes.

Product innovation remains robust, with BASF’s Fourtiva FCC catalyst delivering improved butylene yields while minimizing coke and dry gas formation, enhancing refinery efficiency. Regulatory frameworks such as the European Sustainability Reporting Standards (ESRS) are mandating detailed Product Carbon Footprint (PCF) disclosures, accelerating the shift toward low-energy hydrothermal synthesis of zeolites. Additionally, German research institutions are advancing zeolite membrane technologies for hydrogen purification, supporting the growth of the green hydrogen economy. With Clariant reporting CHF 3.915 billion in 2025 sales, a significant portion of R&D is now directed toward sustainable adsorbents and catalysts, reinforcing Germany’s position as a global innovation hub for zeolite-based technologies.

United States Zeolite Molecular Sieves Market: FCC Catalyst Innovation, Carbon Capture Breakthroughs, and Shale Gas Demand

The United States zeolite molecular sieves market is characterized by intensive R&D, strong shale gas-driven demand, and leadership in refining catalyst technologies. Companies like W.R. Grace are driving innovation with solutions such as ACHIEVE® 400 FCC catalyst technology (2025), designed for dynamic refinery environments and optimized hydrocarbon cracking performance. The deployment of RIVE® Molecular Highway® technology further enhances the selectivity of Y-zeolite catalysts, enabling more efficient processing of heavier feedstocks in modern refineries.

Carbon capture and sustainability are emerging as key growth areas, with Honeywell UOP collaborating with the University of Texas (2026) to develop zeolite-solvent hybrid systems aimed at reducing the cost of CO₂ capture in heavy industries. The U.S. shale gas boom, particularly in the Permian Basin, is driving significant demand for 3A and 4A molecular sieves for gas dehydration, essential for LNG export infrastructure requiring ultra-low moisture levels. Additionally, companies such as Albemarle and PQ Corporation are transitioning toward heavy-metal-free zeolite formulations, anticipating stricter EPA regulations, thereby strengthening the U.S. position in sustainable and high-performance zeolite solutions.

Japan Zeolite Molecular Sieves Market: Hydrogen Economy Integration, Functional Innovation, and High-Purity Applications

Japan is advancing the zeolite molecular sieves market through its focus on functional innovation, hydrogen economy integration, and high-purity specialty materials. A key breakthrough is Tosoh Corporation’s development of zeolite-integrated polymer electrolytes (January 2026) for PEM water electrolysis, aimed at reducing reliance on costly fluorinated materials while enhancing stability and efficiency in hydrogen production systems. This innovation aligns with Japan’s broader strategy to lead in clean energy technologies and hydrogen infrastructure development.

Tosoh’s FY2026–2028 Medium-Term Business Plan prioritizes growth in specialty zeolites for emission control, gas separation, and advanced chemical processing, reinforcing Japan’s leadership in precision material engineering. Collaborative research with Yamagata University has also demonstrated new applications in printed electronics using zeolite-modified inks, expanding the material’s role beyond traditional catalysis. Sustainability remains a core focus, with METI-backed projects achieving ISCC PLUS certification for low-carbon chemical production at facilities like Nanyo and Yokkaichi. Additionally, Japanese firms are pioneering the use of zeolite-based SCR catalysts in maritime applications, supporting compliance with IMO 2030 NOx emission standards, further solidifying Japan’s position in next-generation zeolite applications across energy, electronics, and environmental sectors.

Zeolite Molecular Sieves Market Report Scope

Zeolite Molecular Sieves Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.8 Billion

|

|

Market Size (2034)

|

$13.4 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Raw Material Type (Natural Zeolite, Synthetic Zeolite), By Product Form (Powder, Beads and Granules, Pellets, Zeolite Membranes), By Application (Catalysts, Adsorbents and Separation, Detergent Builders, Environmental Remediation, Agriculture and Animal Feed), By Pore Size (Small Pore, Medium Pore, Large Pore)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International Inc., Arkema S.A., BASF SE, W. R. Grace & Co., Tosoh Corporation, Zeochem AG, Albemarle Corporation, Clariant AG, Zeolyst International, Axens S.A., KNT Group, Hengye Group, Luoyang Jianlong Micro-Nano New Materials Co., Ltd., Sinopec Corporation, Sorbead India

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Zeolite Molecular Sieves Market Segmentation

By Raw Material Type

- Natural Zeolite

- Synthetic Zeolite

By Product Form

- Powder

- Beads and Granules

- Pellets

- Zeolite Membranes

By Application

- Catalysts

- Adsorbents and Separation

- Detergent Builders

- Environmental Remediation

- Agriculture and Animal Feed

By Pore Size

- Small Pore

- Medium Pore

- Large Pore

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Zeolite Molecular Sieves Market

- Honeywell International Inc.

- Arkema S.A.

- BASF SE

- W. R. Grace & Co.

- Tosoh Corporation

- Zeochem AG

- Albemarle Corporation

- Clariant AG

- Zeolyst International

- Axens S.A.

- KNT Group

- Hengye Group

- Luoyang Jianlong Micro-Nano New Materials Co., Ltd.

- Sinopec Corporation

- Sorbead India

*- List not Exhaustive