Single-Serve Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Surge in E-Commerce and Consumer Convenience Driving Single-Serve Packaging Market Toward $67.9 Billion by 2034

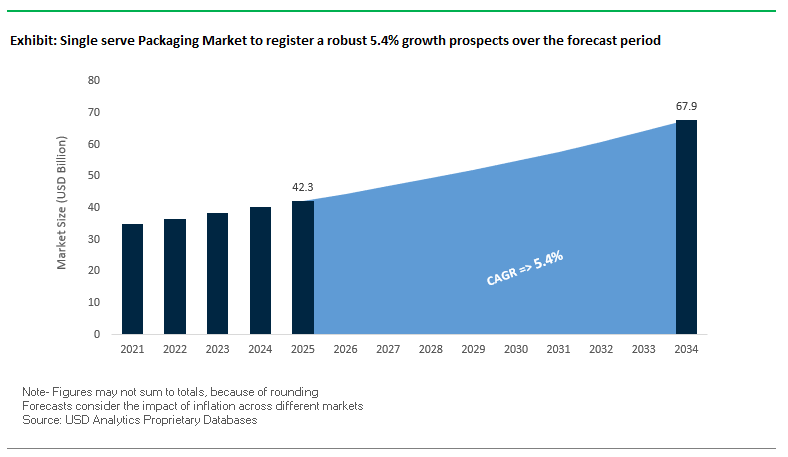

The global single-serve packaging market is projected to grow from $42.3 billion in 2025 to $67.9 billion by 2034, reflecting a CAGR of 5.4%, fueled by e-commerce expansion, health-conscious consumer trends, and innovations in active and sustainable packaging. Single-serve packaging solutions are increasingly vital for efficient logistics, hygiene, and product freshness, meeting the evolving expectations of food, beverage, and pharmaceutical sectors.

Key Insights for Industry Professionals:

- E-commerce and Last-Mile Logistics: Growing online food delivery and retail demand durable, lightweight, and tamper-proof single-serve packs.

- Health, Hygiene, and Convenience: Consumer preference for easy-to-use, hygienic formats drives adoption in food, beverage, and pharma.

- Active Packaging Innovation: Freshness indicators, time-temperature sensors, oxygen scavengers, and antimicrobial agents extend shelf life and enhance safety.

- Sustainable Materials Adoption: Paper-based, compostable, and biodegradable materials are increasingly preferred, with paper and paperboard contributing 38% of revenue in 2024.

- Regulatory and Industry Support: Manufacturers are aligning with sustainability initiatives and recycling mandates, further promoting eco-friendly single-serve packaging.

These factors position single-serve packaging as a critical growth segment for companies seeking operational efficiency, consumer appeal, and sustainability compliance.

Market Analysis: Strategic Acquisitions and Sustainability Awards Are Shaping the Global Single-Serve Packaging Industry

The single-serve packaging market has witnessed a wave of strategic mergers, acquisitions, and sustainability initiatives, reflecting both consolidation and innovation in the sector. In August 2025, Constantia Flexibles completed its acquisition of Aluflexpack, strengthening its presence in high-value segments, including pharmaceuticals and food packaging. Shortly after, in July 2025, Amcor finalized its merger with Berry Global, creating a global leader with a diversified portfolio of flexible and rigid packaging solutions.

Sustainability remains a key focus, with Huhtamaki earning the EcoVadis gold medal in July 2025 for the fifth consecutive year, reinforcing industry leadership in eco-conscious packaging solutions. Companies are also innovating to meet growing production demands; for instance, in April 2025, Maanshan Hengxi Self Heating Technology expanded its factory, and Smurfit Kappa launched paper-based e-commerce packaging solutions in March 2025, emphasizing lightweight and protective designs.

Earlier developments, such as Constantia Flexibles winning WorldStar Global Packaging Awards in January 2025 and Sonoco divesting its Thermoformed and Flexibles Packaging business in April 2025, indicate a trend of portfolio optimization and recognition for sustainable innovation.

Single Serve Packaging Market: Regulatory Pressure and Opportunities for Circular Innovation

Regulatory Pressure on Plastic Pods and Non-Recyclable Laminates

The single serve packaging market is facing intensifying scrutiny due to its reliance on plastic pods and multi-material laminates that are difficult to recycle. The European Union’s Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025, mandates that all packaging must be recyclable in an economically viable manner by 2030. This directive directly impacts single-serve formats like K-Cups, stick packs, and sachets, which often contain layered plastics and aluminum that are incompatible with existing recycling systems. Non-compliance risks both market access restrictions and financial penalties, creating a strong incentive for brands to redesign their packaging portfolios.

The regulatory environment in the United States also reinforces this trend. In September 2024, the U.S. Securities and Exchange Commission (SEC) fined Keurig $1.5 million for misleading recyclability claims regarding its K-Cup pods. This case serves as a cautionary benchmark, highlighting the reputational and legal risks of greenwashing in single-serve packaging. Together, these developments emphasize that brands must rapidly innovate toward recyclable or compostable formats to maintain regulatory compliance and consumer trust.

Corporate Shift to Monomaterial and Recyclable Structures

Global FMCG and beverage brands are proactively investing in monomaterial and recyclable alternatives to overcome the limitations of legacy formats. Nespresso remains a pioneer in aluminum pod adoption, a material valued for being infinitely recyclable and highly protective. According to its 2024 sustainability report, Nespresso has already established 122,000 collection points worldwide for capsule returns and currently achieves a global recycling rate of 35%, with a stated target of 60% by 2030. This demonstrates a clear corporate roadmap toward circularity.

Beyond aluminum, brands are piloting compostable paper pods as a consumer-centric solution. In September 2024, Nespresso launched a pilot for home-compostable paper pods, designed for markets where aluminum recycling infrastructure remains underdeveloped. The full rollout, expected by 2025, signals a significant expansion of recyclable and compostable single-serve packaging formats. These innovations align with both regulatory mandates and consumer demand for eco-friendly, waste-free alternatives.

Development of Certified Home-Compostable Material Systems

One of the most significant opportunities lies in bio-based and compostable material innovation. Startups and established packaging players are accelerating investment in plant-derived alternatives to petroleum-based plastics. In September 2025, UK-based materials company Xampla secured $14 million in Series A funding to scale its Morro material, a protein-based, home-compostable solution designed to replace plastic linings in cups and sachets. This funding milestone underscores the commercial readiness of next-generation compostable materials.

A technical breakthrough in home-compostable films has further expanded the market’s potential. New structures provide high oxygen and moisture barriers, meeting the strict performance requirements of single-serve formats like soups, coffee, and spice sachets, while being certified to decompose in household compost within months. These innovations not only satisfy zero-waste consumer expectations but also address the infrastructure gaps in emerging markets where formal recycling systems are absent.

Integration of Digital Watermarking for Smart Recycling and Engagement

The integration of digital watermarking presents another transformative opportunity. The HolyGrail 2.0 initiative, a collaboration of more than 130 global companies, has proven the technical viability of this solution in large-scale German recycling trials. Results demonstrated sorting purity rates above 95%, enabling food-grade and non-food-grade plastics to be accurately separated—an essential step toward achieving high-quality recycled content for single-serve packaging applications.

Beyond recycling, digital watermarking enhances consumer engagement and anti-counterfeiting capabilities. Single-serve pouches and pods offer ample surface area for QR codes or invisible watermarks, which consumers can scan with their smartphones. These scans provide access to a digital product passport, detailing ingredients, sustainability credentials, and end-of-life instructions. Moreover, unique digital IDs embedded in packaging act as authentication tools, preventing counterfeiting and enhancing supply chain transparency. By combining smart technology with sustainability, digital watermarking positions single-serve packaging as a next-generation, traceable, and consumer-interactive format.

Competitive Landscape: Leading Single-Serve Packaging Companies Drive Innovation, Sustainability, and Global Market Expansion

The global single-serve packaging market is highly competitive, dominated by companies leveraging advanced materials, innovative designs, and sustainable solutions to cater to food, beverage, and pharmaceutical sectors.

Amcor plc: Pioneering Recyclable and High-Barrier Single-Serve Packaging Solutions

Amcor offers a comprehensive portfolio of coffee pods, flexible pouches, and stick packs across food, beverage, and healthcare industries. The Berry Global merger in July 2025 expanded its global footprint, and AmFiber Performance Paper launched in August 2024 provides a curbside-recyclable, high-barrier packaging solution. Amcor’s sachet films ensure easy-open, contamination-resistant sealing, reducing waste and enhancing efficiency.

Tetra Pak: Leading Aseptic Packaging Solutions with Extended Shelf Life and Safety

Tetra Pak specializes in aseptic single-serve packaging for milk, juices, and beverages, ensuring food safety without refrigeration. In November 2024, the company launched India’s first Tetra Stelo package with Minute Maid, reflecting innovation in emerging markets. Tetra Pak focuses on sustainability, recyclability, and renewable material usage, positioning it as a leader in safe, efficient, and environmentally responsible packaging.

Huhtamaki Oyj: Expanding Sustainable Single-Serve Portfolio Through Flexible Mono-Material Solutions

Huhtamaki offers flexible pouches and sachets, including the blueloop™ mono-material platform, supporting recycling and hygiene. In July 2025, the company introduced a recyclable and compostable ice cream packaging solution, further strengthening its sustainable single-serve offering. Huhtamaki’s products feature high-quality printing, lightweighting, and material efficiency, appealing to sustainability-conscious consumers.

Sonoco Products Company: Focusing on High-Quality Rigid and Flexible Single-Serve Containers

Sonoco provides sanitary rigid paperboard and flexible packaging for snacks, coffee, and powdered beverages. Following the sale of its Thermoformed and Flexibles Packaging business in April 2025, Sonoco is emphasizing core packaging capabilities, including the Sonoco Paper Can, a fully recyclable, durable, and hygienic option.

Constantia Flexibles Group: Driving Innovation and Sustainability in Flexible Single-Serve Packaging

Constantia Flexibles offers mono-material, recyclable packaging solutions across food, pharmaceutical, and consumer goods industries. The Aluflexpack acquisition in August 2025 strengthened its high-value segment presence, while awards in January 2025 recognize sustainable innovations like EcoPeelCover and EcoLamHighPlus. Constantia’s portfolio highlights long-term commitment to product preservation, shelf life enhancement, and circular economy solutions.

Single serve Packaging Market Share Insights, 2025-2034

Pouches and Sachets Dominate Market Share by Product Type in the Single-Serve Packaging Industry

Pouches and sachets hold 35% of the single-serve packaging market, underscoring their dominance as the most cost-efficient, lightweight, and versatile format across emerging and developed economies. Their widespread adoption is anchored in the rise of the “sachet economy” in developing regions, where affordability and portion control enable broader access to branded products in categories such as condiments, detergents, shampoos, and pharmaceuticals. In mature markets, pouches and sachets drive premium convenience, particularly in snacks, nutraceuticals, and ready-to-mix beverages. Their low material usage reduces costs for brand owners and improves distribution efficiency, making them the format of choice for mass-scale, high-volume single-serve applications. While bottles, cups, blisters, and trays address niche and regulated requirements, pouches and sachets remain the foundation of single-serve packaging growth globally.

Food and Beverages Dominate Market Share by End-Use in the Single-Serve Packaging Industry

The food and beverage sector consumes 55% of all single-serve packaging, establishing itself as the primary driver of industry expansion. The demand stems from rising urbanization, busy lifestyles, and the global trend toward on-the-go consumption and portion control. Single-serve bottles for hydration, pouches for snacks and sauces, and cups for dairy and desserts are integral to consumer convenience, while portion-controlled packs help reduce food waste in both retail and foodservice channels. Innovation in barrier technologies, microwave-ready formats, and sustainable single-serve solutions such as recyclable PET bottles and compostable coffee pods further strengthens this segment’s dominance. Although healthcare, cosmetics, and industrial chemicals contribute valuable shares, the food and beverage industry’s sheer consumption volume ensures it remains the cornerstone of global single-serve packaging demand, continuously shaping design, material selection, and sustainability priorities.

United States: Sustainability Laws and Functional Packaging Drive Innovation

The United States single-serve packaging market is evolving under a mix of state-level bans and federal recycling goals. In 2025, states such as Maryland, Oregon, and Rhode Island implemented restrictions on single-use plastics like foam containers and food service ware. These regulations are accelerating the transition toward sustainable materials in single-serve packaging formats. Additionally, the U.S. Environmental Protection Agency (EPA) has set a target to increase the national recycling rate to 50% by 2030, driving investments into recycling infrastructure and circular packaging designs.

Beyond regulations, demand for single-serve formats in military rations, emergency kits, and convenience foods is strong, with suppliers increasingly focusing on lightweight and high-performance packaging. Companies such as ProAmpac are leading this shift with their ProActive Recyclable® portfolio, which features plant-based plastics and paper-based flexible packaging tailored to the snack and food sector. A major innovation trend is the integration of smart packaging features, including freshness indicators and QR code-enabled traceability, which enhance consumer engagement while ensuring safety and transparency.

European Union: Circular Economy Regulations Reshaping Single-Serve Packaging

The European Union single-serve packaging market is being reshaped by the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates minimum recycled content in all packaging formats by 2030. This regulation is particularly critical for sachets and pouches, which have historically been difficult to recycle due to their multi-material laminated structures. To address this, the EU is pushing for mono-material flexible packaging and encouraging the adoption of refill and reuse systems for single-serve products.

The Ecodesign for Sustainable Products Regulation (ESPR), introduced in mid-2024, supports this shift by requiring a Digital Product Passport that provides transparency on recyclability and material sourcing. Another key driver is the ban on PFAS in food contact packaging from August 2026, which is accelerating the development of alternative barrier coatings and materials. Leading innovations include Huhtamaki’s recyclable single-coated paper cups, which contain less than 10% plastic content and are fully recyclable, reflecting how the EU market is combining sustainability mandates with innovation in rigid and flexible single-serve solutions.

China: Lazy Economy and E-Commerce Fueling Premium Single-Serve Packaging

The China single-serve packaging market is heavily shaped by the “14th Five-Year Plan”, which emphasizes plastic pollution control and mandates that, starting June 1, 2025, express delivery companies must use eco-friendly, reusable, or reduced packaging. This is particularly impactful in China’s booming e-commerce sector, where single-serve packaging is critical for logistics efficiency.

Consumer trends are equally influential, with the rise of the “Lazy Economy”, where convenience and time-saving products dominate. This has led to explosive growth in self-heating single-serve food formats such as hotpots and noodles, particularly for in-home consumption. Additionally, China is witnessing a surge in luxury and premium single-serve packaging, with brands adopting advanced printing technologies like 3D platinum embossing and gold foil stamping to create more appealing, tamper-evident solutions. Coupled with government tax incentives for green technology adoption, the Chinese market is becoming a hotspot for innovation and sustainable growth in single-serve formats.

India: Regulatory Push and Rising Dairy & E-Commerce Demand

The India single-serve packaging market is being shaped by the Plastic Waste Management (Amendment) Rules, 2024, which place heavy emphasis on Extended Producer Responsibility (EPR). Effective July 1, 2025, all plastic packaging in India must be traceable through barcodes or QR codes, ensuring accountability across the supply chain. While small MSMEs are exempt, the responsibility falls on manufacturers and importers of raw materials.

The market is seeing rapid adoption of single-serve formats in dairy, processed foods, beverages, and personal care products, largely fueled by the expansion of retail and e-commerce channels. The Indian government’s focus on boosting dairy sector productivity has further increased the demand for cost-effective, portion-sized packaging solutions. Together, regulatory compliance and consumer-driven demand are pushing manufacturers to invest in eco-friendly, traceable, and recyclable single-serve packaging formats.

Japan: Plastic Resource Circulation Strategy Accelerating Paper-Based Formats

The Japan single-serve packaging market is driven by the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective the same year, mandates the redesign or reduction of 12 categories of single-use plastic products, further accelerating the shift toward paper-based and compostable single-serve alternatives.

Japan is also targeting to double the use of renewable materials by 2030 and is enforcing stricter waste-sorting protocols to improve recycling efficiency. This regulatory environment is pushing companies to develop innovative single-serve solutions made from bio-based and paper-based materials, with a strong emphasis on maintaining functionality and consumer convenience. As a result, Japan is emerging as a leader in sustainable innovation for small-format packaging.

Brazil: Reverse Logistics System Strengthening Circularity in Single-Serve Packaging

The Brazil single-serve packaging market is strongly supported by the National Solid Waste Policy (PNRS), which emphasizes recycling, reuse, and waste reduction. The implementation of Law No. 15,088 in January 2025, banning the import of solid waste, is pushing manufacturers to rely on domestic recycling and sustainable raw materials.

A significant government initiative is the reverse logistics system, which makes producers accountable for post-consumer recycling and disposal. This policy has created incentives for companies to design sustainable single-serve formats that can fit into Brazil’s circular economy model. With growing consumer awareness and policy enforcement, Brazil is increasingly adopting eco-friendly single-serve packaging, particularly in food, beverage, and personal care segments.

Single serve Packaging Market Report Scope

Single serve Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$42.3 Billion

|

|

Market Size (2034)

|

$67.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Glass, Metal, Bioplastics), By Product Type (Bottles, Pouches & Sachets, Blister Packs, Cups & Lids, Trays & Clamshells, Tubes & Ampoules), By End-Use Industry (Food & Beverages, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Household & Industrial, Retail & E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Huhtamaki Oyj, Berry Global, Inc., ProAmpac, Sonoco Products Company, Constantia Flexibles, Mondi Group, DS Smith Plc, Sealed Air Corporation, WestRock Company, Winpak Ltd., Tetra Pak Inc., Greiner Packaging International GmbH, Klöckner Pentaplast, EPL Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Single serve Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Bioplastics

By Product Type

- Bottles

- Pouches & Sachets

- Blister Packs

- Cups & Lids

- Trays & Clamshells

- Tubes & Ampoules

By End-Use Industry

- Food & Beverages

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Household & Industrial

- Retail & E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Single serve Packaging Market

- Amcor plc

- Huhtamaki Oyj

- Berry Global, Inc.

- ProAmpac

- Sonoco Products Company

- Constantia Flexibles

- Mondi Group

- DS Smith Plc

- Sealed Air Corporation

- WestRock Company

- Winpak Ltd.

- Tetra Pak Inc.

- Greiner Packaging International GmbH

- Klöckner Pentaplast

- EPL Limited

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, data-driven methodology to deliver precise insights into the global Single-Serve Packaging market. Our approach combines extensive secondary research from regulatory reports, industry publications, company filings, and sustainability databases with primary interviews of packaging engineers, supply chain managers, and innovation leaders across the food, beverage, pharmaceutical, and personal care sectors. Market sizing and growth forecasts are segmented by material type (Plastic, Paper & Paperboard, Glass, Metal, Bioplastics), product type (Bottles, Pouches & Sachets, Blister Packs, Cups & Lids, Trays & Clamshells, Tubes & Ampoules), and end-use industry (Food & Beverages, Healthcare, Personal Care, Household & Industrial, Retail & E-commerce), while also evaluating regional adoption trends in North America, Europe, Asia-Pacific, India, Brazil, and Japan. USDAnalytics also analyzes sustainability drivers, regulatory compliance mandates, and innovations such as monomaterial structures, home-compostable systems, active packaging technologies, and digital watermarking for smart recycling. Competitive intelligence focuses on strategic mergers, acquisitions, and product innovation by leading companies such as Amcor, Huhtamaki, Constantia Flexibles, Tetra Pak, and Sonoco, offering actionable insights for industry professionals seeking operational efficiency, regulatory alignment, and sustainable growth in the single-serve packaging space.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.