Metallized Film Market Overview: Size, CAGR, and Industry Insights

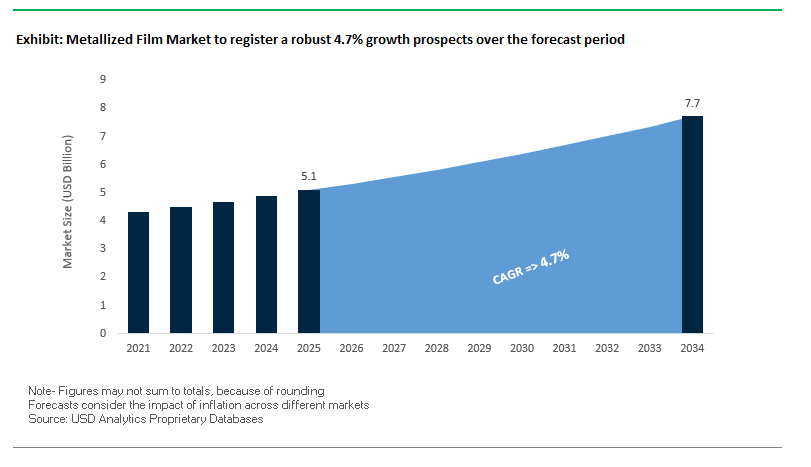

The global Metallized Film Market is projected to grow from $5.1 billion in 2025 to $7.7 billion by 2034, reflecting a CAGR of 4.7%. This growth is fueled by rising demand for high-barrier packaging solutions, aesthetic product differentiation, and advanced applications in electronics, renewable energy, and consumer goods. Metallized films are critical for preserving product integrity, enhancing shelf life, and offering lightweight, cost-effective alternatives to traditional aluminum foils.

Key Insights for Industry Professionals:

- Superior barrier properties: Metallized films protect against moisture, oxygen, and light, reducing spoilage and maintaining product quality.

- Premium aesthetics and branding: Shiny metallic films enable shelf differentiation and premium positioning in sectors like snacks, confectionery, and personal care.

- Electronics and EV applications: Used as dielectric materials in capacitors, smartphones, and renewable energy systems, these films support miniaturization and high-performance requirements.

- Cost-effective lightweighting: Metallized films offer reduced material costs and lower transportation energy consumption, providing both economic and environmental advantages.

- Sustainability focus: Increasing adoption of recyclable and eco-friendly metallic films aligns with global environmental and circular economy trends.

Metallized Film Market Analysis: Key Recent Developments

The metallized films market has experienced significant innovation and strategic investments, driven by the dual need for performance and sustainability. In August 2025, studies highlighted the rapid substitution of traditional aluminum foil with lightweight metallized films, emphasizing their durability and cost-effectiveness. The same month, a Nano Letters study introduced an inhibitor-modified ALD process to produce ultrathin, continuous iridium and platinum films, a breakthrough for advanced electronics.

By July 2025, a major manufacturer announced a Rs 700 crore investment to expand flexible packaging capabilities in India, signaling capacity expansion in response to growing demand. Reports during the same period noted that established converters are investing in wider, faster coating lines, while innovators focus on recycling-ready film structures.

In June 2025, the use of copper in metallic films surged, driven by high-power battery packs and 5G device requirements, while in May 2025, demand for sustainable and protective packaging was recognized as a key market driver. April 2025 marked Mondi Plc’s acquisition of Schumacher Packaging’s Western European assets to enhance its portfolio of high-performance metallized films, and March 2025 highlighted strong results in its flexible packaging segment. As of February 2025, aluminum metallized films dominated with over 66% of revenue in 2024 due to their lightweight, cost-effective, and barrier-efficient nature.

Emerging Trends and Strategic Opportunities in the Metallized Film Market

Accelerated Adoption of High-Barrier Transparent Oxide Coatings

The metallized film market is witnessing a decisive transition from conventional opaque metallized PET and PP films to transparent barrier oxide coatings such as aluminum oxide (AlOx) and silicon oxide (SiOx). This evolution is being driven by rising demand for extended shelf life in sensitive pharmaceuticals and premium foods, while also ensuring that consumers can visibly assess the product—an attribute increasingly tied to brand trust and willingness to pay a premium.

Transparent oxide films deliver oxygen transmission rates (OTR) and water vapor transmission rates (WVTR) on par with metallized polyester, while allowing microwave compatibility—an area where traditional metallized films face limitations. For example, Jindal Films’ Alox-Lyte™ films highlight how nanometer-scale AlOx deposition enables superior barrier properties with about 50% less raw material usage compared to metallized OPP films. This efficiency not only enhances sustainability credentials but also reduces costs.

Furthermore, transparency enables end-of-line metal detection, a major safety advantage for food manufacturers seeking to eliminate contamination risks. As the Flexible Packaging Association (FPA) notes, packaging transparency enhances consumer perception of freshness and quality, reinforcing brand loyalty. Collectively, these benefits are driving the rapid market adoption of transparent high-barrier oxide films as the new gold standard for protective and consumer-friendly flexible packaging.

Strategic Shift to Sustainable and Recyclable Mono-Material Structures

The metallized films sector is undergoing a fundamental design shift toward recyclable mono-material solutions, largely driven by regulatory mandates and brand-owner commitments to sustainability. Historically, multi-material laminates offered strong barrier performance but posed major recycling challenges. Now, the industry is transitioning to polyolefin-based mono-material structures that integrate thin oxide coatings while maintaining compatibility with existing recycling streams.

A landmark partnership in the flexographic printing and film manufacturing industry has demonstrated the feasibility of full polyethylene (PE) high-barrier transparent films that incorporate AlOx GEN II processes, achieving 93% mono-material content. This innovation directly aligns with the EU Packaging and Packaging Waste Regulation (PPWR) goal that all packaging must be recyclable by 2030.

The benefits extend beyond recyclability. Mono-material structures support energy efficiency in processing, with companies like Milliken reporting 5–8% energy savings through polypropylene (PP) additive technologies for thin-wall parts. By combining recyclability, barrier performance, and production efficiency, recyclable mono-material metallized films are becoming a strategic pillar of sustainable flexible packaging.

Development of Ultra-High Barrier Films for Flexible Organic Electronics

The rise of flexible organic electronics including organic photovoltaics (OPVs), OLED displays, and flexible sensors—is creating a high-value opportunity for ultra-barrier metallized films. Unlike food or pharma packaging, these applications demand barrier levels three orders of magnitude higher, with OTR and WVTR requirements that virtually eliminate oxygen and moisture ingress.

Academic research highlights the effectiveness of multi-layer hybrid films that combine organic polymers with inorganic layers to confine permeation to microscopic defects, dramatically improving barrier performance. Such films are critical to protecting expensive organic components in devices like OPVs, where moisture exposure can drastically reduce lifespan and efficiency.

For manufacturers, this represents an opportunity to diversify into the renewable energy and advanced electronics supply chain, offering specialized metallized films that function both as encapsulation barriers and as functional charge transport layers. With flexible electronics poised for rapid adoption in wearable tech, solar applications, and next-generation displays, ultra-high barrier films are set to become a premium niche growth driver in the metallized films market.

Integration of Digital Watermarking for Precision Recycling

A second transformative opportunity lies in embedding digital watermarks directly into metallized films to enhance recycling accuracy. The HolyGrail 2.0 initiative, backed by over 85 global partners, has proven in industrial trials that digital watermarking—when combined with near-infrared (NIR) detection—can enable high-speed, high-precision sorting of flexible packaging.

Trials conducted in Europe between December 2023 and February 2024 demonstrated that marked films could be identified at sorting speeds of 3 meters per second, creating high-purity recycling streams. This precision allows recyclers to distinguish food-grade from non-food-grade plastics, a breakthrough for achieving circularity and meeting safety standards for recycled content in food packaging.

The EU PPWR, approved in late 2024, mandates the integration of standardized digital-marking technologies by August 2026, aligning regulatory pressure with technological innovation. For metallized film producers, embedding watermarking into their products not only secures compliance but also positions them as enablers of the circular economy infrastructure. This regulatory and technological convergence is making digital watermarking a key opportunity for differentiation and leadership in sustainable packaging.

Competitive Landscape: Leading Players in the Global Metallized Film Industry

The global metallized films industry is driven by a combination of advanced polymer expertise, sustainable innovation, and capacity expansion. Leading companies differentiate through high-barrier performance, recyclable solutions, and tailored applications for food, medical, and electronic sectors.

Amcor plc: Innovating Sustainable Metallized Films

Amcor is a global leader in flexible and rigid packaging, offering metallized films for food, beverage, and medical applications. Known for high moisture and oxygen barrier properties, Amcor completed an upgrade at its recycling facility in Heanor, UK in August 2025, enhancing its high-performance recycling infrastructure. The company emphasizes sustainability and lightweighting, aiming for 100% recyclable or reusable packaging by 2025, while providing integrated design, manufacturing, and logistics support for customers.

Jindal Films: Specialty Films and Sustainability-Focused Expansion

Jindal Films manufactures PP and PE metallized films for food, beverage, and medical sectors. In May 2025, it invested Rs 700 crore to expand its Nashik plant with new BOPP and PET lines, reflecting its growth strategy. The company also develops mono-material solutions like EthyLyte™, designed for recyclability, highlighting its focus on innovation, high-barrier films, and sustainability.

Uflex Ltd.: Advancing Flexible Packaging Technologies

Uflex Ltd. is a major Indian multinational specializing in flexible packaging and metallized films for food, pharma, and industrial applications. Its F-ETB-M Film, an easy-tear BOPET metallized film, offers superior oxygen barriers for products like biscuits and mouth fresheners. Uflex invests heavily in eco-friendly technologies and global manufacturing expansion to meet rising demand for sustainable packaging solutions.

DuPont Teijin Films: High-Performance Metallized Film Innovation

DuPont Teijin Films produces metallized polyester films for applications ranging from food packaging to electronics. Its flagship Mylar films combine superior barrier properties with high-gloss aesthetics. The company focuses on sustainable and recyclable solutions, leveraging decades of polymer science expertise to meet demands for high-performance, eco-friendly metallized films.

Celanese Corporation: Polymer Solutions for High-Barrier Films

Celanese provides polymer substrates used in metallized films for flexible electronics and high-barrier packaging. With a focus on cost structure improvements and business differentiation, Celanese optimizes low-cost production in the Western Hemisphere while maintaining high performance. Its materials ensure strength, durability, and moisture/oxygen resistance, making it a strategic partner for metallized film applications.

Metallized Film Market Share Insights

Polypropylene Leads Market Share by Film Material in the Metallized Film Industry

Polypropylene (PP) holds the largest share of the metallized film market at 40%, making it the versatile workhorse of this sector. Its dominance stems from its superior balance of moisture barrier, optical clarity, heat-sealability, and cost-effectiveness, which makes it indispensable in snack food, confectionery, and biscuit packaging. The material’s adaptability to high-speed lamination and printing processes supports brand owners’ demand for lightweight, visually appealing, and shelf-stable packaging. By contrast, PET, with 35% share, is positioned as the premium barrier material for oxygen-sensitive applications such as coffee, powdered beverages, and nutraceuticals, where aroma retention and stiffness are essential. Meanwhile, niche substrates such as PE and polyamide play highly specialized roles in sealant and puncture-resistant laminations, underscoring PP’s unrivaled versatility as the foundation of global metallized film demand.

Packaging Applications Dominate Market Share in the Metallized Film Industry

Packaging accounts for a commanding 75% of metallized film consumption, reflecting its central role in extending product shelf-life and enhancing visual appeal. Metallized films are widely used across snacks, frozen foods, confectionery, dairy products, coffee, and pharmaceuticals, where protection against moisture, oxygen, and light is mission-critical. The segment benefits from dual demand drivers: functional performance, which ensures freshness and product safety, and aesthetic enhancement, as the metallic sheen elevates brand visibility on crowded retail shelves. With regulatory and consumer pressures to reduce aluminum foil usage, metallized films provide a lighter, more recyclable, and cost-effective alternative, cementing their leadership in flexible packaging. Outside packaging, applications such as capacitors, EMI shielding in electronics, reflective insulation for buildings, and decorative films remain high-value niches but collectively represent a fraction of the overall volume compared to packaging’s scale.

United States: EPR Regulations and Technological Breakthroughs Reshape the Metallized Film Industry

The United States metallized film market is undergoing a major transformation due to regulatory and technological shifts. Extended Producer Responsibility (EPR) laws, particularly in California, are creating significant momentum for recyclable and sustainable mono-material metallized films. These laws are reshaping supply chains by compelling manufacturers to develop products that can move seamlessly through existing recycling streams. Alongside regulatory changes, innovation is accelerating with proprietary electron beam evaporation technologies that dramatically enhance barrier properties, making metallized films suitable for critical applications such as medical device packaging, electronics insulation, and integrated circuit storage.

Corporate investments are strengthening U.S. capacity and global competitiveness. In March 2025, Polyplex (USA) LLC initiated trial production on a new brownfield BOPET thin-film line in Alabama, adding an impressive 50,000 metric tons annually to U.S. production capacity. This expansion underscores the strong demand for metallized films across both food packaging and industrial uses. With the food and beverage industry prioritizing extended shelf life and premium aesthetics, and aerospace and defense applications requiring electromagnetic shielding and insulation, the U.S. market is solidifying its role as a leader in advanced metallized films production.

Germany: EU Packaging Regulations and Circular Economy Goals Drive Metallized Film Innovation

Germany’s metallized film market is heavily influenced by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which took effect in January 2025. The regulation mandates a shift away from traditional multi-material laminates toward recyclable mono-material metallized films, forcing innovation across the supply chain. German companies are pioneering solutions such as AluBond technology, which improves metal adhesion, enhances barrier properties, and reduces the need for costly surface treatments before printing. These advancements not only meet EU requirements but also strengthen Germany’s leadership in metallized film technology.

Sustainability and the circular economy remain at the core of Germany’s metallized film industry. The nation’s advanced recycling infrastructure and strong policy support drive adoption of eco-friendly packaging solutions, especially in pharmaceuticals, where the government’s National Pharma Strategy emphasizes safe and sustainable packaging. On the corporate front, Air Liquide’s €250 million investment in Germany to support semiconductor manufacturing is a landmark project, as it ensures access to high-purity metallized films critical for microelectronics. These regulatory, technological, and investment-led shifts are positioning Germany as a global model for sustainable metallized film development.

China: Government Support and Automation Fuel High-Performance Metallized Film Production

China’s metallized film market is being accelerated by robust governmental backing for advanced manufacturing, closely tied to its dual-carbon sustainability targets. Policy measures aimed at simplifying approval processes and fast-tracking new standards are empowering local manufacturers to scale high-performance film production for electronics, packaging, and industrial applications. This proactive government stance is enabling metallized films to play a pivotal role in both consumer and industrial markets, particularly as demand for eco-friendly solutions rises.

Chinese companies are increasingly integrating automation and artificial intelligence into production lines to improve quality control and enhance efficiency. Alongside domestic expansion, multinational FMCG giants are investing in local production facilities to shorten supply chains and meet surging consumer demand. Key applications fueling this growth include snack food packaging, which requires strong oxygen and moisture barrier properties, and consumer electronics, where metallized films are essential for insulation and device durability. Together, these developments ensure that China will remain one of the fastest-growing and most influential metallized film markets worldwide.

India: Policy Initiatives and Industry Investments Position India as a Metallized Film Growth Hub

India is rapidly emerging as a key growth hub in the global metallized film market, supported by strong government initiatives. Programs such as Make in India and the Production Linked Incentive (PLI) scheme are boosting domestic manufacturing while promoting sustainability and circular economy practices. A milestone development occurred in August 2025, when Ester Industries’ joint venture ELITe acquired land in Gujarat to establish India’s first Infinite Loop™ Manufacturing Facility, designed to prioritize recyclability and sustainability in metallized film production.

India’s metallized film industry is also being propelled by technological upgrades and growing demand from the food processing and e-commerce sectors. SRF Limited’s decision in March 2025 to add a fourth Bobst vacuum metallizer to its Indian operations reflects this trend, significantly increasing the supply of advanced metallized BOPP films with high barrier properties. Applications in food and beverage packaging remain dominant, but the pharmaceutical and personal care industries are also becoming major growth drivers. With strong policy support, rising domestic consumption, and substantial corporate investments, India is positioning itself as a powerful player in the global metallized film industry.

Japan: Precision Manufacturing and Specialty Applications Define the Metallized Film Market

Japan’s metallized film market is distinguished by its precision-driven approach and focus on specialty applications. Companies like Toray Industries, Inc. are global leaders in polyester and polypropylene metallized films, consistently delivering products that meet stringent performance and safety standards. Japanese manufacturers are pioneering innovations in thin, high-quality films tailored for cosmetics, pharmaceuticals, and high-tech industries, reflecting the country’s emphasis on high-performance and value-added solutions.

Regulatory policies also strongly shape Japan’s metallized film sector. The Pharmaceuticals and Medical Devices Agency (PMDA) enforces strict packaging requirements, and amendments to the Pharmaceuticals and Medical Devices Act are reinforcing supply stability for drug packaging. Beyond healthcare, metallized films with advanced optical properties are being adopted in display technologies, while durable decorative films are gaining traction in automotive applications. By combining regulatory rigor, cutting-edge technology, and a focus on premium applications, Japan continues to set global benchmarks for excellence in metallized film manufacturing.

Metallized Film Market Report Scope

Metallized Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$7.7 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Metal Type (Aluminum, Copper, Others), By Film Material (PP, PET, PE, Polyamide, Others), By Application (Packaging, Electrical & Electronics, Decorative, Insulation, Other Applications), By End-User (Food & Beverage, Pharmaceuticals & Healthcare, Consumer Electronics, Automotive & Aerospace, Building & Construction, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Jindal Poly Films Ltd., Toray Industries, Inc., Cosmo Films Ltd., Uflex Ltd., Taghleef Industries Group, Polyplex Corporation Ltd., Polinas Plastik Sanayi ve Ticaret A.Ş., Dunmore Corporation, Ester Industries Ltd., SRF Limited, Avery Dennison Corporation, Mitsubishi Polyester Film GmbH, DuPont de Nemours, Inc., Ultimet Films Limited, Vacmet India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metallized Film Market Segmentation

By Metal Type

By Film Material

- PP

- PET

- PE

- Polyamide

- Others

By Application

- Packaging

- Electrical & Electronics

- Decorative

- Insulation

- Other Applications

By End-User

- Food & Beverage

- Pharmaceuticals & Healthcare

- Consumer Electronics

- Automotive & Aerospace

- Building & Construction

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Metallized Film Market

- Jindal Poly Films Ltd.

- Toray Industries, Inc.

- Cosmo Films Ltd.

- Uflex Ltd.

- Taghleef Industries Group

- Polyplex Corporation Ltd.

- Polinas Plastik Sanayi ve Ticaret A.Ş.

- Dunmore Corporation

- Ester Industries Ltd.

- SRF Limited

- Avery Dennison Corporation

- Mitsubishi Polyester Film GmbH

- DuPont de Nemours, Inc.

- Ultimet Films Limited

- Vacmet India Limited

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to provide actionable intelligence on the global Metallized Film Market. Our analysis integrates primary research involving interviews with industry stakeholders, including manufacturers, technology experts, and supply chain leaders, alongside secondary research from company reports, regulatory publications, patent filings, and scientific journals. We evaluate market drivers such as high-barrier packaging solutions, ultra-thin metallized films, recyclable mono-material structures, and emerging applications in electronics, renewable energy, and consumer goods. Advanced forecasting models are applied to assess regional trends across the U.S., Europe, China, India, and Japan, incorporating policy impacts, technological advancements, and sustainability initiatives. USDAnalytics also examines corporate strategies, including capacity expansions, R&D investments, and mergers or acquisitions, while evaluating barrier performance, cost-effectiveness, and eco-friendly innovations such as digital watermarking and transparent oxide coatings. This methodology ensures that industry professionals receive data-driven insights into material selection, application trends, competitive landscape, and strategic growth opportunities within the metallized films ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.