Market Overview: Expanding Role of Multilayer Films and Sustainability in High-Barrier Packaging

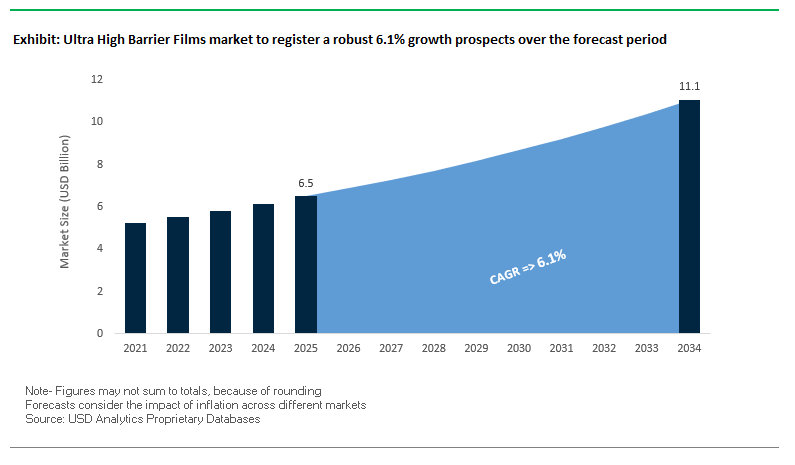

The global ultra-high barrier films market is forecasted to grow from USD 6.5 billion in 2025 to USD 11.1 billion by 2034, advancing at a strong CAGR of 6.1%. This robust growth reflects the rising importance of moisture- and oxygen-resistant packaging solutions across food, pharmaceuticals, and electronics industries. For industry professionals, the key questions focus on how ultra-high barrier films can deliver both performance and recyclability, while addressing supply chain efficiency and compliance with sustainability regulations.

Multilayer films remain the largest product category, offering superior performance through a combination of polymer layers that deliver moisture resistance, oxygen barrier strength, and mechanical durability. The pharmaceutical industry is emerging as a critical growth driver, with blister packaging alone accounting for more than 40% of demand, as it protects sensitive drugs from oxygen, light, and humidity. Asia-Pacific dominates global consumption, led by rapid urbanization, rising disposable incomes, and industrial expansion in food, beverage, and electronics sectors. Sustainability is now central to innovation, with production of recyclable and mono-material barrier films climbing from 480,000 metric tons in 2022 to 620,000 metric tons in 2023, underscoring the industry’s strong push toward circular economy models.

Key Insights for Industry Buyers and Analysts:

- Multilayer films dominance: Superior oxygen and moisture protection drives adoption across industries.

- Pharmaceutical applications rising: Blister packs hold over 40% of pharma-related demand.

- Asia-Pacific leadership: Largest hub for both production and consumption of ultra-high barrier films.

- Sustainability transition: Rapid growth in recyclable and mono-material films reshaping the market.

Market Analysis: Recent Developments in Ultra High Barrier Films Industry

The global ultra-high barrier films industry is undergoing rapid transformation, marked by product innovations, acquisitions, and sustainability-driven launches.

In July 2025, ProAmpac launched recyclable high-barrier fiber-based films with over 90% fiber content, aligned with OPRL guidelines, offering an alternative to plastic-heavy structures in thermoforming applications. Earlier in April 2025, the TOPPAN Group introduced its GL-SP BOPP barrier film, engineered as a recyclable mono-material solution with high barrier functionality. Similarly, in October 2024, Toray Plastics (America) launched Lumirror® TKU2-C, a biaxially oriented PET film with advanced barrier coating designed to extend shelf life and support e-commerce packaging.

Mergers and acquisitions continue to redefine market dynamics. Amcor completed its USD 8.4 billion acquisition of Berry Global in May 2025, strengthening its rigid and flexible packaging portfolio, including high-barrier films. This move, first announced in November 2024, marks one of the most significant consolidations in the packaging industry. In parallel, Sonoco acquired TEQ in March 2025, expanding its healthcare and electronics packaging capabilities.

Competition with alternative barrier solutions is also notable. Sonoco’s May 2025 inauguration of its Metal Packaging Technical & Engineering Center in Ohio demonstrates how steel and tinplate innovations are being positioned as alternatives to high-barrier films in food and aerosol packaging. Meanwhile, corporate restructuring has also impacted the sector, as Ball Corporation divested a 41% stake in its Saudi joint venture in August 2025, streamlining its packaging portfolio to focus on core operations.

Emerging Trends and Opportunities Transforming the Ultra High Barrier Films (UHBF) Market

Accelerated Adoption in the Flexible Electronics Sector for Next-Generation Devices

The ultra-high barrier films market is witnessing a strong demand surge from the flexible electronics sector, where foldable smartphones, OLED displays, and organic photovoltaic devices require advanced encapsulation. These sensitive devices are vulnerable to degradation from oxygen and moisture infiltration, making UHBFs indispensable for extending product lifespan and maintaining performance.

Researchers at DuPont demonstrated that a 25 nm alumina (Al₂O₃) film deposited with Atomic Layer Deposition (ALD) achieved a water vapor transmission rate (WVTR) of 1.7×10⁻⁵ g∙m⁻²∙day⁻¹ a breakthrough that prevents “dark spot” failures in OLEDs. Similarly, findings in ACS Applied Materials & Interfaces showed that encapsulated organic electrochromic displays retained color stability and performance under high humidity, underscoring the crucial role of barrier coatings. Meanwhile, hybrid films combining alternating polyacrylate and nanometric Al₂O₃ layers have achieved WVTRs in the range of 2.3×10⁻² g∙m⁻²∙day⁻¹, representing scalable solutions for mass adoption in consumer electronics.

The proliferation of wearables, foldable displays, and flexible sensors is accelerating the adoption of UHBFs as thin, durable, and transparent protection layers. This convergence of material science and consumer electronics is transforming barrier films from niche solutions into core enablers of next-generation devices.

Strategic Shift Towards Sustainable and Monomaterial High-Barrier Solutions

Alongside performance, sustainability mandates are pushing UHBF development toward monomaterial, recyclable, and bio-based alternatives. Global packaging converters and consumer goods companies are under regulatory pressure from frameworks such as the EU’s Packaging and Packaging Waste Regulation (PPWR), which enforces mandatory recyclability targets by 2030.

Mondi’s FunctionalBarrier Paper Ultimate exemplifies this transition. This paper-based ultra-high barrier solution protects against oxygen and water vapor while being recyclable in paper streams. Backed by a €16 million investment in Poland, it reflects a growing industry trend toward replacing complex laminates with monomaterial alternatives. Similarly, manufacturers are developing mono-PE and mono-PP barrier films that can enter existing recycling streams, ensuring material purity and compliance with circular economy standards.

Meanwhile, tightening plastic taxes across Europe and Asia, alongside corporate pledges from brands like Nestlé and PepsiCo, are reinforcing the shift away from aluminum or multilayer laminates. The result is a dual demand for sustainability and ultra-barrier performance, driving innovation at the intersection of environmental responsibility and technical excellence.

Development of High-Performance Bio-Based Barrier Films

One of the most lucrative growth opportunities lies in bio-based UHBFs that provide functional parity with petroleum-based plastics. This innovation is particularly relevant to the food and beverage packaging market, where shelf life, safety, and sustainability must converge.

Recent academic research highlights the potential of nanocellulose- and clay-reinforced composites in enhancing barrier performance of inherently weak bio-polymers such as PHA or PLA. Another study on chitosan and microcrystalline cellulose films demonstrated strong UV resistance, mechanical stability, and water vapor protection features that can translate directly to commercial packaging.

Beyond passive barriers, active bio-based films are gaining traction. For instance, edible bio-films infused with antimicrobial or antioxidant agents not only preserve food but also reduce spoilage, aligning with global efforts to cut food waste. With major FMCG brands committing to carbon-neutral packaging portfolios, bio-based UHBFs offer a critical pathway to meeting ESG benchmarks while maintaining superior performance.

Integration of Advanced Vapor-Deposited Coatings for Enhanced Performance

The integration of advanced vapor-deposited coatings such as SiOx and AlOx represents a transformative opportunity for both electronics and packaging. Using ALD (Atomic Layer Deposition) or PECVD (Plasma-Enhanced Chemical Vapor Deposition), ultra-thin coatings (<50 nm) can achieve WVTR levels superior to conventional thicker coatings, ensuring long-term protection for OLEDs, solar cells, and pharmaceuticals.

The scalability of these technologies is improving through roll-to-roll (R2R) atmospheric ALD systems, which enable mass production of hybrid polymer-inorganic barrier films. This cost-effective manufacturing method bridges laboratory success with industrial feasibility, making UHBFs more accessible for mainstream use.

Competitive Landscape: Leading Players in the Ultra High Barrier Films Market

The ultra-high barrier films market is highly competitive, defined by R&D investments, sustainability commitments, and global expansions. Key players are differentiating through recyclable mono-material films, strategic acquisitions, and advanced coating technologies.

Amcor plc: Expanding Barrier Film Portfolio with Sustainable Laminates

Amcor offers a diverse portfolio of ultra-high barrier films, including its AmLite recyclable laminate range, which replaces PET and metal layers to reduce carbon footprint. The USD 8.4 billion acquisition of Berry Global in May 2025 significantly expanded Amcor’s plastic packaging capacity, enhancing its position in barrier solutions. With a strategic commitment to 100% recyclable or compostable packaging by 2025, Amcor integrates innovation with global supply chain reach, serving food, healthcare, and personal care industries.

Sealed Air Corporation: Leading in Food Preservation with Cryovac Technology

Sealed Air specializes in ultra-high barrier films for food packaging, with flagship brands such as Darfresh and Cryovac designed for vacuum skin and modified atmosphere packaging. These films extend shelf life for meat, poultry, and cheese products. The company’s core strength lies in application-specific expertise in food preservation. Sealed Air continues to invest in R&D for films compatible with recycling streams, aligning with tightening environmental regulations and rising consumer demand for sustainable solutions.

TOPPAN INC.: Innovating with Transparent High-Barrier BOPP Films

TOPPAN is a leader in transparent high-barrier films, anchored by its GL BARRIER series, which leverages proprietary vapor deposition coating technology. In April 2025, it launched GL-SP BOPP film, a recyclable mono-material solution, underscoring its sustainability commitment. TOPPAN’s R&D focus is on producing transparent films with performance equal to or better than aluminum foil, serving both food and pharmaceutical applications. Its advanced printing and finishing capabilities allow it to offer fully integrated packaging solutions, combining barrier protection with branding advantages.

Mondi Group: Driving Sustainability with Recyclable High-Barrier Films

Mondi offers a wide range of flexible and barrier packaging solutions, with recent developments including its recyclable PET film laminate for food applications. Guided by its “sustainability framework,” Mondi is committed to designing packaging that is recyclable, reusable, or compostable. Its portfolio supports high-speed filling lines and focuses on reducing material weight and food waste, giving it strong traction in the food processing and consumer goods markets.

Sonoco Products Company: Enhancing Healthcare and Electronics Packaging

Sonoco manufactures both rigid and flexible packaging solutions, including a strong portfolio of ultra-high barrier films. Its acquisition of TEQ in March 2025 boosted its healthcare and electronics presence, sectors where barrier films are critical. The company also introduced new frozen food packaging trays in July 2025, complementing its film-based offerings. With expertise in rigid packaging and flexible integration, Sonoco is positioned to deliver complete barrier packaging systems for food, medical, and consumer markets.

Ultra High Barrier Films Market Share Insights

Food & Beverages Anchor Ultra High Barrier Films Market Share by Application

Food and beverages represent 55% of the ultra-high barrier (UHB) films market in 2025, underscoring their central role in driving adoption of advanced barrier technologies. UHB films extend the shelf life of perishable goods like cheese, dried meats, coffee, and ready-to-eat meals by providing unmatched resistance to oxygen, moisture, and gas transmission. This makes them indispensable in reducing global food waste while supporting the industry’s shift toward lightweight, flexible packaging formats. The transition from rigid containers to flexible high-barrier solutions has accelerated in retail and e-commerce channels, where shelf appeal and sustainability are equally critical. Pharmaceuticals, electronics, and cosmetics are high-value segments, with blister packs, OLED displays, and luxury creams increasingly reliant on UHB films, but their aggregate demand trails the enormous scale of food packaging. This dominance highlights how the global food sector directly shapes innovation and material science in ultra-high barrier films.

Transparent Barrier Films Lead Ultra High Barrier Films Market Share by Type

Transparent barrier films account for 45% of the UHB films market in 2025, making them the largest and fastest-growing film type. Their leadership is fueled by the dual advantage of strong oxygen and moisture protection combined with product visibility an increasingly important factor in both food and healthcare packaging. Advanced transparent coatings like aluminum oxide (AlOx) and silicon oxide (SiOx) on PET or BOPP films provide barrier performance comparable to metallized films while allowing consumers and quality inspectors to visually verify product integrity. This is especially critical for fresh foods, medical devices, and pharmaceuticals where visibility drives trust and compliance. Metallized barrier films remain a performance workhorse, excelling in applications requiring light shielding, while white barrier films cater to branding and dairy-focused niches. However, transparent films’ ability to balance visibility, performance, and sustainability ensures they continue to capture the largest share of the UHB film market.

United States: Rising Demand for Ultra High Barrier Films Driven by Sustainability and Advanced Packaging Innovation

The United States ultra high barrier films market is rapidly evolving, fueled by changing consumer preferences and technological innovation. One of the strongest growth drivers is the increasing demand for shelf-stable and ready-to-eat foods, where ultra high barrier films deliver superior protection, extend product shelf life, and preserve flavor integrity. Technological advancements are transforming the packaging landscape, with innovations moving beyond single-solution lacquers to multifunctional thin films that act as anti-corrosion layers, oxygen scavengers, and flavor-neutral protective interfaces simultaneously. This shift not only enhances food safety but also caters to consumer expectations of high-quality packaged goods.

The growth of the U.S. e-commerce industry is reshaping packaging design, requiring lightweight yet durable solutions capable of withstanding long-distance shipping and handling. Companies are introducing recyclable, polyethylene (PE)-based barrier packaging, such as ExxonMobil’s thermoformed food barrier package, to align with sustainability mandates and reduce reliance on mixed-material packaging. Moreover, the U.S. pharmaceutical sector is a major consumer of ultra high barrier films, with growing adoption of anti-counterfeit technologies like RFID tags and holographic labeling to ensure product integrity. Together, these trends position the U.S. as a global leader in high-performance packaging innovation with a strong focus on sustainability.

Germany: Regulatory Mandates and Eco-Design Driving the Ultra High Barrier Films Market

Germany stands at the forefront of the ultra high barrier films market in Europe, largely due to its stringent regulatory framework and leadership in the circular economy. The implementation of the EU Packaging and Packaging Waste Regulation (PPWR) has accelerated the demand for recyclable and eco-friendly packaging solutions, compelling manufacturers to innovate with designs that minimize waste and maximize recyclability. Companies are increasingly developing eco-design solutions, such as flat-pack structures to optimize logistics and water-based inks for sustainable printing, making Germany a model for regulatory compliance and sustainable innovation.

Technological advancements play a critical role in shaping the German market. Leading companies like Klöckner Pentaplast provide PVdC-coated and Aclar laminated films for the pharmaceutical sector, ensuring optimal product protection and shelf-life extension. At the same time, Taghleef Industries’ EXTENDO range delivers exceptional oxygen and moisture barrier properties while preventing mineral oil migration, making it suitable for food safety and aroma protection. Germany’s dual emphasis on strict compliance and eco-design innovation underscores its dominant role in shaping the future of ultra high barrier packaging in Europe.

China: Industrial Growth and Green Transformation Fueling Demand for Ultra High Barrier Films

China’s ultra high barrier films market is experiencing exponential growth, driven by the booming food, pharmaceutical, and logistics sectors. The country’s rapid industrialization and urbanization have amplified the demand for protective packaging, particularly in food and pharmaceuticals, where barrier integrity is vital for consumer safety and product quality. At the same time, the government’s “dual carbon” initiative, aimed at achieving carbon peak and carbon neutrality, is steering industries toward sustainable practices. This has led to stricter packaging regulations, compelling manufacturers to prioritize recyclable and eco-friendly solutions in line with national sustainability targets.

On the technological front, Chinese manufacturers are embracing automation, robotics, and AI-powered production systems to enhance packaging efficiency and stability. A standout development in the region is the widespread use of Biaxially Oriented Polyethylene Terephthalate (BOPET) films, prized for their superior thermal stability, transparency, and barrier strength, making them indispensable for flexible packaging and industrial uses. With its vast manufacturing base and government-backed sustainability agenda, China is rapidly positioning itself as a global hub for next-generation ultra high barrier film innovation.

India: Governmental Push and Food Processing Expansion Driving Ultra High Barrier Films Adoption

India’s ultra high barrier films market is undergoing transformative growth, supported by a mix of governmental initiatives and rising food processing demand. Policies such as “Make in India” and “Zero Effect Zero Defect” are encouraging domestic production, fostering regulatory support, and strengthening industrial infrastructure. This is directly benefiting packaging manufacturers, who are seeing increased demand from India’s expanding food and beverage sector, particularly in ready-to-eat meals, meat, poultry, and bakery products that require durable and hygienic packaging.

Technological innovation is another critical growth driver. Recent investments of over INR 10,000 crore in recycling infrastructure including wash lines, extruders, and decontamination units have enhanced the country’s ability to produce sustainable packaging solutions at scale. Additionally, India’s Plastic Waste Management (Amendment) Rules, which mandate the phase-out of specific single-use plastics, are driving the industry toward biodegradable and recyclable alternatives. This dual push of government-backed regulation and consumer-driven demand is rapidly transforming India into one of the fastest-growing markets for ultra high barrier films in Asia.

Ultra-High Barrier Films Market Report Scope

Ultra High Barrier Films market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.5 Billion

|

|

Market Size (2034)

|

$11.1 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Material Type (PET, PP, PE, PVC, EVOH, PA, Other Materials), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Electronics & Electricals, Other Applications), By Type (Transparent Barrier Films, Metallized Barrier Films, White Barrier Films)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor Plc, Berry Global Inc., Huhtamäki Oyj, Jindal Poly Films Ltd., Mondi Group, Printpack, Sealed Air Corporation, Sonoco Products Company, UFlex Limited, Toppan Inc., Toray Industries, Inc., Klöckner Pentaplast, Constantia Flexibles, Wipak Group, Cosmo Films Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ultra High Barrier Films Market Segmentation

By Material Type

- PET

- PP

- PE

- PVC

- EVOH

- PA

- Other Materials

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Electronics & Electricals

- Other Applications

By Type

- Transparent Barrier Films

- Metallized Barrier Films

- White Barrier Films

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Ultra High Barrier Films Market

- Amcor Plc

- Berry Global Inc.

- Huhtamäki Oyj

- Jindal Poly Films Ltd.

- Mondi Group

- Printpack

- Sealed Air Corporation

- Sonoco Products Company

- UFlex Limited

- Toppan Inc.

- Toray Industries, Inc.

- Klöckner Pentaplast

- Constantia Flexibles

- Wipak Group

- Cosmo Films Limited

*List not Exhaustive

Research Coverage

This detailed report by USDAnalytics investigates the global ultra high barrier films (UHBF) market, examining breakthroughs in multilayer polymer films, monomaterial designs, bio-based composites, and advanced vapor-deposited coatings. The analysis reviews innovations across food, pharmaceutical, electronics, and healthcare applications, highlighting how UHBFs deliver superior oxygen, moisture, and gas barrier properties while enabling recyclability and compliance with sustainability regulations. This report highlights strategic mergers, acquisitions, and capacity expansions, as well as emerging trends in flexible electronics, e-commerce-ready packaging, and active bio-based films, positioning UHBFs as essential enablers of product longevity and ESG alignment. By integrating historic data from 2021 to 2024 with forecasts through 2034, the report provides actionable insights into material diversification, production optimization, and regulatory alignment. This report is an essential resource for manufacturers, packaging converters, brand owners, and industry analysts seeking to navigate competitive dynamics, adopt innovative high-barrier technologies, and capitalize on growth opportunities in global and regional markets.

Scope Highlights:

- Segmentation: By Material Type (PET, PP, PE, PVC, EVOH, PA, Other Materials); By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Electronics & Electricals, Other Applications); By Type (Transparent Barrier Films, Metallized Barrier Films, White Barrier Films)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024; forecast data from 2025 to 2034.

- Companies Covered: Analysis/profiles of 15+ companies including Amcor Plc, Berry Global Inc., Huhtamäki Oyj, Jindal Poly Films Ltd., Mondi Group, Printpack, Sealed Air Corporation, Sonoco Products Company, UFlex Limited, Toppan Inc., Toray Industries, Inc., Klöckner Pentaplast, Constantia Flexibles, Wipak Group, Cosmo Films Limited.

Methodology

The research methodology employed for this report combines rigorous primary and secondary research to deliver a precise and actionable analysis of the ultra high barrier films market. Primary data was sourced through interviews with industry executives, R&D specialists, packaging engineers, and supply chain managers across leading manufacturers and end-use sectors. Secondary research included company annual reports, regulatory frameworks, trade publications, and sustainability disclosures. Market sizing and forecasting were performed using a top-down approach, analyzing historical consumption trends, production capacities, and regional adoption patterns across materials, applications, and film types. Competitive benchmarking assessed strategic mergers, acquisitions, technological innovation, and sustainability initiatives. Emerging trends such as bio-based barrier films, ALD/PECVD coatings, and monomaterial solutions were evaluated through scenario modeling and market simulation. This methodology ensures that stakeholders can confidently identify growth drivers, anticipate regulatory impacts, and optimize operations across high-barrier film applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.