The global Organic Photovoltaics (OPV) sector has accelerated significantly from 2024 through 2025, marked by major improvements in manufacturing scalability, durability, and environmental compliance. In November 2025, the industry celebrated a breakthrough when a large-area 16.94 cm² OPV module achieved 17.85% efficiency, setting a new record and illustrating industry momentum toward high-performance, scalable printing processes. Manufacturing innovations peaked in December 2025, when researchers reported OPV devices achieving 17.4% PCE at coating speeds of 500 mm/s, validating the feasibility of ultra-high-speed roll-to-roll production for future gigawatt-scale facilities.

Sustainability-driven innovation also emerged strongly in August 2025, when a new green solvent engineering approach using o-xylene achieved 20% efficiency with 82% stability retention after 1500 hours, demonstrating OPV’s ability to meet environmental directives including REACH and enabling safer industrial production. Parallel advancements in IoT-focused OPV designs were highlighted in June 2025, when Dracula Technologies upgraded its LAYER® OPV with 15% improved power output using a new silver busbar system—directly addressing the space constraints of miniaturized sensors, wearables, and ESL systems.

In the BIPV category, Heliatek remained the global pace-setter. In October 2024, it launched the HeliaKit platform, enabling architects to rapidly test and deploy OPV façade solutions. The was followed in June 2024 by a major double-façade HeliaSol installation at ESTW in Germany, proving OPV’s adaptability to curved and non-conventional building structures. Earlier, in April 2024, Heliatek achieved IEC 61215 certification, unlocking financing pathways for OPV BIPV. Supporting commercialization, Heliatek expanded distribution through a December 2023 partnership with IGEPA Group, strengthening access to European construction markets. A landmark adoption came when Siemens Energy installed over 150 HeliaSol films directly on factory façades in Germany, exemplifying OPV's retrofit potential for industrial buildings.

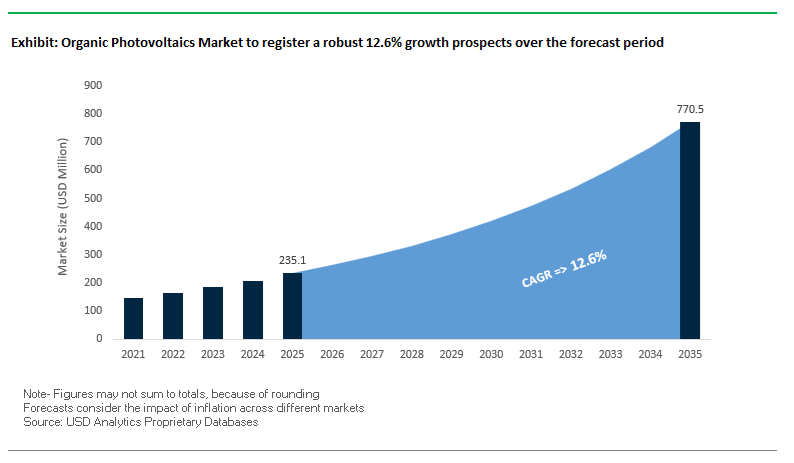

The Organic Photovoltaics (OPV) Market is valued at USD 235.1 million in 2025 and is projected to reach USD 770.3 million by 2035, expanding at a strong CAGR of 12.6% as the industry transitions from research-oriented development to industrial-scale commercialization. A pivotal milestone was achieved in November 2025, when a D18:L8-BO device reached a certified 21.0% PCE in small-area format—placing OPV technology firmly in the high-efficiency category alongside advanced perovskite cells. Scaling improvements were equally notable: a 16.94 cm² OPV module recorded 17.85% efficiency, retaining 87.1% of the original device performance and demonstrating clear progress in tackling the scale-up loss challenge that has historically limited OPV commercialization. Meanwhile, ARMOR Group demonstrated market readiness with its industrial 1 million m²/year R2R capacity, validating OPV as a cost-competitive flexible PV platform for building-integrated and mobility applications. In the indoor PV landscape, Epishine’s commercial OPV modules deliver 22 μW/cm² at 500 lux, making OPV a preferred technology for powering next-generation battery-free IoT sensors. A breakthrough in durability arrived in April 2024, when Heliatek obtained IEC 61215 certification for its OPV film—the first in the world—unlocking bankability for OPV-based BIPV solutions.

- 21% certified small-area efficiency establishes OPV’s competitiveness in next-gen thin-film PV.

- 17.85% scalable module efficiency resolves major scale-up challenges for large-area OPV manufacturing.

- 1 million m²/year industrial capacity validates mass production feasibility for flexible OPV films.

- 22 μW/cm² indoor output positions OPV as a top candidate for battery-free IoT solutions.

- IEC 61215 certification achieved confirms OPV readiness for long-term BIPV deployment.

Breakthrough NFA Materials, Indoor PV Leadership, BIPV Integration, and Ultralight Aerospace-Grade Designs Accelerate the Organic Photovoltaics (OPV) Market

Trend 1: Non-Fullerene Acceptors (NFAs) Emerge as the Universal Standard for Record-Efficiency Organic Photovoltaic Cells

The introduction of Non-Fullerene Acceptors (NFAs) represents the most consequential transformation in OPV research and commercialization history. NFAs overcome the energy loss limitations of traditional fullerene-based acceptors, unlocking unprecedented conversion efficiencies and improved stability.

Key technical milestones include:

- Record certified efficiency of 19.92% (20.52% lab maximum) achieved using advanced quaternary NFA blends such as PM6:D18-Cl:L8-BO:BTP-eC9-propelling OPV into competitive territory with CIGS, CZTS, and other thin-film PV technologies.

- Significant reduction in voltage losses, with NFA–donor material pairings achieving hundreds of millivolts lower VOC loss than C60-based architectures, directly improving device performance.

- Plateauing of older fullerene-based OPV efficiencies at ~11% (solution processed) and ~10% (vacuum processed), underscoring the necessity of the NFA revolution to push the OPV efficiency frontier.

- Enhanced long-term stability, with inverted OPV devices retaining 94.2% of original efficiency after 8,904 hours under ambient, non-encapsulated ISOS-D-1 conditions-demonstrating OPV's potential for commercial durability when coupled with NFA chemistry.

This trend confirms NFAs as the foundational building block for next-generation OPV materials, enabling high-efficiency, stable, and scalable device architectures.

Trend 2: Indoor Energy Harvesting Emerges as OPV’s First High-Volume Commercial Market

The OPV industry is aligning strongly with the Indoor Photovoltaics (IHPV) opportunity, driven by its unique optical properties and exceptional low-light performance. As global IoT deployment accelerates, OPV is emerging as the preferred energy harvester for self-powered IoT sensors, smart home devices, and industrial monitoring systems.

Data-backed performance advantages include:

- Indoor PCE values exceeding 30.6%, with some studies reporting >35% efficiency under 1000 lux LED illumination-far higher than silicon or thin-film alternatives in indoor environments.

- Power output >30 μW/cm² under typical 500 lux office lighting, sufficient to run most wireless IoT sensors with only a few square centimeters of active area.

- Tolerance for thicker active layers (~300 nm) under indoor conditions, enabling high-throughput, cost-efficient manufacturing methods such as roll-to-roll blade coating.

- Bandgap tunability optimized around ~1.9 eV, perfectly aligned with the spectral output of LED and fluorescent indoor lighting.

This trend positions OPV not as a competitor to silicon in utility-scale solar, but as a dominant low-power indoor PV technology, creating a clear early commercialization pathway.

Opportunity 1: Semi-Transparent and Aesthetic OPV Integration into BIPV for Façades, Windows, and Skylights

OPV’s unique visual versatility-color tunability, semi-transparency, patterning-combined with its low embodied carbon footprint creates a compelling opportunity in Building-Integrated Photovoltaics (BIPV). Unlike silicon, OPV can function as both an architectural and energy-generating material.

Key commercial and technical validation points include:

- First commercial façade installation: NEXT Energy Technologies installed 100 square feet of transparent OPV windows (40" × 60") in 2025, proving compatibility with standard architectural glass supply chains.

- Building energy offset of 20–25%, enabling OPV façades to significantly reduce overall building energy consumption while simultaneously reducing HVAC load through IR absorption.

- Energy consumption reduction of 14.80 kW/m² for south-facing façades-demonstrated in simulated comparisons between changeable OPV windows and Low-E glazing.

- Scalable manufacturing, with pilot lines producing large-format transparent OPV glass panels (up to 40" × 60"), supporting mainstream adoption for commercial real estate projects.

This opportunity enables OPV to expand into the rapidly growing BIPV sector, where aesthetics, weight, transparency, and customizability are increasingly prioritized by architects and developers.

Opportunity 2: Ultralight, Flexible OPV Modules for Stratospheric Platforms, Aerospace Robotics, and Near-Space Missions

OPV’s exceptionally low weight, mechanical resilience, and environmental stability unlock high-value aerospace markets-including High-Altitude Platform Stations (HAPS), solar-powered drones, and stratospheric balloons-where every gram counts.

Key differentiators powering this opportunity include:

- Record specific power of 33.8 W/g for 15.8% PCE ultrathin OPV devices-compared to 0.4–0.8 W/g for conventional silicon modules.

- Reliable operation across extreme temperatures from −100°C to +80°C, validating OPV’s viability for high-altitude and atmospheric-edge missions.

- Radiation robustness, with OPVs outperforming leading solar technologies under 10¹² p cm⁻² proton exposure, a critical requirement for aerospace and near-space electronics.

- Minimal device thickness (~3 μm) enabling: 89% performance retention after 4 hours of water immersion and Stability after 300 mechanical stretching cycles at 30% strain under water

These combined properties position OPV as the top emerging technology for ultralight, flexible photovoltaic systems, supporting the next wave of aerospace robotics and atmospheric communications infrastructure.

Organic Photovoltaics Market Share Analysis

Market Share by Product Form: Flexible OPV Films Dominate Through Lightweighting, Roll-to-Roll Scalability, and Superior Conformability

Flexible OPV films hold the leading 50% market share because they embody the core technical and economic advantages that define the Organic Photovoltaics (OPV) market, particularly the ability to deliver ultralight, bendable, and low-cost solar harvesting surfaces. Unlike rigid crystalline silicon, OPV materials can be deposited as printable organic inks, enabling true roll-to-roll manufacturing that drastically lowers production costs and supports gigawatt-scale throughput. This scalable solution-based deposition is a major strategic differentiator, reducing reliance on vacuum tools and high-temperature furnaces, which are costly barriers to entry for manufacturers in traditional PV markets. From a performance standpoint, OPV films’ extreme lightweighting—often under 500 g/m² compared to the 10–15 kg/m² of silicon modules—makes them instantly viable for weight-restricted applications such as membrane roofs, portable structures, tents, greenhouses, and emerging solar mobility concepts. Their sub-200 μm thickness, combined with high conformability, allows OPV to integrate seamlessly onto curved surfaces, textiles, vehicle exteriors, and building facades—applications where rigid PV is fundamentally unsuitable. This versatility aligns directly with market drivers prioritizing design freedom, low installation cost, and integration into surfaces that cannot structurally bear traditional PV systems, cementing flexible films as the primary revenue engine of the OPV industry.

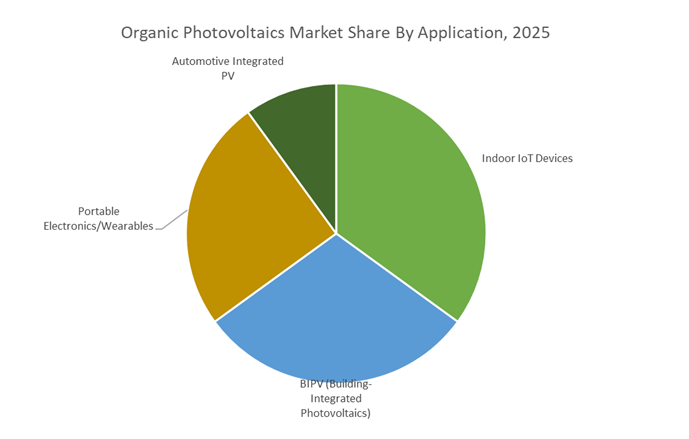

Market Share by Application: Indoor IoT Devices Lead Due to Superior Low-Light Efficiency and Self-Sustaining Power Capabilities

Indoor IoT Devices account for the largest 35% share of the OPV market because OPV technology delivers unmatched energy-harvesting performance under artificial indoor lighting, where conventional silicon drastically underperforms. OPV’s molecular tunability allows the active layer to be chemically engineered to optimally absorb wavelengths between 450–650 nm, aligning with the spectral output of common LED and fluorescent lights. This results in a 2–3× higher relative efficiency under indoor lighting versus silicon, making OPV the superior solution for powering indoor sensors, automation devices, and ambient intelligence systems. Additionally, OPV excels under the low irradiance conditions typical of offices, warehouses, homes, and retail environments—often 200–1000 lux—maintaining strong open-circuit voltage and consistent energy generation. This performance advantage directly supports the rapid expansion of self-powered IoT ecosystems, where eliminating battery replacement is critical to reducing operational expenditure. In large-scale deployments such as smart buildings, logistics monitoring, asset tracking, and industrial automation, battery maintenance often represents the highest cost contributor; OPV solves this by enabling fully autonomous, maintenance-free sensors with power-harvesting surfaces integrated directly into the device housing. As global IoT installations grow exponentially and enterprises shift toward resilient, low-maintenance infrastructure, OPV’s unparalleled indoor energy-harvesting capability positions the segment as the dominant demand driver across the entire OPV value chain.

Country Analysis: Global Organic Photovoltaics (OPV) Commercialization Hubs

Germany – Industrial OPV Scale-Up, Certified Efficiency Records, and Roll-to-Roll Manufacturing Leadership

Germany remains the leading European powerhouse in Organic Photovoltaics commercialization, driving global advances in OPV module efficiency, material innovations, and industrial-scale Roll-to-Roll (R2R) manufacturing. The ecosystem is anchored by a strong combination of academic excellence, specialized chemical suppliers, and advanced machinery manufacturers. In December 2023, the Helmholtz Institute Erlangen-Nuremberg (HI ERN), in collaboration with key partners, achieved a certified world-record OPV module efficiency of 14.46%, validated by Fraunhofer ISE—cementing Germany’s status as the global benchmark for OPV device performance. The team improved the geometrical fill factor (GFF) to 95% by optimizing laser patterning techniques, reducing dead zones and improving current extraction efficiency—critical for large-area commercial modules.

Germany’s leadership extends beyond efficiency records. The region has a rich history of large-area OPV deployments, exemplified by BELECTRIC OPV’s fabrication of 250 m² of aesthetic OPV modules used in the "solar trees" installation at the 2015 Milan Expo. These projects established Europe as an early adopter of aesthetically integrated, lightweight solar solutions suitable for BIPV, architectural installations, and public infrastructure. On the materials front, German chemical conglomerates such as Merck Chemicals continue to develop next-generation donor polymers—including the Lisicon series—engineered for improved stability and high-speed R2R processing. Manufacturing equipment providers like Coatema Coating Machinery support industrial OPV growth with advanced R2R platforms capable of handling web widths up to 1,000 mm, directly enabling mass production of flexible OPV modules.

United States – Transparent OPV BIPV Commercialization and Strong Federal Funding Mechanisms

The United States has positioned itself as a critical hub for transparent OPV technologies, targeting premium-value Building-Integrated Photovoltaics (BIPV) applications where aesthetics, visibility, and design flexibility are essential. In July 2025, NEXT Energy Technologies installed the world’s first commercial-scale transparent OPV façade at its headquarters in Santa Barbara—a milestone proving that OPV window coatings can be integrated into standard commercial glazing systems. Each OPV window measured 40×60 inches, delivering 32% visible light transmission and a commercial-grade 3.5% power efficiency, demonstrating the viability of OPV for real estate developers seeking energy-generating curtain walls without disrupting building aesthetics.

Federal funding plays a foundational role in accelerating U.S. OPV innovation. The Department of Energy’s Solar Energy Technologies Office (SETO) committed $44 million in 2024 through its Advancing U.S. Thin-Film Photovoltaics program, supporting domestic OPV manufacturing and supply chain resilience. This aligns with national goals to strengthen U.S. leadership in emerging solar technologies while reducing foreign dependence. The integration of NEXT’s transparent OPV into traditional window supply chains—leveraging standard low-e coated inboard lites and framing systems from industry leaders like Viracon and Walters & Wolf—demonstrates how the U.S. is driving seamless commercial adoption, reducing retrofit complexity and enabling scalable deployment in office buildings, retail spaces, and high-performance architectural projects.

China – Non-Fullerene Acceptor (NFA) Material Breakthroughs and High-Throughput Printing Ecosystem

China is rapidly becoming a global innovation center for OPV materials science, particularly in the synthesis of advanced non-fullerene acceptors (NFAs) critical for pushing OPV efficiency beyond 18% in laboratory settings. Chinese academic institutions and material suppliers are driving breakthroughs in donor–acceptor pair engineering, enhancing charge mobility, stability, and absorption across broader wavelengths. These innovations are pivotal in addressing OPV’s historical weaknesses related to environmental stability and enabling higher-efficiency tandem structures.

China’s advantage is amplified by its enormous manufacturing base and government-backed investment in next-generation solar technologies. Major PV companies are establishing dedicated flexible-printable solar lines, leveraging OPV’s compatibility with low-temperature, solution-based processes ideal for high-throughput production. This creates a clear commercial pathway for wearables, IoT devices, packaging-integrated photovoltaics, and lightweight portable chargers. As China scales R2R-compatible OPV infrastructure, it is positioning itself as the future leader of low-cost, high-volume organic solar module production, complementing its dominance in silicon and thin-film manufacturing.

Italy – Roll-to-Roll (R2R) Pilot Manufacturing and Cost-Optimized OPV Module Production

Italy plays an emerging but strategically important role in validating industrial-scale Roll-to-Roll production for OPV modules. The country’s innovation, led by Ribes Tech—a spinoff of the Italian Institute of Technology—has produced fully operational R2R pilot lines capable of manufacturing OPV modules optimized for indoor energy harvesting, smart sensors, asset trackers, and low-power IoT devices. This focus aligns with OPV’s core advantages: low weight, flexibility, and strong indoor PCE performance.

Economic modeling from Italian research groups indicates that R2R-produced semitransparent OPV modules could reach future production costs of $0.47/Wp, including inverter costs—positioning OPV as a highly competitive BIPV technology for façades, skylights, and indoor energy applications. Italy’s strong engineering and materials science infrastructure enables it to bridge the gap between lab-scale feasibility and commercial scalability, making the country a critical contributor to the global OPV supply chain and a potential hub for low-cost, high-design-value solar manufacturing.

Competitive Landscape: Leading OPV Innovators Driving Indoor PV, Flexible Modules & BIPV Adoption

The OPV competitive environment is defined by technological specialization: flexible BIPV leaders, R2R production pioneers, indoor-optimized module developers, and advanced material innovators. Together, these companies are actively shaping the global OPV value chain.

Heliatek dominates the BIPV segment through its lightweight HeliaSol and HeliaFilm products, weighing under 2 kg/m² and suitable for curved, load-sensitive façades. Its long-term strategy centers on scaling a >2 million m²/year factory by 2026 using proprietary vacuum thermal evaporation technology. The company’s major credibility boost came in April 2024, when its OPV film became the first globally to achieve IEC 61215 certification, enabling utility-grade durability. Heliatek continues to expand commercial deployments across Europe, including projects with Siemens Energy and municipal buildings in Germany.

ARMOR Group’s ASCA® OPV operates at an industrial scale of 1 million m²/year, representing one of the largest roll-to-roll OPV capacities worldwide. Its films are known for high flexibility, semi-transparency, and custom geometric formats suitable for mobility, building membranes, and off-grid systems. Following strategic restructuring in late 2025, ASCA sharpened its focus on providing semi-finished OPV coils to OEMs, supporting integration into automotive surfaces, urban infrastructure, and temporary structures.

Epishine builds its competitive edge on extremely high indoor energy harvesting efficiency, achieving 22 μW/cm² at 500 lux, outperforming typical amorphous silicon competitors. Its modules are miniaturized with low Z-axis thickness for seamless integration into IoT sensors, ESL tags, and compact consumer electronics. Epishine's form-factor innovation is heavily aligned with emerging global demand for maintenance-free wireless devices in smart buildings and retail automation.

Dracula Technologies utilizes a patented digital printing process to create aesthetic, custom-shaped OPV modules with silver bus bars as thin as 1 mm. Its LAYER® OPV platform recorded a 15% efficiency boost in June 2025, enabling higher power density for smart home products and industrial IoT sensors. Dracula targets design-centric markets including smart retail, consumer electronics, and indoor automation where visual integration is key.

Brilliant Matters focuses on materials innovation, supplying high-performance active layer inks including BM10, which delivers >10% stabilized efficiency in fully printed modules under 1-sun. Its inks are optimized for industrial slot-die and inkjet printing, providing tight molecular weight control (±5 kDa) to ensure consistent yields across full R2R production lines. The company plays a vital role in bridging laboratory OPV performance with scalable manufacturing.

BELECTRIC OPV specializes in customizable OPV modules designed for integration into textiles, automotive surfaces, temporary structures, and outdoor consumer products. Its expertise spans colored OPV, transparent modules, and flexible form factors, positioning it as a key supplier for aesthetic and design-driven PV applications. The company targets markets requiring visually integrated solar generation, ranging from promotional products to architectural shading systems.

Organic Photovoltaics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$235.1 Million

|

|

Market Size (2035)

|

$770.3 Million

|

|

Market Growth Rate

|

12.6%

|

|

Segments

|

By Device Structure (Single-Junction OPV, Tandem/Multi-Junction OPV, Inverted OPV, Non-Fullerene Acceptor OPV), By Material Composition (Polymer-Fullerene Blends, Polymer-Non-Fullerene Acceptor Systems, Small-Molecule Organic Solar Cells), By Product Form (Flexible OPV Film, Rigid OPV, Transparent/Semi-Transparent OPV, Colored/Customized OPV), By Manufacturing Process (Solution Processing, Roll-to-Roll Printing, Vacuum Deposition), By Application (BIPV, Portable Electronics & Wearables, Indoor IoT Devices, Automotive-Integrated PV)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BELECTRIC OPV GmbH, NEXT Energy Technologies Inc., Heliatek GmbH, Ribes Tech, Merck KGaA, Heraeus Group, Sumitomo Chemical Co. Ltd., Konica Minolta Inc., Dyesol (Greatcell Solar Ltd.), Solvay S.A., Coatema Coating Machinery GmbH, Toshiba Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Photovoltaics (OPV) Market Segmentation

By Device Structure

- Single-Junction OPV

- Tandem/Multi-Junction OPV

- Inverted OPV

- Non-Fullerene Acceptor (NFA) OPV

By Material Composition

- Polymer-Fullerene Blends

- Polymer-Non-Fullerene Acceptor (PNFA)

- Small-Molecule Organic Solar Cells (SM-OSC)

By Product Form

- Flexible OPV Film

- Rigid OPV (Glass)

- Transparent/Semi-Transparent OPV

- Colored/Customized OPV

By Manufacturing Process

- Solution Processing

- Roll-to-Roll (R2R) Printing

- Vacuum Deposition (PVD)

By Application

- BIPV (Building-Integrated Photovoltaics)

- Portable Electronics/Wearables

- Indoor IoT Devices

- Automotive Integrated PV

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key OPV Market Players

- BELECTRIC OPV GmbH

- NEXT Energy Technologies, Inc.

- Heliatek GmbH

- Ribes Tech

- Merck KGaA

- Heraeus Group

- Sumitomo Chemical Co., Ltd.

- Konica Minolta Inc.

- Dyesol (Greatcell Solar Ltd.)

- Solvay S.A.

- Coatema Coating Machinery GmbH

- TOSHIBA CORPORATION

*- List not Exhaustive