Metallic Films Market Overview: Size, CAGR, and Strategic Insights

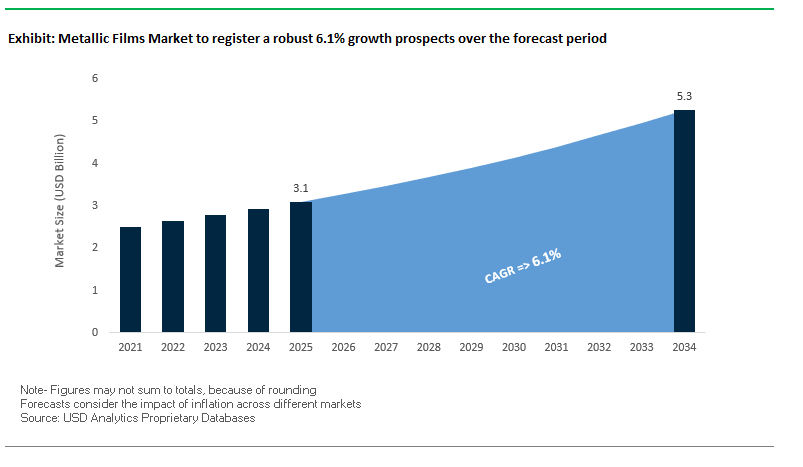

The global Metallic Films Market is projected to grow from $3.1 billion in 2025 to $5.3 billion by 2034, reflecting a robust CAGR of 6.1%. This growth is underpinned by increasing applications in electronics, packaging, renewable energy, and optoelectronics, where metallic films serve as critical components for performance, durability, and aesthetic enhancement. Industry professionals are particularly focused on the adoption of ultra-thin flexible films, high-barrier metallized packaging, and sustainable materials that support a circular economy.

Key Insights for Industry Stakeholders

- Electronics and semiconductor integration: Metallic films are essential for interconnects, gates, and barrier layers in ICs and transistors, driving miniaturization and performance.

- Superior packaging barriers: Metallized films protect food, pharmaceuticals, and sensitive products from moisture, oxygen, and light, extending shelf life and enhancing brand value.

- Innovation in flexible, lightweight films: Advances in ultra-thin, pliable films enable wearable electronics, flexible displays, and next-generation devices.

- Renewable energy applications: Metallic films contribute to thin-film solar panels and smart windows, supporting energy efficiency initiatives.

- Sustainability and recyclability: Growing demand for recyclable and environmentally-friendly metallic films aligns with global sustainability trends.

Recent Developments Shaping the Global Metallic Films Industry

The metallic films market has witnessed significant developments driven by technological innovation, capacity expansion, and regional market growth. In August 2025, studies highlighted the dominance of the Asian market, fueled by strong manufacturing infrastructure and rapid growth in food, beverage, and pharmaceutical industries. The same month, a Nano Letters study introduced a novel inhibitor-modified ALD strategy for ultrathin iridium and platinum films, critical for emerging electronic devices. Additionally, liquid-metal printing techniques enabling flexible indium tin oxide (ITO) films for touchscreens were reported, offering superior transparency and pliability.

July 2025 saw established converters investing in wider, faster coating lines to achieve scale and counter cost inflation, while innovators focused on recycling-ready film structures. Lightweight metallized films are increasingly substituting traditional aluminum foils due to cost-effectiveness and durability. A major manufacturer announced flexible packaging expansion, underscoring strategic capacity growth. By June 2025, copper usage in metallic films surged, driven by high-power battery packs and 5G device requirements. May 2025 reinforced the trend towards sustainable, protective packaging that enhances shelf life, further cementing the market’s growth trajectory.

Transformative Trends and Emerging Opportunities in the Metallic Films Market

Adoption of Transparent High-Barrier Metal Oxide Coatings for Flexible Packaging

The metallic films market is rapidly evolving with the adoption of transparent high-barrier coatings such as aluminum oxide (AlOx) and silicon oxide (SiOx), addressing the dual demand for superior product protection and consumer visibility. These coatings outperform traditional metallized films by delivering ultra-low oxygen transmission rates (OTR <0.5 cc/m²/day) and water vapor transmission rates (WVTR), ensuring extended shelf life for sensitive products like pharmaceuticals and premium foods.

Beyond performance, transparency is driving brand value and safety. Unlike opaque metallized films, transparent AlOx and SiOx films allow end-of-line metal detection, enhancing quality control by enabling the detection of potential contaminants in packaged foods. This feature is becoming a decisive factor for manufacturers focused on safety assurance and regulatory compliance. Moreover, their microwave compatibility expands application versatility across ready-to-eat meals and convenience packaging.

From a sustainability perspective, these coatings require 50% less aluminum than standard metallized OPP, significantly lowering raw material usage and reducing the carbon footprint. Producers such as Jindal Films are promoting solutions like Alox-Lyte™, which combine high-barrier performance, product visibility, and material efficiency, making transparent metallic films a key innovation in next-generation flexible packaging.

Strategic Shift to Sustainable and Recyclable Mono-Material Structures

The market is undergoing a systematic redesign for recyclability, with metallic films increasingly engineered as polyolefin-based mono-material structures. This transition addresses regulatory mandates and brand-owner commitments to reduce multi-material laminates that hinder recycling.

Industry guidelines, supported by research published on ResearchGate, emphasize that polypropylene (PP) and polyethylene (PE), when combined with recyclable barrier layers such as AlOx or SiOx, can replace complex laminates without sacrificing functionality. Projects like HolyGrail 2.0, led by AIM and over 85 brand partners, are validating digital watermarking as a scalable sorting solution for mono-material packaging, ensuring industrial-level recycling accuracy and high-quality material recovery.

Additionally, mono-materials bring operational benefits. Additives from companies like Milliken are enabling 5–8% energy savings in polypropylene processing, reducing both costs and emissions. With regulators tightening Design for Recycling Guidelines and brands pledging higher recycled content, the shift toward recyclable mono-material metallic films is both a compliance-driven necessity and a competitive advantage for manufacturers.

Development of Thin-Film Barriers for Flexible Organic Photovoltaics (OPV)

A fast-emerging niche for metallic films lies in flexible organic photovoltaics (OPV), which require extreme barrier protection to shield sensitive organic layers from oxygen and moisture degradation. Unlike conventional packaging applications, OPV films must maintain ultra-low permeability while also integrating functional roles such as charge transport.

Studies published in MDPI and ResearchGate highlight how metal oxide thin films can simultaneously serve as encapsulation layers and electron/hole transport layers in OPVs. This dual-functionality is essential for enhancing stability and extending the lifespan of flexible solar cells. Given the rising demand for lightweight, portable, and bendable solar solutions, specialized metallic films designed for OPV applications present a high-value growth avenue for manufacturers willing to invest in R&D for renewable energy sectors.

Integration of Anti-Counterfeiting and Smart Features via Advanced Metallization

The global rise in counterfeiting across pharmaceuticals, cosmetics, and consumer electronics is driving the adoption of anti-counterfeiting metallic films embedded with both overt and covert security features. Using advanced metallization techniques, films can incorporate holograms, microtext, and digitally-readable patterns that are nearly impossible to replicate.

Overt features such as holographic films enhance both aesthetics and security, offering brand owners a dual benefit of premium shelf appeal and consumer trust. Meanwhile, covert features—such as microscale images and unique digital patterns detectable only by machine vision—add an additional layer of authentication against sophisticated counterfeit attempts. Reports from leading security firms highlight that integrated NFC/QR-enabled metallized films also boost consumer engagement by linking packaging directly to digital verification platforms.

As regulatory frameworks tighten around product authentication and brands seek to safeguard supply chains, metallic films with built-in security and smart packaging features are emerging as a critical tool for brand protection and differentiation in high-value markets.

Competitive Landscape: Key Players Driving Innovation in Metallic Films

The global metallic films industry is dominated by leading material innovators and packaging specialists who focus on high-performance films, sustainability, and technological advancements. Companies are strategically investing in new materials, recycling-ready solutions, and capacity expansion to meet rising demand.

DuPont Teijin Films: Pioneering High-Barrier Polyester Films

DuPont Teijin Films is a leading producer of polyester films, offering metallized films for food packaging, insulation, and electronics. Its flagship Mylar products provide superior barrier properties and high-gloss finishes for decorative and functional applications. The company focuses on high-performance functional films and is actively investing in sustainable and recyclable packaging innovations, maintaining a strong competitive position through continuous R&D and product diversification.

Celanese Corporation: Polymer Expertise Driving High-Barrier Applications

Celanese Corporation provides polymer materials often used as substrates for metallized films in flexible electronics, food, and medical packaging. The company’s strength lies in its polymer chemistry expertise, enabling high-performance materials that offer exceptional moisture and oxygen barriers. Strategic investments in sustainable technologies and circular economy practices position Celanese as a key supplier for high-quality metallized films in critical industrial and consumer applications.

Amcor plc: Global Expansion in Sustainable Metallized Packaging

Amcor is a leader in flexible and rigid packaging, producing metallized films for food, beverage, and medical applications. The company is investing in new coating facilities to enhance high-barrier film production. Amcor’s strategy emphasizes sustainability and lightweighting, aiming for 100% recyclable or reusable packaging by 2025. Its integrated services—from design support to logistics—enable customers to streamline product launches and meet sustainability goals efficiently.

Uflex Ltd.: Innovative Flexible Packaging Solutions

Uflex Ltd. is a major Indian multinational providing metallized films for food, pharmaceutical, and industrial applications. The company emphasizes sustainable product development, launching recyclable and compostable films. Strategic investments in new manufacturing facilities support global expansion and rising demand, particularly in the medical and pharmaceutical packaging sector, strengthening Uflex’s position as a sustainability-driven leader.

Jindal Films: Specialty Films and Recycling-Ready Innovations

Jindal Films manufactures polypropylene (PP) and polyethylene (PE) metallized films used in food, beverage, and medical packaging. In May 2025, the company invested Rs 700 crore to expand its Nashik plant, adding advanced BOPP film lines. Jindal’s EthyLyte™ films are designed for “ready-to-recycle” applications, reflecting a strong focus on sustainability, innovation, and high-barrier performance. The company’s expertise in polymer-based metallic films positions it as a key player in the global market.

Metallic Films Market Share Insights

Polypropylene Leads Market Share by Film Material in the Metallic Films Industry

Polypropylene (PP) dominates the metallic films industry with a projected 35% share in 2025, primarily due to the widespread adoption of biaxially oriented polypropylene (BOPP) films in high-volume packaging. Their exceptional clarity, moisture resistance, and stiffness at a competitive cost make them indispensable for flexible packaging in snacks, confectionery, and labeling, where shelf appeal through high-gloss finishes drives consumer engagement. PET films follow closely with a 30% share, offering superior tensile strength, thermal stability, and gas barrier properties, which make them the material of choice for retort pouches, coffee packaging, and technical laminates where durability and shelf-life extension are paramount. Polyethylene contributes 20% of market share, largely through co-extruded and laminated applications, where metallized PE provides critical sealability and moisture protection for bag-in-box liners and bakery wraps. Niche segments such as polyimide (8%) command a high-value role in electronics and aerospace due to unmatched thermal resistance and dielectric strength, while other materials like nylon and PLA together account for 7%, showcasing innovations in puncture resistance and biodegradable metallized packaging. The dominance of PP and PET highlights how cost-to-performance balance and recyclability pathways define competitive positioning in metallic films packaging.

Food & Beverage Drives Market Share by End-User in the Metallic Films Industry

Food and beverage packaging secures the largest share at 55% of the metallic films industry, fueled by the dual advantage of superior barrier protection and premium shelf aesthetics. Metallized PP and PET films extend the shelf life of moisture- and oxygen-sensitive products such as chips, coffee, frozen foods, and dairy, while delivering the reflective, high-impact appearance that boosts retail visibility and consumer perception of quality. Consumer electronics, representing 18%, leverage metallized films for EMI/RFI shielding, static protection, and decorative applications in device housings and cables, with PET and polyimide as the leading materials. Pharmaceuticals and healthcare follow with 15% share, where blister lidding and sterile pouches require near-hermetic seals and regulatory-compliant performance to protect sensitive formulations. Automotive and aerospace account for 7% of demand, deploying metallized films for heat reflection, wiring harness insulation, and aerospace thermal blankets, where reliability under extreme conditions is mission-critical. Building and construction, at 5%, applies metallized films in radiant barrier laminates for energy-efficient insulation solutions. Overall, the food and beverage sector anchors volume growth, while electronics and healthcare secure high-value demand in technical applications.

United States: Technological Breakthroughs and Expanding Corporate Investments Reshape the Metallic Films Market

The United States metallic films market is evolving rapidly, with technological innovations driving adoption across electronics, aerospace, defense, and packaging. U.S. manufacturers are leading research into advanced metallic films with enhanced flexibility, conductivity, and barrier protection, positioning the country at the forefront of high-performance material science. One of the most significant developments has been in metallized polyester films for food packaging, which combine transparency with superior oxygen barrier properties, directly extending shelf life and reducing waste in the food and beverage sector. This innovation highlights how sustainability and functionality are intersecting in the U.S. packaging market.

Corporate investments further strengthen the U.S. position in the global metallic films industry. Early in 2025, a U.S.-based company announced the launch of a next-generation metallic film line targeting food packaging applications, underscoring the sector’s strong growth potential. Beyond packaging, aerospace and defense applications—where metallic films are used for electromagnetic shielding and insulation—are creating new opportunities. Together, these factors demonstrate how U.S. technological leadership and corporate investment strategies are setting global benchmarks in the metallic films market.

Germany: Regulatory-Driven Innovation and Sustainability Leadership in Metallic Films

Germany stands out in the metallic films market due to its alignment with the European Union’s Packaging and Packaging Waste Regulation (PPWR), implemented in January 2025. These stringent rules are pushing manufacturers to prioritize recyclability, high-value materials, and compatibility with circular economy principles. As a result, German companies are innovating rapidly, integrating recycled content into metallic film manufacturing and advancing film-coating technologies that reduce environmental impact while enhancing performance. The adoption of novel techniques such as “can contouring” also illustrates Germany’s commitment to consumer-driven design innovation, enhancing both ergonomics and brand identity.

Corporate investments play a critical role in Germany’s metallic films industry, especially in high-value applications such as semiconductors. Air Liquide’s €250 million investment in new gas production units to support chip manufacturing directly links to the need for ultra-pure metallic films in microelectronics. This intersection of regulatory frameworks, corporate funding, and sustainability-focused infrastructure places Germany at the forefront of Europe’s metallic films market, ensuring it remains a hub of innovation and circular economy leadership.

China: Governmental Support and Automation Fuel Metallic Films Growth

China’s metallic films market is accelerating due to strong governmental backing for high-end manufacturing, particularly in alignment with the nation’s dual-carbon sustainability targets. Policies aimed at fast-tracking technology standards and simplifying approvals are enabling local manufacturers to scale production efficiently. This top-down support is fostering a market environment where metallic films are increasingly integrated into electronics, packaging, and industrial applications, all while meeting sustainability benchmarks.

On the corporate side, both domestic and multinational companies are expanding aggressively. Chinese manufacturers are investing heavily in automation and AI to enhance quality control, improve efficiency, and increase capacity for high-quality circular products. At the same time, global FMCG giants are localizing metallic film production in China to reduce supply chain risks and respond to rising consumer demand. These combined trends ensure that China will remain one of the fastest-growing and most influential players in the global metallic films market.

India: Government Programs and Domestic Champions Boost Metallic Films Manufacturing

India is emerging as a promising growth hub for the metallic films market, fueled by government-backed initiatives such as Make in India and the Production Linked Incentive (PLI) scheme. These programs are actively encouraging domestic manufacturing and investment in advanced materials, while simultaneously promoting a circular economy that aligns with global sustainability targets. This policy landscape is driving significant expansion in the country’s metallic film production capabilities.

Technological adoption is also on the rise in India, with metallic films gaining traction in flexible packaging, consumer electronics, and e-commerce-driven logistics. Leading domestic players such as Cosmo Films Ltd, Jindal Poly Films Ltd, and Uflex Ltd are heavily investing in R&D to create innovative metallic films with enhanced barrier protection and aesthetic appeal. Demand is particularly strong in food and beverage packaging, where extended shelf life is crucial, and in pharmaceutical and personal care industries, which rely on metallic films for safety and quality preservation. With rising consumption patterns and government support, India is on a trajectory to become a major metallic films hub in Asia-Pacific.

Japan: Precision Manufacturing and Specialty Metallic Films Drive Market Growth

Japan’s metallic films market is characterized by advanced technologies and high-value specialty products. Companies like Toray Industries, Inc. are globally recognized for their leadership in polyester and polypropylene metallic films, producing materials that meet the strict safety and performance standards demanded by Japan’s precision manufacturing industries. The sector is increasingly focused on high-performance films with unique properties, such as improved optical clarity for displays and enhanced durability for automotive applications.

Regulation also plays a decisive role in Japan’s market dynamics. The Pharmaceuticals and Medical Devices Agency (PMDA) enforces stringent packaging standards, and recent amendments to the Pharmaceuticals and Medical Devices Act aim to improve drug supply chain stability. This is expected to increase demand for high-quality metallic films in pharmaceutical packaging. Additionally, the market is witnessing strong momentum in cosmetics and specialty consumer goods, where thin, value-added films with premium finishes are gaining traction. Japan’s combination of regulatory rigor, precision technology, and focus on high-performance applications ensures its metallic films market remains a global benchmark for quality and innovation.

Metallic Films Market Report Scope

Metallic Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$5.3 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Metal Type (Aluminum, Copper, Others), By Film Material (PP, PET, PE, Polyimide, Other Materials), By Application (Packaging, Electrical & Electronics, Decorative, Insulation, Other Applications), By End-User (Food & Beverage, Pharmaceuticals & Healthcare, Consumer Electronics, Automotive & Aerospace, Building & Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries, Inc., Cosmo Films Ltd., Jindal Poly Films Ltd., Uflex Ltd., Taghleef Industries Group, Polinas Plastik Sanayi ve Ticaret A.Ş., Dunmore Corporation, Ester Industries Ltd., SRF Limited, Avery Dennison Corporation, Celplast Metallized Products Limited, Mitsubishi Polyester Film GmbH, DuPont de Nemours, Inc., Ultimet Films Limited, Polyplex Corporation Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metallic Films Market Segmentation

By Metal Type

By Film Material

- PP

- PET

- PE

- Polyimide

- Other Materials

By Application

- Packaging

- Electrical & Electronics

- Decorative

- Insulation

- Other Applications

By End-User

- Food & Beverage

- Pharmaceuticals & Healthcare

- Consumer Electronics

- Automotive & Aerospace

- Building & Construction

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Metallic Films Market

- Toray Industries, Inc.

- Cosmo Films Ltd.

- Jindal Poly Films Ltd.

- Uflex Ltd.

- Taghleef Industries Group

- Polinas Plastik Sanayi ve Ticaret A.Ş.

- Dunmore Corporation

- Ester Industries Ltd.

- SRF Limited

- Avery Dennison Corporation

- Celplast Metallized Products Limited

- Mitsubishi Polyester Film GmbH

- DuPont de Nemours, Inc.

- Ultimet Films Limited

- Polyplex Corporation Ltd.

* List Not Exhaustive

Methodology

USDAnalytics leverages a rigorous, multi-dimensional research methodology to deliver precise and actionable insights into the global Metallic Films Market. Our approach integrates primary research, including consultations with industry leaders, manufacturers, and technical experts, with secondary research sourced from corporate filings, regulatory reports, scholarly publications, and verified industry databases. Market drivers such as ultra-thin flexible films, high-barrier metallized packaging, sustainable mono-material structures, and renewable energy applications are analyzed alongside regional market dynamics, including technological adoption, regulatory frameworks, and government initiatives in the U.S., Europe, China, India, and Japan. USDAnalytics applies advanced modeling techniques to forecast market size, growth rates, material- and application-specific trends, and end-user adoption patterns. Corporate developments, including capacity expansions, mergers and acquisitions, and R&D investments, are monitored to assess competitive positioning, while sustainability and circular economy practices, such as recyclable films and digital watermarking initiatives, are evaluated for their impact on product innovation and regulatory compliance. This comprehensive methodology ensures industry professionals receive high-value, data-driven intelligence to make informed strategic decisions in the metallic films ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.