Market Overview: Functional Films Driving Electronics, Packaging, and Sustainability

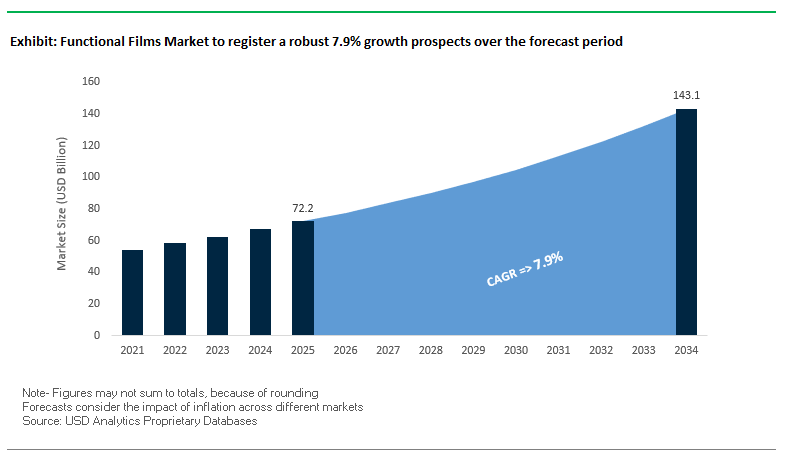

The Global Functional Films Market is projected to grow from USD 72.2 billion in 2025 to USD 143.1 billion by 2034, advancing at a strong CAGR of 7.9%. These high-performance films go beyond basic protection and structural use, offering specialized properties such as optical enhancement, conductivity, heat resistance, and barrier protection. They are widely adopted across consumer electronics, automotive, packaging, renewable energy, and healthcare, making them one of the most versatile material categories in advanced manufacturing.

A major growth driver is the miniaturization and lightweight design trend in electronics, where functional films such as conductive, optical, and protective films enable foldable smartphones, tablets, and wearable devices. The sector is also accelerating toward sustainability, with strong momentum in developing biodegradable and recyclable packaging films, particularly for the food and beverage sector.

Another critical driver is the rising demand for high-performance optical films, supporting the proliferation of 4K/8K televisions, high-resolution laptops, and OLED/AMOLED smartphones. In addition, the renewable energy sector is a strong growth area, as anti-reflective and light-diffusing films improve photovoltaic panel efficiency, supporting global clean energy targets.

Key Insights for Industry Professionals:

- Market Size: USD 72.2B (2025) → USD 143.1B (2034).

- CAGR: 7.9% fueled by electronics, packaging, and solar adoption.

- Electronics: Conductive and optical films crucial for foldable devices.

- Packaging: Bio-based and recyclable films addressing sustainability.

- Energy: Anti-reflective coatings boosting solar panel efficiency.

Market Analysis: Recent Developments in Functional Films Industry

The Global Functional Films Industry has seen a wave of technology launches, sustainability projects, and global expansions in recent years.

In September 2025, LyondellBasell partnered with Futamura Chemical and Iwatani Corporation to develop a bio-based cosmetic film solution, highlighting cross-industry applications. That same month, Ester Industries showcased its advances in functional and eco-friendly polyester films at the 12th Specialty Films & Flexible Packaging Global Business Summit in Mumbai.

Also in August 2025, Dai Nippon Printing (DNP) announced two strategic exhibitions Drinktec 2025 for aseptic packaging innovations and Medical Fair Thailand for sustainable medical packaging solutions. In July 2025, DNP revealed plans to open its first overseas R&D center in the Netherlands, dedicated to Co-Packaged Optics R&D, targeting the data center industry.

Sustainability remains a central theme. Reports in July 2025 emphasized rising demand for bio-based lubricants and eco-friendly materials, while March 2025 reports highlighted the adoption of functional lid stock for pharmaceutical single-dose packaging. Meanwhile, rising raw material cost volatility in 2024 prompted companies to optimize procurement strategies, indirectly affecting film manufacturers’ margins.

Emerging Trends and Strategic Opportunities in the Functional Films Market

Accelerated Adoption of Ultra-High Barrier Films for Flexible Electronics

One of the most transformative trends is the adoption of ultra-high barrier functional films for next-generation flexible electronics, including foldable smartphones, OLED displays, and wearables. Flexible OLEDs are extremely sensitive to oxygen and moisture, requiring water vapor transmission rates (WVTR) as low as 10⁻⁶ g·m⁻²·day⁻¹—a performance level far beyond that of food or medical packaging films.

To address this, researchers are advancing thin-film encapsulation (TFE) technologies that combine alternating organic and inorganic layers to achieve the required barrier levels while maintaining flexibility. These innovations enable devices to withstand repeated mechanical stress while preserving long lifespans. For film manufacturers, this trend represents a premium growth avenue, as flexible electronics adoption accelerates globally and brands like Samsung, LG, and BOE scale foldable product lines. This development is also reshaping the value chain, driving closer collaborations between material suppliers and electronics OEMs to ensure barrier films integrate seamlessly with precision device manufacturing.

Integration of Anti-Microbial and Anti-Viral Surface Functionality

Post-pandemic, demand has surged for functional films with permanent antimicrobial and antiviral properties, particularly in high-touch applications across healthcare, public transportation, and consumer electronics. Unlike traditional coatings that leach over time, new solutions utilize surface-active technologies such as silver nanoparticles, zinc pyrithione, and photocatalytic coatings to provide long-term protection.

Companies like 3M and polyurethane film manufacturers have launched antimicrobial films that withstand frequent cleaning, while academic research continues to refine nanoparticle properties to maximize efficiency. The ability to reduce microbial spread without chemical migration offers a powerful value proposition for regulated industries such as healthcare and food processing. By offering permanently active surfaces, film manufacturers can differentiate their portfolios and expand into sectors where hygiene and safety are paramount, cementing this as a durable trend within the global functional films market.

Development of Functional Films for Perovskite Solar Cells

The rise of perovskite solar cells (PSCs) presents one of the largest untapped opportunities for functional film suppliers. PSCs are highly efficient but unstable when exposed to oxygen and moisture, creating an urgent need for ultra-high barrier encapsulation films. Alongside encapsulants, there is parallel demand for transparent conductive electrodes (TCEs) and light-management films to improve stability and efficiency.

Recent studies highlight the promise of PEDOT:PSS films, carbon nanomaterials, and metal nanowires as alternatives to traditional ITO electrodes for flexible solar devices. For manufacturers, this represents a multi-film stack opportunity spanning barrier protection, conductivity, and optical enhancement. As PSC commercialization progresses, collaboration between film producers, material science innovators, and renewable energy firms will be crucial. With PSCs seen as a low-cost alternative to silicon photovoltaics, functional film suppliers that can deliver high-performance encapsulants and TCEs are positioned to capture a rapidly expanding market segment.

Smart Films with Dynamic Optical Properties for Automotive & Building Glazing

A second high-value opportunity lies in the expansion of smart functional films with dynamic optical properties, including suspended particle device (SPD) and electrochromic films. These films enable glass surfaces to switch from transparent to opaque on demand, offering applications in automotive sunroofs, aerospace windows, architectural glazing, and privacy partitions.

SPD films can switch states in less than one second, blocking up to 99.9% of UV rays and over 50% of infrared radiation, reducing glare and improving energy efficiency. Companies like Research Frontiers and Smart Film are already commercializing retrofit and OEM solutions. Automotive brands are increasingly offering SPD-enabled sunroofs as premium features, while architects integrate electrochromic glazing for sustainable building designs.

The market impact extends across industries, creating a new collaborative value chain between film manufacturers, construction firms, and mobility OEMs. As energy efficiency, user comfort, and personalized control gain importance, dynamic smart films represent a significant growth frontier, transforming functional films into core enablers of next-generation infrastructure and mobility solutions.

Competitive Landscape: Leading Companies in Functional Films Market

The Functional Films Market is highly competitive, with global players leveraging material innovation, R&D investment, and circular economy strategies to lead across electronics, automotive, packaging, and renewable energy.

3M Company drives innovation with advanced optical and protective films

3M is a pioneer in functional films, offering optical, reflective, and protective films for consumer electronics, automotive, and industrial applications. It has developed polyimide films for flexible electronics, offering superior thermal stability and durability. The company’s strategy centers on R&D investment and product innovation, positioning it as a key supplier for next-generation devices.

Covestro AG develops bio-based polycarbonate films for sustainability

Covestro specializes in polycarbonate films with applications in displays, touch panels, and automotive interiors. Its recent bio-based film series, derived from renewable feedstocks, supports circular plastics development. Covestro’s films combine optical clarity, impact resistance, and weatherability, making them essential for high-end displays and mobility solutions. Its strategy is strongly aligned with creating a circular economy for plastics.

Dai Nippon Printing Co., Ltd. (DNP) expands global R&D for functional films

DNP leverages its expertise in printing and materials science to deliver transparent barrier films, touch sensors, and high-performance packaging films. In July 2025, it established its first overseas R&D center in the Netherlands to focus on Co-Packaged Optics for high-speed data transmission. Its strategy emphasizes adding new functionalities—such as heat control, content protection, and eco-friendly designs to strengthen its market position.

Toray Industries, Inc. strengthens Lumirror® high-performance films portfolio

Toray is a global leader in functional films, with its Lumirror® biaxially oriented films widely adopted in electronics, packaging, and automotive. It has developed new films with enhanced clarity, durability, and heat resistance, catering to next-generation devices. With a global presence across Asia, Europe, and the Americas, Toray’s focus remains on technological advancement and diversified applications.

Eastman Chemical Company pioneers recycling-based functional films

Eastman is a strong player in automotive protection films, display films, and specialty packaging films. It is investing heavily in chemical recycling technologies, converting difficult plastic waste into high-performance functional films. Known for its durability and optical clarity, Eastman’s strategy is rooted in advancing circular economy models while supplying industries like electronics, automotive, and renewable energy.

Functional Films Market Share Insights

Optical Films Dominate Market Share by Film Type in Functional Films Industry

Optical films lead the functional films industry with 30% share in 2025, reflecting their indispensable role in the booming electronics sector. These films are core to displays in smartphones, tablets, laptops, and televisions, providing brightness enhancement, anti-glare, light diffusion, and energy efficiency. As consumer electronics shift toward higher-resolution OLED and micro-LED displays, the performance requirements for optical films continue to intensify, ensuring steady innovation. Barrier films follow with 25% share, driven by dual demand from food packaging—where they extend product shelf life by blocking oxygen and moisture—and electronics, where they protect sensitive OLED panels and flexible components. Conductive films form the backbone of touchscreens, transparent antennas, and EMI shielding, and their market share is expanding alongside IoT devices and smart wearables. Protective films, while often temporary, remain ubiquitous across industries, safeguarding surfaces from scratches, dust, and abrasion during production and transport. Niche innovations in photovoltaic, smart, and biomedical films represent the cutting edge, where specialized performance dictates adoption. This segmentation demonstrates how optical films drive growth in electronics while barrier, conductive, and protective films anchor volume across packaging and industrial sectors.

Electronics & Semiconductors Lead Market Share by Application in Functional Films Industry

The electronics and semiconductors sector holds 40% of functional films demand in 2025, cementing its position as the primary growth driver. Functional films are not ancillary but enabling technologies for modern devices, powering displays, touchscreens, circuit boards, and chip packaging. The push toward thinner, lighter, and more energy-efficient devices ensures this sector remains the largest and most innovation-driven application. Packaging, with 25% share, is the next largest consumer, relying on high-barrier films to protect food, beverages, and pharmaceuticals from oxygen and moisture while supporting the global shift toward flexible packaging solutions. Automotive adoption is accelerating, as films are integrated into interior touch panels, decorative trims, and thermal/acoustic management solutions, aligning with the rise of connected and electric vehicles. Healthcare and pharmaceuticals increasingly depend on films for sterile medical packaging, drug delivery patches, and diagnostic devices, emphasizing purity and regulatory compliance. Meanwhile, specialized applications in energy (solar films, battery separators) and construction (window tints, protective coatings) highlight how functional films address critical sustainability and performance goals across industries. This segmentation demonstrates how electronics drive cutting-edge innovation, packaging anchors volume, and automotive, healthcare, and energy sectors expand high-value functional film applications.

United States Functional Films Market Accelerated by EPR Regulations and Sustainable Innovations

The U.S. functional films market is navigating a fragmented regulatory environment, with increasing adoption of Extended Producer Responsibility (EPR) laws that transfer the financial burden of recycling and waste management from taxpayers to manufacturers. Technological advancements are reshaping the industry, with the development of mono-material films for pouches and biodegradable solutions emerging as key trends. Academic research highlights the growing use of bio-based films, enhancing sustainability while maintaining functional performance.

Corporate consolidation is influencing market dynamics, with Amcor’s planned acquisition of Berry Global Group in mid-2025 set to strengthen R&D investment in sustainable solutions. Key applications are concentrated in electronics, automotive, and flexible packaging, where films are used for battery insulation, in-cabin displays, and exterior protection in electric vehicles. Sustainability remains a core focus, with manufacturers prioritizing eco-friendly materials such as bio-based films and recyclable paperboard to meet rising consumer and corporate demand for environmentally responsible functional films.

Germany Functional Films Market Leading in Circular Economy and High-Performance Innovations

Germany’s functional films market is shaped by stringent regulations under the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating fully recyclable or reusable packaging by 2030 with strict recycled content guidelines. Technological innovation is driving growth, with Klöckner Pentaplast introducing kp Elite® Nova, a lightweight MAP tray, and winning the German Packaging Award for its Tray2Tray® innovation, emphasizing leadership in circularity.

The country’s Packaging Act (VerpackG) incentivizes recyclable and reusable designs, particularly in food packaging, while the automotive and medical sectors drive demand for reliable, high-performance films. Germany’s strong manufacturing base and export orientation support the market’s growth, with companies focusing on sustainable, technologically advanced functional films that meet regulatory requirements and global standards.

China Functional Films Market Driven by Green Policies and Automation Integration

China’s functional films industry is benefiting from government initiatives aligned with the “dual carbon” goal, encouraging recycling and sustainable materials adoption. The Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement (March 2024) and the GB/T 31268 standard (November 2024) are reshaping packaging practices, especially in e-commerce.

Technological advancements, including AI, automation, and 5G-enabled industrial internet integration, are optimizing production efficiency and flexible manufacturing. Domestic substitution of imported technology is a growing trend, as local companies expand capacity to meet demand. Key applications are concentrated in electronics, automotive, and e-commerce industries, with China’s manufacturing sector driving demand for high-performance composite functional films.

India Functional Films Market Expands with Circular Economy Policies and Local Manufacturing Growth

India’s functional films market is poised for growth due to the Ministry of Environment, Forest and Climate Change’s draft Extended Producer Responsibility (EPR) Rules, 2024, which will impact packaging and printing sectors. Technological advancements, including automated printing systems and specialized film production, are increasing capacity for flexible packaging, particularly in food processing and personal care.

Corporate investments are rising, supported by the Make in India initiative, enabling local manufacturing and technological development. Key applications include frozen and packaged foods, snacks, and e-commerce packaging solutions. The rapid growth of the domestic food processing industry is a significant driver, fostering demand for modern, high-performance, and sustainable functional films across multiple sectors.

Japan Functional Films Market Focused on Recycled BOPP and Specialty High-Performance Films

Japan leads in precision manufacturing and sustainable functional film production, exemplified by Toppan Inc., RM Tohcello Co. Ltd., and Mitsui Chemicals Inc. creating mass-producible recycled BOPP film in September 2024. The Plastic Resource Circulation Act promotes “Design for the environment” and reduced single-use plastics, guiding the industry toward eco-friendly solutions.

Focus is on high-performance, specialty films with superior barrier properties and IoT-enabled tracking. Innovations such as easy-open tear notches and resealable closures cater to single-person households and aging populations. Corporate expansions, including increased PET bottle production by Coca-Cola Bottlers Japan Inc., demonstrate a market response to rising domestic demand for sustainable, technologically advanced functional films.

South Korea Functional Films Market Strengthened by Optical Innovations and Value-Added Products

South Korea’s functional films industry is evolving through technological advancements in biaxially oriented films, with strong positions in optical, electronic, and new energy films. Corporate strategies include alliances like SK Microworks and Kolon Industries joining forces to strengthen competitiveness in technical films against Chinese rivals.

Key applications focus on electronics and automotive sectors, with a shift from LCD to OLED displays maintaining demand for display and optical films. Manufacturers are emphasizing specialty and value-added products due to limited commodity film growth. South Korea’s high export orientation, including electronics, semiconductors, and vehicles, supports demand for high-performance functional films that meet stringent global standards.

Functional Films Market Report Scope

Functional Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$72.2 Billion

|

|

Market Size (2034)

|

$143.1 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Film Type (Optical Films, Barrier Films, Conductive Films, Protective Films, Others), By Material (PET, PP, PE, PVC, Others), By Application (Electronics & Semiconductors, Automotive, Packaging, Energy, Healthcare & Pharmaceuticals, Construction), By Functionality (Anti-reflection, Anti-glare, Heat Control, Anti-fog, Scratch Resistance)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DIC Corporation, DuPont de Nemours, Inc., 3M Company, Nitto Denko Corporation, Sumitomo Chemical Co., Ltd., Eastman Chemical Company, Teijin Limited, LG Chem, SK Group, TORAY INDUSTRIES, INC., FUJIFILM Corporation, Mitsubishi Chemical Group Corporation, Klöckner Pentaplast, The Dow Chemical Company, SABIC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Functional Films Market Segmentation

By Film Type

- Optical Films

- Barrier Films

- Conductive Films

- Protective Films

- Others

By Material

By Application

- Electronics & Semiconductors

- Automotive

- Packaging

- Energy

- Healthcare & Pharmaceuticals

- Construction

By Functionality

- Anti-reflection

- Anti-glare

- Heat Control

- Anti-fog

- Scratch Resistance

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Functional Films Market

- DIC Corporation

- DuPont de Nemours, Inc.

- 3M Company

- Nitto Denko Corporation

- Sumitomo Chemical Co., Ltd.

- Eastman Chemical Company

- Teijin Limited

- LG Chem

- SK Group

- TORAY INDUSTRIES, INC.

- FUJIFILM Corporation

- Mitsubishi Chemical Group Corporation

- Klöckner Pentaplast

- The Dow Chemical Company

- SABIC

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive and integrated research methodology to analyze the Global Functional Films Market, combining primary and secondary research to deliver actionable insights for industry professionals. Primary research included in-depth interviews with key stakeholders, such as film manufacturers, electronics OEMs, packaging converters, renewable energy firms, and regulatory authorities, providing firsthand knowledge of emerging technologies, sustainability initiatives, and market dynamics. Secondary research drew from company reports, press releases, trade journals, government publications, patent filings, and industry databases to validate trends, market drivers, and competitive strategies. Market sizing and forecasts were calculated using historical data, econometric modeling, and trend analysis, emphasizing high-growth segments like optical films for electronics, ultra-high barrier films for flexible devices, bio-based and recyclable packaging films, and films for perovskite solar cells. Regional insights covering the United States, Germany, China, India, Japan, and South Korea were assessed to highlight regulatory impact, technological adoption, and market expansion opportunities. Competitive landscape analysis examined strategic initiatives, R&D investments, and mergers by leading players such as 3M, Toray Industries, Dai Nippon Printing, Covestro, and Eastman Chemical, ensuring a detailed, data-driven, and forward-looking market perspective.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.