Packaging Films Market Outlook, Growth Drivers, and Strategic Insights

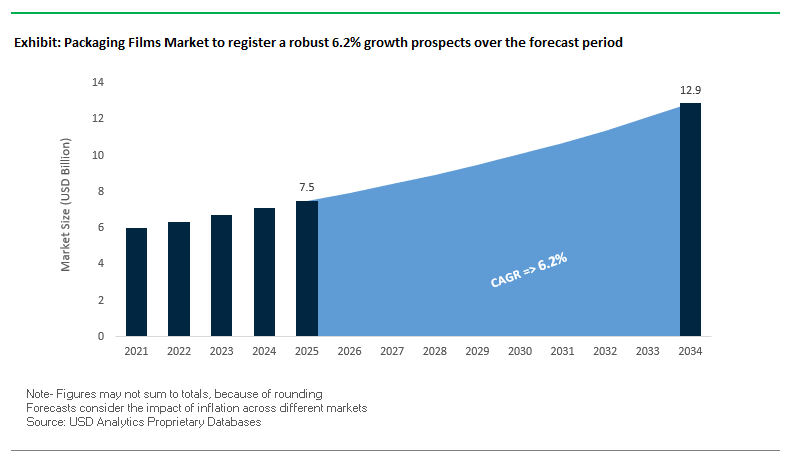

The Global Packaging Films Market is projected to expand from $7.5 billion in 2025 to $12.9 billion by 2034, reflecting a CAGR of 6.2%. This robust growth is fueled by the rising demand for high-performance protective, functional, and decorative films across food, beverage, pharmaceutical, and consumer goods sectors. Packaging films have become indispensable in preserving product quality, extending shelf life, and enhancing brand appeal, while simultaneously supporting sustainability and operational efficiency goals.

Key Insights for Industry Stakeholders

- High-Barrier Film Demand: Films offering protection against moisture, oxygen, and light are critical for reducing food waste and ensuring product safety.

- Shift Toward Sustainable and Mono-Material Films: Growing adoption of single-polymer, bio-based, and recycled content films is reshaping production and recycling requirements.

- Enhanced Aesthetic and Consumer Engagement: Innovative finishes such as matte, velvet, and haptic effects enhance brand differentiation and unboxing experiences.

- Integration of Smart Packaging: Incorporation of QR codes, traceability, and digital interfaces supports real-time product tracking, authenticity verification, and brand-consumer engagement.

- Strategic Industry Consolidation: Mergers, collaborations, and capacity expansions are driving the adoption of high-performance films and shaping competitive dynamics.

The market is defined by a convergence of technological innovation, sustainability imperatives, and consumer-centric design, creating a fertile environment for advanced, flexible, and recyclable film solutions.

Strategic Developments and Sustainability Trends Accelerating Global Packaging Films Market

The Global Packaging Films Industry is evolving rapidly due to technological advancements, strategic mergers, and sustainability initiatives. In August 2025, Amcor announced major upgrades to its Heanor, UK recycling facility to expand high-performance recycled film capabilities, reflecting an increasing focus on circular economy principles. In the same month, Shell Polymers and Charter Next Generation established a commercial agreement for ISCC PLUS certified circular polyethylene, enabling high-performance films with enhanced sustainability credentials.

The July 2025 merger of Amcor and Berry Global Group created a dominant player in flexible films and rigid containers, amplifying demand for next-generation film solutions. In February 2025, Berry Global partnered with Mars to convert pantry jars for M&M’s®, SKITTLES®, and STARBURST® brands to 100% recycled plastic, highlighting a practical implementation of high-performance, sustainable films.

Earlier, October 2024 saw Sabert launch the Hot2Go pack, a fiber-based, fully recyclable packaging solution for hot food, emphasizing plastic-free innovations. Similarly, September 2024 reports underscored the rise of mono-material packaging, driving demand for films compatible with single-polymer recycling streams. In March 2024, Berry Global expanded its flexible film recycling capacity across Europe, while June 2024 marked Toppan’s introduction of the Coreless Organic Interposer, supporting next-generation semiconductor inspection.

Trends and Opportunities Transforming the Packaging Films Market

Accelerated Regulatory Push for Mandated Recycled Content in Plastic Films

The packaging films market is entering a period of legislatively driven transformation as global regulations enforce recycled content mandates. In India, Extended Producer Responsibility (EPR) guidelines from the Ministry of Environment, Forest and Climate Change will require, starting April 2025, a minimum of 10% recycled plastic content in multi-layer flexible packaging films, rising to 20% by 2028–2029. This makes recycled content integration not a choice but a compliance imperative. In parallel, the European Union’s Packaging and Packaging Waste Regulation (PPWR) mandates 30% recycled content for non-food contact plastic packaging by 2030, moving industry practice from voluntary pledges to enforceable obligations. This shift is catalyzing investments in advanced recycling capacity, including PureCycle’s polypropylene recycling facility in Georgia (December 2024) designed to produce virgin-quality resin from waste. At the brand level, companies such as Unilever are backing their 2024 goal to halve virgin plastic usage through direct collaborations with recyclers across Asia. The convergence of regulation, infrastructure investment, and corporate commitments is creating unprecedented demand for post-consumer resin (PCR), making recycled-content films a cornerstone of future packaging strategies.

Strategic Shift to Monomaterial Polyethylene (PE) Film Structures for Recyclability

A parallel transformation in the packaging films market is the shift to monomaterial film structures, particularly polyethylene (PE), to enable compatibility with established recycling streams. Procter & Gamble has already introduced an all-PE pouch for its Lenor laundry product line, demonstrating that recyclable monomaterial formats can provide required oxygen and moisture barriers. The e-commerce sector is another driver, adopting recyclable PE shipping films to simplify end-of-life sorting and reduce landfill contributions. Crucially, technological breakthroughs in plasma coatings and extrusion-based barriers have overcome the historical limitations of monomaterials, enabling PE and PP films to match the oxygen and moisture resistance of traditional multi-layer laminates. Collaboration across the value chain is accelerating commercialization: in a partnership, SABIC and Unilever developed certified circular PE resin derived from mixed plastic waste, which was successfully converted into recyclable monomaterial films. This collaborative approach underscores how polymer producers, converters, and FMCG brands are aligning to scale monomaterial adoption, making recyclability a built-in feature rather than an afterthought.

Development of High-Barrier, Compostable Films for Flexible Packaging

The demand for compostable films is accelerating, particularly in applications where food contamination makes recycling impractical. Research from the Bhabha Atomic Research Centre in India has demonstrated that biodegradable guar gum-based films can provide viable food packaging solutions that decompose with organic waste. This addresses the recycling contamination challenge while advancing circularity. Historically, compostable films lacked barrier performance, but advances in biopolymer blends and nanocomposites now deliver high oxygen and moisture protection, extending shelf life for snacks, fresh produce, and bakery items. Commercial launches are validating scalability: in February 2025, TIPA introduced a home-compostable metallized film for snack packaging, proving compostable materials can meet high-barrier requirements in niche but growing applications. Regulatory frameworks, particularly in Europe, are creating additional incentives by supporting compostable solutions for tea bags, coffee pods, and foodservice items. With industrial composting infrastructure expanding globally, compostable films are emerging as a credible alternative to plastics in food-contact flexible packaging, bridging performance and sustainability requirements.

Integration of Digital Watermarking Technology for Advanced Sorting and Traceability

Another transformative opportunity lies in the adoption of digital watermarking technologies that enable precision sorting and end-to-end traceability. The HolyGrail 2.0 initiative has demonstrated the scalability of this innovation, with German material recovery facility trials processing 56,000 packages daily at 90% detection efficiency. Critically, the technology enabled the identification of nearly 6,000 unique SKUs, allowing recyclers to create high-quality, application-specific recycled streams, a critical step for achieving food-grade recycled content. Waste management companies are responding by investing in add-on watermark readers, with Pellenc ST and Tomra commercializing modules that integrate into existing sorting lines. Beyond recycling, digital watermarks also act as Digital Product Passports, tracking packaging through the supply chain and providing brands with verifiable compliance data for EPR reporting. For consumers, this enhances transparency and brand accountability by enabling real-time authentication and sustainability information. By combining advanced sorting, traceability, and consumer engagement, digital watermarking elevates packaging films from functional substrates to data-rich enablers of the circular economy.

Competitive Landscape: Key Players Driving Innovation and Sustainable Packaging Films

The Global Packaging Films Industry is dominated by leaders leveraging materials science expertise, technological innovation, and sustainability-focused solutions to cater to evolving market needs. These companies are defining industry standards through high-performance, durable, and recyclable film offerings.

Amcor PLC: Leading Sustainable High-Performance Film Solutions

Amcor PLC is a global leader in flexible and rigid packaging, providing a wide portfolio of high-barrier films, flexible pouches, and medical-grade films. The company’s innovations include the AmLite Recyclable film, offering a metal-free, high-barrier solution. Recent moves include recycling facility upgrades in August 2025 and completion of its merger with Berry Global in July 2025, strengthening its leadership in sustainable consumer packaging. Amcor focuses on circular economy adoption, product recyclability, and sustainable innovation.

Berry Global Group, Inc.: Advancing Circular Economy and High-Performance Film Capabilities

Berry Global specializes in multilayer films for food, agricultural, and industrial applications, emphasizing sustainability through its Sustane® recycled polymer range. Strategic developments include Mars collaboration in February 2025 to transition pantry jars to 100% recycled plastic and expanded European recycling capacity in March 2024. Berry Global’s Impact 2025 plan drives innovation in recycled-content films while supporting clients’ circular economy goals.

CCL Industries Inc.: Innovating Specialty Films with Global Expansion Focus

CCL Industries, through its Innovia Films division, provides high-performance BOPP and specialty films for food, beverage, and personal care. August 2025 financial results underscored strong growth and global expansion initiatives. Key offerings include Propafilm™, a sustainable, versatile film product. CCL emphasizes global capacity optimization, innovation in extrusion facilities, and premium specialty packaging solutions.

Sealed Air Corporation: Enhancing Food Safety with Protective and Recyclable Films

Sealed Air Corporation focuses on high-barrier protective films for perishable goods, including the Cryovac® brand. Recent developments include Q2 2025 financial results and executive leadership updates. Sealed Air aims to deliver recyclable and reusable packaging by 2025, improving food safety and supply chain efficiency. Its strategic emphasis is on sustainability, innovation, and e-commerce-ready film solutions.

Jindal Poly Films Limited: Expanding Global BOPP and BOPET Film Capabilities

Jindal Poly Films is a leading manufacturer of BOPP and BOPET films for flexible packaging, labeling, and industrial applications. August 2025 initiatives include industrial innovation projects and new partnerships to broaden application scenarios. Jindal focuses on continuous product innovation, manufacturing excellence, and global market expansion.

Uflex Limited: Integrating Sustainability and Technology Across Film and Packaging Solutions

Uflex Limited, based in India, offers BOPET, BOPP, and CPP films, including high-barrier, metallized, and holographic options. Recent innovations include Asclepius™ BOPET films with 100% PCR content and Satellite Thermal Insulation Film for ISRO. Uflex leverages vertically integrated operations to provide comprehensive, sustainable packaging solutions, encompassing design, manufacturing, and recycling.

Packaging Films Market Share Insights

Biaxially Oriented Films Dominate Market Share by Film Type in the Packaging Films Industry

Biaxially oriented films (BOPP, BOPET, etc.) command 32% of the global packaging films market, securing their position as the most widely used film type across food, beverage, and personal care applications. Their dominance stems from the unique balance of optical clarity, tensile strength, barrier performance, and cost efficiency, making them indispensable in flexible packaging structures. BOPP films are the backbone of snack, confectionery, and label packaging, while BOPET’s higher oxygen and aroma barrier properties make it ideal for dried foods, coffee, and premium laminates. In contrast, stretch and shrink films collectively account for a substantial share in transport and logistics packaging, with stretch films driving pallet unitization efficiency and shrink films ensuring multipack integrity for beverages and retail-ready products. Meanwhile, specialty films such as metallized and lidding films, though smaller in volume, play an outsized role in value creation with metallized films extending product shelf-life and enhancing shelf appeal, and lidding films enabling modified atmosphere packaging (MAP) and sterile pharmaceutical sealing. This segmentation demonstrates how biaxially oriented films lead on scale, while specialty films capture premium value in highly regulated and sensitive applications.

Food & Beverage Packaging Holds the Largest Market Share by Application in the Packaging Films Industry

The food and beverage sector accounts for 58% of global demand for packaging films, establishing itself as the primary growth driver for this industry. The shift from rigid packaging formats to flexible films is accelerating, fueled by consumer demand for convenience, lightweighting, and extended shelf-life solutions. High-barrier packaging films are indispensable for frozen meals, snack foods, dairy, beverages, and portion-controlled packs, reducing food waste and meeting regulatory standards for food safety. The sector’s influence is amplified by the rise of ready-to-eat meals, frozen foods, and e-commerce-driven grocery distribution, all of which demand films with tailored performance properties such as puncture resistance, seal integrity, and moisture/oxygen control. Beyond volume, the food and beverage industry also sets the innovation agenda for packaging films, driving investment in recyclable mono-material films, compostable bio-films, and advanced lidding technologies. While healthcare, pharmaceuticals, and personal care leverage specialized films for sterile packaging and aesthetics, it is the food and beverage segment that continues to dictate the global packaging films demand curve.

United States Packaging Films Market Strengthened by EPR Laws and Recycling Initiatives

The United States packaging films market is increasingly shaped by the country’s evolving Extended Producer Responsibility (EPR) framework. State-level regulations, such as California’s SB-54, require manufacturers to boost the use of recyclable materials and increase post-consumer recycled (PCR) content in packaging films. In 2025, Hawaii and Rhode Island passed pre-EPR bills, setting the stage for broader legislation that will accelerate circular economy practices. This trend has pushed brand owners and film converters to redesign materials for recyclability and to adopt mono-material solutions that align with regulatory requirements.

A major highlight is the August 2025 launch of the U.S. Flexible Film Initiative (USFFI) by General Mills, Mars, PepsiCo, and other partners. This nonprofit aims to prove that flexible packaging can be recycled at scale, funding Material Recovery Facilities (MRFs) and recyclers across the country. Such initiatives, coupled with federal support for eco-friendly materials, underscore the growing integration of sustainability into packaging. Demand is particularly strong in e-commerce and consumer packaged goods (CPG), with healthy snacks and fortified smoothies requiring high-barrier films to ensure freshness and extended shelf life.

Germany Packaging Films Market Driven by EU PPWR Compliance and Advanced Film Technologies

Germany’s packaging films market is heavily influenced by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which mandates ambitious recyclability and recycled-content targets. To comply, German producers are investing in high-performance materials that balance barrier properties with environmental credentials. The amended German Packaging Act further strengthens this demand, ensuring that packaging films are optimized for sustainability and circularity.

In March 2025, Innovia Films launched a €70 million production line utilizing LISIM (Linear Motor Simultaneous Stretching Machine) technology to manufacture thinner, energy-efficient multi-layer co-extrusion films. This facility reflects the country’s position as a hub for advanced extrusion lines and sustainable packaging innovation. The investment is part of Innovia’s “Better Future” strategy, focusing on eco-friendly films for flexible packaging and labeling. The strongest growth is visible in food and beverage applications, where packaging films preserve freshness, extend shelf life, and comply with sustainability regulations while meeting consumer expectations for product safety.

China Packaging Films Market Accelerated by Dual-Carbon Goals and Crackdown on Over-Packaging

The Chinese packaging films market is undergoing rapid transformation under the government’s dual-carbon targets, which aim for carbon peaking by 2030 and neutrality by 2060. These policies are driving the adoption of recyclable, lightweight, and eco-friendly films. At the same time, the State Council has launched initiatives to curb over-packaging, with a whole-chain administration system set to be operational by 2025. Retailers are being obligated to provide in-store take-back programs and disclose packaging reduction metrics, creating stricter demand for sustainable packaging films.

Chinese producers are also making significant strides in automation and AI-driven packaging film production, improving efficiency and traceability across supply chains. The government is backing these moves with smart regulatory tools that enhance food safety and product tracking. Market growth is strongest in e-commerce, consumer goods, and electronics packaging, supported by the massive scale of parcel deliveries—measured in hundreds of billions annually. These dynamics are reinforcing China’s role as one of the fastest-growing and innovation-led packaging films markets worldwide.

India Packaging Films Market Boosted by PLI Scheme and Sustainable Film Innovation

The Indian packaging films market is benefiting from government-led programs such as Make in India and the Production Linked Incentive (PLI) scheme, which support local manufacturing and innovation. The Union Budget 2025 also prioritized MSME development and sustainability, signaling a favorable policy landscape for film converters and packaging producers. The government’s strict Plastic Waste Management Rules, including bans on single-use plastics, are accelerating the demand for recyclable and compostable packaging films.

Corporate players are responding with innovation. Cosmo Films is pioneering sustainable film technologies, using renewable resources to reduce plastic dependence. These efforts align with India’s broader circular economy goals and reflect growing consumer demand for eco-friendly packaging. Applications are especially strong in on-the-go beverages and ready-to-drink products such as juices, energy drinks, and RTD teas and coffees. With e-commerce expanding rapidly, packaging films are now indispensable for brand presentation, product safety, and shelf appeal, cementing their role in India’s fast-evolving packaging industry.

Japan Packaging Films Market Evolving Under Positive List Regulations and Bio-Based Plastics

Japan’s packaging films market is influenced by regulatory changes that came into force on June 1, 2025, introducing a positive list system for food-contact materials. This regulation restricts synthetic substances in packaging, driving adoption of paper-based and bio-based alternatives with approved coatings. These measures are closely tied to Japan’s ambitious climate targets of reducing greenhouse gas emissions by 46% by 2030 and reaching carbon neutrality by 2050.

On the corporate front, Japanese firms are pioneering high-quality and functional packaging films that combine sustainability with performance. In September 2025, LyondellBasell partnered with Futamura Chemical and Iwatani to integrate bio-based polypropylene into cosmetic packaging. This initiative reflects Japan’s goal of introducing 2 million tonnes of bio-PP plastic products annually by 2030. Strong demand comes from ready-to-drink tea, coffee, and snack packaging, where lightweight, durable, and aesthetically pleasing films remain essential. By prioritizing both functionality and environmental compliance, Japan continues to set benchmarks in sustainable packaging film design.

Brazil Packaging Films Market Strengthened by Anvisa Regulations and Circular Economy Goals

Brazil’s packaging films market is adapting to new food-contact safety regulations introduced by Anvisa in February 2025, which revised the positive list of substances for plastics in contact with food. This update, which added two new approved chemicals, aligns Brazilian standards with international benchmarks and ensures greater consumer protection. Additionally, the National Solid Waste Policy (PNRS) is obligating companies to recycle a higher share of their products, directly impacting the design and sustainability of packaging films.

Sustainability is also being reinforced by corporate and collaborative innovation. Klabin, in partnership with Optima and Soulpack, recently launched a recyclable paper-based diaper packaging solution, demonstrating Brazil’s growing commitment to reducing plastic use. At the same time, manufacturers are increasing adoption of bio-based materials derived from corn starch and sugarcane bagasse. The food and beverage industry remains the largest consumer of packaging films in Brazil, with canned goods and processed food requiring high-barrier films for product protection and shelf stability. With recycling obligations set to tighten further, the demand for recyclable and bio-based films is expected to accelerate.

Packaging Films Market Report Scope

Packaging Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.5 Billion

|

|

Market Size (2034)

|

$12.9 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Material Type (PP, PE, PET, PA, PVC, Others), By Film Type (Cast Films, Biaxially Oriented Films, Metallized Films, Lidding Films, Shrink Films, Stretch Films), By Application (Food & Beverage, Healthcare & Pharmaceutical, Personal Care & Cosmetics, Industrial, Automotive, Others), By End-Use Industry (Food Processing, Pharmaceutical Manufacturing, Consumer Goods, Retail, E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Huhtamaki Oyj, Mondi Group, Sealed Air Corporation, Taghleef Industries, Cosmo Films Ltd., Toray Industries, Inc., Tekni-Plex, Inc., Transcontinental Inc., Winpak Ltd., Flexopack S.A., Innovia Films Ltd., Novolex Holdings, LLC, Tredegar Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Films Market Segmentation

By Material Type

By Film Type

- Cast Films

- Biaxially Oriented Films

- Metallized Films

- Lidding Films

- Shrink Films

- Stretch Films

By Application

- Food & Beverage

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- Industrial

- Automotive

- Others

By End-Use Industry

- Food Processing

- Pharmaceutical Manufacturing

- Consumer Goods

- Retail

- E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Films Market

- Amcor plc

- Berry Global Inc.

- Huhtamaki Oyj

- Mondi Group

- Sealed Air Corporation

- Taghleef Industries

- Cosmo Films Ltd.

- Toray Industries, Inc.

- Tekni-Plex, Inc.

- Transcontinental Inc.

- Winpak Ltd.

- Flexopack S.A.

- Innovia Films Ltd.

- Novolex Holdings, LLC

- Tredegar Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and multi-faceted research methodology to analyze the Global Packaging Films Market, combining both primary and secondary research sources to ensure accuracy and relevance for industry professionals. Primary research includes direct interviews with key executives, product managers, and industry stakeholders from leading packaging film manufacturers such as Amcor, Berry Global, and Uflex, along with surveys of end-users across food & beverage, pharmaceutical, and consumer goods sectors to capture demand-side insights. Secondary research encompasses an exhaustive review of company reports, press releases, regulatory frameworks, government policies, trade associations, and industry publications to map market trends, technological innovations, and sustainability initiatives. Quantitative modeling is applied to forecast market size, segment shares, and growth trajectories using historical data, current developments, and macroeconomic indicators such as consumer demand, e-commerce penetration, and regulatory mandates like EPR and PPWR. Additionally, USDAnalytics incorporates scenario-based analysis to account for emerging trends, including monomaterial and compostable films, digital watermarking for traceability, and AI-enabled quality monitoring, ensuring that forecasts reflect both current realities and future disruptions. Competitive intelligence is assessed by analyzing strategic mergers, capacity expansions, and technology adoption among global players, providing actionable insights into market dynamics, key opportunities, and potential risks. The methodology emphasizes transparency, repeatability, and professional relevance, making it a robust framework for stakeholders seeking to navigate the evolving packaging films landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.