Medical Packaging Films Market Overview: Size, Growth, and Key Insights

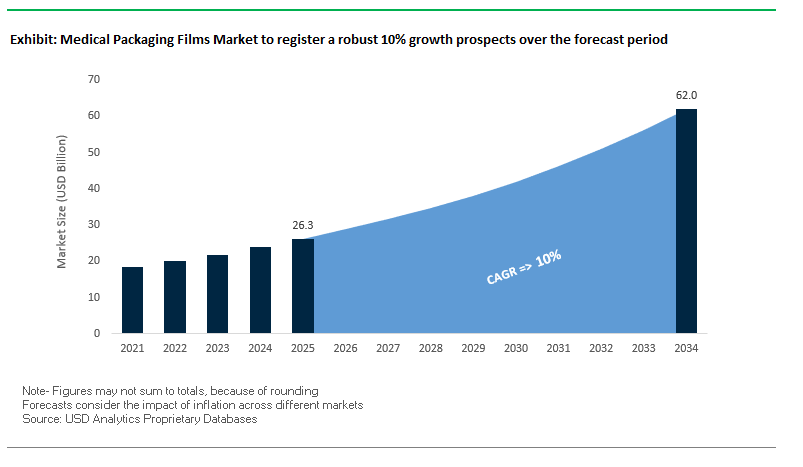

The global medical packaging films market is projected to reach $26.3 billion in 2025 and expand to $62 billion by 2034, growing at an impressive CAGR of 10%. This growth reflects the critical role of packaging films in safeguarding medical devices, diagnostics, and pharmaceuticals while ensuring sterility, integrity, and sustainability. For industry professionals, this market answers key questions: How are sterile barriers evolving with advanced sterilization methods? How do high-barrier films extend shelf life and product efficacy? And how are sustainability and recyclability reshaping procurement decisions?

A defining factor for the industry is the non-negotiable demand for sterile barrier films, as healthcare systems worldwide expand their reliance on single-use and minimally invasive devices. Another critical growth driver is the increasing adoption of high-barrier films to protect sensitive pharmaceuticals and diagnostics against oxygen, light, and moisture, ensuring longer shelf lives and reducing product wastage. At the same time, the sustainability imperative is forcing packaging providers to innovate with recyclable, paper-based, and circular economy-friendly solutions. Additionally, the rise of thermoformable films is fueling demand for trays, blisters, and protective packaging that combine formability with strong barrier performance.

Key Insights for Industry Professionals:

- Sterile barrier films are indispensable for infection control and compliance with regulatory sterilization standards.

- High-barrier medical films extend pharmaceutical product integrity and reduce spoilage across supply chains.

- Sustainable materials—including paper-based and recycle-ready films—are gaining adoption in alignment with ESG mandates.

- Thermoformable films are expanding with the growing use of rigid and semi-rigid medical device packaging.

Market Analysis: Recent Developments Reshaping Medical Packaging Films

The medical packaging films industry is undergoing rapid transformation, driven by investments, mergers, and innovations that directly impact how packaging films are designed and used. In September 2025, a new industry report highlighted the steady rise of barrier materials, emphasizing their importance in both pharmaceutical growth and sustainable packaging adoption. This focus on sustainability and partnerships shows how leading companies are aligning long-term strategies with regulatory and market demands.

Several pivotal developments in July 2025 reflect how global leaders are reshaping capacity and innovation. Amcor announced its upcoming fiscal 2025 results release, signaling transparency in financial performance to stakeholders and shedding light on the company’s broader healthcare packaging strategy. That same month, JPFL Films committed Rs 700 crore to expand its Nashik plant in India, a move aimed at scaling flexible packaging capabilities for industries including healthcare. Meanwhile, Jindal Films launched India’s first BOPA nylon films for pharma and food, underscoring the industry’s focus on advanced barrier materials. On the technology side, Dymax introduced its hybrid light-curable adhesive platform in June 2025, a development that could indirectly influence film specifications as device assembly requirements evolve.

Expansion in Asia-Pacific is another clear market-shaping trend. In May 2025, Oliver Healthcare Packaging opened its largest Asia-Pacific facility in Malaysia, enhancing local capacity for sterile barrier solutions. This follows Amcor’s April 2025 completion of its advanced coating facility in Selangor, Malaysia, featuring air knife technology for superior medical substrates. Consolidation is also influencing competition: in March 2025, the merger approval of DS Smith and Mondi Group signaled the creation of a global packaging powerhouse with implications for supply chain scale, innovation speed, and market competition.

Key Trends and High-Value Opportunities in the Medical Packaging Films Market

Strategic Investment in High-Barrier Films for Biologics and mRNA Therapeutics

The medical packaging films market is witnessing a surge in demand for ultra-high barrier films due to the rapid growth of biologics and mRNA-based therapeutics. These advanced pharmaceuticals are highly sensitive to oxygen and moisture, requiring packaging that surpasses conventional blister or pouch films. The expansive pipeline of mRNA therapies, including over 100 programs across infectious diseases, oncology, rare, and latent diseases as of September 2025, is driving this need. High-barrier films provide ultra-low permeability, with oxygen transmission rates (OTR) and water vapor transmission rates (WVTR) below 0.1, ensuring the stability and potency of sensitive biologics. Such films are essential for preventing protein degradation and maintaining lyophilized drug efficacy from manufacturing to patient administration. Strategic capacity expansions by key players like DuPont, with investments in the Tyvek® line, are meeting the surging demand for medical-grade, high-performance films in the growing biopharma sector.

Accelerated Adoption of Recyclable Mono-Material Polymer Structures

The push for sustainability is driving medical packaging companies to adopt mono-material polymer films that are fully recyclable, replacing multi-layer laminates that are difficult to recycle. Mono-material films reduce carbon footprint significantly; research indicates that incorporating 10% recycled content in mono-material films can cut CO2 emissions by over 3,600 kg per ton of plastic. Regulatory mandates like the EU Packaging and Packaging Waste Regulation (PPWR) are compelling companies to meet ambitious recyclability targets, further accelerating the adoption of sustainable solutions. Innovations such as graphene oxide-coated mono-material films achieve barrier properties comparable to multi-material laminates, with a 94-99% reduction in oxygen transmission and 68-73% reduction in water vapor permeation. Collaborations by industry leaders like Toppan are advancing sustainable, single-stream recyclable films, showcasing the market’s move towards environmentally friendly yet high-performance packaging solutions.

Expansion of Film-Based Packaging for Automated Dispensing Systems

The increasing reliance on automated pharmacy and bedside dispensing systems presents a lucrative opportunity for unit-dose medical packaging films. These systems enhance pharmacy efficiency, reducing manual medication handling by up to 80%, minimizing human error, and enabling pharmacists to focus on patient care. Films must be compatible with high-speed robotics, ensuring precision in automated sealing and handling of blister packs and soft pill packets. Unit-dose packaging also supports patient adherence in home care, simplifying complex regimens and reducing the likelihood of missed or incorrect doses. The trend underscores the growing importance of film-based packaging solutions tailored to automation and patient-centric applications in both hospital and at-home settings.

Development of Smart Film Packaging for Supply Chain Integrity and Patient Engagement

The integration of digital technologies with packaging films is creating opportunities for smart medical packaging that enhances supply chain integrity and patient engagement. NFC, RFID, and QR codes embedded in films provide robust safeguards against counterfeiting, offering a secure digital fingerprint for each product unit. Smart films also improve patient adherence by tracking dosage removal and sending real-time data to mobile apps, which is critical for clinical trial compliance. Additionally, embedding RFID and NFC technologies into films delivers end-to-end supply chain visibility, allowing stakeholders to monitor product location and environmental conditions, ensuring product integrity and reducing waste. This convergence of packaging and technology is redefining the value proposition of medical packaging films in the digital healthcare era.

Competitive Landscape: Leading Companies in the Medical Packaging Films Industry

The global medical packaging films market is highly competitive, with leaders differentiating themselves through advanced material science, sustainability initiatives, and geographic expansions. The competition is marked by innovations in recyclable and high-barrier films, alongside large-scale facility investments in Asia and Europe. Below is an overview of the top companies shaping this industry.

Amcor plc: Advancing Sustainable and Recyclable Medical Films

Amcor is a global leader in flexible and rigid packaging with a strong healthcare portfolio, including retortable films, barrier laminates, and thermoformable films. In April 2025, Amcor completed a state-of-the-art coating facility in Selangor, Malaysia—the first in Asia to produce top and bottom substrates for sterile medical packaging. Its AmSky system, a vinyl- and aluminum-free blister solution made from polyethylene (PE), is recycle-ready and compatible with existing packaging lines. Amcor’s long-term vision is tied to sustainability, with a goal of making all packaging recyclable, reusable, or compostable by 2030 and incorporating at least 30% recycled materials.

Oliver Healthcare Packaging: Strengthening Sterile Barrier Leadership in Asia-Pacific

Oliver Healthcare Packaging specializes in sterile barrier flexible solutions such as pouches, lids, and roll stock. In May 2025, it opened its largest Asia-Pacific manufacturing facility in Johor, Malaysia, equipped with ISO-7 and ISO-8 cleanrooms and certified to ISO 13485 standards. This expansion enhances Oliver’s ability to serve growing pharmaceutical and device demand in the region. The company also strengthened its European operations through the 2023 acquisition of EK-Pack Folien, improving supply chain security. Its strength lies in its global sterile packaging expertise, combined with in-region facilities that support regulatory compliance and reliability.

Constantia Flexibles: Driving Eco-Friendly Medical Films Through Innovation

Constantia Flexibles is a major global supplier of flexible packaging with a dedicated pharmaceutical division. In July 2025, the company announced a €6.5 million investment in film technology, including a Hosokawa Alpine MDO line, signaling its commitment to advanced barrier and sustainable solutions. Constantia’s award-winning products, including EcoPeelCover and EcoLamHighPlus, focus on recyclable, mono-material films that maintain high-barrier protection. Its strategic direction is clear: being a sustainability leader in flexible packaging while responding to pharmaceutical and healthcare customer needs for eco-friendly yet high-performance films.

Jindal Films: Expanding Specialty Film Capabilities with Large Investments

Jindal Films is a global leader in polypropylene (PP) and polyethylene (PE) films, serving multiple industries including pharmaceuticals. In July 2025, it announced a Rs 700 crore expansion at its Nashik plant, aimed at enhancing BOPP film lines with advanced packaging film capabilities. It also introduced India’s first BOPA nylon films for pharma and food, reflecting its innovation edge. With a sustainability focus, Jindal has launched EthyLyte™ films, designed for recycle-ready solutions. Its acquisition of DOMO Films Solutions in 2021 strengthened its nylon films portfolio, expanding its role in specialized pharmaceutical packaging.

3M Company: Leveraging Materials Science for Medical Film Innovation

3M maintains a strong presence in the medical films market, producing medical-grade films, tapes, and laminates used in wound care, surgical applications, and transdermal patches. In March 2024, 3M launched an eco-friendly barrier film, highlighting its shift toward sustainability. Its competitive edge lies in combining advanced materials science with expertise in skin-friendly solutions that enhance patient comfort and device reliability. 3M’s broad offerings, backed by significant R&D investment, position it as a versatile player with solutions spanning medical packaging films and adhesive technologies.

Medical Packaging Films Market Share Insights

Thermoformable Films Dominate Market Share by Product Type in Medical Packaging Films

Thermoformable films command 35% of the medical packaging films market, underscoring their role as the backbone of sterile barrier systems. These films, primarily PETG, PP, or multilayer structures, are used to create rigid cavities in surgical trays that protect high-value instruments, implants, and complex procedure kits. Their dominance is fueled by the growth of single-use surgical kits and advanced device sets, which require precise formability, clarity for visibility, and mechanical strength to withstand global logistics. Moreover, thermoformable films support branding and labeling requirements while maintaining compliance with ISO 11607 sterile packaging standards. While high-barrier and co-extruded films address niche needs, thermoformable films remain the structural core of sterile medical packaging, ensuring their leading share.

Bags and Pouches Hold the Largest Market Share by Application in Medical Packaging Films

Bags and pouches account for 45% of medical packaging film applications, making them the high-volume workhorse of sterile medical packaging. They are universally adopted for packaging a wide range of disposable medical devices, from syringes and sutures to advanced diagnostic kits. Their popularity is driven by cost-effectiveness, flexibility, and versatility, with clear polymer films combined with Tyvek® or breathable membranes to allow sterilant penetration while ensuring a microbial barrier. Bags and pouches also reduce logistics costs by minimizing bulk, making them the most efficient solution for large-scale hospital and manufacturing use. As healthcare providers expand single-use sterile supplies to reduce infection risks, this segment’s dominance will continue to be reinforced by both volume demand and regulatory compliance requirements.

United States Medical Packaging Films Market Expands with FDA QMSR Compliance and Smart Innovations

The U.S. medical packaging films market is governed by strict FDA regulations, including the Quality Management System Regulation (QMSR) Final Rule, effective early 2024, aligning with ISO 13485:2016. This framework ensures sterility, integrity, and uniform quality standards across medical device packaging. Technological innovations are driving the adoption of smart and sustainable packaging films, integrating sensors and indicators for sterilization monitoring, temperature control, and environmental tracking. In January 2025, a leading U.S. firm launched PFAS-free hydrophilic films, reflecting the growing trend toward eco-friendly and safe packaging materials.

Corporate investments are expanding production capacity, such as Amcor’s acquisition of a medical device packaging company in February 2024 to enhance its Asia-Pacific presence. Demand is strong in home healthcare and e-commerce, driven by continuous glucose monitors and remote patient monitoring systems, requiring durable, sterile, and user-friendly packaging films. Sustainability remains a priority, with companies developing recyclable and bio-based materials, exemplified by novel thermoforming films introduced in November 2023, ensuring compliance with environmental regulations and industry standards.

Germany Medical Packaging Films Market Strengthens with MDR Compliance and Sustainable Innovations

Germany’s medical packaging films market operates under the European Union Medical Device Regulation (MDR 2017/745), requiring enhanced traceability via UDI systems that influence labeling and film design. The market is a leader in high-performance and sustainable packaging films, with companies like Mondi showcasing plastic-free, recyclable designs at FachPack trade fairs. These innovations address eco-conscious regulations while ensuring product safety and integrity.

Germany’s focus on circular economy practices promotes the use of de-inkable, solvent-free, and water-based adhesive films, reducing environmental impact. High-value applications such as surgical instruments, implants, and diagnostics drive the demand for advanced packaging films, with the country’s robust healthcare and MedTech sectors supporting continuous innovation and adoption of regulatory-compliant, sustainable film solutions.

China Medical Packaging Films Market Grows Through Government Initiatives and Technological Advancements

China’s medical packaging films market is supported by government measures, including a mid-2025 10-measure plan to advance high-end medical device production and standardization. The NMPA is implementing regulatory reforms, such as the draft Medical Device Administrative Law (MDAL), which removes the pre-approval requirement in the device’s country of origin, streamlining foreign packaging film market entry.

Technological investments in automation and AI enhance production efficiency, particularly for high-end domestic devices, driving demand for advanced films that meet international safety and quality standards. Applications span films for various medical devices to single-use disposables, with a strong emphasis on sterility, barrier protection, and compliance to serve China’s rapidly growing healthcare sector.

India Medical Packaging Films Market Boosted by Make in India and Advanced Barrier Technologies

India’s medical packaging films market is propelled by the Make in India initiative and the National Medical Devices Policy 2023, aimed at enhancing domestic manufacturing. In August 2025, the CDSCO amended risk-based categorization for cardiovascular and neurological devices, supporting industry growth. The Production Linked Incentive (PLI) Scheme encourages domestic and foreign investments in MedTech manufacturing, including advanced packaging films.

The market is witnessing rising adoption of high-performance sterilization and barrier films, capable of withstanding harsh processes while maintaining product integrity. Investments in medical device parks like the Andhra Pradesh MedTech Zone (AMTZ) facilitate growth in R&D, production, and commercialization, supporting applications in pharmaceutical, surgical, and implantable medical devices.

Japan Medical Packaging Films Market Leads with Precision Engineering and High-Barrier Innovations

Japan’s medical packaging films market leverages the country’s expertise in precision manufacturing and advanced material technologies. Companies like Toray Industries produce high-barrier films for pharmaceuticals and medical devices, ensuring reliability and sterility. Regulatory oversight by the PMDA, alongside a May 2025 amendment to the Pharmaceuticals and Medical Devices Act, strengthens supply chain stability and impacts film production and logistics.

The market is increasingly focused on specialty and value-added packaging films, catering to sensitive devices that require fast, reliable, and automated assembly solutions. Innovations in functionality address surgical and dental packaging needs, providing improved sterility, usability, and compliance with global standards.

Brazil Medical Packaging Films Market Expands with UDI System and Sustainable Manufacturing

Brazil’s medical packaging films market benefits from the national UDI system (Siud) launched in July 2025, aligning with global traceability requirements and influencing packaging and labeling compliance. Technological advancements emphasize biodegradable, recyclable, and compostable films, with companies like Indorama Ventures expanding recycling capabilities to increase recycled PET supply for packaging films.

Corporate investments strengthen local manufacturing, exemplified by Sonoco’s acquisition of a Brazilian flexible packaging joint venture in April 2022, reducing import dependency and enhancing the domestic supply chain. The market is driven by pharmaceutical and medical device sectors, supported by growing demand for packaged goods and the rise of online retail, emphasizing the need for high-quality, compliant, and sustainable packaging films.

Medical Packaging Films Market Report Scope

Medical Packaging Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26.3 Billion

|

|

Market Size (2034)

|

$62 Billion

|

|

Market Growth Rate

|

10%

|

|

Segments

|

By Material (Plastics, Paper & Paperboard, Metal), By Product Type (Thermoformable Films, High-Barrier Films, Breathable & Porous Films, Co-extruded & Laminated Films), By Application (Bags & Pouches, Blister Packs, Lidding, Form-Fill-Seal), By End-User (Pharmaceutical Manufacturing, Medical Device Manufacturers, Diagnostic Laboratories, Hospitals & Clinics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Tekni-Plex, Inc., Huhtamaki Oyj, Sonoco Products Company, Bemis Company, Inc., Avery Dennison Corporation, Klöckner Pentaplast, Coveris Holdings S.A., Oliver Healthcare Packaging, Toray Industries, Inc., ACG, Wipak Group, SteriPack Group, Nelipak Healthcare Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Packaging Films Market Segmentation

By Material

- Plastics

- Paper & Paperboard

- Metal

By Product Type

- Thermoformable Films

- High-Barrier Films

- Breathable & Porous Films

- Co-extruded & Laminated Films

By Application

- Bags & Pouches

- Blister Packs

- Lidding

- Form-Fill-Seal

By End-User

- Pharmaceutical Manufacturing

- Medical Device Manufacturers

- Diagnostic Laboratories

- Hospitals & Clinics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Packaging Films Market

- Amcor plc

- Berry Global Inc.

- Tekni-Plex, Inc.

- Huhtamaki Oyj

- Sonoco Products Company

- Bemis Company, Inc.

- Avery Dennison Corporation

- Klöckner Pentaplast

- Coveris Holdings S.A.

- Oliver Healthcare Packaging

- Toray Industries, Inc.

- ACG

- Wipak Group

- SteriPack Group

- Nelipak Healthcare Packaging

* List Not Exhaustive

Methodology

The research methodology for the global Medical Packaging Films market employs a combination of primary interviews, secondary research, and rigorous analytical modeling to deliver actionable insights for industry professionals. Primary research involved discussions with packaging film manufacturers, pharmaceutical and medical device companies, regulatory authorities, and supply chain experts to understand adoption trends in high-barrier, thermoformable, and sustainable films. Secondary research included analyzing company reports, press releases, ISO 11607 and FDA QMSR standards, EU Packaging Waste Regulations, and trade publications to validate innovations, regulatory compliance, and sustainability initiatives. Market sizing, segmentation by material, product type, application, and end-user, along with forecasting growth, was conducted using both top-down and bottom-up approaches, factoring in key drivers such as biologics and mRNA therapeutic expansion, automated dispensing systems, and smart packaging technologies. This comprehensive methodology ensures that USDAnalytics provides precise, data-driven intelligence on market dynamics, competitive strategies, and emerging opportunities within the medical packaging films industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.