Market Overview: Strong Growth Driven by Minimally Invasive Surgeries and Wearable Devices

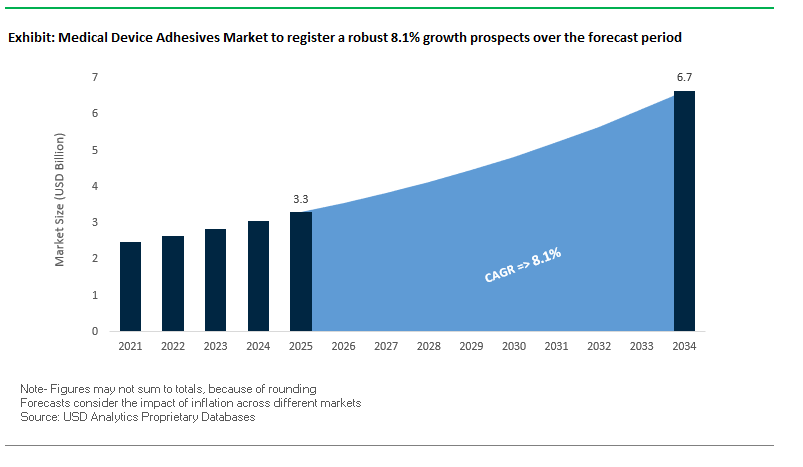

The global medical device adhesives market is projected to grow from $3.3 billion in 2025 to $6.7 billion by 2034, expanding at a healthy CAGR of 8.1%. This growth is fueled by a combination of rising demand for minimally invasive procedures, increasing use of wearable health technologies, and stricter biocompatibility regulations for adhesives used in medical device assembly. The market is also seeing greater emphasis on versatility, with adhesives required to bond plastics, metals, and glass for complex device designs. For industry professionals and buyers, the key questions revolve around how adhesive suppliers are meeting regulatory compliance, scaling sustainable production, and adapting to wearable medical device applications that require skin-friendly, long-lasting adhesion.

Key Insights for professionals

- Minimally Invasive Procedures Boost Demand: Advanced adhesives are increasingly preferred over sutures or staples in wound closure and device fixation.

- Wearables Drive New Applications: Adhesives for continuous glucose monitors and health trackers must be sweat-resistant, durable, and skin-compatible.

- Regulatory Compliance Imperative: ISO 10993 biocompatibility testing is a standard benchmark for adhesive safety and approval.

- Versatile Bonding Solutions: Manufacturers demand adhesives that can bond diverse materials like ABS plastics, stainless steel, and polycarbonate with precision.

Market Analysis: Recent Industry Developments and Emerging Trends

The medical device adhesives industry is undergoing rapid transformation, with innovation, regulatory milestones, and regional growth shaping the competitive landscape. In September 2025, a Roots Analysis study highlighted Asia’s growing dominance in the medical adhesives sector, attributing this to rising healthcare expenditure, industrial growth, and strong demand for advanced wound closure and device assembly solutions. The Asian market is expected to play a critical role in global supply chain expansion.

In August 2025, Paris-based TISSIUM secured FDA Investigational Device Exemption (IDE) approval for its vascular sealant polymer, a light-activated pre-polymer that reduces postoperative bleeding and doubles as a resin for 3D-printed implantable devices. Around the same time, a 24ChemicalResearch report underlined three major drivers of market innovation: FDA approvals for new adhesive products, advancements in sustainable raw materials, and the integration of 3D printing with biomaterials for next-generation medical devices. Meanwhile, Arkema’s Bostik division was recognized in July 2025 for its advancements in fluoropolymer adhesives, further solidifying its R&D leadership.

Technological innovation is also accelerating. In June 2025, Dymax introduced its Hybrid Light-Curable (HLC) adhesive platform, with the first product (HLC-M-1000) capable of bonding opaque substrates, a breakthrough for complex medical device designs. Similarly, in March 2025, Henkel showcased its LED-curing technologies under the LOCTITE brand, enabling energy-efficient and eco-friendly production. Demand for biologically derived solutions also grew, with a Coherent Market Insights report (April 2025) emphasizing fibrin-based adhesives as a growing preference due to ease of use and superior sealing. On the corporate side, H.B. Fuller’s January 2025 financial outlook announced strategic investments in high-performance medical adhesives, including topical skin adhesives and device assembly solutions.

Emerging Trends and Strategic Opportunities in the Global Medical Device Adhesives Market

Accelerated Development of Biocompatible, Breathable, and Skin-Friendly Hydrogel Adhesives

The medical device adhesives market is witnessing a significant shift towards advanced hydrogel formulations, moving beyond traditional acrylic and silicone adhesives. These next-generation hydrogels provide superior skin compatibility, moisture vapor transmission, and long-term adhesion, which is crucial for wearable devices such as continuous glucose monitors (CGMs) and cardiac patches. Products like P-DERM® Hydrogel adhesives allow extended wear of up to 7 days, absorb skin moisture, and are removed cleanly without residue, significantly improving patient comfort and compliance. Hydrogels maintain adhesion in challenging environments, including high humidity and perspiration, overcoming limitations of conventional adhesives. Their structural similarity to natural tissue and extracellular matrix mimicry facilitates tissue ingrowth, aiding in wound healing and tissue repair, as highlighted in Biomaterials Science. Furthermore, tough hydrogel adhesives developed by Harvard’s Wyss Institute provide three times stronger adhesion than traditional adhesives while stretching up to 20 times their original length, ensuring reliability for dynamic tissue applications. The combination of high adhesion, flexibility, and biocompatibility positions hydrogel adhesives as a cornerstone innovation for next-generation medical devices.

Adoption of Light-Cure and Instant-Bonding Cyanoacrylate Adhesives for Miniaturized and Assembly-Sensitive Devices

The demand for miniaturized, single-use, and complex medical devices is driving the adoption of light-cure (UV/LED) and instant-bonding cyanoacrylate adhesives. These adhesives enable ultra-fast curing, often in seconds, supporting high-speed automated assembly for devices such as syringes, catheters, and microfluidic chips. For example, Loctite 4310 offers curing in less than 10 seconds with visible light and under 5 seconds with UV, allowing seamless integration into production lines. Precision bonding is critical for miniaturized components, and companies like DELO Adhesives provide solutions compatible with plastics, silicones, metals, and glass. Another key advantage is resistance to sterilization, ensuring that adhesives maintain bond integrity under autoclaving, gamma radiation, or ethylene oxide processes. The combination of rapid curing, precision, and sterilization stability makes light-cure and CA adhesives indispensable for next-generation medical device manufacturing.

Development of Bio-Absorbable and Removable Adhesives for Temporary Implants and Wound Closure

There is a growing market opportunity for bio-absorbable and removable adhesives designed for temporary medical applications such as wound closure, sutureless procedures, and biodegradable implant fixation. These adhesives offer less invasive alternatives to sutures and staples, reducing scarring and patient discomfort, as reported in MDPI. Advances in tunable degradation adhesives allow materials to safely dissolve or be absorbed by the body over time, supporting tissue regeneration without the need for secondary procedures. Such innovations are particularly relevant in wet or internal environments and are poised to transform temporary fixation and wound management strategies in clinical practice.

Integration of Smart and Functional Adhesives with Drug Delivery or Sensing Capabilities

Medical device adhesives are evolving from passive bonding agents to active functional components. Drug-delivering bioadhesives utilize nanoparticles for targeted transdermal delivery, improving retention and penetration, as highlighted in PMC publications. Bio-sensing adhesives can respond to physiological stimuli such as pH or temperature, enabling early detection of infections or tissue conditions. Additionally, conductive adhesives for wearable biosensors, like ECG electrodes, ensure accurate signal transmission and reliable performance, as demonstrated by DELO Adhesives. The integration of these smart functionalities into adhesives creates multi-purpose solutions, enhancing device performance, patient outcomes, and diagnostic capabilities in the growing field of wearable medical technology.

Competitive Landscape: Leading Players in Medical Device Adhesives

The medical device adhesives market is characterized by strong competition among global players focused on biocompatibility, sustainability, and innovation in wearable and minimally invasive applications. Companies are advancing LED- and light-curable technologies, expanding portfolios for skin-friendly adhesives, and leveraging expertise in polymer chemistry to meet evolving medical standards.

Henkel AG & Co. KGaA: Pioneering LED-Curing Adhesive Solutions

Henkel, through its LOCTITE brand, is a leader in biocompatible medical adhesives, offering cyanoacrylates, epoxies, and light-curing acrylics. In March 2025, the company unveiled new LED-curing systems that reduce energy consumption and speed up assembly processes, directly addressing manufacturers’ efficiency needs. Henkel’s core strength lies in its technical expertise and ability to provide on-site support, making it a trusted partner for medical device companies seeking faster, safer, and more reliable adhesive solutions.

3M Company: Advancing Long-Wear Skin-Friendly Adhesives

3M is a global powerhouse in medical-grade adhesives, films, and tapes, with strong applications in diagnostics, wound care, and wearable devices. Its adhesives can last on skin for up to 21 days, a critical advantage for continuous glucose monitors and other health trackers. Leveraging its extensive R&D and deep knowledge of skin science, 3M designs adhesives that balance durability with patient comfort, enhancing device performance and patient compliance.

H.B. Fuller Company: Expanding Skin and Device Assembly Adhesives

H.B. Fuller is recognized for its targeted adhesive solutions, including topical skin adhesives, catheter securement, and microbial sealants. The company reaffirmed its strategic commitment to high-performance medical adhesives in January 2025, focusing on improving patient outcomes while ensuring compliance with global standards. Its strength lies in developing tailored solutions for specific medical applications, such as catheters and filters, enabling safer and more effective treatments.

Dymax Corporation: Innovating Hybrid Light-Curable Adhesives

Dymax stands out for its light-curable adhesives designed for fast, eco-friendly assembly of medical devices like prefilled syringes and drug delivery systems. In June 2025, it launched the Hybrid Light-Curable (HLC) adhesive platform, with HLC-M-1000 enabling bonding of opaque substrates, solving a long-standing challenge in device assembly. Known for its solvent-free, one-part formulations, Dymax supports manufacturers with productivity-enhancing and sterilization-resistant adhesives.

Arkema S.A.: Materials Science Leadership in Medical Adhesives

Arkema, through its Bostik subsidiary, plays a pivotal role in medical adhesives with solutions spanning device assembly, PPE, and disposable healthcare products. In July 2025, Arkema’s scientific team earned the Heroes of Chemistry Award, showcasing its R&D strength in fluoropolymer adhesives. The company emphasizes bio-based and sustainable raw materials, aligning with healthcare’s shift toward greener supply chains. Arkema’s diversified portfolio and expertise in specialty polymers ensure it remains highly competitive across global markets.

Medical Device Adhesives Market Share Insights

Synthetic and Semi-Synthetic Adhesives Dominate Market Share by Resin Type in the Medical Device Adhesives Industry

Synthetic and semi-synthetic adhesives command an overwhelming 92% of the medical device adhesives market, reflecting their engineered performance, reliability, and scalability across diverse device categories. This dominance is rooted in the flexibility of chemistries such as cyanoacrylates, silicones, acrylics, epoxies, and polyurethanes, each tailored to deliver specific performance attributes like sterilization resistance, fast curing, flexibility, and chemical durability. These materials meet the stringent ISO 10993 biocompatibility standards, making them indispensable in applications ranging from invasive implants to wearable devices. The ability of synthetic adhesives to withstand sterilization processes such as gamma irradiation, ethylene oxide, and autoclaving ensures device integrity and patient safety over long product lifecycles. Furthermore, the miniaturization of medical devices, the rapid adoption of wearable health technologies, and the expansion of advanced wound care solutions are directly reinforcing demand for these high-performance adhesives. Their unmatched adaptability and regulatory reliability explain why synthetic systems remain the uncontested backbone of this high-value market.

Medical Device Assembly Holds the Largest Market Share by Application in Medical Device Adhesives

Medical device assembly accounts for 40% of the medical device adhesives market, highlighting its central role in the structural integrity of modern healthcare technologies. This segment includes bonding in catheters, IV sets, diagnostic equipment, implantable devices, and surgical instruments, where adhesives replace traditional fasteners to enable miniaturization and reduce manufacturing complexity. The growth of this segment is directly tied to the increasing sophistication of medical devices, integration of electronic components, and demand for minimally invasive technologies, all of which require precise and durable bonding solutions. Adhesives used in device assembly must withstand sterilization cycles, mechanical stresses, and long-term biocompatibility tests, making their engineering a mission-critical function. Additionally, the shift towards disposable and single-use devices in infection control is fueling higher adhesive volumes across hospitals and outpatient care centers. As the global medical device sector expands with aging populations and rising chronic disease prevalence, assembly-related adhesive demand continues to anchor the market’s largest and most stable revenue stream.

United States Medical Device Adhesives Market Expands with FDA Regulations and Smart Biocompatible Solutions

The U.S. medical device adhesives market is driven by strict FDA regulations, including the 2023 guidance on tissue adhesives for topical skin approximation, which mandates testing for tensile strength, peel adhesion, and material purity. The rise of wearable devices has accelerated the demand for biocompatible, skin-friendly adhesives, with companies like 3M and Henkel developing low-trauma adhesives for continuous glucose monitors and ECG patches.

Corporate investments, such as H.B. Fuller’s acquisition of GEM & Medifill in 2024, reflect strategic expansion in high-performance medical adhesives. Key applications focus on minimally invasive procedures and single-use medical devices, including catheters, endoscopes, and surgical instruments, where strong, reliable, and biocompatible bonding is critical. The U.S. also leads in R&D for light-cure and UV-curable adhesives, supporting faster processing for high-volume medical device assembly, making it a global hub for innovative adhesive solutions.

Germany Medical Device Adhesives Market Benefits from MDR Compliance and Sustainable Innovation

Germany’s medical device adhesives market operates under the EU Medical Device Regulation (MDR) 2017/745, which emphasizes device traceability through UDI systems and impacts adhesive selection in medical device assembly. German manufacturers are advancing high-performance, fast-curing adhesives, such as Henkel’s January 2025 light-cure products for flexible medical devices and challenging substrates like TPE.

Sustainability and the circular economy are influencing adhesive innovation, with growing interest in solvent-free and water-based adhesives to meet low-VOC requirements. Key applications include surgical adhesives, implants, and diagnostics, supported by Germany’s robust healthcare and medical technology sectors, which drive demand for advanced, environmentally conscious adhesive solutions.

China Medical Device Adhesives Market Strengthens with Government Support and Domestic Manufacturing

China’s medical device adhesives market is propelled by governmental initiatives aimed at advancing the high-end medical device sector, including a 10-measure plan released in mid-2025 to simplify approval processes and standardize new technologies. Regulatory reforms by the NMPA, particularly the draft Medical Device Administrative Law (MDAL) in September 2024, could streamline foreign market entry by removing prior country-of-origin approvals.

Technological advancements focus on automation, AI integration, and high-quality adhesive production for domestic devices. The market is driven by China’s rapidly growing healthcare sector, with applications spanning dental adhesives, surgical sealants, and medical equipment assembly, emphasizing high-performance and internationally compliant adhesives.

India Medical Device Adhesives Market Expands under Make in India and National Medical Devices Policy

India’s medical device adhesives sector benefits from the Make in India initiative and the National Medical Devices Policy 2023, promoting domestic manufacturing and reducing import dependence. Regulatory oversight by the CDSCO, under the Medical Devices Rules 2017, implements a risk-based framework tailored to device-specific requirements, enhancing safety and compliance.

Advanced adhesive adoption is increasing, particularly in dental and surgical applications, fueled by the country’s expanding healthcare infrastructure. Corporate investments, supported by medical device parks like AMTZ, enhance production and R&D capabilities. Rising local demand and supportive government policies are accelerating the adoption of high-performance, biocompatible adhesives for both domestic and export markets.

Japan Medical Device Adhesives Market Advances with Precision Manufacturing and Specialty Solutions

Japan’s medical device adhesives industry leverages its global leadership in precision manufacturing to deliver high-performance and reliable adhesives. The PMDA enforces strict labeling, quality, and safety standards, driving innovation to meet the needs of an aging population and advanced medical devices.

The market is focused on specialty and value-added adhesives for single-use devices, enabling fast-curing, reliable bonding in high-volume automated assembly. Demand is rising for surgical and dental adhesives, including suture alternatives that accelerate healing and reduce scarring, positioning Japan as a hub for innovative, high-quality medical adhesive solutions.

Medical Device Adhesives Market Report Scope

Medical Device Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2034)

|

$6.7 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Resin Type (Synthetic & Semi-Synthetic Adhesives, Natural Adhesives), By Technology (Water-based, Solvent-based, Hot-melt, Reactive & Others), By Application (Medical Device Assembly, Wound Care, Dental, Surgical, Wearable Devices)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Henkel AG & Co. KGaA, H.B. Fuller Company, Dymax Corporation, Ethicon (Johnson & Johnson), Dentsply Sirona, Panacol-Elosol GmbH, Master Bond Inc., Permabond LLC, B. Braun Melsungen AG, Ashland Inc., Scapa Group Plc, Adhezion Biomedical LLC, Cohera Medical, Inc., Novachem Corporation Ltd

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Device Adhesives Market Segmentation

By Resin Type

- Synthetic & Semi-Synthetic Adhesives

- Natural Adhesives

By Technology

- Water-based

- Solvent-based

- Hot-melt

- Reactive & Others

By Application

- Medical Device Assembly

- Wound Care

- Dental

- Surgical

- Wearable Devices

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Device Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Dymax Corporation

- Ethicon (Johnson & Johnson)

- Dentsply Sirona

- Panacol-Elosol GmbH

- Master Bond Inc.

- Permabond LLC

- B. Braun Melsungen AG

- Ashland Inc.

- Scapa Group Plc

- Adhezion Biomedical LLC

- Cohera Medical, Inc.

- Novachem Corporation Ltd

* List Not Exhaustive

Methodology

The research methodology for the global Medical Device Adhesives market integrates both primary and secondary research techniques to deliver accurate, data-driven insights for industry professionals. Primary research included interviews with medical device manufacturers, adhesive suppliers, regulatory experts, and R&D specialists to understand emerging trends in biocompatible, hydrogel, and light-curable adhesives, as well as evolving applications in minimally invasive surgeries and wearable devices. Secondary research encompassed comprehensive analysis of company reports, FDA, PMDA, and EU MDR guidelines, scientific publications, press releases, and industry databases to validate product innovations, regulatory compliance, and market developments. Market sizing, growth projections, and segment performance by resin type, technology, and application were determined using a combination of top-down and bottom-up approaches. Key focus areas included biocompatibility standards, adhesive performance under sterilization, wearable device integration, and sustainable material adoption. This methodology ensures that USDAnalytics provides a holistic view of the medical device adhesives market, highlighting growth drivers, technological advancements, strategic opportunities, and regional dynamics shaping the industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.