Medical Device Packaging Market Overview: Size, Growth, and Industry Insights

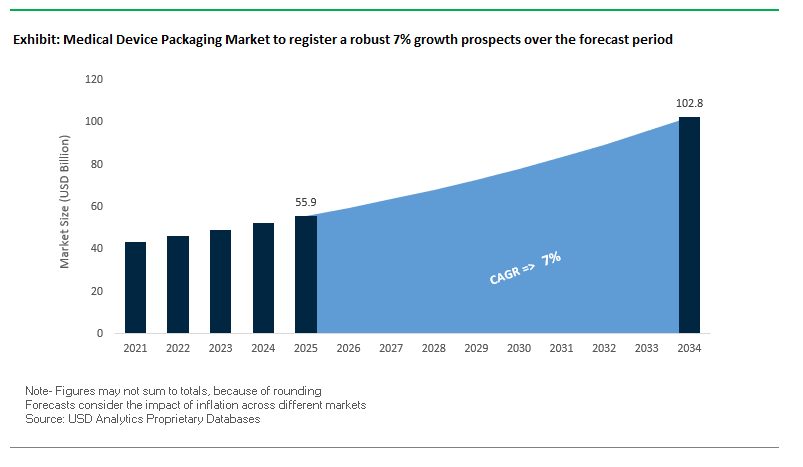

The global medical device packaging market is projected to reach $55.9 billion in 2025 and expand to $102.8 billion by 2034, reflecting a CAGR of 7% over the forecast period. This strong growth is driven by the rising adoption of single-use and minimally invasive devices, stricter regulatory requirements for sterility, and advancements in sustainable and smart packaging technologies. Packaging is no longer viewed as a passive container—it is now a critical enabler of product safety, patient trust, and supply chain resilience. Industry professionals are closely evaluating solutions that balance compliance, performance, and sustainability while adapting to global demand growth, especially in emerging markets.

Key Insights for Industry Professionals:

- Sterile packaging as a growth driver: Essential for protecting single-use and implantable devices.

- Sustainability shift: Surge in recyclable and paper-based medical packaging aligning with ESG goals.

- Product security: Rising demand for tamper-evident and child-resistant features to ensure patient safety.

- Smart technologies: Increasing integration of RFID tags, sensors, and QR codes for authenticity and supply chain visibility.

- Regional growth: Asia-Pacific and emerging markets are witnessing accelerated facility expansions by global leaders.

Market Analysis: Recent Developments Shaping the Medical Device Packaging Industry

The medical device packaging industry is in a period of accelerated transformation, with regulatory approvals, sustainability breakthroughs, and digital integration reshaping the competitive landscape. In August 2025, Paris-based TISSIUM received FDA Investigational Device Exemption (IDE) approval for its vascular sealant polymer, which also functions as a 3D printing resin for implantable devices. This development underscores how advances in biomaterials and 3D printing will intensify demand for sterile, high-performance packaging. That same month, industry reports highlighted that FDA approvals, sustainability-driven material innovations, and biomaterial-packaging convergence are defining the next wave of growth.

Strategic acquisitions and facility expansions are also steering the industry’s trajectory. In July 2025, Aptar Pharma expanded its clinical trial packaging capabilities through a strategic materials acquisition, reinforcing its integrated approach to drug delivery systems. In May 2025, Oliver Healthcare Packaging launched its largest Asia-Pacific manufacturing facility in Johor, Malaysia, boosting its capacity to serve growing pharmaceutical and device demand in the region. Similarly, April 2025 saw Amcor complete a state-of-the-art coating facility in Selangor, Malaysia, using air knife technology to advance sterile barrier substrate production. In the same month, Integer’s acquisition of Precision Coating strengthened its advanced coating technology offerings, directly influencing packaging durability and compatibility with high-performance medical devices.

Mergers and regulatory approvals are further consolidating industry power. In March 2025, DS Smith and Mondi Group secured merger approval, creating a new packaging giant with expanded global reach. Meanwhile, specialized drug formats are influencing packaging design, as seen in January 2025 when Eisai Co. Ltd. received FDA approval for its subcutaneous injection for early Alzheimer’s disease, driving demand for packaging solutions tailored to stability and patient-friendly delivery.

Transformative Trends and Emerging Opportunities in the Medical Device Packaging Market

Strategic Corporate Investment in U.S.-Based Sustainable Packaging Manufacturing

The medical device packaging market is undergoing a significant transformation driven by sustainability and domestic manufacturing initiatives. Major players are making substantial capital investments to expand production of sustainable packaging materials within the United States, aligning with regulatory shifts and growing demand for environmentally responsible solutions. DuPont, for instance, leverages its U.S. manufacturing footprint to provide medical-grade Tyvek® with Renewable Attribution, sourcing 100% of electricity from renewable energy certificates (DuPont 2024 Sustainability Report). Similarly, Oliver Healthcare Packaging announced a new facility in Costa Rica, complementing its existing U.S. plants, strengthening regional supply chains and mitigating risks from single-source dependence. The broader pharmaceutical industry is also reshoring production, with companies like Eli Lilly and Novo Nordisk investing billions to expand U.S. facilities, indirectly driving demand for domestic medical packaging. Beyond energy and production, firms are implementing circular economy strategies, such as mass balance approaches using certified renewable raw materials, which reduce reliance on fossil fuels while maintaining product performance—offering “drop-in” solutions for device manufacturers.

Integration of Advanced Supply Chain Technology for Regulatory Compliance

Regulatory mandates and the fight against counterfeit medical products are propelling the integration of smart technologies in medical device packaging. Compliance with the European MDR and U.S. UDI system requires unique identifiers on each package, typically a 2D data matrix code, to ensure traceability. Coupled with the DSCSA, these requirements drive packaging companies to implement secure serialization using GTINs and unique serial numbers, creating a verifiable digital trail from manufacturer to patient (GS1 US). Advanced printing, vision systems, RFID, and NFC integration support automated data capture, reducing human error while improving operational efficiency. Real-time monitoring of location, temperature, and tampering becomes critical for high-value or temperature-sensitive devices, offering manufacturers end-to-end supply chain visibility and enhanced patient safety.

Development of Packaging for Novel Cell and Gene Therapies

The emergence of advanced therapeutic medicinal products (ATMPs) presents a compelling opportunity for specialized ultra-cold chain packaging solutions. Cell and gene therapies often require storage below -130°C, posing challenges for traditional packaging, which may become brittle and compromise container closure integrity (CCI). Innovative materials like Daikyo Crystal Zenith vials offer inert, break-resistant solutions suitable for cryogenic conditions (West Pharmaceutical Services whitepaper). Packaging for these high-value therapies must also withstand multiple freeze-thaw cycles, prevent contamination, and ensure sterile closed systems, aligning with EMA guidelines. Hermetically sealed cryovials, for example, provide a robust alternative to traditional cryo-bags, safeguarding product integrity and patient safety for doses worth hundreds of thousands of dollars.

Standardization of Packaging for At-Home Healthcare Delivery

The shift toward hospital-at-home and ambulatory care necessitates packaging that is patient-safe, intuitive, and sterile. Packaging must be easy to open, clearly labeled, and durable enough to maintain sterility in uncontrolled environments (Medical Packaging Inc.). There is a growing opportunity to integrate patient education features such as step-by-step instructions, pictorial guides, QR codes linking to videos, and tamper-evident or color-coded components, ensuring proper device use. Additionally, sustainable materials, including paper-based solutions and single-material flexible pouches, are increasingly being adopted to facilitate residential recycling while maintaining performance and safety standards. This convergence of usability, sterility, and sustainability positions medical packaging as a critical enabler of at-home healthcare innovation.

Competitive Landscape: Leading Companies in the Medical Device Packaging Market

The medical device packaging market is highly competitive, with global leaders differentiating through innovation, sustainability, and regional expansions. Companies are investing heavily in advanced technologies, eco-friendly solutions, and integrated services to secure their market share in a regulatory-intensive and quality-driven industry.

Amcor plc: Driving Sustainable Innovation in Flexible and Rigid Packaging

Amcor is a dominant player in flexible and rigid healthcare packaging, offering blister packs, pouches, and bags designed for sterility and compliance. In April 2025, it completed its advanced coating facility in Selangor, Malaysia, using air knife technology—a first in Asia for sterile medical packaging. With its AmPrima recyclable solutions, Amcor demonstrates leadership in sustainability while targeting full recyclability by 2025. The company’s Malaysia expansion strengthens its foothold in Asia and aligns with its long-term growth strategy in high-demand regions.

Gerresheimer AG: Expanding High-Value Packaging for Biologic Drugs

Gerresheimer specializes in glass and plastic packaging, producing vials, ampoules, syringes, and cartridges for injectable medicines. Its Gx Elite Glass vials are known for superior strength and quality, while its ready-to-fill syringes simplify pharmaceutical operations. Focused on biologics, Gerresheimer is scaling capacity for injectable solutions, including expansions at its Wertheim facility. Its Gx Biological Solutions unit further enhances offerings for biotech clients, positioning Gerresheimer as a leader in packaging tailored to next-generation therapeutics.

West Pharmaceutical Services, Inc.: Innovating Wearable and Injectable Packaging Systems

West is a global leader in containment and delivery systems for injectable medicines, offering stoppers, seals, syringe components, and self-injection devices. The company’s SmartDose 10 mL platform, a wearable injector, highlights its focus on self-administered and large-volume drug delivery. With expertise in polymers like Daikyo Crystal Zenith, West provides advanced alternatives to glass for sensitive biologics. Its Integrated Solutions Program combines packaging, testing, and regulatory support, enabling clients to accelerate product launches with safe and reliable packaging systems.

AptarGroup, Inc.: Strengthening Drug Delivery and Digital Health Packaging

Aptar is a leader in dispensing and drug delivery systems across injectables, respiratory, and nasal applications. In July 2025, it acquired a strategic materials manufacturer to enhance clinical trial packaging, reinforcing its position in integrated development support. Aptar’s portfolio includes inhaler valves, nasal spray pumps, and smart inhalers that bridge packaging with digital health. Its strategy prioritizes sustainability and patient-centered design, making it a preferred partner for pharma companies seeking both innovation and usability.

Oliver Healthcare Packaging: Expanding Sterile Barrier Packaging Capabilities in Asia

Oliver Healthcare Packaging is recognized for its sterile barrier flexible packaging, including pouches, lids, and roll stock. In May 2025, it opened its largest facility in Johor, Malaysia, built to ISO 13485 standards with advanced cleanroom environments. This expansion strengthens Oliver’s ability to serve Asia-Pacific demand while ensuring global quality consistency. Its 2023 acquisition of EK-Pack Folien reinforced supply chain security and European capacity. With expertise in sterile packaging and a strong regional presence, Oliver holds a competitive advantage in meeting strict regulatory requirements worldwide.

Medical Device Packaging Market Share Insights

Pouches & Bags Dominate Market Share by Product Type in Medical Device Packaging

Pouches and bags account for 45% of the medical device packaging market, establishing themselves as the most widely used format for sterile packaging solutions. Their leadership stems from their versatility across simple and complex medical products, ranging from gauze and syringes to catheter kits and diagnostic tools. The combination of transparent medical-grade plastic films with Tyvek® lids allows breathability for sterilization while maintaining a microbial barrier until the point of use. This balance of cost-effectiveness, regulatory compliance (ISO 11607), and shipping efficiency secures their adoption by both high-volume disposable device categories and sophisticated surgical kits. As healthcare systems continue to expand single-use sterile products, pouches and bags will remain the backbone of sterile medical device packaging.

Medical Device Manufacturers Drive Market Share by End-User in Medical Device Packaging

Medical device manufacturers command 55% of demand in the medical device packaging industry, reinforcing their role as the primary decision-makers and specifiers of packaging systems. For these companies, packaging is not merely a logistics requirement but an integral part of regulatory approval, sterility assurance, and brand value. Their packaging needs span across pouches, trays, blister packs, and cartons, depending on the complexity of the device, and each design must be validated for compatibility with sterilization processes like ethylene oxide, gamma radiation, or steam sterilization. Furthermore, global players are increasingly demanding sustainable packaging solutions that reduce material usage and improve recyclability without compromising barrier integrity. As the developers of high-value surgical and diagnostic devices, manufacturers will continue to lead innovation in packaging selection, ensuring this segment maintains its commanding market share.

United States Medical Device Packaging Market Strengthened by FDA QMSR Rule and Smart Packaging Innovations

The U.S. medical device packaging market is heavily regulated under FDA standards, with the January 2024 Quality Management System Regulation (QMSR) Final Rule harmonizing U.S. regulations with ISO 13485:2016. This alignment ensures packaging design, labeling, and manufacturing meet the highest standards for sterility and integrity. Technological innovations, such as RFID tags and environmental sensors, are enabling real-time monitoring of temperature-sensitive medical devices, crucial for patient safety and product efficacy. Hydromer’s 2025 launch of PFAS-free hydrophilic coatings highlights the industry’s commitment to eco-friendly and safer materials.

Corporate investments are expanding global production capabilities. Amcor’s acquisition of a Shanghai-based medical device packaging company in February 2024 demonstrates strategic positioning to meet Asia-Pacific demand. The market sees strong application growth in home healthcare and e-commerce, particularly for devices like continuous glucose monitors and remote patient monitoring systems, which require durable, user-friendly, and sterile packaging. Sustainability remains a priority, with firms like Coveris developing recyclable thermoforming films to comply with California’s Extended Producer Responsibility (EPR) laws.

Germany Medical Device Packaging Market Drives Innovation with MDR Compliance and Circular Economy Initiatives

Germany’s medical device packaging market operates under the EU Medical Device Regulation (MDR) 2017/745, ensuring enhanced traceability through the Unique Device Identifier (UDI) system. This regulation impacts packaging design, labeling, and material selection, driving innovation in performance and compliance. Companies like Mondi are introducing plastic-free and recyclable packaging solutions, while German converters integrate oxygen-barrier labels with UDI data to maintain drug stability and regulatory compliance.

The country’s leadership in the circular economy promotes advanced, easily de-inkable, and recyclable packaging. There is also growing adoption of solvent-free and water-based adhesives to reduce environmental impact. Key applications are concentrated in surgical instruments, implants, and diagnostic devices, driven by Germany’s robust healthcare infrastructure and high-quality medical technology sector. Advanced packaging solutions are increasingly critical for patient safety, device sterility, and operational efficiency.

China Medical Device Packaging Market Expands Through Domestic Manufacturing and Regulatory Reforms

China’s medical device packaging industry benefits from government initiatives like the 10-measure plan (mid-2025), aimed at advancing high-end medical device production and streamlining approval processes for innovative packaging solutions. Regulatory reforms by the NMPA—including the draft Medical Device Administrative Law (MDAL)—could remove the requirement for foreign devices to have prior approval in their country of origin, simplifying market entry.

Technological advancements include automation, AI, and precision packaging systems to ensure compliance with sterility, safety, and international quality standards. Domestic manufacturing of high-end medical devices drives demand for advanced packaging for both disposables and complex medical equipment. The market is fueled by China’s rapidly growing healthcare sector, modernization of hospitals, and increased need for temperature-controlled and secure packaging solutions.

India Medical Device Packaging Market Bolstered by Make in India and PLI Scheme Investments

India’s medical device packaging market is supported by the Make in India initiative and the National Medical Devices Policy 2023, aimed at promoting domestic manufacturing and reducing import dependence. Regulatory updates by the CDSCO in August 2025 amended risk-based categorization for cardiovascular and neurological devices, which impacts packaging requirements.

Technological advancements focus on sterilization, barrier protection, and high-performance packaging. The Production Linked Incentive (PLI) Scheme, with an outlay of ₹3,420 crore, encourages investments in medical device parks like the Andhra Pradesh MedTech Zone (AMTZ), fostering local R&D and production. The market sees strong demand in high-value devices, driven by India’s growing healthcare infrastructure, expanding medical device adoption, and increasing focus on compliant, durable, and patient-safe packaging solutions.

Japan Medical Device Packaging Market Advances with Precision Manufacturing and Regulatory Enhancements

Japan’s medical device packaging industry thrives on precision manufacturing and advanced material technology, offering solutions with superior barrier properties and reliability. The Pharmaceuticals and Medical Devices Agency (PMDA) enforces strict labeling and quality standards, and the May 2025 amendment to the Pharmaceuticals and Medical Devices Act strengthens supply stability, directly influencing packaging logistics.

The market is witnessing a pivot toward specialty and value-added packaging solutions, especially for sensitive medical devices requiring high-volume automated assembly. Innovation focuses on surgical and dental device packaging, improving sterility, functionality, and ease of use, while supporting Japan’s position as a global leader in high-quality healthcare products and patient safety.

Brazil Medical Device Packaging Market Strengthens with UDI Implementation and Sustainable Innovations

Brazil’s medical device packaging market is advancing through the national UDI system (Siud), effective July 2025, aligning with global standards for device traceability and regulatory compliance. Technological innovation is prominent, with manufacturers developing biodegradable, recyclable, and compostable packaging to reduce environmental impact.

Corporate investments, such as Sonoco acquiring the remaining stake in its Brazilian flexible packaging joint venture in April 2022, are enhancing local manufacturing capabilities and reducing import dependence. The market is particularly strong in pharmaceuticals and medical devices, fueled by Brazil’s growing demand for packaged healthcare products, the rise of online retail, and increasing emphasis on safe, sterile, and compliant packaging solutions.

Medical Device Packaging Market Report Scope

Medical Device Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$55.9 Billion

|

|

Market Size (2034)

|

$102.8 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Material (Plastics, Paper & Paperboard, Glass, Metal), By Product Type (Pouches & Bags, Trays, Boxes & Cartons, Blister Packs, Vials & Ampoules, Others), By Application (Sterile Packaging, Non-Sterile Packaging), By End-User (Medical Device Manufacturers, Contract Manufacturing & Sterilization Organizations, Pharmaceutical & Biotechnology Companies, Hospitals & Clinics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, West Pharmaceutical Services, Inc., Gerresheimer AG, SCHOTT AG, Tekni-Plex, Inc., AptarGroup, Inc., Berry Global Inc., Oliver Healthcare Packaging, Sonoco Products Company, Huhtamaki Oyj, WestRock Company, Nelipak Healthcare Packaging, Sealed Air Corporation, SteriPack Group, CCL Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Device Packaging Market Segmentation

By Material

- Plastics

- Paper & Paperboard

- Glass

- Metal

By Product Type

- Pouches & Bags

- Trays

- Boxes & Cartons

- Blister Packs

- Vials & Ampoules

- Others

By Application

- Sterile Packaging

- Non-Sterile Packaging

By End-User

- Medical Device Manufacturers

- Contract Manufacturing & Sterilization Organizations

- Pharmaceutical & Biotechnology Companies

- Hospitals & Clinics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Device Packaging Market

- Amcor plc

- West Pharmaceutical Services, Inc.

- Gerresheimer AG

- SCHOTT AG

- Tekni-Plex, Inc.

- AptarGroup, Inc.

- Berry Global Inc.

- Oliver Healthcare Packaging

- Sonoco Products Company

- Huhtamaki Oyj

- WestRock Company

- Nelipak Healthcare Packaging

- Sealed Air Corporation

- SteriPack Group

- CCL Industries Inc.

* List Not Exhaustive

Methodology

The research methodology for the global Medical Device Packaging market leverages a comprehensive approach combining primary interviews, secondary data analysis, and advanced market modeling to deliver actionable insights for industry professionals. Primary research included discussions with packaging manufacturers, device OEMs, contract sterilization organizations, regulatory experts, and supply chain specialists to understand trends in sterile and sustainable packaging, smart technologies, and regional expansions. Secondary research analyzed company reports, FDA, EU MDR, PMDA, and NMPA regulations, industry whitepapers, press releases, and scientific publications to validate packaging innovations, material performance, and regulatory compliance. Market sizing, growth projections, and segmentation by material, product type, application, and end-user were calculated using both top-down and bottom-up approaches, accounting for factors like sterility assurance, supply chain security, patient safety, and ESG compliance. This methodology ensures that USDAnalytics provides a holistic, data-driven overview of market dynamics, technological advancements, competitive positioning, and emerging opportunities across global regions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.