Medical Device Coating Market Overview: Key Industry Statistics

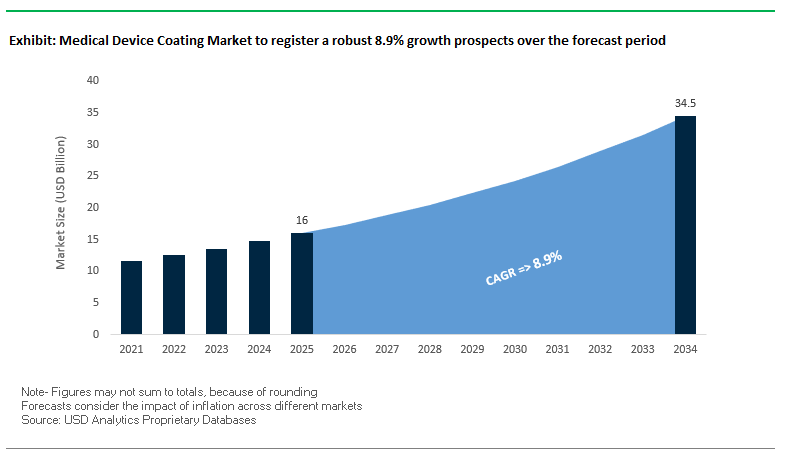

The global medical device coating market is projected to reach $16 billion in 2025 and nearly $34.5 billion by 2034, reflecting a strong CAGR of 8.9%. This growth is driven by increasing adoption of minimally invasive procedures, the rising need for antimicrobial protection, and the integration of nanotechnology in coatings. For buyers and industry professionals, the key questions center on which coating technologies ensure compliance with ISO 10993 standards, how antimicrobial coatings are reshaping infection control, and which innovations are setting benchmarks for durability and device performance.

Medical device coatings are no longer limited to providing friction reduction; they now play a central role in infection prevention, enhanced biocompatibility, and improved mechanical strength. Surgeons, device manufacturers, and hospital procurement teams increasingly rely on advanced coatings to improve device lifespan, patient outcomes, and regulatory approval success rates.

Key Insights for Industry Professionals:

- Minimally invasive procedures are accelerating demand for low-friction, high-durability coatings on surgical instruments and catheters.

- Biocompatibility testing (ISO 10993) remains a non-negotiable industry requirement, shaping material R&D pipelines.

- Antimicrobial coatings are becoming a standard in device development to combat hospital-acquired infections (HAIs).

- Nano-coatings offer unmatched performance in terms of durability, corrosion resistance, and mechanical strength without adding bulk.

Market Analysis: Recent Developments in the Medical Device Coating Industry

The medical device coating sector is experiencing a surge of innovation, with 2025 marking a pivotal year for FDA approvals, mergers, and material advancements. In August 2025, Paris-based TISSIUM received FDA Investigational Device Exemption (IDE) approval for its vascular sealant polymer, a light-activated pre-polymer with dual functionality as a 3D printing resin for implantable devices. In the same month, a report from 24ChemicalResearch highlighted how the convergence of 3D printing, biomaterials, and sustainable coatings is reshaping industry direction.

Momentum continued in July 2025, when Arkema’s adhesives business, Bostik, was honored for fluoropolymer innovation, reinforcing its commitment to high-performance solutions across healthcare. One month earlier, in June 2025, Dymax introduced its hybrid light-curable (HLC) adhesive platform, enabling rapid curing and strong bonding to opaque materials, making it highly relevant for complex device assembly. In May 2025, a report by The Business Research Company spotlighted the market’s growing shift toward fibrin natural resin coatings, prized for simplicity and superior sealing performance.

Earlier in the year, strategic moves further shaped the industry. In April 2025, Integer Holdings acquired Precision Coating, strengthening its footprint in advanced medical coatings for implantables. In March 2025, Henkel’s LOCTITE brand showcased LED-curing technologies that promise faster, greener production cycles. January 2025 brought multiple developments: H.B. Fuller announced a stronger strategic focus on high-performance medical adhesives and coatings, while the merger between DS Smith and Mondi Group gained approval, with potential implications for the packaging of coated medical devices.

Key Innovations and Growth Opportunities in the Global Medical Device Coatings Market

Strategic Shift Towards Durable, Bioactive Antimicrobial Coatings to Combat Healthcare-Associated Infections (HAIs)

The medical device coatings market is witnessing a transformative shift from traditional passive antimicrobial agents, such as silver ions, to advanced bioactive and non-eluting coatings. These next-generation coatings provide long-lasting protection against microbial colonization without contributing to antibiotic resistance, addressing a critical need in combating healthcare-associated infections (HAIs). HAIs, especially those related to cardiac implantable electronic devices (CIEDs), significantly increase patient mortality—by over threefold—and incur hospital costs averaging $55,000 per patient, according to Circulation: Arrhythmia and Electrophysiology. Advanced coatings prevent biofilm formation, a primary cause of device-related infections, using enzymatic or non-eluting mechanisms that sustainably inhibit microbial adhesion without continuous biocide release, reducing the risk of resistance. Natural and biocompatible materials like chitosan are gaining traction for surgical sutures, demonstrating superior biofilm prevention and promoting wound healing (Biomaterials Science). Additionally, collaborative initiatives such as the AMiCI project in Europe are driving the development of “safe by design” antimicrobial coatings, accelerating industry adoption of durable, effective, and patient-safe solutions.

Adoption of Hydrophilic and Lubricious Coatings for Minimally Invasive Surgical (MIS) Tools

The rapid expansion of robotic-assisted and laparoscopic surgeries is fueling demand for hydrophilic and lubricious coatings on surgical tools, including catheters, guidewires, and endoscopic instruments. These coatings absorb water to create an ultra-low-friction surface, enhancing precision in robotic procedures, as AI-assisted systems have demonstrated up to 40% improvement in surgical accuracy (PMC review). Hydrophilic coatings reduce tissue trauma and patient discomfort by providing friction levels close to natural human tissue, which is critical for safe device insertion. Advanced coating systems, combining covalently bonded basecoats and topcoats, ensure long-term durability and prevent particulate shedding (Biocoat technical bulletin). Their applications extend to interventional devices such as balloon catheters and introducer sheaths used in cardiovascular and neurovascular procedures, highlighting the market’s broad need for high-performance, low-friction coatings that improve clinical outcomes.

Development of “Smart” Drug-Eluting Coatings with Targeted Therapeutic Release

The drug-eluting coatings segment represents a high-value opportunity for precision therapeutics in medical devices. Coatings that deliver controlled doses of anti-proliferative drugs, growth factors, or anti-inflammatory agents directly to the implant site can improve efficacy while reducing systemic side effects. For instance, orthopedic implants coated with antibiotics demonstrated 100% infection prevention in preclinical mouse studies and were fully absorbed in 20 days, eliminating reliance on systemic antibiotics (Duke University & UCLA). Controlled-release technologies enable precise delivery for applications like drug-eluting stents, reducing restenosis, and potentially eliminating the need for complex two-stage orthopedic surgeries. Polymer and ceramic coatings allow fine-tuning of release profiles, enhancing the therapeutic value and safety of implantable devices.

Expansion of Coatings for Complex, High-Value Biologics and Cell-Based Therapies

The rise of cell therapies, biologics, and regenerative medicine presents a critical frontier for specialized coatings. These coatings prevent protein denaturation, maintain sterility, and provide bioactive surfaces supporting cell viability and proliferation in implants and storage vessels. Non-fouling polymers such as polyethylene glycol (PEG) reduce protein adsorption, preserving biologic activity (MDPI review). Coatings integrating extracellular matrix proteins like collagen and fibronectin create optimal microenvironments for stem cell culture, facilitating tissue engineering and regenerative applications (Corning Life Sciences). Furthermore, functional hydrogel coatings loaded with growth factors or bioactive molecules promote cell proliferation and scaffold integration, enabling advanced regenerative therapies and next-generation biomedical applications.

Competitive Landscape: Leading Companies in the Medical Device Coating Industry

The medical device coating market is shaped by a mix of global material science leaders, niche innovators, and contract manufacturers offering specialized solutions. Competition is increasingly driven by biocompatibility, antimicrobial innovation, and nano-coating technologies, alongside strategic acquisitions to expand market reach. Below is an in-depth look at leading players:

PPG Industries: Expanding Medical Coatings Through Materials Science

PPG Industries offers a comprehensive portfolio of coatings for surgical tools, implants, and device components, with a strong focus on biocompatibility and performance. The company invests heavily in sustainable, high-performance technologies, leveraging its global scale and deep R&D expertise. Its strength lies in its broad material science knowledge and long-standing relationships with device manufacturers, giving it a competitive edge in durability and functionality-driven coatings.

Henkel AG & Co. KGaA: Driving Growth with LOCTITE Biocompatible Coatings

Through its LOCTITE brand, Henkel delivers light-curing acrylics and epoxies designed to meet ISO 10993 standards. Recent innovations include LED-curing systems that accelerate assembly processes while lowering energy consumption. Henkel’s technical expertise and customer training programs enable device manufacturers to adopt optimized assembly and coating solutions. Its strategy is anchored in sustainability and high-performance coatings tailored for next-gen smart medical devices.

Surmodics, Inc.: Leading in Hydrophilic Coating Technologies

Surmodics is a recognized leader in surface modification technologies, with a strong focus on hydrophilic coatings that reduce friction and enhance catheter performance. The launch of Preside Medical Device Coating Technology has reinforced its position in the market by improving lubricity and durability. Its strategy centers on leveraging proprietary chemistry to enhance patient outcomes, while its deep expertise in coatings for complex medical devices makes it a key partner for manufacturers.

Harland Medical Systems, Inc.: Integrated Coating Equipment and Services

Harland Medical Systems specializes in providing coating equipment and turnkey services for manufacturers. Its offerings include antimicrobial, hydrophobic, and hydrophilic coatings, backed by systems like the CTS1100 Coating Thickness Testing System. Expanding globally, Harland opened a European HQ in Ireland (April 2022) to provide localized expertise. Its strength lies in integrated, scalable solutions that help manufacturers accelerate time-to-market while ensuring consistent coating quality.

Biocoat, Incorporated: Biomaterial Coatings with Full-Service Solutions

Biocoat focuses on hydrophilic biomaterial coatings for medical devices, known for their lubricity, abrasion resistance, and biocompatibility. Through acquisitions like Chempilots, Biocoat has expanded its R&D and manufacturing capabilities. Its EMERSE dip-coating equipment allows manufacturers to bring coating processes in-house, a rare full-service model that combines both coating materials and application equipment, enhancing its competitive positioning.

Specialty Coating Systems (SCS): Pioneering Parylene Coating Solutions

SCS is a leader in Parylene conformal coatings, offering superior barrier properties, biocompatibility, and chemical resistance. The company invests in R&D for next-generation coating technologies and provides end-to-end services, from design to production. With multiple ISO 9001-certified facilities, SCS is known for quality control and consistency, making it a trusted partner for device manufacturers requiring high-reliability coatings in surgical and implantable devices.

Medical Device Coating Market Share Insights

Hydrophilic Coatings Lead Market Share by Type in the Medical Device Coating Industry

Hydrophilic coatings hold the largest share of the medical device coating industry, accounting for around 30% of the market, owing to their critical role in enabling minimally invasive procedures. These coatings reduce surface friction during insertion of catheters, guidewires, and introducer sheaths, which directly improves patient comfort, procedural safety, and clinical outcomes. Their dominance is further supported by the rising global burden of cardiovascular disease, the increasing use of urinary catheters in aging populations, and the wider adoption of interventional neurology and urology procedures. Meanwhile, antimicrobial and drug-eluting coatings are growing segments but remain secondary, reinforcing hydrophilic solutions as the core technology standard across high-volume device categories. The ability of these coatings to bridge clinical efficiency with regulatory compliance secures their place as the market’s most indispensable coating type.

Cardiovascular Devices Dominate Market Share by Application in Medical Device Coatings

The cardiovascular segment represents 35% of the medical device coatings market, making it the single largest application category. This dominance is explained by the sheer number of coated devices used in cardiovascular care, including drug-eluting stents, pacemaker leads, vascular grafts, angioplasty catheters, and guidewires. Coatings here must deliver multiple performance benefits simultaneously—lubricity, anti-thrombogenic properties, and in some cases drug delivery—making them highly specialized and high-value. The increasing shift from open-heart surgeries to catheter-based, minimally invasive interventions is directly driving demand for advanced coating solutions. With cardiovascular disease remaining the leading cause of global mortality, coatings in this segment will continue to define innovation priorities and capture the largest market share.

United States Medical Device Coatings Market Accelerates with FDA Approvals and Nanotechnology Innovations

The U.S. medical device coatings market is heavily influenced by FDA regulations, exemplified by the 2024 De Novo approval for Onkos Surgical's antibacterial coated implants, which sets a clear regulatory pathway for antimicrobial and biocompatible coatings. Technological advancements in nanotechnology-based coatings and drug-eluting formulations are revolutionizing implantable medical devices, reducing inflammation and supporting tissue regeneration. Collaborative innovations, such as the DSM Biomedical and Castor partnership to develop lubricious catheter coatings, are enhancing patient comfort and device performance.

Corporate investments, including VitaTek’s strategic agreement with Chamfr in January 2025, are facilitating the global rollout of VitaCoat hydrophilic coatings, accelerating accessibility for OEMs. High demand is concentrated in cardiovascular, orthopedic, and neurology applications, particularly in minimally invasive procedures requiring coatings that enhance device longevity and functionality. The industry is also embracing eco-friendly, PFAS-free coatings, with Hydromer launching new environmentally responsible hydrophilic coatings in January 2025, reflecting a broader commitment to sustainable materials.

Germany Leads in Advanced Medical Device Coatings with MDR Compliance and Surface Modification Innovations

Germany’s medical device coatings industry is regulated under the EU Medical Device Regulation (MDR) 2017/745, which emphasizes enhanced traceability and stringent clinical data requirements. German companies, such as Evonik Industries, are pioneering high-performance, fast-curing coatings that enhance biocompatibility and drug delivery for implants, surgical instruments, and diagnostics.

The country’s strong focus on R&D and healthcare innovation drives advancements in surface modification technologies and novel coating application methods. Key applications are concentrated in high-value medical devices, including surgical tools, implants, and diagnostics, fueled by Germany’s aging population and demand for high-quality healthcare solutions. The integration of cutting-edge coatings ensures reliability, durability, and patient safety, positioning Germany as a global hub for premium medical device coatings.

China Medical Device Coatings Market Expands with Domestic Manufacturing and Sustainable Standards

China’s medical device coatings market benefits from governmental initiatives like Made in China 2025, which promote locally manufactured high-value medical equipment to reduce import reliance. The NMPA’s regulatory reforms are streamlining approvals for innovative devices, while the country’s dual-carbon targets are encouraging low-VOC and sustainable coatings.

Technological investments focus on automation, AI, and advanced hydrophilic coating equipment, enabling uniform application and efficient UV curing with minimal manual intervention. Companies such as jMedtech are leading innovations in precision coating technologies. The market is primarily driven by China’s expanding healthcare infrastructure, growing prevalence of chronic diseases, and the modernization of hospitals, resulting in high demand for coated cardiovascular, orthopedic, and dental devices.

India Medical Device Coatings Market Grows with Make in India and PLI Incentives

India’s medical device coatings sector is propelled by the Make in India initiative and the National Medical Devices Policy 2023, which support domestic manufacturing and reduce import dependence. Government schemes like the “Scheme for Strengthening the Medical Device Industry” provide financial support for common facilities and skill development, encouraging innovation in coatings.

Advanced coatings, particularly antimicrobial and hydrophilic solutions, are seeing increased adoption. Abbott’s launch of a drug-eluting coronary stent system in May 2024 exemplifies the move toward sophisticated coated implants. Corporate investments are further strengthened by the Production Linked Incentive (PLI) Scheme, allocating ₹3,420 crore to encourage domestic and foreign MedTech manufacturing. High demand exists in dental, orthopedic, and cardiovascular sectors, driven by India’s expanding healthcare infrastructure and the rising need for high-quality, reliable medical device coatings.

Medical Device Coating Market Report Scope

Medical Device Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16 Billion

|

|

Market Size (2034)

|

$34.5 Billion

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Type (Hydrophilic Coatings, Hydrophobic Coatings, Antimicrobial Coatings, Anti-thrombogenic Coatings, Drug-Eluting Coatings, Other Coatings), By Material (Polymers, Metals, Ceramics, Composites), By Device Type (Catheters, Stents, Surgical Instruments, Implants, Guidewires, Others), By Application (Cardiovascular, Neurology, Orthopedics, General Surgery, Dentistry, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DSM-Firmenich, SurModics, Inc., Hydromer, Inc., Biocoat Incorporated, Harland Medical Systems, Inc., Covalon Technologies Ltd., Dymax Corporation, Freudenberg Medical, Adhezion Biomedical LLC, Master Bond Inc., Nordson Corporation, Sono-Tek Corporation, Coatings2Go, Inc., Materion Corporation, VITA-ASSIST, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Device Coating Market Segmentation

By Type

- Hydrophilic Coatings

- Hydrophobic Coatings

- Antimicrobial Coatings

- Anti-thrombogenic Coatings

- Drug-Eluting Coatings

- Other Coatings

By Material

- Polymers

- Metals

- Ceramics

- Composites

By Device Type

- Catheters

- Stents

- Surgical Instruments

- Implants

- Guidewires

- Others

By Application

- Cardiovascular

- Neurology

- Orthopedics

- General Surgery

- Dentistry

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Device Coating Market

- DSM-Firmenich

- SurModics, Inc.

- Hydromer, Inc.

- Biocoat Incorporated

- Harland Medical Systems, Inc.

- Covalon Technologies Ltd.

- Dymax Corporation

- Freudenberg Medical

- Adhezion Biomedical LLC

- Master Bond Inc.

- Nordson Corporation

- Sono-Tek Corporation

- Coatings2Go, Inc.

- Materion Corporation

- VITA-ASSIST, Inc.

* List Not Exhaustive

Methodology

The research methodology for the global Medical Device Coating market is grounded in a combination of primary and secondary research strategies to provide comprehensive, accurate insights for industry professionals. Primary research included interviews with coating manufacturers, medical device OEMs, regulatory experts, and R&D specialists to understand emerging technologies, antimicrobial innovations, hydrophilic and drug-eluting coatings, and trends in minimally invasive procedures. Secondary research involved analyzing company reports, FDA, EU MDR, and NMPA regulations, scientific publications, industry whitepapers, and press releases to validate technological developments, material performance, and regulatory compliance. Market sizing, growth projections, and segmentation by type, material, device, and application were derived using both top-down and bottom-up approaches, with attention to factors such as durability, biocompatibility, infection control, and patient safety. This methodology ensures that USDAnalytics delivers a holistic, data-driven perspective on market dynamics, competitive landscape, and emerging opportunities across global regions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.