Protective Films Market Size, Overview, and Growth Outlook (2025–2034)

Protective Films Market Poised to Reach $68.5 Billion by 2034, Driven by Self-Healing and UV-Blocking Technologies

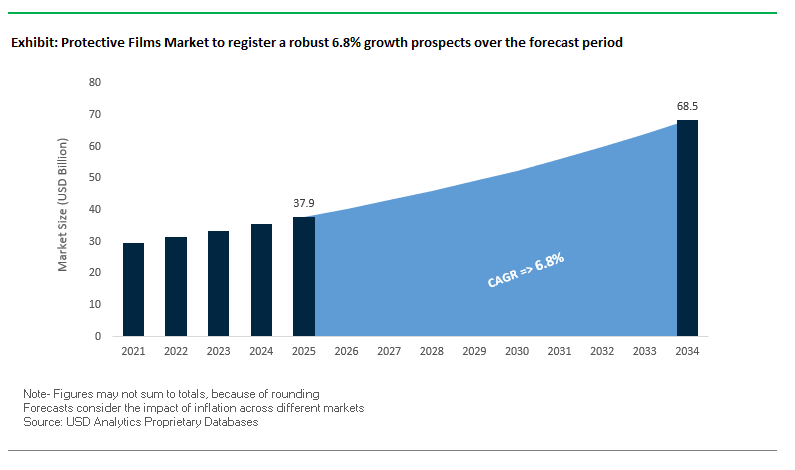

The global protective films market is projected to grow from $37.9 billion in 2025 to $68.5 billion by 2034, reflecting a CAGR of 6.8%. Protective films are increasingly recognized not only for surface protection but also for energy efficiency, aesthetic enhancement, and safety applications. Innovations such as self-healing TPU films, UV and solar rejection technologies, and anti-vandalism solutions are shaping market growth across automotive, architectural, and electronics segments.

Key Insights for industry professionals and buyers:

- Self-Healing Films Enhance Durability: Thermoplastic polyurethane (TPU) films repair minor scratches with heat exposure, extending product life and visual appeal.

- UV and Solar Rejection Drive Adoption: High-performance films block over 99% of UV rays and 80% of solar energy, reducing fading and cooling costs.

- Polyurethane is the Material of Choice: Preferred for automotive applications due to elasticity, impact resistance, and residue-free removal.

- Security and Anti-Vandalism Use Cases Expand: Films strengthen glass to prevent dangerous fragments and deter theft, serving both safety and security needs.

- Customization Trends Influence Vehicle Personalization: Emerging colored PPFs combine protection with aesthetic enhancement, reflecting consumer demand for personalization.

Market Analysis: Recent Innovations and Strategic Partnerships Are Driving High-Performance Protective Film Adoption

The protective films industry has recently seen substantial innovation in materials, coatings, and smart applications. In September 2025, XPEL, Inc. launched its COLOR Paint Protection Film (PPF) series, offering 16 vibrant colors for automotive personalization, signaling strong demand for both aesthetics and protection. Similarly, in August 2025, Luminous introduced a colored PPF to meet growing consumer expectations for vehicle customization. Concurrently, a Nano Letters study in August 2025 demonstrated inhibitor-modified ALD strategies for ultrathin, continuous films, representing a potential breakthrough in nanocoating technology for high-performance protective films.

Security, anti-vandalism, and architectural applications have also advanced. In July 2025, a leading manufacturer released an anti-graffiti film, and a U.S. university installed smart privacy films in conference rooms to enhance security and adaptability. Meanwhile, in June 2025, Covestro and PolySource formed a strategic partnership to expand polycarbonate availability in the U.S., supporting protective film manufacturing.

Architectural and aesthetic innovations are also influencing market dynamics. In April 2025, a major player launched over a hundred decorative glass finishes, responding to demand for customizable design solutions. Earlier, in November 2024, 3M introduced its Print Wrap Film IJ280, which installs up to 20% faster, improving efficiency in high-performance graphics applications.

Emerging Trends and Growth Opportunities in the Protective Films Market

Adoption of Ultra-Low Contamination and Ultra-Clean Films for High-Precision Manufacturing

The protective films market is seeing accelerated adoption of ultra-clean films specifically designed for high-precision applications such as electronics, semiconductors, and flat-panel displays. In the production of mobile phones, tablets, and advanced displays, even microscopic contamination can lead to costly product defects. Manufacturers such as BenQ Materials emphasize the development of protective films with ultra-low crystal points and exceptional cleanliness standards, ensuring a 99% residual follow-up and virtually eliminating micro-particle transfer. These films protect sensitive components during the manufacturing process without leaving residue, thereby improving yield and reducing production costs. In parallel, demand for optically clear films is rising for use in lenses, touchscreens, and other high-value optical devices. For example, 3M’s display protection films are engineered with low-tack adhesives that enable clean removal while maintaining greater than 93% light transmission with no distortion. This ensures that protective layers safeguard sensitive surfaces during production and logistics without compromising optical performance. As precision electronics manufacturing continues to expand, ultra-clean protective films are becoming a vital enabler of quality assurance and production efficiency.

Development of Sustainable and Recyclable Mono-Material Protective Films

Sustainability mandates and circular economy goals are reshaping the protective films landscape, driving the transition from multi-layer laminates to recyclable mono-material solutions. A National Institutes of Health (NIH) study highlighted that mono-material films with a 10% circulating mass can cut CO₂ emissions by over 3,600 kg per ton of plastic after just four recycling cycles, underscoring the environmental advantage of single-polymer structures. Global FMCG leaders are setting the pace—Unilever, for example, has committed to converting flexible packaging formats like pouches into polyethylene-based mono-materials, which simplifies end-of-life recycling. For protective films, this trend represents a major opportunity to align with brand owners’ sustainability goals, especially in packaging, healthcare, and electronics. Manufacturers are investing in developing recyclable polyethylene (PE) and polypropylene (PP)-based protective films that deliver durability, clarity, and functional performance while ensuring compatibility with established recycling streams. As legislation such as the EU’s Packaging and Packaging Waste Regulation (PPWR) takes effect, demand for recyclable protective films will expand, making sustainability-driven innovation a competitive differentiator in the market.

Expansion of Anti-Microbial and Self-Disinfecting Films for High-Touch Surfaces

Heightened hygiene awareness in public spaces, healthcare facilities, and transportation systems has created a strong demand for antimicrobial protective films. These films incorporate active agents like silver ions, zinc oxide, and copper compounds to provide continuous protection against bacteria and viruses. Silver Defender’s self-disinfecting film, for example, is already being deployed on elevator buttons, handrails, and door handles in commercial buildings, as highlighted in a case study from Silverstein Properties. By delivering constant antimicrobial activity, these films reduce the risk of cross-contamination in high-traffic environments. The U.S. Environmental Protection Agency (EPA) has approved several of these active agents, reinforcing safety and credibility for broader adoption. For hospitals, schools, and office complexes, antimicrobial films not only enhance user confidence but also help facilities meet stringent hygiene standards. This opportunity aligns with growing global investments in public health and wellness, ensuring long-term market relevance for self-cleaning protective films.

Integration of Smart and Functional Films with Sensing Capabilities

The evolution of protective films into multifunctional smart materials represents one of the most promising opportunities in this market. Advances in printed electronics are enabling the integration of RFID antennas, temperature sensors, and even gas-sensitive indicators directly into flexible film substrates. Witte Technology, for instance, has demonstrated that functional circuits can be printed onto films, transforming them into intelligent surfaces capable of real-time monitoring. Smart protective films can track parameters such as temperature fluctuations, pressure changes, or atmospheric composition during storage and transportation. Colorimetric indicators embedded within films can even provide visual alerts of spoilage or tampering, ensuring supply chain integrity for food, pharmaceuticals, and other sensitive goods. This innovation not only reduces losses from damage and waste but also enhances consumer confidence by providing visible proof of product safety. As logistics, healthcare, and high-value goods markets demand more traceability and transparency, smart protective films with embedded sensing technologies are poised to become a disruptive force in packaging and product monitoring.

Competitive Landscape: Top Companies Are Leveraging Advanced Materials and Innovation to Dominate the Protective Films Market

The global protective films market is led by companies focusing on self-healing technology, UV protection, and security applications, while strategically expanding their global footprint. These leaders are committed to R&D-driven innovation, sustainability, and integrated customer solutions.

3M Company: Leveraging Materials Science Expertise to Deliver Durable and Aesthetic Protective Films

3M offers a wide range of protective films for automotive paint, architectural glass, and electronics surfaces. Its 3M™ Fasara™ Glass Finishes provide on-trend designs while maintaining privacy and protection. With a network of trained installers and strong materials science expertise, 3M ensures high durability and quality. The company’s strategy emphasizes digital transformation, AI, and IoT integration to develop innovative solutions.

Eastman Chemical Company: Advancing High-Performance Films with Sustainability and Molecular Recycling

Eastman’s protective films portfolio includes LLumar® and Suntek® brands for automotive and architectural applications. The company leverages innovation platforms and molecular recycling technologies to create high-performance, sustainable films. A 2020 capacity expansion in Dresden, Germany enhanced coating and laminating capabilities, supporting growing global demand. Eastman films are valued for UV rejection, solar control, durability, and ease of installation.

Avery Dennison Corporation: Combining Science and Technology for Superior Paint and Architectural Film Solutions

Avery Dennison offers paint protection films and architectural films with advanced performance features. The Supreme™ PPF Xtreme Gloss incorporates RAPID EDGE™ technology to improve installation efficiency and self-healing. The company’s digital product cloud, atma.io, connects physical films to digital information for enhanced transparency, reflecting a strong focus on AI, IoT, and digital transformation.

LINTEC Corporation: Driving Innovation Through Integrated Adhesive and Surface Technologies

LINTEC produces a range of privacy, security, and protective films for commercial and residential applications. The company leverages four core technologies adhesive applications, surface improvement, specialty paper, and release materials—to deliver highly differentiated products. LINTEC’s strategy emphasizes technology-driven R&D and global expansion to strengthen market presence.

Saint-Gobain (Solar Gard): Combining Energy Efficiency and Safety in High-Performance Films

Saint-Gobain’s Solar Gard® brand offers SolarZone and SafetyZone films, improving energy efficiency, UV protection, and safety. Its Graffitigard® product protects surfaces from vandalism. Solar Gard is distinguished as the only window film manufacturer with carbon-negative architectural films, emphasizing sustainability and high performance across automotive and architectural markets.

XPEL, Inc.: Innovating Vehicle Protection with Color Options and Global Installer Networks

XPEL is a leader in paint protection, surface protection, and window films. In September 2025, it launched the COLOR PPF line with 16 colors for vehicle personalization. The company maintains a global installer network and proprietary DAP software for precision fitment. XPEL focuses on high-quality products, expert support, and total vehicle protection solutions, reinforcing its market leadership.

Protective Films Market Share Insights, 2025-2034

Self-Adhesive Films Dominate Market Share by Type in the Protective Films Industry

Self-adhesive films hold the majority share at 65% of the protective films industry, underscoring their versatility and ease of application across automotive, consumer electronics, appliances, and metal coil markets. Their pre-applied pressure-sensitive adhesive eliminates the need for heat or solvents, making them highly adaptable from small DIY uses, like smartphone screen protection, to large-scale industrial processes. The dominance of this segment is directly linked to the growing need for cost-effective, residue-free, and temporary protection solutions during manufacturing, shipping, and installation. Adhesive-coated films, with about 20% share, cater to high-performance industrial applications where specialized adhesion is necessary, while coextruded films, at 15%, serve sensitive surfaces where residue-free removal is critical. This segmentation demonstrates how self-adhesive films have become the global standard, while performance-driven alternatives carve out niches in specialized applications.

Automotive and Electronics Drive Market Share by End-Use in the Protective Films Industry

The automotive sector leads with 30% of protective film demand, propelled by rising adoption of paint protection films (PPF) and temporary surface shields during manufacturing and transit. Increasing investments in self-healing polyurethane films and durable protective solutions for electric vehicles reinforce this dominance. Electronics follow closely at 25%, where manufacturers rely on ultra-clear, anti-static, and residue-free films to safeguard delicate displays and high-value components during production and shipment. Construction holds around 20% share, driven by the widespread use of films to protect windows, floors, and stainless-steel surfaces in renovation projects. Packaging accounts for 15%, where barrier-enhancing protective films are integrated into flexible food and medical packaging. Niche but critical applications in aerospace and medical devices, each at 5%, demand specialized films that meet rigorous performance and regulatory standards. Collectively, these insights highlight how high-value automotive and electronics markets set the pace for innovation, while construction and packaging provide steady, high-volume demand.

United States: VOC Reduction Rules and Rise of Premium TPU Films

The U.S. protective films market is strongly shaped by regulatory oversight from the Environmental Protection Agency (EPA), which recently updated standards requiring a 20% reduction in VOC emissions from protective film production. This mandate is pushing manufacturers toward water-based and solvent-free coatings, exemplified by Toray Industries’ new PET film designed for excellent adhesion while eliminating solvent-derived CO₂ emissions. Sustainability compliance is a critical factor for companies aiming to remain competitive.

On the innovation front, the U.S. market is witnessing rapid adoption of thermoplastic polyurethane (TPU) films for applications such as paint protection films (PPF) in automotive and high-end consumer electronics. TPU’s self-healing, non-yellowing, and abrasion-resistant properties make it a premium choice in both automotive wraps and architectural glass applications. Parallel to material advances, smart films and switchable glass solutions are gaining traction in commercial and residential projects for on-demand privacy and energy savings. Meanwhile, digital UV and eco-solvent printing technologies are enabling high-definition, fade-resistant graphics, with premium cast films carving out strong growth in luxury markets.

European Union: PPWR, ESPR, and Shift Toward PVC-Free Sustainable Films

In the European Union, the protective films market is being redefined by two major regulations. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates recyclability standards and reusable material requirements, impacting films used in both packaging and industrial applications. Complementing this, the Ecodesign for Sustainable Products Regulation (ESPR) (mid-2024) establishes eco-design requirements and introduces the Digital Product Passport, which demands full transparency regarding origin, recyclability, and compliance.

Manufacturers are accelerating innovation in PVC-free protective films as sustainable alternatives to conventional vinyl. Research investments are concentrated on solvent-free and water-based adhesives to reduce carbon footprints while maintaining performance. Market consolidation is also a defining factor UPM Raflatac’s acquisition of Metamark expanded its footprint in the graphics sector and reinforced its sustainability-driven portfolio. These shifts highlight the EU’s commitment to circular economy principles, with companies aligning to regulatory and consumer demands for eco-friendly, recyclable protective films.

China: PDLC Leadership, Industrial Clusters, and Advanced Automotive Films

China is a global powerhouse in protective film production, with the government encouraging domestic innovation and industrial upgrading to reduce dependence on imports. The country has become a leading manufacturer of PDLC (Polymer Dispersed Liquid Crystal) smart films, widely adopted for switchable privacy glass in automotive and architectural applications. The transformation of industrial hubs, such as Taihu, into manufacturing bases for functional films and optical adhesives underscores China’s dominance. Companies like Jinzhang Technology command significant market share in niche segments.

The automotive aftermarket is a critical growth driver, with local firms investing heavily in new processing lines for PPF and high-performance automotive films. Large-scale automation enables cost-effective production at scale, supported by a wide variety of adhesive options (transparent, grey, black) tailored to different uses. Additionally, manufacturers are supplying films compatible with eco-solvent, solvent, and UV printing technologies, ensuring versatility across global markets. China’s ability to combine volume production, automation, and high-end innovation solidifies its role as a leader in the protective films industry.

Japan: TPU Innovation and Premium Graphics in a Highly Regulated Market

Japan’s protective films market balances stringent regulation with technological leadership. The government’s positive list for synthetic food containers and packaging, effective June 1, 2025, establishes strict guidelines for materials deemed safe, indirectly influencing protective film material choices. Regulatory oversight by the Japan Vinyl Industry Association (JVIA) further ensures adherence to high safety and quality standards.

Technologically, Japan is at the forefront of TPU-based protective films, which dominate due to their self-healing, non-yellowing, and durable properties. These films are heavily used in electronics, automotive PPF, and premium construction applications. The country’s emphasis on aesthetic quality and high-resolution graphics sustains demand for premium printable films in signage, wraps, and architectural decoration. With the ongoing shift to electric vehicles (EVs), demand for heat-resistant and durable protective tapes and films is growing, further expanding the country’s innovation-driven market.

South Korea: Electronics Manufacturing and Transparent Polyimide Driving Growth

South Korea’s protective films market is anchored by its electronics manufacturing dominance, where protective films are critical for displays, semiconductors, and precision components. Companies like SKC have pioneered innovation with PET film development and continue to supply high-performance functional films across sectors.

A key breakthrough is the transparent polyimide film, which offers flexibility to bend, twist, and replace glass in foldable displays—a game-changer for the smartphone and consumer electronics industries. Beyond electronics, polyvinyl butyral (PVB) films are gaining adoption in automotive windshields and architectural glass for safety and structural strength. Firms like Kosan Technology further expand market capabilities by coating acrylic, silicone, and urethane adhesives onto films, offering customized solutions across electronics, automotive, and construction markets. South Korea’s positioning as a technology-intensive and export-oriented hub strengthens its influence in the global protective films landscape.

India: Local Manufacturing and Rising Demand for Automotive PPF

India’s protective films market is expanding under the Make in India initiative, which encourages domestic manufacturing of printable films and specialty coatings. A significant development is Nippon Paint’s entry into India’s PPF market under the N-Shield brand, offering products engineered for local conditions with UV stability, dust resistance, and self-healing performance. While TPU base films are currently sourced from Chinese and Japanese vendors, plans for domestic production are underway, aligning with long-term self-reliance goals.

The market is also witnessing rising demand from MSMEs for cost-effective films, particularly in signage, packaging, and protective applications. Regulatory frameworks such as the India Plastics Pact—a collaboration between the Confederation of Indian Industry (CII) and WWF India—target 100% reusable or recyclable plastic packaging by 2030, driving innovation in eco-friendly protective films. As domestic and export-oriented industries scale, India is positioning itself as both a volume-driven and innovation-focused hub for protective films, particularly in automotive, retail, and construction applications.

Protective Films Market Report Scope

Protective Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.9 Billion

|

|

Market Size (2034)

|

$68.5 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Material (PE, PP, PET, PVC, PU, TPU), By Type (Adhesive-Coated Films, Self-Adhesive Films, Coextruded Films), By End-Use Industry (Automotive, Electronics, Construction, Packaging, Aerospace, Medical), By Application (Surface Protection, Component Protection, Tamper Evident, Solar Control)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Avery Dennison Corporation, Eastman Chemical Company, Nitto Denko Corporation, Saint-Gobain S.A., Gerber Technology, LLC, XPEL, Inc., Cosmo Films Ltd., Toray Industries, Inc., SKC Co., Ltd., Madico, Inc., Ritrama S.p.A. (Fedrigoni Self-Adhesives), Nan Ya Plastics Corporation, Uflex Ltd., Hexis S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Protective Films Market Segmentation

By Material

By Type

- Adhesive-Coated Films

- Self-Adhesive Films

- Coextruded Films

By End-Use Industry

- Automotive

- Electronics

- Construction

- Packaging

- Aerospace

- Medical

By Application

- Surface Protection

- Component Protection

- Tamper Evident

- Solar Control

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Protective Films Market

- 3M Company

- Avery Dennison Corporation

- Eastman Chemical Company

- Nitto Denko Corporation

- Saint-Gobain S.A.

- Gerber Technology, LLC

- XPEL, Inc.

- Cosmo Films Ltd.

- Toray Industries, Inc.

- SKC Co., Ltd.

- Madico, Inc.

- Ritrama S.p.A. (Fedrigoni Self-Adhesives)

- Nan Ya Plastics Corporation

- Uflex Ltd.

- Hexis S.A.

* List Not Exhaustive

Methodology

The research methodology for the Protective Films Market integrates both primary and secondary research approaches to deliver precise, actionable insights for industry professionals. USDAnalytics conducted in-depth interviews with key stakeholders, including protective film manufacturers, automotive and electronics OEMs, architectural and construction specialists, packaging companies, and regulatory authorities, to capture emerging trends, material innovations, and adoption patterns. Secondary research involved comprehensive analysis of company reports, investor presentations, trade journals, patents, technical white papers, and verified market databases, focusing on self-healing TPU films, UV-blocking technologies, smart films, and sustainable mono-material solutions. Market sizing, CAGR estimation, and segment-level insights were validated using top-down and bottom-up approaches, triangulating macroeconomic trends, regulatory frameworks, technological advancements, and regional adoption dynamics. Competitive benchmarking and company profiling assessed innovation pipelines, strategic partnerships, and sustainability initiatives, providing a holistic understanding of market growth drivers, technological disruption, and opportunities across automotive, electronics, construction, packaging, and healthcare applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.