Privacy Film Market Size, Overview, and Growth Outlook (2025–2034)

Privacy Film Market to Reach $4.5 Billion by 2034 Driven by Advanced UV Protection and Dynamic Privacy Solutions

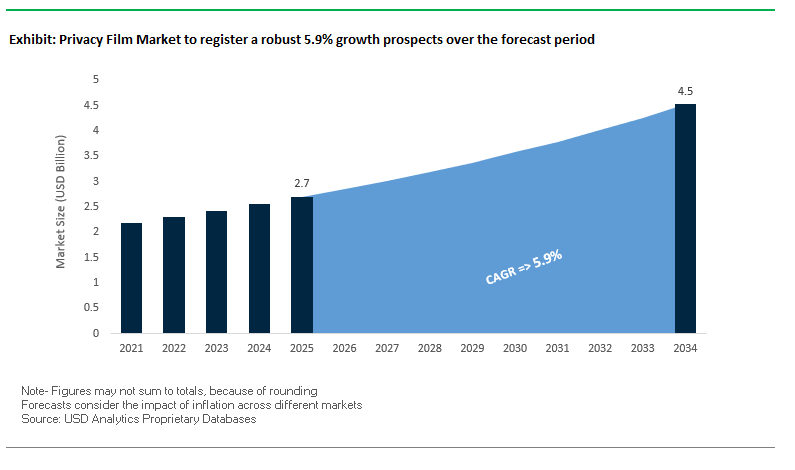

The global privacy film market is projected to grow from $2.7 billion in 2025 to $4.5 billion by 2034, at a CAGR of 5.9%. This growth is propelled by increasing demand for films that combine privacy, security, and energy efficiency. High-performance privacy films are now valued not only for visual screening but also for their ability to block over 99% of UV rays and reject more than 80% of solar energy, helping reduce interior fading and cooling costs in commercial and residential buildings.

Key Insights for industry professionals and buyers:

- UV and IR Rejection Drive Adoption: Films protect interiors while reducing energy costs.

- Security Integration Expands Applications: Safety features in privacy films prevent dangerous glass fragments.

- Decorative Privacy Films Enhance Design Flexibility: Frosted, etched, and textured films allow light diffusion while maintaining privacy.

- Dynamic and Smart Films Are Emerging: Switchable films for offices, healthcare, and conference rooms provide innovative solutions.

- Sustainability Considerations Are Rising: Materials with lower environmental impact are becoming preferred in architectural and automotive applications.

Market Analysis: Recent Innovations in Privacy Films Are Redefining Architectural and Commercial Applications

The privacy film industry has seen significant technological and design-driven innovations. In August 2025, a Nano Letters study introduced an inhibitor-modified atomic layer deposition (ALD) method for ultrathin films, potentially enhancing nanocoating formulations for high-performance privacy films. The same month, Afera highlighted European adhesive tape industry strategies for trade diversification, demonstrating supply chain resilience and raw material planning relevant to privacy film production.

Smart privacy films are gaining real-world adoption. In July 2025, a U.S. university installed smart films in conference rooms, enabling instant switching from transparent to opaque for security and privacy, signaling a growing interest in dynamic applications. Material supply strategies also evolved; in June 2025, Covestro partnered with PolySource to expand polycarbonate availability in the U.S., ensuring stable inputs for privacy film manufacturing.

Decorative and functional expansion continues to shape the market. In March 2025, a leading company launched over 100 new decorative glass finishes, meeting growing demand for customized architectural solutions. Earlier, in February 2025, Avery Dennison’s AD Stretch accelerator program partnered with startups to explore sustainability, customer experience, and value chain innovations in privacy films. Complementary advancements in high-performance graphics, such as 3M’s Print Wrap Film IJ280 (November 2024), illustrate material innovations with potential cross-applications in privacy and decorative films.

Emerging Trends and High-Value Opportunities in the Privacy Film Market

Integration of Advanced Light Directional Control for Visual Ergonomics

Privacy films are rapidly evolving from basic darkening overlays into precision-engineered solutions that enhance both security and workplace comfort. Micro-louver technology, which functions like a system of microscopic vertical blinds, is increasingly being integrated into privacy filters to direct light toward the intended user while blocking side-angle views. Lenovo’s privacy filter line highlights this advancement, demonstrating how the technology not only safeguards data but also creates a distraction-free environment by reducing peripheral visibility. At the same time, manufacturers are responding to the rising demand for ergonomic workspaces by incorporating matte finishes and anti-glare coatings into privacy films. According to a publication from the University of British Columbia’s Human Resources department, glare is a leading cause of eye strain in offices, and filters with light-diffusing properties help mitigate visual fatigue. This trend reflects a dual-purpose evolution of privacy films: protection from prying eyes and improved screen usability for modern, high-illumination office environments.

Mandated Adoption in Public Sectors for Data Protection and Compliance

Growing awareness of “visual hacking” is accelerating the mandated use of privacy films across government, finance, and enterprise sectors. A Ponemon Institute study revealed that 91% of visual hacking attempts—where confidential information is stolen simply by observing someone’s screen—were successful, often within 15 minutes. This alarming statistic positions privacy films as a frontline defense against one of the simplest yet most overlooked forms of data theft. Regulatory frameworks such as the EU’s GDPR and India’s DPDP Act, while primarily focused on digital data, have pushed organizations to embrace holistic compliance strategies that include physical safeguards. BankInfoSecurity has emphasized that preventing “shoulder surfing” in open workspaces, airports, and government offices is now considered a necessary component of enterprise-grade security. As a result, mandated rollouts of privacy films in sensitive industries are emerging as a global driver for market adoption, reinforcing their role in compliance-based procurement.

Development of Switchable Smart Films for Dynamic Privacy Control

One of the most significant opportunities lies in the commercialization of switchable smart films, particularly Polymer-Dispersed Liquid Crystal (PDLC) solutions. These films provide dynamic privacy on demand, shifting from transparent to opaque at the touch of a remote or smartphone app. A product overview from Smart Film illustrates how enterprises are deploying PDLC films in offices, conference rooms, and healthcare facilities to replace blinds or curtains, offering flexible space management while preserving aesthetics. Beyond privacy, these films deliver measurable energy efficiency by blocking solar heat in opaque mode, reducing reliance on air conditioning. Technical product data also confirms their ability to block 99% of harmful UV radiation, protecting interiors from long-term sun damage. This dual benefit—dynamic privacy and energy savings—positions switchable films as a strategic innovation for sustainable building design and modern workplace architecture.

Expansion of Anti-Bluetooth and RFID Shielding Films for Digital Privacy

As digital connectivity grows, so does the risk of electronic data theft via RFID skimming, NFC breaches, and Bluetooth exploitation. This creates an opportunity for niche but high-value privacy films that shield devices and documents from wireless intrusions. RFID Cloaked, for example, has developed specialist polymer alloy films that block a broad spectrum of radio frequencies, effectively creating a Faraday cage barrier. These films are being embedded into document holders, travel wallets, and even industrial storage solutions to prevent unauthorized scanning of credit cards, passports, or sensitive corporate data. In an era where cyber-physical attacks are on the rise, such films offer consumers and businesses an additional layer of protection against non-contact theft. Their adoption not only enhances personal and organizational security but also opens new verticals for the privacy film industry, bridging the gap between physical screen protection and digital data defense.

Competitive Landscape: Leading Privacy Film Companies Are Driving Growth Through Innovation, Sustainability, and Multi-Functional Solutions

The global privacy film market is characterized by a competitive landscape where product innovation, energy efficiency, and multi-functionality differentiate leading players. Companies focus on security, aesthetic appeal, and sustainability, offering solutions for architectural, commercial, residential, and automotive applications.

3M Company: Combining Aesthetic Design and Safety in High-Performance Privacy Films

3M’s Fasara™ Glass Finishes and Scotchshield™ Safety & Security Window Film offer privacy with UV protection and enhanced safety. The Fasara range provides frosted, gradation, and natural designs, allowing light diffusion while maintaining privacy. Widely used in offices, hotels, retail, and healthcare, 3M films leverage materials science expertise and a trained installer network to deliver quality and durability, reinforcing the company’s industry leadership.

Eastman Chemical Company: Balancing High-Performance Privacy and Solar Control Solutions

Eastman’s LLumar® and Suntek® brands serve both architectural and automotive sectors. Focused on innovation and high-value films, Eastman expanded capacity in Dresden, Germany (2020) to meet demand for UV-rejecting, glare-reducing, and durable films. Their privacy films are known for easy installation and maintenance, catering to offices, homes, and high-performance commercial applications.

LINTEC Corporation: Leveraging Technology-Driven Solutions to Expand Global Privacy Film Presence

LINTEC emphasizes technology-centered innovation, combining adhesive and surface enhancement technologies to create market-leading privacy films. Expanding sales and production bases in the U.S. and Asia, LINTEC provides films for privacy, security, and decorative applications in residential and commercial buildings, with specialty offerings for unique architectural needs.

Hanita Coatings: Delivering Energy-Efficient and Durable Privacy Films for Architectural Applications

Hanita Coatings’ SolarZone and SafetyZone films enhance energy performance while providing superior privacy. Their portfolio includes matte translucent, black-out, and white-out films, along with anti-graffiti and anti-scratch options. Focused on R&D and cutting-edge solutions, Hanita supports sustainability and protection, enabling long-term value in corporate, healthcare, and public spaces.

Madico Inc.: Ensuring Safety and Privacy with High-Performance, Multi-Functional Films

Madico offers privacy films for commercial, residential, and automotive use, combining UV rejection, solar control, and security. Known for durability and performance, their films protect against weather, vandalism, and forced entry, with a wide portfolio including decorative and solar control solutions, creating a one-stop-shop for privacy film applications.

ASWF (American Standard Window Film): Integrating Advanced Production Technology for Superior Privacy Solutions

ASWF manufactures privacy films in its Las Vegas facility, featuring innovations like a three-coating head with automated rewind system. Their Excel IRP and Carbon Ultra series provide lifetime color stability, advanced carbon technology, and non-reflective aesthetics. ASWF expands distribution across North America and Canada, ensuring efficient service and superior performance for residential, commercial, and automotive clients.

Privacy Film Market Share Insights, 2025-2034

Window Privacy Films Dominate Market Share by Type in the Privacy Film Industry

Window privacy films, including static and decorative/frosted variants, command the majority share of the privacy film industry, collectively accounting for 75% of demand. Their dominance is tied to retrofit applications in commercial offices, healthcare facilities, and residential apartments, where they provide a low-cost and non-permanent solution compared to replacing architectural glass. Static window films are favored for compliance-driven uses in conference rooms, clinics, and government buildings, while decorative and frosted films are increasingly positioned as interior design elements, enabling branded environments and customized aesthetics. Screen privacy films hold a smaller but critical share at 20%, driven by corporate data security requirements in finance, healthcare, and government operations, where visual data protection is non-negotiable. Smart switchable films, though only 5% of current demand, represent the highest-growth niche, benefiting from the shift toward smart buildings and flexible workspaces. Their adoption in corporate boardrooms, high-end residential projects, and patient care facilities demonstrates the industry’s move toward high-value, technology-integrated privacy solutions.

Commercial & Office Buildings Lead Market Share by Application in the Privacy Film Industry

Commercial and office buildings dominate the privacy film market with a commanding 55% share, reflecting the central role of these films in modernizing open-plan workspaces and glass-walled offices. Enterprises are increasingly investing in decorative and switchable films for branding, confidentiality, and regulatory compliance, positioning this segment as the backbone of industry demand. The residential sector follows at 30%, fueled by the DIY home renovation trend and rising demand for cost-effective privacy solutions in urban apartments. Automotive applications contribute 10%, where films serve both functional (UV and glare reduction) and aesthetic (tinting and styling) purposes, though adoption is shaped by regional regulations on window tinting. Consumer electronics, while holding a smaller 5% niche, is strategically important as screen privacy films become standard in ATMs, POS systems, and laptops for data security. This segmentation highlights how corporate real estate and workspace modernization anchor growth, while smart films and consumer electronics drive new high-value opportunities.

United States: Data Privacy Laws and Smart Film Adoption Driving Growth

The United States privacy film market is being shaped by a robust regulatory landscape, led by the Federal Privacy Act of 1974, HIPAA, and state-level frameworks like the California Consumer Privacy Act (CCPA). These laws ensure data protection in commercial, healthcare, and residential spaces, fueling demand for privacy films in offices, hospitals, and homes. Compliance with privacy and data protection requirements has accelerated the use of frosted, tinted, and switchable smart films that safeguard sensitive information while enhancing aesthetics.

Technology is a major trend, with innovations in electrochromic and thermochromic films that adjust tint automatically in response to light, improving energy efficiency in smart buildings. The automotive sector is also seeing rapid adoption of switchable glass films for instant privacy. The U.S. market is investing in UV-curable and eco-solvent digital printing technologies to produce high-definition, fade-resistant graphics, allowing customization for branding and décor. A notable trend is the premiumization of privacy films, with manufacturers focusing on cast films for luxury vehicles and architectural projects. Additionally, AI-powered customization software is being introduced to accelerate design workflows for tailored privacy solutions.

European Union: PPWR Regulations and Circular Economy Driving PVC-Free Films

The European Union privacy film market is being redefined by the Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which sets higher standards for recyclability and reusable materials. This regulation influences not only packaging but also self-adhesive films used in architectural and retail applications, pushing companies to invest in PVC-free alternatives. The European Green Deal and Net Zero commitments further support the adoption of films that reduce energy usage and enable sustainable building design.

Industry events like the European Tape Week 2025, hosted by the European Adhesive Tape Association (Afera), have highlighted key market drivers such as sustainable chemistries, water-based adhesives, and digital transformation. Market consolidation is also notable, with UPM Raflatac’s acquisition of Metamark expanding its graphics and film portfolio. Manufacturers are focusing on circular economy principles, creating privacy films that are durable, removable, and recyclable, ensuring compliance while aligning with consumer demand for sustainability.

China: PDLC Leadership and Large-Scale Automation Boosting Supply

China is a global leader in PDLC (Polymer Dispersed Liquid Crystal) smart film production, which is widely used for switchable glass in offices, vehicles, and public infrastructure. The government supports innovation through policies that streamline industrial upgrading and reduce reliance on imports. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) continue to tighten regulations on plastic pollution, impacting substrate and adhesive choices in privacy film manufacturing.

China’s booming e-commerce and domestic demand under the Dual Circulation strategy is increasing consumption of printable and switchable films. Regulatory changes, such as the June 2025 packaging law, are encouraging recyclable and reusable materials in film applications. The General Administration of Customs (GACC) now requires a Product Expiration Date on imported goods, influencing printing practices on privacy and branding films. Manufacturers are scaling up with automated production lines for paint protection films (PPF), printable vinyl, and automotive wraps, strengthening China’s role as a high-volume global exporter of privacy films.

India: Make in India Manufacturing and Smart Glass Film Adoption

India’s privacy film market is expanding under the Make in India initiative, which promotes domestic manufacturing of printable films and smart glass solutions. The country’s PrintPack 2025 trade show emphasized chemical-free production and green practices, highlighting a shift toward eco-friendly film manufacturing. The market demand is driven by MSMEs seeking cost-effective privacy films and by rising e-commerce and advertising, which require self-adhesive films for promotional applications.

A notable trend in India is the growing use of switchable smart glass films, particularly in conference rooms, hospitals, and retail displays, where on-demand privacy and energy efficiency are crucial. Companies like Glasstronn are showcasing innovations in smart films tailored for both commercial and residential markets. Additionally, India’s Plastic Waste Management Rules (2016, amended 2022) reinforce Extended Producer Responsibility (EPR), encouraging manufacturers to adopt recyclable substrates and biodegradable adhesives. These combined factors are positioning India as an emerging innovation and volume-driven market for privacy films.

Japan: Premium Graphics, Regulatory Oversight, and EV Adoption Expanding Use

Japan’s privacy film market emphasizes premium quality and design precision, driven by its culture of aesthetic detail and high-performance materials. The Japan Vinyl Industry Association (JVIA) and related regulatory bodies oversee safety and quality standards for vinyl products, ensuring that privacy films meet strict compliance requirements. Demand is high for printable vinyl films in signage, vehicle wraps, and architectural applications, where clarity and durability are critical.

The market is evolving with the transition toward electric vehicles (EVs), which require durable, heat-resistant films for battery protection and component safety. Manufacturers are also developing films compatible with eco-solvent and UV inkjet printing systems, catering to diverse printing needs. With its combination of advanced R&D, stringent regulations, and high consumer expectations, Japan continues to lead in premium-grade privacy and graphic films for both industrial and consumer-facing applications.

United Kingdom: Plastic Packaging Tax and Smart Sustainable Packaging Initiatives

The United Kingdom privacy film market is influenced by sustainability regulations such as the Plastic Packaging Tax (PPT), introduced in April 2022, which taxes plastic products with less than 30% recycled content. This has created a strong economic incentive for recyclable privacy films and accelerated adoption of circular material practices. Complementing this, the Smart Sustainable Plastic Packaging (SSPP) Challenge, a £60 million funding initiative, has supported over 80 projects focused on recycling technologies and material innovation.

The government is also advancing a deposit return scheme for plastic bottles, which is shaping consumer behavior toward recycling and indirectly influencing film producers to design for circularity. Regulatory oversight extends to the healthcare sector, with the Medicines and Healthcare products Regulatory Agency (MHRA) providing guidelines for medical packaging, including films used in pharmaceuticals. As a result, UK manufacturers are investing in single-material recyclable films and water-based adhesives, aligning with both compliance requirements and market expectations for sustainability.

Privacy Film Market Report Scope

Privacy Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Type (Screen Privacy, Window Privacy, Decorative & Frosted, Smart/Switchable), By Technology (Screen Privacy, Window Privacy), By Application (Screen Privacy, Window Privacy), By Material (PET, PVC, PDLC, Ceramic)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Eastman Chemical Company, Saint-Gobain S.A., Avery Dennison Corporation, Hanita Coatings RCA Ltd., Johnson Window Films, Inc., Madico, Inc., Cosmo Films Ltd., Toray Industries, Inc., Gentex Corporation, Purlfrost Ltd., UPM Raflatac, ORAFOL Europe GmbH, Glass Apps, Smart Film Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Privacy Film Market Segmentation

By Type

- Screen Privacy

- Window Privacy

- Decorative & Frosted

- Smart/Switchable

By Technology

- Screen Privacy

- Window Privacy

By Application

- Screen Privacy

- Window Privacy

By Material

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Privacy Film Market

- 3M Company

- Eastman Chemical Company

- Saint-Gobain S.A.

- Avery Dennison Corporation

- Hanita Coatings RCA Ltd.

- Johnson Window Films, Inc.

- Madico, Inc.

- Cosmo Films Ltd.

- Toray Industries, Inc.

- Gentex Corporation

- Purlfrost Ltd.

- UPM Raflatac

- ORAFOL Europe GmbH

- Glass Apps

- Smart Film Ltd.

* List Not Exhaustive

Methodology

The research methodology for the Privacy Film Market integrates a robust combination of primary and secondary research approaches to provide comprehensive insights for industry professionals. Primary research involved detailed interviews with key stakeholders, including privacy film manufacturers, architects, commercial and residential facility managers, automotive experts, R&D specialists, and regulatory advisors across North America, Europe, Asia-Pacific, and emerging markets. Secondary research encompassed a thorough review of company reports, investor presentations, trade publications, patents, and verified market studies, with a focus on UV and solar control technologies, smart/switchable films, decorative innovations, and sustainable materials. USDAnalytics employed advanced data triangulation methods to ensure accuracy in market sizing, CAGR projections, and segmentation analyses, integrating macroeconomic trends, regional regulatory influences, technological adoption, and raw material availability. Top-down and bottom-up approaches were used to validate global and regional forecasts, while competitive intelligence captured company strategies, innovation pipelines, and mergers/acquisitions. This methodology ensures that the report delivers reliable, actionable, and professional-grade intelligence on market dynamics, growth opportunities, and emerging technologies in the privacy film industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.