Market Overview: Expansion Driven by E-Commerce and Sustainable Protective Solutions

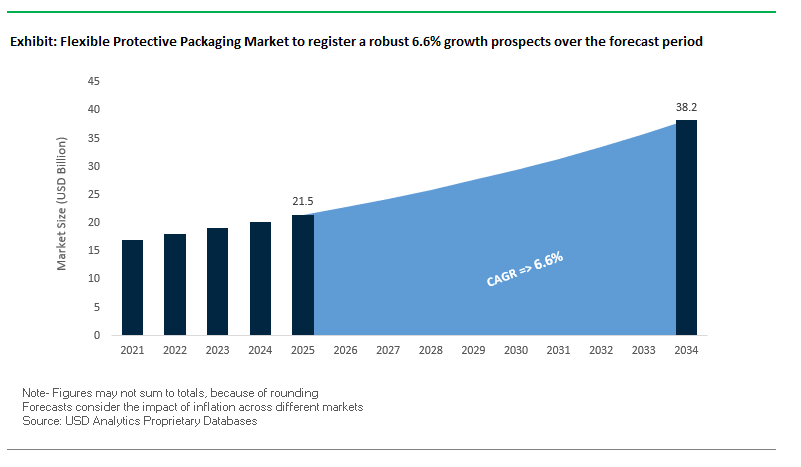

The Global Flexible Protective Packaging Market is projected to grow from USD 21.5 billion in 2025 to USD 38.2 billion by 2034, advancing at a strong CAGR of 6.6%. As a crucial component of global supply chains, flexible protective packaging ensures damage prevention, optimized logistics, and product safety across diverse industries. With e-commerce volumes surging and sustainability regulations tightening, the market is experiencing accelerated innovation in both materials and automation.

A key trend is the shift toward paper-based protective solutions. Kraft paper and corrugated inserts are increasingly adopted as recyclable, eco-friendly alternatives to traditional plastic void fill. At the same time, demand for air cushions, bubble wraps, and inflatable packaging continues to expand, particularly in e-commerce fulfillment centers, where lightweight and space-efficient materials are critical for shipping optimization.

The industry is also witnessing rapid integration of automation and smart packaging technologies. Automated void-fill systems and cushioning machines are helping companies improve packaging efficiency, while features like QR codes and RFID tags are being embedded to support supply chain traceability. Furthermore, the move toward mono-material designs ensures compatibility with recycling streams, addressing one of the biggest challenges in protective packaging sustainability.

Key Insights for industry professionals and buyers:

- Market size to reach USD 38.2B by 2034, CAGR 6.6%.

- Paper-based protective packaging is gaining market share as a sustainable substitute.

- Air cushions and bubble wraps remain essential for e-commerce and retail.

- Automation and smart tracking technologies enhance efficiency and visibility.

- Strong focus on circular economy-compatible designs for recyclability.

Market Analysis: Recent Developments in Flexible Protective Packaging

The Flexible Protective Packaging Industry has been reshaped by sustainability initiatives, acquisitions, and cross-industry collaborations over the last two years.

In September 2025, the Flexible Plastic Fund (FPF) released its FlexCollect report in the UK, highlighting the success of its at-home collection scheme for flexible plastics. With 89% consumer satisfaction and nearly 90% of collected material clean for recycling, this model presents a benchmark for other regions.

In August 2025, ProAmpac announced plans to acquire PAC Worldwide, expanding its role in protective and e-commerce packaging. During the same month, Sealed Air reported stabilization of protective packaging volumes, with its industrial portfolio showing renewed growth, reflecting improved demand across B2B and retail channels. Also in August 2025, Amcor upgraded its Heanor, UK recycling facility, adding capacity for 2,800 tonnes of recyclate annually to support flexible protective applications.

Meanwhile, the U.S. Flexible Film Initiative (USFFI) launched in August 2025 as a coalition to build a circular recovery system for flexible packaging in the U.S., reflecting strong industry alignment with recycling and sustainability.

Earlier, in July 2025, major industry mergers reshaped the landscape. The Amcor–Berry Global merger formed a dominant leader across flexibles and rigid containers, while the Smurfit Kappa–WestRock merger created a giant in paper-based protective alternatives. Similarly, in October 2024, shareholders of International Paper and DS Smith approved a combination to create one of the largest global players in corrugated and paper-based protective solutions.

Transformative Trends and High-Value Opportunities in the Flexible Protective Packaging Market

Strategic Shift to Paper-Based Protective Solutions

The flexible protective packaging market is undergoing a significant transformation as leading e-commerce and logistics companies pivot from plastic-based void fill and cushioning to paper-based alternatives. This trend is driven by consumer demand for sustainable packaging, corporate ESG commitments, and tightening regulations on plastic waste. Paper-based solutions are designed to achieve performance parity, offering equivalent transit protection while being environmentally sustainable. Companies like Sealed Air have introduced BUBBLE WRAP® embossed paper, which is curbside-recyclable, while Pregis invested $14 million to produce its EverTec™ paper mailers, highlighting a clear market pivot. This trend presents a high-value growth avenue, particularly for manufacturers delivering strong, tear-resistant, and compliant paper products. It also reshapes the value chain, requiring close collaboration between paper mills, converters, and R&D teams to ensure consistent supply and high-performance standards.

Adoption of Right-Sizing and On-Demand Packaging Systems

To optimize efficiency, reduce material usage, and lower carbon emissions, the market is seeing widespread adoption of automated right-sizing and on-demand packaging systems. These systems leverage software and automated machinery to create custom-sized corrugated boxes and dispense precise amounts of protective dunnage, minimizing overpacking. Implementation of such systems can reduce packaging size by 40% and corrugated material use by 26%, according to Integrated Systems Design. Key players like Packsize and Ranpak provide on-demand solutions capable of producing a wide variety of box sizes rapidly. Brands like Helly Hansen are leveraging this technology to cut labor costs, increase throughput, and meet sustainability targets. By enabling just-in-time packaging, manufacturers create a high-value growth avenue, reducing dimensional weight shipping costs and improving supply chain efficiency. The deployment fosters a data-driven, interconnected value chain, enhancing collaboration between packaging providers and logistics operators while reducing truck space waste.

Development of High-Performance Recycled Content Paper Cushioning

There is a notable opportunity to develop next-generation paper protective products made entirely from post-consumer recycled content that match or exceed the performance of virgin paper or plastic alternatives. Advanced pulping and manufacturing techniques are enhancing the strength, tear resistance, and cushioning properties of recycled paper, closing the loop on a circular economy. Companies like Storopack provide paper cushioning with up to 100% recycled content, while Pregis has perfected high-performance recycled paper mailers through extensive R&D. Commercializing these solutions represents a major growth avenue, appealing to brands seeking certified, functional, and environmentally friendly protective packaging. This opportunity is reshaping the value chain, fostering collaboration among paper mills, material scientists, and packaging manufacturers to deliver seamless, end-to-end solutions designed for circularity.

Bio-Based and Home-Compostable Flexible Foams

For applications requiring plastic foams, such as high-value electronics and fragile items, there is a significant opportunity to develop bio-based, home-compostable protective foams derived from renewable polymers like PLA and PHA. These materials provide superior protection while being certified for home composting, addressing end-of-life plastic challenges. Products like Storopack AIRplus® Bio Home Compostable film and BASF ecovio® biopolymer demonstrate the viability of robust, eco-friendly alternatives. Companies like FKuR are advancing high-performance, biodegradable plastics from corn and sugarcane for protective films and foams. Academic research confirms these materials withstand mechanical stress and moisture, ensuring performance comparable to conventional plastics. The commercialization of bio-based compostable foams presents a high-value growth opportunity, catering to consumer demand for plastic-free packaging and enabling brands to meet sustainability targets while maintaining product safety.

Competitive Landscape: Leading Players in Flexible Protective Packaging

The Flexible Protective Packaging Market is led by multinational players combining scale, material science, and automation expertise to meet rising e-commerce and sustainability demands.

Sealed Air Corporation strengthens protective volumes with automation focus

Sealed Air is a global leader in protective and food packaging, best known for BUBBLE WRAP® and Cryovac® films. In August 2025, it reported stabilization in volumes and growth in its industrial segment. Its strategy is to provide high-performance, cost-effective, and recyclable protective packaging, with commitments to 100% recyclable/reusable packaging by 2025 and net-zero carbon by 2040.

Pregis LLC advances on-demand and paper-based protective systems

Pregis specializes in custom-engineered protective packaging with expertise in on-demand air and paper solutions. Its portfolio includes AirSpeed® inflatables, Easypack® cushioning, and EverTec™ mailers. With its “2k30 mission,” Pregis aims to ensure that all products are recyclable, reusable, or reduce virgin plastic reliance by at least 30% by 2030.

Smurfit Kappa Group PLC expands paper-based protective dominance

Following its merger with WestRock in July 2025, Smurfit Kappa emerged as a global leader in corrugated and paper-based protective packaging. Its offerings include corrugated inserts, void fill, and specialty protective boxes. Its strategy centers on circular economy solutions, reducing customers’ environmental footprint while scaling paper-based alternatives.

Ranpak Holdings Corp. grows with automation-led paper cushioning

Ranpak is recognized for paper-based protective packaging systems like PadPak® and FillPak®. In August 2025, it reported its eighth consecutive quarter of growth, supported by enterprise contracts in North America. Its automation backlog reflects demand for system-based solutions that combine materials with efficiency-enhancing equipment.

ProAmpac expands protective packaging through PAC Worldwide acquisition

ProAmpac, a leader in flexible and protective packaging, announced in August 2025 its acquisition of PAC Worldwide, strengthening its e-commerce fulfillment offerings. Its ProActive Recyclable® films provide drop-in replacements for hard-to-recycle laminates, aligning with its goal of sustainability-driven innovation across protective and food packaging.

Flexible Protective Packaging Market Share Insights

Films & Wraps Dominate Packaging Type in Flexible Protective Packaging Market

In the flexible protective packaging market, films and wraps secure the largest projected share of 45% in 2025, reflecting their indispensability in product protection, load stabilization, and damage prevention across supply chains. Stretch film remains critical for pallet unitization, shrink film ensures tamper evidence and bundling integrity, while cushioning films and bubble wraps safeguard fragile products during transit. Bags and sacks complement this leadership by offering tailored containment solutions, from anti-static bags for electronics to heavy-duty woven sacks for chemicals and industrial parts. Protective pouches, including padded mailers, foil-lined pouches, and ESD-safe solutions, are rapidly gaining adoption due to the exponential growth of e-commerce and direct-to-consumer shipments. The “Other” segment, encompassing foam wraps, inflatable void-fill, and bespoke engineered designs, addresses specialized needs in aerospace, automotive, and high-value electronics. This segmentation emphasizes how films & wraps form the backbone of protective packaging while pouches evolve as the most responsive format to last-mile e-commerce demands.

E-commerce Emerges as the Largest End-Use Industry in Flexible Protective Packaging

E-commerce leads with 30% share of the flexible protective packaging market in 2025, driven by the unprecedented surge in online retail and last-mile delivery requirements. Every shipped item demands protective solutions, from void-fill air pillows and paper wraps to bubble mailers, making e-commerce the central growth engine of this sector. Industrial packaging follows closely with 25% share, reflecting its massive consumption of stretch wrap, heavy-duty sacks, and pallet protection products across global manufacturing and B2B shipping. Food and beverages remain essential, particularly for perishables requiring insulated liners and barrier films, while pharmaceuticals demand ultra-secure, sterile packaging with tamper-evident and temperature-controlled features to safeguard efficacy. Electronics add another high-value layer, with precision requirements for anti-static and conductive films ensuring component protection against electrostatic discharge. Other end-uses, including automotive and aerospace, adopt tailored solutions for part durability and safe distribution. The segmentation underscores how e-commerce drives volume expansion, industrial sectors anchor stability, and regulated industries like pharmaceuticals and electronics fuel high-performance innovation.

United States Flexible Protective Packaging Market Driven by Sustainable and Smart Packaging Innovations

The U.S. flexible protective packaging market is undergoing rapid transformation driven by a fragmented regulatory landscape and the adoption of Extended Producer Responsibility (EPR) laws across multiple states, including Maryland. These regulations shift the financial responsibility of recycling and waste management from taxpayers to manufacturers, encouraging the development of recyclable mono-material films and minimizing multi-layer laminates. Technological advancements, such as smart packaging with QR codes and NFC chips, provide enhanced consumer engagement, supply chain traceability, and even augmented reality experiences, while new protective film formats improve durability and product safety during transit.

Corporate investments are accelerating sustainable packaging production, with Amcor announcing a $250 million expansion of its Wisconsin facility to boost capacity for recyclable and bio-based protective materials. Key applications include e-commerce, direct-to-consumer (DTC) segments, and the food and beverage industries, driven by the growing need for lightweight, robust, and efficient packaging solutions. Sustainability remains a critical market imperative, with the adoption of eco-friendly materials like bio-based films and recyclable paperboard, meeting consumer demand for environmentally responsible packaging while maintaining product protection standards.

Germany Flexible Protective Packaging Market Strengthened by Circular Economy and Regulatory Compliance

Germany’s flexible protective packaging market is governed by strict regulatory measures, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates that all packaging be fully recyclable or reusable by 2030 and phases out harmful substances such as PFAS. The Packaging Act (VerpackG) reinforces circular economy initiatives by incentivizing packaging design for recyclability, supported by reusable containers and trays for FMCG products.

Technological innovation is driving sustainable production, with machinery capable of handling eco-friendly materials and the development of digital product passports and watermarks enhancing transparency and recycling efficiency. Corporate developments, such as Amcor’s CleanStream technology showcased at Fachpack Expo 2025, utilize domestically recovered, mechanically recycled polypropylene (PP). Demand remains high in retail and food service sectors, with consumers seeking premium pouches and high-barrier films that extend shelf life while adhering to Germany’s eco-conscious packaging standards.

China Flexible Protective Packaging Market Expands Through Green Initiatives and Domestic Manufacturing

China’s flexible protective packaging market is shaped by governmental “dual carbon” policies and the March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, promoting recycling and sustainable material usage. Regulatory reforms introduced in September 2023 limit excessive packaging by defining maximum layers and void ratios, directly impacting e-commerce packaging.

Technological advancements, including automation, AI, and the integration of “5G plus industrial internet,” optimize production efficiency and flexible packaging capabilities. Domestic manufacturing is a growing trend, with local companies expanding capacities to replace imported solutions. The rapid growth of e-commerce and food delivery sectors drives demand, with online grocery deliveries forecasted to account for a significant share of flexible protective packaging volumes, positioning China as a hub for innovative, circular packaging solutions.

India Flexible Protective Packaging Market Fueled by Circular Economy Policies and High-Performance Solutions

India’s flexible protective packaging market benefits from government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which ensure food-grade safety and prohibit recycled plastics for food contact. Technological adoption is rising, with innovations such as UFlex’s Electron Beam Coating Technology and Ascelpius™ BOPET film made with up to 100% PCR content enabling high-performance and sustainable protective packaging.

Corporate investments in new production facilities support domestic demand, with UFlex operating over 100,000 TPA and four government-approved R&D laboratories. Key applications include the food and beverage and personal care sectors, while e-commerce growth and sustainability concerns drive demand for robust, eco-friendly protective solutions. The “Make in India” initiative further supports local manufacturing, fostering innovation and technological development to meet the increasing domestic demand.

Japan Flexible Protective Packaging Market Embraces Advanced Films and Functional Packaging Innovations

Japan’s flexible protective packaging industry leverages precision manufacturing and sustainability-driven innovations. In September 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., developed a recycled BOPP film ready for mass production, exemplifying the country’s circular economy focus. The Plastic Resource Circulation Act (April 2022) promotes environmental design and reduces single-use plastics, targeting 2 million tonnes of bio-based products annually by 2030.

The market emphasizes specialty and value-added films with superior barrier properties, IoT-enabled tracking, and functional innovations like easy-open tear notches and resealable closures, catering to aging and single-person households. Strategic mergers, including Sika AG’s acquisition of Hamatite from Yokohama Rubber Co., strengthen technological capabilities and market presence, particularly in automotive and construction applications, ensuring Japan remains at the forefront of advanced and sustainable flexible protective packaging solutions.

Brazil Flexible Protective Packaging Market Accelerates Through Sustainability Initiatives and Technological Innovation

Brazil’s flexible protective packaging market is driven by government initiatives promoting sustainable waste management, including the January 2025 amendment to the National Solid Waste Policy, which restricts solid waste imports to strengthen domestic recycling programs. Technological innovation is accelerating, with companies incorporating robotics and AI for efficiency, automated label selection, and defect detection in protective packaging.

The market is shifting toward premium, digitally enabled packaging solutions that extend product shelf life while maintaining freshness and quality. Sustainability is a core focus, highlighted by Klabin’s introduction of EkoFlex, its first flexible packaging paper, and collaborations like iFood and XPRIZE’s $20 million competition for flexible, biodegradable packaging. These initiatives underscore Brazil’s commitment to innovative, eco-friendly protective packaging solutions that meet growing market demand.

Flexible Protective Packaging Market Report Scope

Flexible Protective Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.5 Billion

|

|

Market Size (2034)

|

$38.2 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Foils, Bioplastics), By Packaging Type (Pouches, Films & Wraps, Bags & Sacks, Other Packaging Types), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Electronics, E-commerce, Industrial, Other End-Use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Berry Global Group, Inc., Sonoco Products Company, Sealed Air Corporation, DS Smith plc, ProAmpac, UFlex Ltd., Constantia Flexibles Group, TC Transcontinental Packaging, Printpack Inc., Novolex Holdings, LLC, Pregis LLC, Ranpak Holdings Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Protective Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Foils

- Bioplastics

By Packaging Type

- Pouches

- Films & Wraps

- Bags & Sacks

- Other Packaging Types

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Electronics

- E-commerce

- Industrial

- Other End-Use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Protective Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Berry Global Group, Inc.

- Sonoco Products Company

- Sealed Air Corporation

- DS Smith plc

- ProAmpac

- UFlex Ltd.

- Constantia Flexibles Group

- TC Transcontinental Packaging

- Printpack Inc.

- Novolex Holdings, LLC

- Pregis LLC

- Ranpak Holdings Corp.

* List Not Exhaustive

Methodology

USDAnalytics conducted an extensive, multi-layered research process to produce an authoritative analysis of the Global Flexible Protective Packaging Market. This methodology combined primary research—comprising in-depth interviews with packaging manufacturers, logistics operators, e-commerce fulfillment leaders, and sustainability experts—with secondary research, including company filings, trade publications, patent databases, and industry reports. Market sizing, growth projections, and trend identification were evaluated across material types, packaging formats, and end-use industries, with particular attention to innovations such as paper-based protective solutions, bio-based compostable foams, high-performance recycled content papers, and smart, automated on-demand systems. Regional regulations and initiatives in the U.S., Germany, China, India, Japan, and Brazil were analyzed to assess compliance, sustainability adoption, and impact on corporate ESG strategies. Key corporate developments, mergers, acquisitions, and technological advancements were incorporated to offer actionable insights, highlighting opportunities for manufacturers, brand owners, and logistics providers seeking efficient, eco-friendly, and high-performance protective packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.