Bubble Wrap Packaging Market Overview: Sustainability and E-commerce as Core Growth Drivers

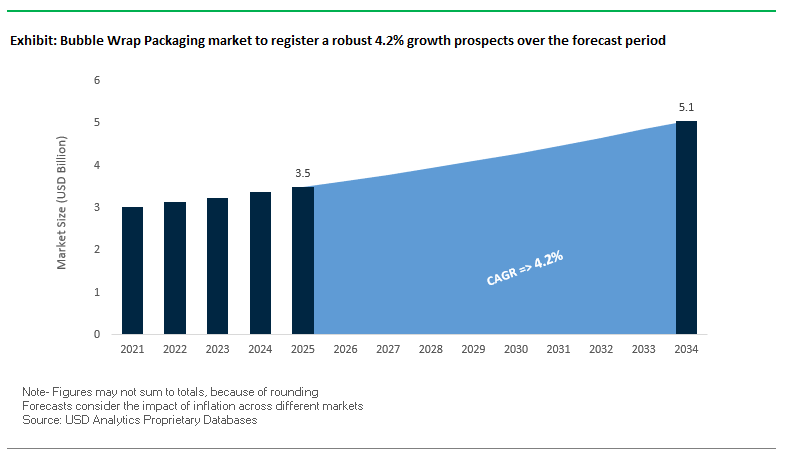

The bubble wrap packaging market is expected to grow from USD 3.5 billion in 2025 to USD 5.1 billion by 2034, at a CAGR of 4.2%. This growth is underpinned by the unstoppable rise of e-commerce shipments, the increasing emphasis on eco-friendly packaging materials, and the integration of automation and smart packaging technologies. For buyers and industry professionals, the central question is how effectively packaging suppliers can deliver durable, lightweight, and recyclable protective solutions that align with regulatory mandates and consumer expectations without compromising performance.

Key Insights Defining the Bubble Wrap Packaging Market

- E-commerce dominance: Protective packaging has become a non-negotiable element in supply chains, with millions of parcels shipped daily.

- Over 40% material reduction: Lightweighting innovations such as on-demand inflatable systems and air cushions are cutting raw material use dramatically.

- Electronics and electricals as top users: Fragile devices and components require superior shock and vibration protection, making this sector a critical revenue driver.

- Biodegradable and paper-based wraps rising: Alternatives such as 100% paper bubble wraps are gaining traction, supported by recyclability and growing regulatory backing.

Market Analysis: Recent Global Developments in Bubble Wrap Packaging

The past 18 months have seen transformative changes in the bubble wrap packaging industry, reflecting broader market trends around sustainability, acquisitions, and smart packaging integration. In August 2025, Sealed Air Corporation announced its Q2 results, highlighting its protective packaging segment’s strongest performance since 2021, supported by a resurgence in industrial packaging demand. Around the same period, May 2025 brought a breakthrough study on bioplastics derived from cornstarch, reinforcing the viability of renewable feedstocks for high-performance protective films.

Sustainability-focused innovation gained momentum in April 2025, when LEIPA UK Ltd and Papair’s PapairWrap the world’s first 100% paper bubble wrap won the Innovation Gallery Award at Packaging Innovations & Empack 2024. In March 2025, a global logistics provider unveiled IoT-enabled smart packaging solutions, allowing real-time monitoring of shipments with embedded sensors, addressing product safety and supply chain transparency. Similarly, in December 2024, Pregis LLC committed to matching 100% of electricity consumed at six facilities with wind power, strengthening its 2040 net-zero pledge.

E-commerce continues to shape demand. In November 2024, a global e-commerce retailer launched a pilot program to replace plastic-based bubble wrap with paper-based cushioning, a move that will significantly shift demand dynamics. Governments are also playing a critical role; a European subsidy program in October 2024 began funding research into agricultural waste valorization, driving the next generation of bio-based packaging films. To close the loop, September 2024 saw the publication of a paper in the Journal of Packaging Technology and Science on chemical recycling of multi-layer bubble films, pushing the sector closer to achieving true circularity.

Emerging Trends and Opportunities Defining the Bubble Wrap Packaging Market

Strategic Shift Towards On-Demand, Right-Sized Inflatable Packaging Systems

The bubble wrap packaging market is undergoing a major transformation as e-commerce growth and fulfillment efficiency push companies toward on-demand inflatable systems. Traditional pre-inflated rolls take up significant storage space, create inefficiencies in handling, and add to dimensional weight shipping costs. To overcome these challenges, fulfillment centers are deploying automated void-fill systems that generate inflatable cushioning at the point of use. For instance, Sealed Air’s BUBBLE WRAP® brand offers flat-roll systems that save up to 80% of warehouse space, enabling fulfillment hubs to maximize storage capacity for products or add more automation equipment. Regulatory changes are reinforcing this trend: the European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, requires that “empty space” in packaging be reduced to 50% or less by 2030. On-demand inflatable packaging directly addresses this requirement by producing air pillows that minimize dunnage and improve cube utilization in shipping cartons. Operational efficiency gains are equally notable: leading solution providers report up to 20% faster packing speeds with on-demand cushioning systems, as workers can instantly create the exact volume of material needed without handling bulky pre-inflated rolls. This combination of regulatory compliance, cost savings, and operational agility is rapidly cementing on-demand inflatable systems as the new standard in protective packaging.

Material Innovation Focused on Recycled Content and Recyclability

The shift towards sustainability is reshaping the material science behind bubble wrap and inflatable cushioning. With increasing post-consumer recycled (PCR) content mandates, manufacturers are re-engineering their films to meet brand and regulatory demands. Sealed Air has introduced inflatable cushioning films containing up to 70% post-industrial recycled content, while its inflatable air pillows incorporate up to 50% PCR content, helping brands cut reliance on virgin resins. These initiatives align directly with the EU PPWR’s 2030 recyclability mandate, which requires all packaging to be fully recyclable within established waste streams. As a result, the industry is pivoting towards mono-material polyethylene (PE) films, which are compatible with existing store drop-off recycling programs. Unlike laminated or multi-layer films that create contamination issues, mono-material designs ensure a cleaner recycling process and better material recovery rates. This trend not only addresses regulatory compliance but also aligns with corporate ESG commitments, brand plastic-reduction pledges, and consumer demand for transparent, sustainable packaging solutions. In effect, bubble wrap is evolving from a single-use plastic emblem to a recyclable and circular material solution.

Development of Performance-Competitive Paper-Based Cushioning Alternatives

The global push to eliminate plastics has opened significant opportunities for paper-based cushioning solutions that can match the protective performance of bubble wrap. Brands with “no plastic” mandates, particularly in consumer electronics, cosmetics, and lifestyle goods, are actively piloting alternatives. Companies such as EcoCushion Paper (India) are introducing honeycomb paper wraps that expand into 3D cushioning formats, delivering biodegradability and curbside recyclability while effectively replacing plastic films for fragile goods like glassware. Similarly, ExpandOS has developed engineered paper pyramids, which are dispensed on demand to fill void spaces and absorb impact. This system is already being used by global companies such as Epson USA to remove plastics from their supply chain. These alternatives provide brands with a compelling value proposition: robust protection, consumer-friendly disposal, and alignment with sustainability branding. As regulations increasingly penalize virgin plastics and consumer preferences tilt towards eco-conscious packaging, paper-based bubble wrap substitutes are emerging as a high-growth category in protective packaging.

Integration of Smart and Connected Packaging Features for Supply Chain Visibility

Bubble wrap and inflatable packaging, with their large printable and surface areas, represent an underutilized platform for embedding smart technologies that enhance supply chain visibility. The logistics sector is adopting IoT-enabled sensors that can be seamlessly integrated into protective cushioning to track shock, vibration, and handling conditions during transit. This innovation provides real-time data on shipment integrity, giving brands and logistics providers a new level of control over product quality. Beyond real-time monitoring, this data offers predictive insights, allowing companies to identify problematic carriers, routes, or distribution points that contribute to higher damage rates. By creating a data-driven quality control loop, smart-enabled bubble wrap helps reduce product returns, lower insurance claims, and enhance customer satisfaction. As e-commerce volumes continue to climb, especially for high-value electronics, pharmaceuticals, and fragile consumer goods, the integration of smart tracking into protective packaging is poised to become a major differentiator for packaging suppliers and logistics providers alike.

Competitive Landscape: Global Leaders in Bubble Wrap Packaging

The bubble wrap packaging market is highly consolidated, with major companies focusing on sustainability, automation, and substrate diversification to remain competitive. Their strategies combine R&D in materials science, investments in renewable energy, and customer-driven innovations.

Sealed Air Corporation strengthens leadership with multi-material innovation

Sealed Air, the inventor of Bubble Wrap®, remains a dominant force with a diverse portfolio spanning inflatable systems, specialty cushioning films, and temperature-sensitive packaging. In August 2025, the company reported strong protective packaging performance, crediting its organizational “de-layering” strategy and renewed distributor engagement. Sealed Air is expanding beyond plastics, adopting a “substrate agnostic” approach, with increasing investments in paper-based alternatives. Its strength lies in brand recognition, IP portfolio, and global scale, reinforced by its vision of “packaging for a better world.”

Pregis LLC advances net-zero goals with wind-powered facilities

Pregis is a leading innovator in on-demand air cushion systems (AirSpeed®) and paper-based protective packaging (Easypack®). In December 2024, it matched 100% of the electricity consumed at six plants with wind power, reinforcing its 2040 net-zero carbon commitment. Pregis’s “More with Less” strategy prioritizes material reduction without compromising performance, while its partnership with a chemical company enabled the creation of certified-circular polyethylene foams. Its strength lies in customer-centric design, ensuring protective packaging solutions that balance sustainability, cost, and product safety.

Shurtape Technologies (Tesa SE) integrates tapes and void-fill into holistic solutions

Though not a direct bubble wrap producer, Shurtape (Tesa SE) plays a pivotal role in packaging lines with its adhesive tapes, protective films, and void-fill solutions. Its competitive edge lies in R&D excellence, enabling the production of eco-optimized tapes with superior adhesion and recyclability. Shurtape’s integration strategy ensures that customers receive complete packaging solutions, combining films, foams, and tapes, to enhance efficiency and sustainability across supply chains.

Intertape Polymer Group expands reach under Clearlake Capital ownership

Intertape Polymer Group (IPG) manufactures a wide array of protective products, including bubble rolls, bubble bags, and hybrid solutions. Acquired by Clearlake Capital in 2022, IPG has accelerated its growth strategy with a focus on portfolio diversification and global expansion. Its strength is its broad product base, serving e-commerce, consumer goods, and industrial clients with reliable protective packaging. The company’s one-stop-shop model enables efficient customer engagement across multiple packaging needs.

Ranpak Holdings scales paper-based alternatives for e-commerce

Ranpak is redefining protective packaging with renewable, recyclable, and compostable paper-based cushioning systems. Although not a bubble wrap producer, Ranpak competes directly with plastic bubble wrap by offering eco-friendly void-fill solutions for e-commerce. In 2025, it secured its second major e-commerce deal, reinforcing its position as a sustainable alternative provider. Ranpak’s competitive advantage lies in its automation-ready paper systems, which combine sustainability with operational efficiency, helping retailers meet carbon reduction goals while ensuring product safety.

Bubble Wrap Packaging market Share Insights

Market Share by Material Type in the Bubble Wrap Packaging Industry

Low-density polyethylene (LDPE) dominates the bubble wrap packaging market with an overwhelming 88% share in 2025, reflecting its entrenched position as the most cost-effective and scalable solution. LDPE’s unique balance of flexibility, durability, and clarity allows manufacturers to consistently produce uniform, air-filled bubbles that provide reliable cushioning for a wide range of goods. Its global availability and low production cost have cemented it as the default choice across industries, ensuring stability in high-volume applications such as e-commerce and consumer goods. However, biodegradable and alternative materials are emerging as the critical growth segment, driven by corporate ESG commitments, government regulations on plastic reduction, and consumer demand for eco-friendly packaging. These include recycled PE films, PLA blends, and compostable polymers, which, while premium-priced, are being increasingly adopted by major retailers and e-commerce giants looking to align with sustainability targets. Other materials, including HDPE and co-extruded polymer blends, play a niche but important role in high-value or fragile applications. These engineered solutions offer enhanced puncture resistance or tailored performance attributes but are not positioned to challenge LDPE’s dominance at scale, instead serving as specialty options for sensitive shipments.

Market Share by End-Use Industry in the Bubble Wrap Packaging Industry

E-commerce and retail dominate the bubble wrap packaging market with a commanding 65% share in 2025, underscoring the segment’s role as the primary driver of demand. With the rapid rise of online shopping, bubble wrap has become indispensable for last-mile delivery protection, where the risk of shock, drops, and handling damage is highest. This segment’s growth is directly tied to global e-commerce volumes, making it the cornerstone of the industry. Electronics account for 15% of the market, forming a high-value segment where protection is critical. Anti-static and conductive bubble wraps are widely used here to shield smartphones, laptops, and electronic components from both impact and electrostatic discharge, ensuring safe delivery of fragile and high-priced products. Consumer goods contribute substantially to volume demand, covering a wide range of everyday products such as toys, ceramics, furniture, and glassware. This category typically relies on cost-efficient LDPE bubble wrap, feeding directly into the e-commerce ecosystem. Automotive and pharmaceuticals serve as smaller but strategically important niches. In automotive, bubble wrap is used to protect fragile parts, lights, and glass during transport, while in pharmaceuticals it cushions medical devices, glass bottles, and lab equipment to ensure integrity. Food and beverage remains a minimal application area, as bubble wrap is unsuitable for direct food contact; its limited role is in bulk transit, where it protects glass bottles or packaging containers being shipped to filling plants. Collectively, these end-use industries highlight how bubble wrap packaging continues to balance low cost, versatility, and protective performance, even as sustainability-driven alternatives begin reshaping its long-term outlook.

United States: E-Commerce Growth and Sustainable Bubble Wrap Packaging Driving Market Expansion

The United States bubble wrap packaging market is thriving, largely due to the country’s dominance in global e-commerce. With online retail booming across categories such as electronics, fragile consumer goods, and household essentials, the need for protective packaging solutions like bubble wrap has surged. Companies are introducing technological innovations such as self-inflating bubble wrap and high-retention air pockets that deliver superior cushioning and reduce material waste, making them ideal for high-volume shipping operations.

Sustainability is also reshaping the U.S. market. Major players like Sealed Air are pioneering biodegradable and recycled bubble wrap alternatives, aligning with consumer preferences for eco-friendly packaging. The integration of automated packaging systems in fulfillment centers is further enhancing productivity, reducing labor costs, and meeting the speed demands of online retail giants. Strategic partnerships between packaging firms, e-commerce platforms, and logistics providers underscore the market’s evolution toward tailored, efficient, and sustainable packaging solutions that support long-term industry growth.

China: Explosive E-Commerce Growth and Industrial Capacity Expansion in Bubble Wrap Packaging

China’s bubble wrap packaging market is experiencing exponential growth, fueled by the country’s massive e-commerce sector that dominates both domestic and cross-border trade. With millions of shipments daily, protective packaging solutions like bubble wrap are essential for safeguarding fragile and high-value goods. To meet this immense demand, Chinese manufacturers are investing heavily in new production capacity and advanced machinery, enabling large-scale and cost-efficient output.

Government policies promoting supply chain modernization and sustainability are shaping the industry’s direction. While regulations are increasingly targeting plastic waste, the sheer scale of e-commerce shipments ensures bubble wrap remains a critical protective material. Chinese firms are adopting automated wrapping technologies and exploring new material innovations to enhance durability, reduce costs, and align with environmental mandates. As a result, China is positioning itself as a global leader in scalable, technologically advanced bubble wrap manufacturing.

Germany: EU Sustainability Regulations and High-Value Industries Fueling Bubble Wrap Alternatives

Germany’s bubble wrap packaging industry is evolving under the strong influence of European Union regulations such as the Packaging and Packaging Waste Regulation (PPWR). These rules are accelerating the transition away from traditional plastic bubble wrap toward recyclable and paper-based protective packaging solutions like honeycomb paper wrap. Germany’s long-standing commitment to the circular economy ensures that packaging innovations focus on reusability, recyclability, and eco-friendly material sourcing.

In addition to sustainability, Germany’s automotive and electronics industries are major drivers of demand for advanced protective packaging. These high-value sectors require specialized bubble wrap with anti-static properties and superior cushioning, ensuring safe transit of sensitive components. By combining regulatory pressure with industry-specific needs, Germany is setting benchmarks in eco-friendly innovation and premium protective packaging solutions.

India: E-Commerce Boom and Regulatory Shifts Creating Demand for Eco-Friendly Bubble Wrap Packaging

India’s bubble wrap packaging market is rapidly expanding, powered by the country’s fast-growing e-commerce sector catering to a young, tech-savvy consumer base. Fragile goods such as electronics, personal care items, and consumer products are fueling the demand for reliable protective packaging solutions. In response, domestic manufacturers are scaling up production capacity, investing in modern machinery to produce diverse formats including rolls, sheets, and custom bubble wrap pouches.

The government’s Plastic Waste Management Rules introduced by the CPCB are encouraging packaging companies to develop recyclable and eco-friendly protective materials. While bubble wrap does not always fall under single-use plastic bans, the regulations are nudging the industry toward sustainable practices. Beyond e-commerce, pharmaceuticals and personal care industries are increasingly adopting bubble wrap packaging to ensure product integrity during distribution, highlighting India’s transition into a multi-industry demand hub for protective packaging.

Japan: Precision Manufacturing and Technological Innovation Defining Bubble Wrap Packaging Market

Japan’s bubble wrap packaging market is shaped by the country’s demand for high-precision protective packaging, particularly in sectors such as electronics, medical devices, and automotive components. The need to ensure product integrity in these industries drives demand for advanced cushioning materials with reliable, consistent performance.

Japanese manufacturers are recognized for their technological innovation in protective packaging, with developments in lightweight materials and single-material structures that minimize environmental impact while maximizing efficiency. Combined with Japan’s robust recycling infrastructure, companies are focusing on designing bubble wrap solutions that are fully compatible with national recycling programs. This commitment to sustainability and high-performance packaging makes Japan a global benchmark for premium protective packaging standards.

Bubble Wrap Packaging Market Report Scope

Bubble Wrap Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$5.1 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Material Type (Polyethylene, Low-Density Polyethylene, High-Density Polyethylene, Biodegradable Plastic, Other Materials), By Product Type (General Grade Bubble Wraps, High-Grade Bubble Wraps, Anti-Static Bubble Wraps, Temperature-Controlled Bubble Wraps, Other Specialty Wraps), By End-Use Industry (E-commerce & Retail, Electronics, Automotive, Consumer Goods, Food & Beverage, Pharmaceuticals, Other Industrial Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Pregis Corporation, Smurfit Kappa Group, DS Smith plc, Storopack Hans Reichenecker GmbH, Veritiv Corporation, Nefab Group, Ivex Protective Packaging Inc., Shandong Bohui Packaging Co., Ltd., Jiffy Packaging Co. Ltd., Pactiv Evergreen Inc., ACH Foam Technologies, Inc., Sonoco Products Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bubble Wrap Packaging Market Segmentation

By Material Type

- Polyethylene

- Low-Density Polyethylene

- High-Density Polyethylene

- Biodegradable Plastic

- Other Materials

By Product Type

- General Grade Bubble Wraps

- High-Grade Bubble Wraps

- Anti-Static Bubble Wraps

- Temperature-Controlled Bubble Wraps

- Other Specialty Wraps

By End-Use Industry

- E-commerce & Retail

- Electronics

- Automotive

- Consumer Goods

- Food & Beverage

- Pharmaceuticals

- Other Industrial Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bubble Wrap Packaging market

- Sealed Air Corporation

- Pregis Corporation

- Smurfit Kappa Group

- DS Smith plc

- Storopack Hans Reichenecker GmbH

- Veritiv Corporation

- Nefab Group

- Ivex Protective Packaging Inc.

- Shandong Bohui Packaging Co., Ltd.

- Jiffy Packaging Co. Ltd.

- Pactiv Evergreen Inc.

- ACH Foam Technologies, Inc.

- Sonoco Products Company

*List not Exhaustive

Research Coverage

This report investigates the dynamic evolution of the Bubble Wrap Packaging market, with a focus on sustainability, e-commerce growth, and technological innovation. It highlights breakthroughs in material science, such as biodegradable films, mono-material PE structures, and paper-based alternatives, alongside advancements in on-demand inflatable systems and smart, IoT-enabled packaging. The analysis reviews historical market performance from 2021 to 2024, evaluating factors such as regulatory compliance, material innovation, and global e-commerce trends. It also highlights strategic developments, mergers, and acquisitions among leading players, providing insights into competitive positioning, capacity expansion, and R&D investments. This report is an essential resource for packaging professionals, supply chain managers, and brand owners seeking to understand emerging opportunities, optimize protective packaging strategies, and align with ESG objectives. USDAnalytics delivers this comprehensive market intelligence, ensuring actionable insights for decision-makers driving innovation, cost-efficiency, and sustainability in protective packaging.

Scope Highlights:

- Segmentation: By Material Type (Polyethylene, Low-Density Polyethylene, High-Density Polyethylene, Biodegradable Plastic, Other Materials), By Product Type (General Grade Bubble Wraps, High-Grade Bubble Wraps, Anti-Static Bubble Wraps, Temperature-Controlled Bubble Wraps, Other Specialty Wraps), By End-Use Industry (E-commerce & Retail, Electronics, Automotive, Consumer Goods, Food & Beverage, Pharmaceuticals, Other Industrial Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Company Coverage: Analysis and profiles of 15+ companies, including Sealed Air Corporation, Pregis LLC, Smurfit Kappa Group, DS Smith plc, and others

Methodology

The analysis is conducted using a robust, multi-step methodology integrating primary and secondary research sources. Primary research involved interviews with industry executives, packaging engineers, and supply chain managers, while secondary research encompassed company annual reports, regulatory publications, and industry journals. Quantitative models and forecasting techniques, including trend extrapolation and CAGR-based analysis, were applied to historical data from 2021–2024 to generate projections through 2034. Market sizing considered production capacity, regional consumption patterns, material costs, and end-use demand dynamics. Competitive benchmarking evaluated R&D capabilities, product portfolios, mergers and acquisitions, and sustainability initiatives of key players. USDAnalytics applied rigorous validation protocols to ensure accuracy, relevance, and reliability of insights, providing a comprehensive understanding of market trends, emerging opportunities, and challenges shaping the global Bubble Wrap Packaging landscape.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.