Market Overview: Inflatable Packaging to Reach $4.1 Billion by 2034 Driven by E-commerce and Sustainable Materials

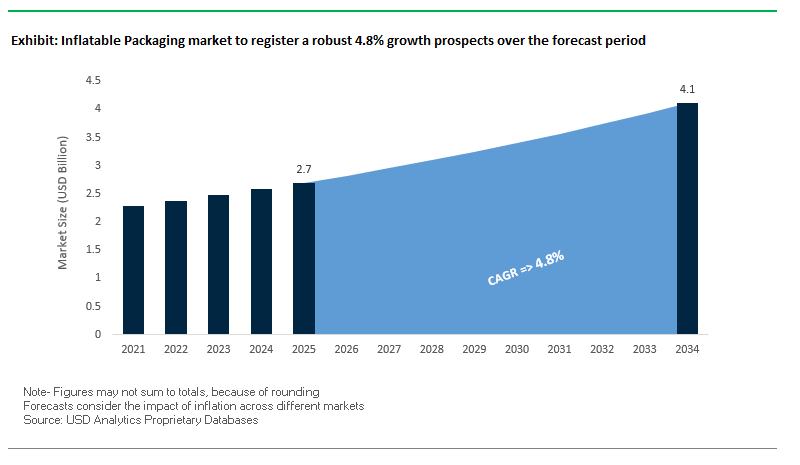

The global inflatable packaging market is projected to grow from $2.7 billion in 2025 to $4.1 billion by 2034, at a steady CAGR of 4.8%. This sector is rapidly becoming indispensable for supply chain managers, e-commerce platforms, and manufacturers of fragile goods. The value proposition lies in lightweight, on-demand protection that reduces transportation emissions, lowers storage costs, and provides maximum product safety. As brands pivot toward eco-conscious solutions, recyclable PE films and paper-based inflatable cushions are reshaping the market landscape.

Key Insights for Industry Stakeholders

- E-commerce growth fuels adoption: Online retail demands flexible, void-fill protection for diverse products.

- Cost and carbon reduction: Inflatable packaging reduces warehouse space and logistics expenses by shipping flat.

- Superior protection: Air cushions prevent product movement and damage during long-haul delivery, critical for electronics and cosmetics.

- Sustainable shift: Movement toward recyclable PE and paper-based systems addresses regulatory and consumer sustainability demands.

Market Analysis: Strategic Developments from 2024–2025 Reshape the Inflatable Packaging Sector

Between 2024 and 2025, leading players accelerated innovation and expansion to meet e-commerce and sustainability challenges. In August 2025, Pregis launched EasyPack GeoTerra paper cushioning, a curbside-recyclable solution combining premium protection with sustainability. The same month, Smurfit Kappa completed its merger with WestRock, forming Smurfit WestRock, a powerhouse in recyclable paper-based packaging, which directly impacts future adoption of paper inflatable systems.

Sustainability milestones also defined progress. In June 2025, DS Smith reaffirmed its commitment to eliminate 1 billion pieces of problem plastics by the end of 2025 through paper cushioning innovations. In April 2025, Sealed Air introduced its BUBBLE WRAP® Rocket Inflatable Void Fill System, capable of producing 100 feet of protective pillows per minute critical for high-volume fulfillment centers. Pregis also expanded its South Carolina film operations in March 2025, increasing capacity for EVOH barrier films that enhance durability in inflatable packaging applications.

Earlier moves in late 2024 set the stage for this momentum. Pregis acquired a European protective packaging firm in November 2024 to expand globally, while Atlantic Packaging (October 2024) and DS Smith advanced paper-based, curbside-recyclable alternatives.

Trends and Opportunities Defining the Inflatable Packaging Market

Strategic On-Demand Manufacturing and Warehouse Automation Integration

The inflatable packaging market is experiencing a fundamental transformation as e-commerce giants and third-party logistics (3PL) providers replace bulk-packed void-fill with on-demand inflatable systems. By generating cushions and air pillows directly at fulfillment centers, companies eliminate the need to store bulky void-fill products like peanuts or bubble wrap, reducing storage requirements and transportation costs for packaging inventory. For example, Sealed Air’s on-demand solutions demonstrate that a single roll of flat film can yield the equivalent of an entire pallet of loose-fill material, creating immense space and cost savings.

This trend is tightly linked to the adoption of automation in warehouse operations. Inflatable packaging systems are increasingly integrated into robotic pick-and-pack and automated lines to boost efficiency. A logistics provider noted that by adopting automated inflatable packaging lines, clients reduced labor by 40–60% while simultaneously achieving a 50% increase in throughput. Moreover, companies such as Packsize are advancing right-sizing technologies that customize packaging to product dimensions, reducing film usage, cutting shipping costs, and ensuring better product protection. Collectively, these innovations underscore how inflatable packaging is moving from a secondary material choice to a core element of modern e-commerce logistics efficiency.

Rapid Material Transition to Recyclable and Mono-Material Films

Sustainability pressures are reshaping material choices in the inflatable protective packaging sector, with regulators and brands driving a decisive transition away from multi-laminate films toward mono-material polyethylene (PE) and polypropylene (PP). These new formats are designed to be fully recyclable in store drop-off systems, ensuring compliance with legislation such as the EU’s Packaging and Packaging Waste Regulation (PPWR).

Material innovation is accelerating, with one chemical company partnering with a converter and machinery provider to develop a 7-layer mono-material MDOPE film incorporating an EVOH barrier a significant leap in recyclable oxygen-barrier performance. At the same time, brands are demanding recycled content as part of their ESG targets. A leading protective packaging supplier recently launched a new air pillow line with 95% recycled plastic, combining post-industrial and post-consumer waste streams to meet corporate sustainability goals. These developments highlight how recyclability and PCR integration are no longer optional add-ons but industry standards for inflatable packaging.

Development of Performance-Enhanced Bio-Based and Compostable Films

Beyond recyclability, a major opportunity lies in developing bio-based and compostable inflatable films that eliminate fossil-fuel inputs and address contamination issues. Academic research has already yielded a polylactic acid (PLA) film derived from 80% bio-based sources, compatible with conventional film processing, representing a breakthrough for high-performance, renewable packaging.

This innovation is particularly relevant for food e-commerce applications, where packaging contamination complicates recycling. Compostable inflatable films provide a clear end-of-life solution by allowing packaging to degrade naturally with food residues. Companies in Europe have introduced self-inflating air cushions made from recyclable and biodegradable films, showing market demand for alternatives that align with circular economy goals. For brands with ambitious carbon neutrality and zero-plastic commitments, performance-enhanced bio-based films represent a strategic pathway to combine product protection with climate-friendly credentials.

Expansion into High-Value, Industrial Non-E-Commerce Applications

While e-commerce remains the primary growth driver, the industrial, automotive, and electronics sectors offer untapped opportunities for inflatable packaging adoption. The technology’s ability to create a 360-degree protective barrier makes it particularly suitable for high-value components such as medical devices, electronics modules, and automotive parts, where vibration, shock, and compression resistance are critical.

Inflatable dunnage bags are already widely used for freight and pallet stabilization, filling voids inside shipping containers and preventing cargo movement during rail, sea, or road transport. Compared to traditional protective materials like foam or corrugated inserts, inflatable packaging is lighter, reusable, and more space-efficient when deflated, dramatically reducing storage and shipping costs. As industries seek both efficiency and sustainability, inflatable packaging offers a compelling alternative for B2B logistics, positioning suppliers to diversify beyond e-commerce into resilient industrial supply chains.

Competitive Landscape: Innovation, Automation, and Sustainability Define Market Leaders

The inflatable packaging market is highly competitive, featuring global multinationals and niche sustainability-driven challengers. Companies compete on automation integration, lightweight materials, recyclable designs, and paper-based alternatives. Below are the profiles of leading players shaping the sector.

Sealed Air Corporation Market leader with iconic BUBBLE WRAP® systems

Sealed Air dominates through its BUBBLE WRAP® brand and Rocket/Flex on-demand systems, enabling packaging creation at fulfillment sites. Its automation-ready solutions cut logistics costs and free up warehouse space. Beyond plastics, the company invests in recyclable Jiffy® paper mailers and sustainability-focused innovations under its CRYOVAC® line. Its global brand recognition and integrated equipment + material offering position Sealed Air as the benchmark in e-commerce, electronics, and food applications.

Pregis LLC Scaling sustainable cushioning and barrier film capacity

Pregis, with its AirSpeed® brand, offers a broad portfolio of air pillows and cushions plus integrated inflation systems. In August 2025, it introduced GeoTerra paper cushioning, furthering its recyclable packaging push. Expansion in March 2025 boosted EVOH barrier film capacity to improve performance for high-value applications. Pregis is guided by its “2k30” sustainability goals, committing to 100% recyclable or reusable output, while its systems streamline supply chain integration for customers globally.

Atlantic Packaging Pioneer in curbside-recyclable cushioning and bio-foam alternatives

Atlantic Packaging emphasizes paper mailers and paper cushioning as substitutes for plastic. Its innovations include Canopy™ Wrap (recyclable bottle bundling) and Cruz Foam (bio-based foam alternatives). The company promotes optimization with its “reduce your footprint” strategy, offering not just materials but also consulting to improve packaging efficiency. Its strong sustainability-first culture helps position it as a preferred partner for eco-conscious e-commerce brands.

Smurfit Kappa Group PLC Paper-based giant expanding through WestRock merger

Smurfit Kappa, now merged with WestRock (July 2025), has become one of the largest global providers of paper packaging. Its cushioning and void-fill systems compete directly with inflatable solutions by offering sustainable, recyclable paper options. With its SupplySmart optimization tools and wide global network, Smurfit WestRock can challenge plastic inflatable formats with large-scale, paper-based alternatives across multiple consumer industries.

DS Smith PLC Circular economy leader removing plastic from protective packaging

DS Smith focuses exclusively on corrugated and paper-based protective packaging, with the ambitious target of eliminating 1 billion pieces of plastic by 2025. Its Circular Design specialists engineer recyclable cushioning and inserts that rival traditional inflatable plastics. The company’s “Now and Next” strategy ensures 100% recyclable packaging, aligning with major retailers’ plastic reduction goals. Its expertise in corrugated-based cushioning positions DS Smith as a transformative competitor against plastic inflatable suppliers.

Inflatable Packaging Market Share Insights

Air Pillows Lead Inflatable Packaging Market Share by Product Type

Within inflatable packaging, air pillows secure the largest share at 40% in 2025, reflecting their role as the workhorse of modern e-commerce and logistics. Their dominance stems from efficiency: deflated storage reduces warehouse space, and automated inflation systems enable rapid deployment for void-fill applications. Bubble wrap continues to hold a strong share as the iconic protective medium, particularly in wrapping and cushioning fragile goods, though its growth is tempered by sustainability concerns and competition from lighter void-fill solutions. Air column bags are gaining ground as premium cushioning for electronics and fragile goods, while dunnage bags dominate in block-and-brace applications for industrial and container shipping. Air cushions represent the smallest segment, addressing specialized packaging needs. Together, these dynamics show how air pillows drive scalability, bubble wrap maintains versatility, and column and dunnage bags expand high-performance, application-specific use cases.

Void Fill Dominates Inflatable Packaging Market Share by Application

By application, void fill accounts for 50% of the inflatable packaging market in 2025, underpinned by the exponential growth of e-commerce and fulfillment logistics. Air pillows lead this segment by delivering fast, low-cost protection against product movement in transit, making them indispensable for high-volume shippers. Cushioning applications follow, leveraging bubble wrap, air columns, and air cushions to protect fragile, high-value goods where performance trumps cost. Wrapping continues to serve a critical role for fragile items that require individual isolation and abrasion protection, even as automation-friendly solutions gradually encroach. Block and brace, while smaller in share, remains indispensable for industrial logistics, securing entire pallet loads during long-haul transport with dunnage bags. The segmentation highlights how void fill has become the core demand driver, while cushioning and block-and-brace applications carve out essential niches in both consumer and industrial supply chains.

United States: E-Commerce Expansion and Sustainable Innovations Driving Growth

The U.S. inflatable packaging market is witnessing significant growth driven by the booming e-commerce and logistics sectors. Companies increasingly demand lightweight and efficient void fill and cushioning solutions to minimize shipping costs and reduce product damage. Automation is a key trend, with on-demand inflatable packaging systems producing air pillows and cushions to streamline operations and address labor shortages in high-volume e-commerce fulfillment centers. Sustainability is a critical driver, with manufacturers developing films containing post-consumer recycled (PCR) content in response to California’s SB-54 EPR law and PFAS-free mandates. Innovations in lightweighting reduce material usage and transportation costs while improving operational efficiency. Additionally, specialized applications in the medical and pharmaceutical sectors are expanding, where inflatable packaging is used to protect fragile, high-value equipment requiring superior cushioning during transit.

Germany: Circular Economy and Paper-Based Solutions Leading Market Development

Germany’s inflatable packaging market is shaped by strict regulations and a strong focus on sustainability. The German Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR) drive demand for eco-friendly materials and recyclable solutions. Germany has emerged as a leader in the circular economy, with manufacturers collaborating with end-users to develop packaging systems that use high recycled content and are fully recyclable. A notable trend is the rise of paper-based inflatable packaging, offering plastic-free alternatives that integrate seamlessly with cardboard boxes. These innovations not only comply with regulatory frameworks but also meet growing consumer and corporate sustainability expectations, solidifying Germany’s leadership in environmentally responsible packaging solutions.

China: E-Commerce Surge and Automated Packaging Technologies Fuel Market Expansion

China’s inflatable packaging industry is propelled by the rapid growth of e-commerce and logistics sectors, which demand secure and efficient packaging to protect products during shipping and handling. Government initiatives aimed at reducing over-packaging in express delivery services are encouraging manufacturers to adopt eco-friendly and reusable packaging solutions, reinforcing sustainability in the supply chain. Technological advancements are another key factor, with companies investing in automation and AI-powered packaging systems to enhance production efficiency, improve equipment stability, and meet the high-volume demands of modern logistics networks. The integration of robotics in production and fulfillment further expands opportunities for inflatable packaging designed for automated handling.

India: E-Commerce Growth and Cost-Effective Sustainable Solutions Driving Market Demand

India’s inflatable packaging market is strongly influenced by the rapid expansion of e-commerce, which creates high demand for secure, lightweight, and durable packaging solutions that enhance the consumer unboxing experience. Regulatory frameworks, including the Plastic Waste Management (Amendment) Rules, 2022 and the draft Extended Producer Responsibility (EPR) Rules, 2024, are driving the adoption of sustainable alternatives and promoting a circular economy. The market’s cost-sensitive nature incentivizes the development of efficient, compact, and affordable inflatable packaging solutions, balancing performance with operational economics. Manufacturers are increasingly designing products that reduce shipping costs while remaining easy to handle and environmentally responsible, reflecting the dual priorities of sustainability and cost-efficiency in India.

Brazil: Circular Economy Policies and Bioplastics Innovation Shaping Market Dynamics

The Brazilian inflatable packaging market is heavily shaped by government initiatives promoting a circular economy through the National Solid Waste Policy, mandating reverse logistics for packaging waste. This Extended Producer Responsibility (EPR) framework enhances recycling rates and encourages manufacturers to adopt recyclable materials. Rapid growth in Brazilian e-commerce has fueled demand for secure and efficient packaging solutions, including inflatable options. Additionally, innovations in bioplastics, such as green polyethylene produced from sugarcane ethanol, are influencing the market by reducing dependence on fossil fuels and promoting sustainable alternatives. These developments are driving competitive pressure and stimulating further innovation across the packaging sector.

Japan: Automation, Quality, and Recycling Initiatives Driving Market Leadership

Japan’s inflatable packaging market is propelled by a highly developed e-commerce sector and a high proportion of single-person households, creating strong demand for automated, lightweight, and efficient packaging solutions. The government’s commitment to recycling through the Plastic Resource Circulation Act fosters a supportive environment for paper-based inflatable packaging, which is easily recyclable and aligns with sustainability goals. The Japanese market also emphasizes product quality and safety, with manufacturers prioritizing the production of reliable inflatable packaging capable of withstanding shipping stresses while maintaining product integrity. These trends collectively reinforce Japan’s position as a leader in technologically advanced, safe, and sustainable inflatable packaging solutions.

Inflatable Packaging Market Report Scope

Inflatable Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.1 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Air Pillows, Air Bubble Wraps, Air Dunnage Bags, Air Cushions, Air Column Bags), By Material (Polyethylene, Polypropylene, Polyvinyl Chloride, Recycled Plastics, Paper & Paperboard), By Application (Void Fill, Cushioning, Block and Brace, Wrapping), By End-Use Industry (E-commerce, Electronics & Electricals, Food & Beverages, Pharmaceuticals & Medical Devices, Automotive, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Pregis LLC, Ranpak Holdings Corp., Storopack Hans Reichenecker GmbH, International Paper, Automated Packaging Systems, Inc., Smurfit Kappa Group plc, Veritiv Corporation, Macfarlane Group PLC, The Intertape Polymer Group Inc., Fromm Packaging Systems, Free-Flow Packaging International Inc. (FP International), Shurtape Technologies, LLC, Kite Packaging, Zezhi Packaging Technology Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Inflatable Packaging Market Segmentation

By Product Type

- Air Pillows

- Air Bubble Wraps

- Air Dunnage Bags

- Air Cushions

- Air Column Bags

By Material

By Application

- Void Fill

- Cushioning

- Block and Brace

- Wrapping

By End-Use Industry

- E-commerce

- Electronics & Electricals

- Food & Beverages

- Pharmaceuticals & Medical Devices

- Automotive

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Inflatable Packaging Market

- Sealed Air Corporation

- Pregis LLC

- Ranpak Holdings Corp.

- Storopack Hans Reichenecker GmbH

- International Paper

- Automated Packaging Systems, Inc.

- Smurfit Kappa Group plc

- Veritiv Corporation

- Macfarlane Group PLC

- The Intertape Polymer Group Inc.

- Fromm Packaging Systems

- Free-Flow Packaging International Inc. (FP International)

- Shurtape Technologies, LLC

- Kite Packaging

- Zezhi Packaging Technology Co., Ltd.

*List not Exhaustive

Research Coverage

This report investigates the global inflatable packaging market, providing a comprehensive analysis of industry dynamics, technological breakthroughs, and emerging sustainability trends shaping the sector from 2025 through 2034. USDAnalytics’ analysis reviews innovations in air pillows, bubble wraps, dunnage bags, and air column bags, highlighting breakthroughs in recyclable polyethylene (PE), polypropylene (PP), and paper-based inflatable systems that reduce logistics costs, carbon emissions, and storage requirements. This report emphasizes how e-commerce growth, warehouse automation, and right-sizing technologies are transforming supply chain efficiency, while sustainable and compostable materials are becoming critical differentiators for industry leaders. Strategic developments in on-demand inflation systems, bio-based films, and high-barrier EVOH laminates are explored, providing insights into material performance, production scalability, and circular economy initiatives. The report highlights competitive moves, capacity expansions, and mergers that strengthen global market positioning, making this report an essential resource for packaging engineers, logistics managers, R&D leaders, and sustainability officers aiming to optimize product protection, reduce environmental impact, and capture emerging opportunities across consumer and industrial applications.

Scope Highlights

- Segmentation: By Product Type (Air Pillows, Air Bubble Wraps, Air Dunnage Bags, Air Cushions, Air Column Bags), By Material (Polyethylene, Polypropylene, Polyvinyl Chloride, Recycled Plastics, Paper & Paperboard), By Application (Void Fill, Cushioning, Block and Brace, Wrapping), By End-Use Industry (E-commerce, Electronics & Electricals, Food & Beverages, Pharmaceuticals & Medical Devices, Automotive, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ companies including Sealed Air Corporation, Pregis LLC, Ranpak Holdings Corp., Storopack Hans Reichenecker GmbH, International Paper, Smurfit Kappa Group plc, Veritiv Corporation, Macfarlane Group PLC, and others.

Methodology

The research methodology for this report integrates primary interviews, secondary data collection, and proprietary analytics to deliver actionable insights for industry professionals. USDAnalytics leveraged market intelligence from company annual reports, regulatory filings, trade journals, and logistics data, complemented by insights from packaging engineers, sustainability managers, and supply chain executives. Quantitative analysis involved bottom-up market sizing using historical production volumes, material consumption trends, and adoption rates of air pillows, bubble wraps, and other inflatable products. Forecasts to 2034 incorporate macroeconomic indicators, e-commerce growth, technological integration in fulfillment centers, and sustainability mandates such as EPR and PPWR. Competitive benchmarking evaluated innovation in recyclable films, compostable materials, on-demand inflation systems, and automation integration, ensuring that projections reflect both current industry practices and emerging trends. This methodology provides a high-fidelity roadmap for strategic decision-making in packaging, logistics, and sustainability planning.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.