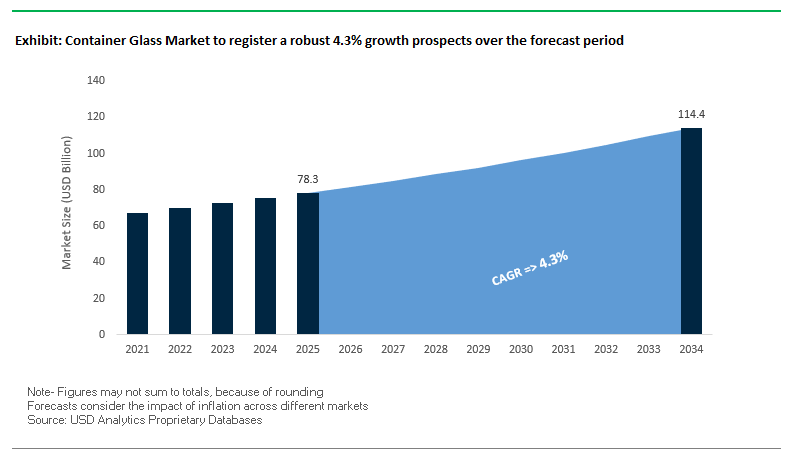

Market Overview: Global Container Glass Market Valued at $78.3 Billion in 2025

The Global Container Glass Market is valued at USD 78.3 billion in 2025 and is expected to reach USD 114.4 billion by 2034, expanding at a steady CAGR of 4.3%. The industry is entering a pivotal stage where circular economy mandates, lightweighting innovations, and energy efficiency measures are reshaping the production and adoption of glass packaging. For manufacturers and brand owners, container glass is not only a functional and aesthetic choice but also a strategic tool for decarbonization and premiumization.

A defining driver is the growing reliance on cullet (recycled glass content). For every 10% of cullet integrated, energy consumption falls by 5% and carbon dioxide emissions drop by 12%, making it central to both cost optimization and ESG reporting. Premium beverages including spirits, wines, and craft beers continue to anchor demand for glass bottles, leveraging their weight, tactile feel, and recyclability to differentiate from alternative packaging.

The industry is also innovating with lightweight bottles, which are now up to 30% lighter than conventional designs while maintaining structural strength. Meanwhile, cold-end coatings are being deployed to enhance scratch and impact resistance by 20%, reducing breakage during high-volume filling and logistics. These advancements demonstrate how container glass is evolving beyond tradition, becoming a science-driven material aligned with efficiency, sustainability, and branding goals.

Key Insights for Industry Professionals:

- Market Size 2025: USD 78.3 Billion | 2034: USD 114.4 Billion | CAGR: 4.3%

- Cullet adoption: 10% cullet = 5% less energy + 12% lower CO₂ emissions.

- Premium dominance: Bottles remain core to spirits, wine, and craft beer markets.

- Lightweight glass: Up to 30% weight reduction improves logistics and costs.

- Cold-end coatings: Enhance durability and reduce breakage by ~20%.

- Circular economy: Industry pivoting toward full recyclability and closed-loop systems.

Market Analysis: Strategic Developments Driving the Container Glass Industry in 2025

The container glass industry in 2025 is marked by a series of strategic initiatives, restructuring efforts, and sustainability breakthroughs across major markets.

In August 2025, GCA accelerated its global expansion with investments in Türkiye and Europe, signaling an aggressive strategy to strengthen supply in growth regions. That same month, the Glass Packaging Institute (GPI) launched an industry coalition targeting small-format recovery, addressing one of the biggest recyclability gaps in the sector. Also in August, Beta Glass reported a 63% revenue surge in its half-year results, underscoring strong demand in emerging markets.

Innovation continues to shape the landscape. In July 2025, Verallia introduced Vista glass, made entirely from 100% post-consumer recycled (PCR) content, setting a new industry benchmark for circular packaging. In contrast, O-I Glass terminated its costly MAGMA project in July, pivoting toward a cost-driven profitability model. Meanwhile, in June 2025, GPI announced the 2025 Clear Choice Awards, recognizing design and sustainability excellence, while also publicly challenging U.S. DOE funding cuts for industrial decarbonization, stressing glass’s role as a strategic manufacturing sector.

Earlier in March 2025, HORN completed 12 furnace start-ups, a key indicator of continuous investment in capacity expansion and modernization. Collectively, these developments reflect an industry balancing cost competitiveness with sustainability imperatives. Established leaders are accelerating cullet integration and lightweighting, while industry associations are pushing governments for equitable support in decarbonization funding.

Transformative Trends and Strategic Opportunities in the Container Glass Market

Accelerated Demand for High Cullet Content Driven by Corporate Sustainability Mandates

The container glass market is experiencing a paradigm shift as leading consumer goods companies set ambitious sustainability targets that significantly increase the demand for high-cullet-content glass. Anheuser-Busch InBev (AB InBev), for instance, is targeting net zero across its value chain by 2040, highlighting circular packaging including recycled glass integration as a key pillar. The environmental benefits of using cullet are compelling: every 10% increase in recycled glass reduces energy consumption by 3% and carbon emissions by 5%, providing a tangible incentive for glass manufacturers to innovate. Companies like O-I Glass are proactively investing in cullet supply chains, such as the Glass to Glass Denver facility, ensuring a steady source of high-quality recycled material. Legislative pressures, such as Washington State’s mandate requiring certain glass containers to contain at least 35% post-consumer recycled content, further strengthen the demand-pull for cullet, ensuring long-term market growth for sustainable glass packaging.

Strategic Investment in Lightweighting and Hybrid Forming Technologies

To reduce environmental impact and transportation costs, leading glass manufacturers are aggressively investing in lightweighting and hybrid forming technologies. O-I Glass’s MAGMA (Modular Advanced Glass Manufacturing Asset) technology has enabled a 7.4% reduction in bottle weight, demonstrating that advanced manufacturing processes can achieve substantial sustainability gains without compromising structural integrity. Lightweighting also directly reduces emissions; in 2022, O-I Glass saved over 5,000 tons of glass through this initiative, equivalent to 16.2 million beer bottles. Hybrid technologies, like Ardagh Group’s NextGen hybrid electric furnace, further decouple production from fossil fuels, achieving up to a 64% reduction in carbon emissions for amber glass containers. These innovations position manufacturers to deliver both cost-effective and environmentally sustainable glass packaging solutions.

Development of Ultra-Low Carbon Melting Technologies (Hydrogen, Electric, Hybrid)

The transition to ultra-low carbon melting represents a critical opportunity for first movers in container glass manufacturing. Hydrogen pilot projects, such as the 30-tonne-per-day pilot furnace by Glass Futures in the UK, are demonstrating industrial-scale hydrogen-based melting with significant energy and emission reductions. Hybrid electric furnaces, exemplified by Ardagh’s NextGen system, show the commercial feasibility of producing up to 350 tons per day while cutting carbon footprints. Collaborative projects like Germany’s ZeroCO2Glas, funded by BMWK, aim to further reduce energy consumption by 15% and achieve CO2-neutral glass melting. Early adoption of these technologies will allow manufacturers to meet stringent regulatory requirements while securing competitive advantages in sustainability-focused markets.

Integration of Digital Watermarks for High-Fidelity Closed-Loop Recycling

Digital watermarking technologies, including initiatives like HolyGrail 2.0, offer container glass manufacturers a pathway to high-precision recycling and circularity. These watermarks enable automated detection and sorting of glass containers, ensuring high-purity food-grade cullet. Trials have achieved a 99% detection rate, demonstrating the potential to significantly improve recycling efficiency. Beyond recycling, digital watermarks provide direct-to-consumer engagement opportunities by delivering sustainability credentials, recycling instructions, or marketing content via smartphone scanning. This dual functionality adds value to both manufacturers and end-users, transforming traditional glass containers into interactive, sustainability-compliant assets.

Competitive Landscape: Leading Companies in the Container Glass Market

The global container glass market is defined by multinational players who combine scale, R&D, and sustainability commitments to maintain leadership. Strategic moves in 2025 emphasize restructuring, recycled content integration, and premium product innovation.

O-I Glass, Inc.: Restructuring to Drive Profitability

O-I remains a global leader with 69 manufacturing plants across 19 countries. In 2025, its “Fit to Win” program delivered $145 million in savings, boosting EPS guidance by up to 90%. The company shifted focus away from the high-cost MAGMA project, instead emphasizing cullet integration with a target of 40% global recycled content use. Its portfolio spans bottles and jars for beer, wine, spirits, and food, with strengths in global reach and operational optimization.

Ardagh Group S.A.: Recapitalization and Eco-Light Bottles

Ardagh operates one of the largest glass divisions globally under Ardagh Glass Packaging (AGP). In August 2025, it secured majority support for recapitalization plans, leading to creditors assuming control from founder Paul Coulson. Despite restructuring, Ardagh continues to push sustainable innovation, including Eco-Light bottles designed for lightweighting and lower transportation costs. Its strategic focus remains on circularity and carbon reduction across its glass and metal packaging businesses.

Verallia S.A.: Launching 100% PCR Glass Solutions

Verallia, Europe’s largest and the world’s third-largest container glass producer, is positioning itself as a circular economy leader. In July 2025, it launched Vista glass, made entirely from post-consumer recycled content, reinforcing its ESG-driven strategy. The company is expanding capacity with two new furnaces in Spain and Italy by 2026. Its long-term vision is to “re-imagine glass for a sustainable future,” focusing on maximum cullet use, lightweighting, and design flexibility.

Gerresheimer AG: Strategic Realignment Toward Pharma Core

Gerresheimer, traditionally strong in special-purpose glass for pharma and biotech, also serves food and beverage packaging. In August 2025, it announced plans to divest its moulded glass division, sharpening focus on high-value pharma containers. Despite this shift, it continues to offer compliant solutions for food and beverages. Its strategy includes 50% CO₂ reduction by 2030 and 100% renewable electricity procurement. Gerresheimer’s strength lies in regulatory compliance, hygiene standards, and high-quality production expertise.

Stoelzle Glass Group: Expanding Premium Spirits and Eco-Design

Stoelzle is an international leader in premium flint glass packaging for spirits, perfumery, and pharmaceuticals. In 2025, it launched EcoSecur, a new Type 2 glass that reduces chemical use and environmental impact. Stoelzle also expanded its lightweight bottle portfolio with minimalist designs, targeting sustainability-conscious premium brands. Under new leadership, the company is broadening access to premium stock bottles with low minimum order quantities, catering to both large distillers and boutique producers.

Container Glass Market Share Insights

Bottles Dominate Market Share by Product Type in Container Glass Industry

Glass bottles account for approximately 65% of the global container glass market, reflecting their undisputed dominance across the food and beverage packaging landscape. Their leadership is driven by colossal demand from alcoholic beverages (beer, wine, spirits) and non-alcoholic drinks (soft drinks, water, juices), where glass remains the material of choice for its inertness, recyclability, and premium image. In addition to the beverage sector, bottles hold critical importance in edible oils, sauces, and condiments, where consumer trust in purity and safety underpins their preference for glass over plastic alternatives. The ability of glass bottles to provide an impermeable barrier against oxygen and moisture ensures extended shelf life, which is especially crucial for premium beverages and perishable products. With global beverage production exceeding hundreds of billions of liters annually, bottles secure their position as the volume king of the container glass industry.

Food and Beverages Retain the Largest Market Share by End-Use in Container Glass Industry

The food and beverage sector dominates container glass demand, commanding around 70% of market share and serving as the backbone of the entire industry. This overwhelming leadership is tied to the sheer scale of bottled beverage consumption globally and the increasing trend of consumers shifting away from plastics toward sustainable and recyclable packaging formats. Glass is perceived as a premium, eco-friendly material that enhances brand equity, particularly in wine, spirits, and craft beverages where packaging directly influences consumer purchasing decisions. In the food industry, glass jars and bottles maintain strong demand for sauces, condiments, and baby food, supported by consumer perceptions of product safety and purity. Regulatory and policy initiatives in regions like the EU, which are accelerating bans on single-use plastics, further reinforce the preference for glass packaging. As global food and beverage volumes continue to expand, this end-use sector will remain the industry’s engine of growth, shaping innovation in lightweight glass, refillable formats, and high-speed production technologies.

United States: Regulatory Shifts and Premium Applications Drive the Container Glass Market

The container glass market in the United States is evolving rapidly under stricter environmental regulations and rising sustainability commitments. California’s Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54) is setting a benchmark by mandating higher recyclability and reusability, creating strong growth opportunities for glass packaging. This aligns with consumer and corporate preferences for sustainable, long-lasting materials. The industry is also witnessing a green shift with launches like Ardagh Group’s 2024 line of craft beverage bottles, made from 100% recyclable glass. These initiatives highlight how container glass is being positioned as an eco-friendly solution in response to plastic reduction mandates.

Innovation and investment are central to the U.S. container glass market. O-I Glass’s $100 million investment in a new production plant in Mexico to serve North American beverage brands underlines capacity expansion trends, while lightweighting technologies are gaining traction to reduce costs and enhance transport efficiency. The food and beverage sector remains the largest application, with craft beer, wine, and spirits driving demand, alongside growing requirements from the pharmaceutical and cosmetics industries for premium, safe, and specialized glass containers. E-commerce is another major growth catalyst, as brands seek durable yet visually appealing glass containers that can withstand shipping pressures. Corporate adoption, like Olay’s 2025 launch of its Super Cream in a glass jar, reflects how brands are leveraging glass for both sustainability and a premium consumer image.

Germany: Circular Economy and EU PPWR Regulations Reshape Container Glass Industry

Germany’s container glass market operates within one of the strictest recycling and packaging frameworks in the world, driven by the EU Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. The regulation requires all packaging to be fully recyclable by 2030 and sets ambitious targets for recycled content and reuse. Complementing this, Germany’s Packaging Act (Verpackungsgesetz) enforces producer responsibility across the packaging lifecycle, incentivizing innovation in recyclability and eco-friendly materials.

German manufacturers are global leaders in sustainable packaging innovation, responding to regulatory demands with next-generation solutions. For example, Gerresheimer AG introduced a glass jar with a bio-based forewood closure in 2024, combining traditional glass durability with renewable materials. This reflects how sustainability goals are driving product development in pharmaceuticals, cosmetics, and food packaging. With EU mandates focusing on recyclability and waste reduction, German producers are investing in advanced recycling technologies and material efficiency improvements. The combination of a robust recycling system, consumer preference for eco-friendly packaging, and strong governmental mandates ensures Germany remains a frontrunner in the European container glass market.

China: Dual Carbon Goals and High-Tech Manufacturing Expand Container Glass Market

China’s container glass market is undergoing a transformation driven by the government’s dual carbon targets of achieving carbon peak and neutrality. These initiatives are fueling a major shift toward eco-friendly, reusable packaging materials, boosting the adoption of container glass across food, beverage, and pharmaceutical industries. Policies restricting non-degradable plastics are also accelerating glass adoption as a sustainable alternative.

Technological innovation is a defining feature of the Chinese market. Manufacturers are leveraging automation, 5G-enabled industrial internet, and artificial intelligence to improve production flexibility and efficiency, aligning with the Made in China 2025 plan, which requires 70% domestic content of core materials by 2025. The country’s rapidly growing e-commerce sector is also creating strong demand for secure, tamper-proof glass containers suitable for shipping food, beverages, and personal care products. At the same time, Chinese manufacturers are enhancing product quality and reducing costs to strengthen their role as a major global export hub for affordable yet high-performance container glass.

India: Infrastructure Growth and Sustainability Policies Accelerate Container Glass Adoption

The container glass market in India is gaining momentum due to strong governmental initiatives like Make in India and the Zero Effect Zero Defect mission, which emphasize high-quality domestic manufacturing. Supportive policies such as the Production Linked Incentive (PLI) Scheme with an outlay of INR 10,900 crore for the food processing industry are stimulating investments in manufacturing infrastructure and standardized, high-quality packaging. In parallel, the Plastic Waste Management (Amendment) Rules, which phase out single-use plastics, are fueling the demand for eco-friendly glass alternatives.

India’s expanding consumer base, rising disposable income, and rapid urbanization are shifting preferences toward single-serve, on-the-go, and premium products, directly boosting demand for glass containers. The pharmaceutical and healthcare industries, driven by an aging population and rising chronic diseases, are increasingly adopting secure, tamper-evident, and child-resistant glass packaging. In the premium cosmetics and perfumery segment, PGP Glass continues to invest heavily, catering to both domestic and global brands. With a combination of regulatory push, rising consumer expectations, and corporate investments, India is emerging as one of the fastest-growing container glass markets in Asia.

Brazil: Sustainability Regulations and Capacity Expansion Strengthen the Container Glass Market

Brazil’s container glass market is being reshaped by its National Solid Waste Policy, which emphasizes a circular economy and pushes industries to move away from plastic dependency. The January 2025 law banning the import of solid waste, including plastics, has further encouraged domestic glass recycling and reuse practices. Brazil also has one of the highest glass recycling rates in Latin America, with nearly 47% of glass packaging being recycled, ensuring a consistent cullet supply for new container production.

Technological modernization is a strong driver, with manufacturers adopting robotics and AI to enhance efficiency and improve defect detection. Strategic investments also play a pivotal role, as seen in Owens-Illinois’ expansion of its São Paulo facility in 2024 to meet the growing demand from beverage brands. Sustainability commitments are encouraging brands to choose glass as an eco-friendly and premium packaging solution for beverages, pharmaceuticals, and cosmetics. With strong recycling infrastructure, rising consumer awareness, and global players investing in capacity expansion, Brazil is becoming a key hub for sustainable container glass production in Latin America.

Japan: Advanced Recycling and Bio-Based Innovations Redefine the Container Glass Market

Japan’s container glass market stands out for its advanced recycling infrastructure, anchored by the Containers and Packaging Recycling Law, which assigns recycling responsibilities to businesses and ensures efficient collection and repurposing systems. These regulations are complemented by new updates from the Ministry of Health, Labour and Welfare (MHLW) in May 2025, which introduced stricter standards for food-contact packaging, including migration limits for synthetic resin materials, indirectly supporting glass packaging adoption as a safer alternative.

The market is also shifting toward bio-based and innovative solutions. For example, LyondellBasell’s bio-based polypropylene has been incorporated into Shiseido’s packaging, showing the broader shift in Japan toward sustainable materials across cosmetics and personal care. At the same time, the container glass sector is innovating to improve functionality with products that offer high dimensional stability, resistance to deformation, and long-term performance for premium applications. Japan’s commitment to recycling, bio-based integration, and constant innovation makes it one of the most technologically advanced and sustainability-driven markets for container glass globally.

Container Glass Market Report Scope

Container Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$78.3 Billion

|

|

Market Size (2034)

|

$114.4 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product Type (Bottles, Jars, Vials & Ampoules, Decorative Containers), By End-Use Industry (Food & Beverage, Pharmaceuticals & Nutraceuticals, Cosmetics & Personal Care, Chemicals), By Glass Type (Borosilicate Glass, Soda-Lime Glass), By Capacity (Less than 50 ml, 50–250 ml, 251–500 ml, 501–1,000 ml, More than 1,000 ml)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Owens-Illinois Inc., Ardagh Group, Verallia, Vidrala, Vetropack Holding Ltd., Piramal Glass Limited, Gerresheimer AG, Nihon Yamamura Glass Co., Ltd., BA Glass B.V., Heinz-Glas GmbH & Co. KGaA, SGD Pharma, AGI Greenpac Limited, Hindusthan National Glass & Industries Ltd., Stoelzle Glass Group, Toyo Seikan Group Holdings, Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Container Glass Market Segmentation

By Product Type

- Bottles

- Jars

- Vials & Ampoules

- Decorative Containers

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Nutraceuticals

- Cosmetics & Personal Care

- Chemicals

By Glass Type

- Borosilicate Glass

- Soda-Lime Glass

By Capacity

- Less than 50 ml

- 50–250 ml

- 251–500 ml

- 501–1,000 ml

- More than 1,000 ml

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Container Glass Market

- Owens-Illinois Inc.

- Ardagh Group

- Verallia

- Vidrala

- Vetropack Holding Ltd.

- Piramal Glass Limited

- Gerresheimer AG

- Nihon Yamamura Glass Co., Ltd.

- BA Glass B.V.

- Heinz-Glas GmbH & Co. KGaA

- SGD Pharma

- AGI Greenpac Limited

- Hindusthan National Glass & Industries Ltd.

- Stoelzle Glass Group

- Toyo Seikan Group Holdings, Ltd.

* List Not Exhaustive

Methodology

The insights and projections presented in this Container Glass Market report have been meticulously compiled and analyzed by USDAnalytics using a combination of primary and secondary research methodologies, ensuring actionable intelligence for industry professionals. Primary research included in-depth interviews with leading manufacturers, brand owners, and supply chain stakeholders across key geographies such as the United States, Germany, China, India, Brazil, and Japan. Secondary research involved comprehensive examination of company annual reports, government regulations, industry publications, and market bulletins to validate trends such as cullet adoption, lightweighting innovations, ultra-low carbon melting technologies, and sustainability mandates. USDAnalytics also applied advanced forecasting models to evaluate historical data (2015–2024), current industry developments, and emerging technologies, enabling accurate projections for the market size, CAGR, and strategic growth opportunities up to 2034. The methodology emphasizes a holistic assessment of production technologies, regional regulatory frameworks, competitive landscapes, and consumer-driven trends to deliver insights that are relevant, precise, and immediately applicable for decision-makers in manufacturing, packaging, and sustainability-driven industries.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.