Global Cider Packaging Market to Reach USD 7.4 Billion by 2034 with 7% CAGR Driven by Sustainability and Format Diversification

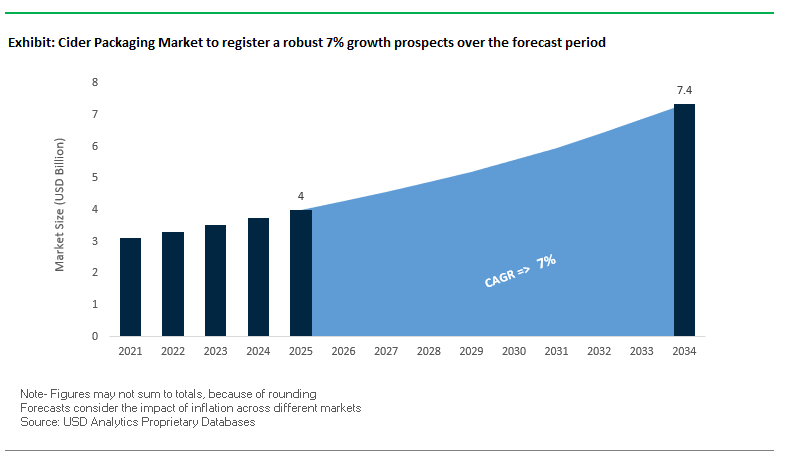

The global cider packaging market is projected to expand from USD 4 billion in 2025 to USD 7.4 billion by 2034, registering a CAGR of 7%. This growth is supported by rising consumer demand for premium and craft beverages, the increasing adoption of sustainable packaging materials, and format innovations across both on-premise and off-premise channels. Glass continues to dominate premium positioning, while aluminum cans are gaining traction due to their portability, durability, and recyclability.

The market is also being reshaped by consumer-driven sustainability preferences. High-recycled-content glass (up to 90% cullet usage) and infinitely recyclable aluminum cans are increasingly preferred, while flexible and paper-based formats are entering the cider value chain to reduce environmental impact. Moreover, packaging functionality particularly closures and liners designed to preserve carbonation and flavor is becoming a critical differentiator for cider producers competing in crowded retail spaces.

Key Insights for Industry Professionals

- Glass vs. cans dynamic: Glass dominates premium segments, while cans lead convenience-driven sales.

- Sustainability is a primary driver, with recycled glass cullet and aluminum gaining traction.

- On-premise channels use kegs and draughts, while off-premise and e-commerce lean on bottles, cans, and multipacks.

- Innovations in closures, liners, and lightweighting are extending shelf life and product quality.

Market Analysis: Sustainability and Legal Precedents Shape Cider Packaging Developments

Recent industry developments highlight how sustainability, design innovation, and regulatory cases are shaping the future of cider packaging.

In July 2025, a UK Court of Appeal partly overturned a lower court ruling, finding that Aldi’s Taurus cider packaging unfairly benefited from the branding of Thatchers, underscoring the strategic importance of distinctive, legally defensible packaging design. In the same month, Australia’s Kaiju Brewery abandoned bottles for cans, citing logistical ease, durability, and recyclability reflecting a broader consumer and producer preference shift also evident in the cider category.

On the sustainability front, producers are increasingly aligning with recycling mandates. May 2025 reports from PMMI forecasted a decline in rigid glass and plastic use, with notable increases in flexible and paper-based packaging formats a direct reflection of cider producers adapting to single-serve and ready-to-drink trends. Complementing this, the BALT-FIN-CIDER project launched in June 2025, focusing on packaging and logistics for cider exports to Australia, showing how packaging innovation is central to international market entry strategies.

Design innovation also remains at the forefront. The World Drinks Awards 2025 (June) and Wine Packaging Masters (August 2025) celebrated top packaging designs, influencing cider brand strategies toward premium, visually distinctive, and shelf-ready packaging. Meanwhile, product innovation is influencing format requirements: AVID Cider’s passion fruit tangerine launch in February 2025 emphasized gluten-free, fruit-based credentials, further driving packaging that communicates authenticity and health-conscious branding.

Transformative Trends and Emerging Opportunities in the Global Cider Packaging Market

Strategic Shift to Lightweighting and Alternative Materials to Reduce Environmental Footprint

The cider packaging market is witnessing a strong focus on lightweighting and material substitution as brands aim to reduce both environmental impact and production costs. Major cider producers are transitioning from heavy glass bottles to lighter glass variants and aluminum cans, which offer superior recyclability and lower transportation weight. Studies show a 500-mL aluminum can weighs just 15–20g compared to 300–500g for glass, significantly lowering energy consumption and carbon emissions during transport. Recycling aluminum consumes only 5% of the energy needed to produce new aluminum from raw bauxite, whereas glass recycling saves about 30% of production energy, providing further incentive for brands to adopt aluminum. European recycling rates for aluminum cans exceed 75% in several countries, reinforcing the environmental and operational benefits. This trend drives innovation in lightweight glass bottles while offering brands a competitive edge in sustainability-conscious markets.

Proliferation of Can Format for Premium and Craft Cider Brands

The 16oz (473ml) can has emerged as the preferred packaging format for craft and premium cider launches, offering branding flexibility, portability, and superior product protection. Cans are opaque, preventing light-induced spoilage (“light strike”), and provide a hermetic seal to maintain freshness and flavor, critical for delicate craft beverages. The 360-degree printable surface allows eye-catching graphics and brand messaging, enhancing shelf visibility for smaller and emerging brands. Additional advantages include portability, suitability for outdoor events, and faster chilling due to superior thermal conductivity; studies indicate cans can reach half their original temperature in approximately four minutes, compared to ten minutes for glass bottles. This shift to cans aligns with modern consumer lifestyles and supports the growth of premium and craft cider segments.

Adoption of Digital Printing for Limited-Edition and Personalized Cider Cans

The rise of digital printing technology in cider packaging enables brands to produce short-run, highly customized cans for seasonal campaigns, regional promotions, and limited editions. Direct-to-shape digital printing eliminates the need for plastic sleeves or labels, supporting sustainability and high-quality photorealistic designs. This flexibility reduces inventory and storage costs, minimizes overproduction, and accelerates market responsiveness. The adoption of digital printing transforms the relationship between cider brands and packaging suppliers, facilitating smaller, targeted production runs and supporting agile craft cider companies seeking a marketing edge.

Development of Functional and Bio-Based Secondary Packaging

The secondary packaging segment presents an opportunity to replace traditional plastic multipacks with 100% paper-based, bio-based, and recyclable carriers. This trend is driven by global bans on plastic rings and growing consumer demand for sustainable, functional packaging solutions. Companies such as Graphic Packaging International and Stora Enso are developing paperboard carriers and fiber-based gift boxes that are eco-friendly, visually appealing, and premium in feel. Beyond multipacks, these materials can be used for premium gifting solutions, adding value and differentiation for cider brands. The emergence of bio-based secondary packaging necessitates collaboration between cider producers, packaging designers, and material suppliers, creating a new high-value segment in the cider packaging market while supporting a bio-based circular economy.

Competitive Landscape: Leading Companies Driving Innovation in Cider Packaging

The cider packaging market is defined by global packaging leaders competing across glass, cans, and paper-based solutions, with sustainability, lightweighting, and recyclability as key differentiators.

Ardagh Group Strengthens Position with Recycled Glass Innovation

Ardagh Group remains a global leader in glass and metal cider packaging, supplying bottles and cans for multinational and craft producers. In South Africa, its Nigel facility added a new furnace enabling the use of up to 90% recycled cullet across 130+ bottle designs, demonstrating its commitment to sustainability and design versatility.

Smurfit Westrock Expands Paper-Based Packaging for Multipacks

Formed in August 2025 through the merger of Smurfit Kappa and WestRock, Smurfit Westrock is now a global leader in corrugated and paperboard cider packaging. Its strength lies in sustainable, display-ready solutions for multipacks and retail carriers. The company’s new Great Lakes hub in Wisconsin strengthens its ability to serve the North American beverage sector with eco-friendly secondary packaging.

Ball Corporation Leverages Aluminum Leadership for Cider Cans

Ball Corporation is a pioneer in aluminum can packaging, supporting cider producers embracing the global shift to cans. In August 2024, Ball’s packaging enabled Flow Beverage Corp. to launch mineral water in bottles made with 70% recycled aluminum, a trend increasingly mirrored by cider brands. Ball’s infinitely recyclable cans give cider producers a sustainability edge and logistics efficiency.

International Paper Focuses on Secondary Corrugated Packaging

International Paper provides corrugated packaging for cider transport and retail displays. Following its July 2025 divestiture of five European box plants, the company restructured its footprint to enhance competitiveness in North America. Its focus remains on sustainability and protective secondary packaging, crucial for shipping cider across both domestic and export markets.

O-I Glass Innovates with Lightweight Glass Bottles

O-I Glass, a global glass packaging leader, continues to serve premium cider producers. In 2024, it launched lightweight glass bottles, reducing material use while maintaining durability a major sustainability milestone. O-I’s expertise in premium aesthetics and structural integrity makes it a preferred partner for cider brands seeking a balance of luxury appeal and eco-responsibility.

Cider Packaging Market Share Insights

Bottles Retain Largest Market Share by Packaging Type in the Cider Packaging Industry

Bottles hold the largest share at 45% of the cider packaging market in 2025, sustaining their dominance due to strong associations with heritage, craft positioning, and premium perception. Glass bottles remain the preferred packaging for on-trade channels such as pubs, bars, and restaurants, where visual appeal and tradition strongly influence consumer choice. Despite rising competition from cans, bottles continue to anchor premium and traditional cider brands, particularly in Europe, where glass packaging carries cultural weight. Brand owners leverage bottles for premium cues, longer shelf life, and superior product protection, especially for artisanal and specialty ciders. While cans are catching up rapidly with advantages in sustainability, portability, and modern branding, bottles remain the flagship format for premium positioning in cider packaging.

Flavored Cider Commands Largest Market Share by Application in the Cider Packaging Market

Flavored cider leads with a 45% market share, highlighting how innovation in taste profiles is driving volume growth and consumer conversion from adjacent beverage categories like hard seltzers, RTD cocktails, and flavored beers. This segment has become the mainstream growth engine by appealing to younger consumers seeking sweet, approachable, and refreshing alternatives to traditional alcoholic beverages. Berry, citrus, and tropical fruit flavors dominate product launches, often packaged in cans and bottles designed to capture impulse purchase appeal in retail. The flavored cider segment also benefits from crossover marketing with RTDs and seasonal limited editions, making it a focal point for brand differentiation. While sparkling and still cider maintain cultural and traditional relevance, flavored ciders drive mainstream adoption, mass-market expansion, and continuous product innovation, cementing their role as the largest and most dynamic application segment.

United States Cider Packaging Market Accelerates with Sustainable and Lightweight Innovations

The U.S. cider packaging market is strongly influenced by federal and state regulations, with a growing emphasis on sustainability. The EPA’s “National Strategy to Prevent Plastic Pollution,” released in November 2024, has accelerated industry adoption of alternative, eco-friendly packaging materials. Companies are strategically investing in lightweight and highly recyclable materials, such as aluminum cans and lightweight glass bottles, to align with environmental policies and consumer preferences.

Technological advancements support the circular economy, exemplified by a March 2025 investment in an Ohio glass manufacturing facility to increase the use of recycled glass (cullet) in bottle production. Key applications span on-premise (bars and restaurants) and off-premise (retail and grocery) sectors. The rise of craft ciders has bolstered demand for premium glass bottles, while aluminum cans cater to convenience-driven and multi-pack consumers. Extended Producer Responsibility (EPR) bills in states like Washington and Maryland further incentivize recyclable packaging, while the rapid growth of direct-to-consumer (DTC) sales fuels innovation in e-commerce-ready, durable, and visually appealing cider packaging.

Germany Cider Packaging Market Benefits from Circular Economy Regulations and R&D Investments

Germany’s cider packaging market operates under strict EU and national regulations, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reusability by 2030. The German Packaging Act (VerpackG) emphasizes producer responsibility across the packaging lifecycle, leading to designs compatible with recycling streams and sustainable material use.

Technological innovation is a core driver, with beverage packaging machinery orders rising 18% in February 2025 to accommodate sustainable materials. Key applications include still and sparkling ciders, with a focus on premium glass bottles and functional ciders enriched with vitamins and minerals. Germany’s robust research and development ecosystem fosters collaboration between companies and research institutions, driving lighter, stronger, and eco-friendly packaging solutions that comply with regulatory demands and meet growing consumer expectations.

China Cider Packaging Market Expands with Green Policies and Domestic Innovation

China’s cider packaging industry is strongly influenced by the government’s “dual carbon” goal, promoting sustainable and energy-efficient industrial practices. Regulatory reforms include two new national standards for “Limit of Harmful Substances of Coatings,” issued on May 30, 2025, and effective June 1, 2026, aligning packaging development with international safety and environmental benchmarks.

Manufacturers are adopting automation, AI, and “5G plus industrial internet” technologies to optimize production and support flexible, high-quality packaging. Domestic manufacturing is emphasized to reduce dependence on imported technologies, while the rapid growth of the beverage and food industry, especially ready-to-drink products, drives demand. China’s active research landscape, with a high number of patents in packaging, promotes innovative materials and production methods that enhance sustainability, safety, and performance in cider packaging.

Brazil Cider Packaging Market Shaped by Sustainable Policies and Technological Integration

Brazil’s cider packaging market is influenced by the 2010 National Solid Waste Policy and new laws banning single-use disposable items, with a 2030 deadline for fully compostable or returnable packaging. Technological advancements such as robotics and AI enhance operational efficiency and quality control, enabling advanced sorting and defect detection in cider packaging processes.

Sustainability is a central focus, with growing adoption of circular economy principles. Key applications include food and beverage, with an emphasis on premium cider brands. Governmental targets for recycling, including 30% in 2025 and 50% by 2040, directly impact packaging materials and design. Corporate initiatives are investing in machinery to improve quality, sustainability, and efficiency, ensuring that Brazilian cider packaging meets both environmental and market-driven demands.

Japan Cider Packaging Market Leads with Smart and Inclusive Packaging Innovations

Japan’s cider packaging sector is a hub for advanced manufacturing and circular economy solutions. Kirin Holdings pioneered the use of chemically recycled PET resin for alcoholic beverages, demonstrating innovation in sustainable packaging. The “Plastic Resource Circulation Act” of April 2022 guides manufacturers in designing environmentally responsible packaging and reducing single-use plastics.

Smart packaging innovations, such as Heineken Strongbow cider’s incorporation of NaviLens technology in September 2025, improve accessibility for visually impaired consumers. High-performance can coatings focus on dimensional stability and resistance to deformation, while Toppan and other corporations develop recyclable, lightweight, and biodegradable packaging materials. Academic research further supports sustainability by exploring biopolymers and natural agents, solidifying Japan’s position as a leader in functional, eco-conscious, and inclusive cider packaging solutions.

Cider Packaging Market Report Scope

Cider Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4 Billion

|

|

Market Size (2034)

|

$7.4 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Material Type (Glass, Metal, Plastic, Paper & Paperboard), By Packaging Type (Bottles, Cans, Kegs & Barrels, Pouches & Bags-in-box), By Cider Type (Hard Cider, Non-Alcoholic Cider, Flavored Cider, Seasonal Cider), By End-Use (On-Premise, Off-Premise, E-commerce), By Application (Still Cider, Sparkling Cider, Flavored Cider, Specialty Cider)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Ardagh Group S.A., Ball Corporation, O-I Glass, Inc., Smurfit Kappa Group, Crown Holdings Inc., DS Smith Plc, Huhtamäki Oyj, International Paper Company, WestRock Company, Graphic Packaging Holding Company, Sonoco Products Company, Mondi Group, Tetra Pak International S.A., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cider Packaging Market Segmentation

By Material Type

- Glass

- Metal

- Plastic

- Paper & Paperboard

By Packaging Type

- Bottles

- Cans

- Kegs & Barrels

- Pouches & Bags-in-box

By Cider Type

- Hard Cider

- Non-Alcoholic Cider

- Flavored Cider

- Seasonal Cider

By End-Use

- On-Premise

- Off-Premise

- E-commerce

By Application

- Still Cider

- Sparkling Cider

- Flavored Cider

- Specialty Cider

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cider Packaging Market

- Amcor plc

- Ardagh Group S.A.

- Ball Corporation

- O-I Glass, Inc.

- Smurfit Kappa Group

- Crown Holdings Inc.

- DS Smith Plc

- Huhtamäki Oyj

- International Paper Company

- WestRock Company

- Graphic Packaging Holding Company

- Sonoco Products Company

- Mondi Group

- Tetra Pak International S.A.

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics utilizes a rigorous, data-driven approach to provide comprehensive insights into the global cider packaging market. Our methodology integrates primary research, including interviews with key packaging manufacturers, cider producers, material suppliers, and regulatory authorities, with secondary research from company reports, patent filings, sustainability disclosures, and trade publications. Market sizing, growth projections, and trend analyses cover packaging materials (glass, metal, plastic, paper & paperboard), packaging types (bottles, cans, kegs, pouches), and cider categories including hard, flavored, non-alcoholic, and seasonal variants. We also assess end-use channels spanning on-premise, off-premise, and e-commerce distribution. USDAnalytics evaluates innovations in closures, liners, digital printing, lightweighting, and smart packaging to understand product quality, shelf-life enhancement, and consumer convenience. Sustainability trends, regulatory frameworks across the U.S., EU, China, Brazil, and Japan, and technological adoption including AI, robotics, and automation are incorporated to provide actionable insights. By combining market dynamics, competitive landscape, and regional regulatory compliance, USDAnalytics delivers a detailed and forward-looking perspective that helps industry professionals optimize strategy, innovation, and investment decisions in the cider packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.