Can Coatings Market to Reach USD 5.6 Billion by 2034 with 4.2% CAGR Amid Demand for BPA-Free and Sustainable Solutions

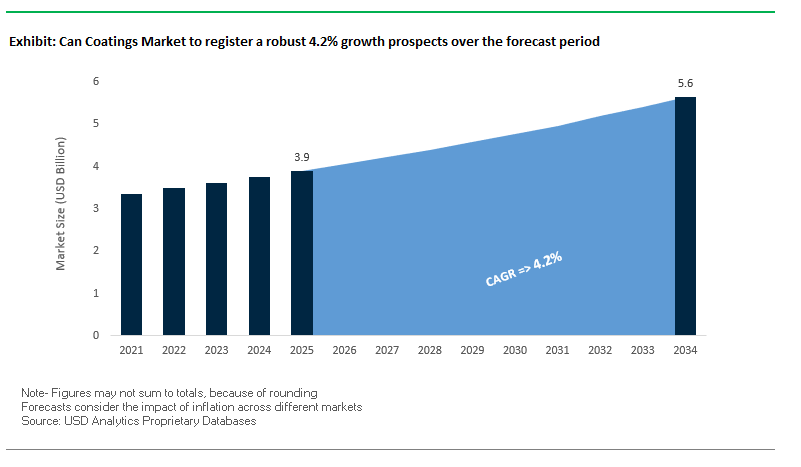

The global can coatings market is projected to grow from USD 3.9 billion in 2025 to USD 5.6 billion by 2034, registering a CAGR of 4.2%. Market expansion is driven by the increasing demand for BPA-free, PFAS-free, and sustainable coating solutions that comply with global food safety regulations. With food and beverage cans being a major packaging format worldwide, coating technologies play a critical role in ensuring product integrity, extending shelf life, and meeting consumer expectations for safety and sustainability.

Acrylic-based coatings dominate due to their excellent adhesion, transparency, and resistance to chemicals, while the industry is shifting toward water-based and bio-based alternatives to meet sustainability targets. At the same time, nanocoatings and digital process integration are enabling efficiency gains such as reduced film thickness, cutting material usage and carbon emissions by up to 20%.

Key Insights for Industry Professionals

- Market size trajectory: USD 3.9B (2025) → USD 5.6B (2034), CAGR 4.2%.

- Acrylic coatings dominate due to adhesion, gloss retention, and durability.

- BPA-free & PFAS-free demand drives product portfolio diversification.

- Sustainable water-based & bio-based coatings gaining rapid adoption.

- Nanocoatings unlock durability and regulatory compliance advantages.

Market Analysis: Regulatory Shifts and Corporate Expansions Reshape Can Coatings

The can coatings industry is witnessing regulatory tightening, portfolio diversification, and regional R&D expansions, reinforcing its pivotal role in food safety and sustainability.

In August 2025, AkzoNobel highlighted new bisphenol-free packaging coatings designed for seamless integration into existing production lines, demonstrating how manufacturers are balancing compliance with commercial viability. In July 2025, PPG Industries broadened its BPA-free and PFAS-free coatings range with three new series targeting aluminum beverage can ends, underscoring rising demand from beverage giants facing stricter regulations.

Policy shifts are also catalyzing innovation. In June 2025, the European Union revised its Packaging and Packaging Waste Regulation (PPWR), enforcing stricter recyclability requirements and driving coating formulators to deliver mono-material and recyclable solutions. Earlier, in March 2025, a global research study identified antimicrobial coatings as a rising trend to enhance the safety and longevity of packaged food and beverages, creating opportunities for differentiated offerings.

Expansion of R&D infrastructure remains central to competition. In November 2024, Beckers Group opened a new packaging coatings lab in Shanghai, strengthening its presence in Asia-Pacific one of the fastest-growing regional markets. In October 2024, AkzoNobel Packaging Coatings launched a BPA non-intent range of external beverage end coatings with multiple color options, merging regulatory compliance with consumer appeal. Similar sustainability efforts are evident in Billerud’s ConFlex CoatBase Met innovation, enabling recyclability of previously non-recyclable laminates.

Transformative Trends and Emerging Opportunities in the Can Coatings Market

Rapid Transition to BPA-NI and Next-Generation Non-BPA Coatings

The can coatings market is undergoing a significant transformation as brand owners accelerate the adoption of BPA-Non-Intent (BPA-NI) coatings, primarily acrylic and polyester-based alternatives. This trend is fueled by increasing consumer health awareness and stringent regulatory pressures, particularly in the European Union where BPA use in food containers is heavily restricted. Leading manufacturers, such as PPG, have expanded their aluminum beverage can coatings portfolio to eliminate BPA and PFAS, meeting global demand for safer packaging solutions. These next-generation coatings not only ensure compliance but also deliver enhanced durability, corrosion resistance, and aesthetic appeal, supporting brands in protecting a wide range of beverages, from beer to energy drinks. Reports indicate significant market growth in the acrylic segment, driven by superior chemical resistance and long-term performance. The move towards BPA-NI coatings thus represents a dual benefit of regulatory compliance and premium product differentiation, positioning it as a high-growth avenue within the global can coatings landscape.

Development of Polymer-Free and Functionalized Inorganic Coatings

Another key trend shaping the can coatings market is the emergence of polymer-free, ultra-thin inorganic coatings, including silica- and zirconia-based solutions applied via Plasma Enhanced Chemical Vapor Deposition (PECVD). These coatings provide an inert, robust barrier that resists chemical degradation and high temperatures, addressing both product shelf-life requirements and sustainability objectives. Academic research has demonstrated that vacuum-deposited inorganic layers can outperform conventional polymer coatings in preventing oxygen and moisture ingress while preserving recyclability, making them ideal for circular economy goals. The adoption of inorganic coatings shifts the value chain by creating demand for specialists in vacuum deposition and inorganic materials, replacing traditional polymer resin suppliers. This technological trend represents a strategic growth avenue, particularly for premium and sensitive products that require high-performance, long-lasting protection without compromising environmental standards.

Bio-Based and Compostable Coating Formulations

The can coatings market is also seeing emerging opportunities in bio-based and compostable formulations derived from renewable sources such as soy, lignin, and chitosan. Driven by growing environmental awareness and sustainability mandates, these coatings enable brands to pursue truly bio-circular packaging solutions. While still in early development for can liners, research and pilot initiatives highlight the potential to match the performance of conventional coatings in terms of heat resistance and barrier properties. For example, coatings derived from agricultural waste are being explored for their ability to withstand canning processes while providing reliable protection. Successful commercialization would allow brands to appeal to environmentally conscious consumers and differentiate in competitive markets, while also creating a new supply chain that benefits agricultural and forestry sectors.

Smart and Active Coatings with Embedded Functionality

A growing market opportunity lies in smart and active coatings that integrate advanced functionalities such as oxygen scavenging, spoilage detection, or color-change indicators for temperature abuse. These coatings address critical demands for food safety, shelf-life extension, and supply chain transparency. Academic research has explored nanoparticle-based coatings that change color in response to gases from bacterial growth, offering real-time product monitoring. Active coatings that reduce residual oxygen can extend shelf life for oxygen-sensitive products like fruit juices and sauces. The integration of such technologies transforms packaging into a high-value, interactive product, enabling brands to reduce food waste, improve consumer trust, and add measurable value. Implementation requires novel manufacturing processes and quality control systems, creating a high-revenue segment for materials with embedded functionalities.

Competitive Landscape: Leading Companies Driving the Can Coatings Market

The can coatings industry is moderately consolidated, with global leaders such as AkzoNobel, PPG, Sherwin-Williams, Valspar, Kansai Nerolac, and Beckers shaping innovation around food safety compliance, BPA-free solutions, and eco-friendly coatings.

AkzoNobel N.V. Expands BPA-Free and Color-Coating Portfolio

AkzoNobel is a global leader in packaging coatings for food, beverage, aerosol, and general cans. In August 2025, the company introduced external beverage end coatings that are BPA non-intent as standard, reflecting its safety-first strategy. With more than 40 laboratories worldwide, AkzoNobel’s strength lies in its ability to tailor global solutions to local markets, while prioritizing sustainability and regulatory compliance.

PPG Industries Enhances Aluminum Beverage End Coatings

PPG’s extensive can coatings portfolio covers internal and external food and beverage applications, with a strong emphasis on BPA-free technologies. In July 2025, it launched new aluminum beverage end coatings such as PPG Innovel PRO PPG2489 and PPG iSENSE PPG5018, positioning itself at the forefront of food safety compliance. PPG’s coatings are designed for high-speed production lines and extreme temperature resistance, reinforcing its leadership in performance-based solutions.

Sherwin-Williams Strengthens Market Position with valPure Series

Sherwin-Williams, through its valPure line, offers one of the broadest portfolios of non-BPA coatings for metal packaging. Its valPure V70 epoxy system is the first of its kind in the food and beverage can industry. By deploying its Safety by Design protocol, the company ensures scientifically validated and regulatory-compliant coatings that support global sustainability mandates.

Valspar Leverages Sherwin-Williams’ Global R&D Network

As a subsidiary of Sherwin-Williams, Valspar continues to expand its footprint in packaging coatings, offering primers and coatings for coil, extrusion, and industrial applications. By leveraging its parent company’s global R&D network and sustainability expertise, Valspar maintains a reputation for high-performance and eco-friendly coatings that align with evolving regulatory frameworks.

Kansai Nerolac Paints Strengthens Asian Market Leadership

Kansai Nerolac Paints, a leading Indian coatings manufacturer, is expanding its portfolio to capture the growing demand for food-grade can coatings. In August 2025, it launched a new line of coatings for the automotive sector, but its diversification into metal packaging coatings positions it as a key regional competitor. Its deep expertise in paints and extensive presence across India give Kansai Nerolac a strong platform to scale further in Asia’s fast-growing packaging industry.

Can Coatings Market Share Insights

Beverage Cans Hold the Largest Market Share by Application in the Can Coatings Industry

Beverage cans represent the largest segment at 45% of the can coatings industry, reflecting the sheer global volume of beer, soda, and energy drink production. Coatings here must ensure taste neutrality, corrosion protection, and high-speed line compatibility, especially with DWI (Drawn and Wall Ironed) processes used in beverage can manufacturing. The scale of global beverage consumption coupled with consumer sensitivity to off-flavors makes this segment highly demanding and a top R&D priority for coating formulators. The push toward BPA-free chemistries and next-generation acrylic and polyester coatings is driven by both regulatory mandates and brand-level sustainability commitments. While food cans capture a close second due to their technical sterilization challenges, beverage cans remain the high-volume driver that secures their leadership in market share.

Food & Beverages Dominate Market Share by End-Use in the Can Coatings Industry

The food and beverages sector commands an overwhelming 82% share of the can coatings market, cementing its position as the industry’s cornerstone. This dominance reflects the non-negotiable need for coatings that provide product safety, extended shelf life, and global compliance with food contact regulations. The shift to BPA-free technologies is particularly acute in this segment, where consumer and regulatory scrutiny is strongest. Within food cans, coatings must withstand retort sterilization and aggressive ingredients, while beverage can coatings must guarantee sensory neutrality under carbonation and acidic conditions. Together, these applications anchor the industry’s R&D pipeline, capital investment, and regulatory lobbying. Other end-use sectors such as personal care aerosols, chemical products, and pharmaceuticals remain important specialty niches, but the scale and global nature of the F&B sector ensures it dictates performance, safety, and sustainability benchmarks across the can coatings landscape.

United States Can Coatings Market Shaped by Regulatory Oversight and Sustainable Innovations

The U.S. can coatings market is heavily influenced by federal and state regulations, with the FDA governing food contact materials and the EPA promoting source reduction through its “National Strategy to Prevent Plastic Pollution” released in November 2024. These regulations are driving innovation in can coatings, pushing manufacturers to adopt sustainable and bisphenol-free formulations that reduce environmental impact. Extended Producer Responsibility (EPR) bills passed in states like Washington and Maryland in 2025 are further incentivizing the development of recyclable and environmentally friendly coating solutions.

Corporate investments are focused on health-conscious and sustainable innovations. PPG Industries introduced PPG INNOVEL PRO in August 2022, a BPA-free internal spray coating for aluminum beverage cans that is infinitely recyclable. Technological advancements in water-based and BPA-free coatings are responding to rising consumer awareness regarding health and environmental safety. Key applications span the beverage and food sectors, particularly soft drinks, beer, and canned foods, where maintaining product integrity and extending shelf life is critical. Sustainability considerations are increasingly embedded across the supply chain, reflecting a broader market shift toward eco-friendly practices.

Germany Can Coatings Market Driven by Circular Economy Regulations and R&D Leadership

Germany’s can coatings industry operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating full recyclability or reuse of packaging by 2030. The Packaging Act (VerpackG) further ensures producer responsibility for the lifecycle of packaging, encouraging coatings compatible with recycling streams and circular economy principles.

Technological innovation is at the forefront, with companies developing machinery capable of handling sustainable materials such as high-barrier paper-based films. The German market is particularly strong in food and beverage applications, with a focus on premium, high-performance coatings. Investments in R&D are robust, as companies and research institutions collaborate to produce lighter, stronger, and environmentally sustainable solutions. The country is positioning itself as a hub for next-generation can coatings, where regulatory compliance, circular economy principles, and technological advancement converge.

China Can Coatings Market Expands with Regulatory Reforms and Industrial Innovation

China’s can coatings market is driven by governmental initiatives under the “dual carbon” goal, emphasizing greener industrial practices and the use of bio-based alternatives. The implementation of mandatory national standards for “Limit of Harmful Substances of Coatings” on June 1, 2026 (GB 30981.1-2025), strengthens environmental and safety controls, aligning local coatings with international benchmarks.

Technological advancements such as AI and “5G plus industrial internet” integration are optimizing production efficiency and flexible capacity. Domestic manufacturers are increasing their capabilities to replace imported technologies, meeting growing demand in the food and beverage sector, particularly for ready-to-eat and convenient products. China also continues to lead in patents and innovation, with ongoing R&D efforts focused on environmentally friendly and high-performance can coatings, cementing its position as a major player in the global market.

India Can Coatings Market Accelerates with Sustainable Policies and Export-Oriented Investments

India’s can coatings industry is supported by government programs like “Make in India” and “Zero Effect Zero Defect,” which promote sustainable domestic production. The Indian Paints and Coatings Sector Skills Council is addressing skill gaps, while broader regulatory policies, including MoEFCC’s initiatives to phase out single-use plastics and encourage sustainable materials, are fostering eco-friendly can coatings adoption.

Technological innovations include automated systems and advanced air-based cold spraying processes, developed by the ARCI, which reduce costs and improve sustainability by replacing helium or nitrogen with air as the process gas. Export-oriented investments, such as Siegwerk’s INR 350 crore commitment in September 2025, are strengthening India’s manufacturing and R&D capabilities for global compliance. The food processing and ready-to-drink beverage sectors are key applications, with demand driven by safety, quality, and performance requirements, positioning India as a growing hub for sustainable can coatings.

Brazil Can Coatings Market Strengthened by Regulatory Reforms and Sustainable Manufacturing

Brazil’s can coatings market is shaped by the National Solid Waste Policy and 2024 legislation mandating all packaging to be returnable, recyclable, or fully compostable by 2030. ANVISA’s RDC No. 854/2024 revises technical regulations for coatings and metallic equipment in contact with food, eliminating heavy metals such as copper and promoting safer materials.

Technological advancements, including robotics and AI, are enhancing operational efficiency and quality control, enabling sophisticated applications from automated sorting to defect detection. Sustainability remains a central focus, with companies investing in machinery and coatings compatible with green manufacturing practices. The food, beverage, and cosmetics sectors are key drivers of demand, while government mandates for recycling (30% in 2025 and 50% by 2040) further incentivize the adoption of environmentally friendly coatings and materials. Corporate investments in advanced technologies ensure that Brazil continues to meet both domestic and international standards for sustainable can coatings.

Can Coatings Market Report Scope

Can Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$5.6 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Material Type (Epoxy, Acrylic, Polyester, Oleoresins, Vinyl, Others), By Application (Food Cans, Beverage Cans, General Line Cans, Aerosol Cans), By End-Use Industry (Food & Beverages, Pharmaceuticals, Chemicals, Personal Care, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Jotun A/S, Kansai Paint Co., Ltd., Axalta Coating Systems, Nippon Paint Holdings Co., Ltd., BASF SE, Hempel A/S, TIGER Coatings GmbH & Co. KG, Toyo Ink SC Holdings Co., Ltd., VPL Coatings GmbH & Co. KG, S.A.S. S.p.A., National Paints Factories Co. Ltd., ACTEGA GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Can Coatings Market Segmentation

By Material Type

- Epoxy

- Acrylic

- Polyester

- Oleoresins

- Vinyl

- Others

By Application

- Food Cans

- Beverage Cans

- General Line Cans

- Aerosol Cans

By End-Use Industry

- Food & Beverages

- Pharmaceuticals

- Chemicals

- Personal Care

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Can Coatings Market

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Axalta Coating Systems

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- Hempel A/S

- TIGER Coatings GmbH & Co. KG

- Toyo Ink SC Holdings Co., Ltd.

- VPL Coatings GmbH & Co. KG

- S.A.S. S.p.A.

- National Paints Factories Co. Ltd.

- ACTEGA GmbH

* List Not Exhaustive

Methodology

USDAnalytics leverages a comprehensive research methodology to provide accurate insights into the global can coatings market. Our approach integrates primary research through detailed interviews with industry stakeholders including can coating manufacturers, packaging specialists, and regulatory authorities, combined with extensive secondary research from company reports, patent filings, scientific studies, trade publications, and global regulatory databases. Market sizing, CAGR projections, and trend analyses are derived by evaluating key coating types such as acrylic, epoxy, polyester, vinyl, and oleoresins, alongside applications spanning beverage cans, food cans, aerosol cans, and general line cans. USDAnalytics also examines regulatory influences including BPA- and PFAS-free mandates, recyclability regulations, and regional policies across the U.S., EU, China, India, Brazil, and Japan. Additionally, corporate strategies, R&D investments, technological innovations including nanocoatings, bio-based formulations, and active coatings are analyzed to offer actionable insights into competitive dynamics, market drivers, and growth opportunities for industry professionals seeking strategic advantage in sustainable and high-performance can coating solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.