Packaging Coatings Market to Reach $9.8 Billion by 2034 at a CAGR of 4.7% Driven by Sustainability and High-Performance Demand

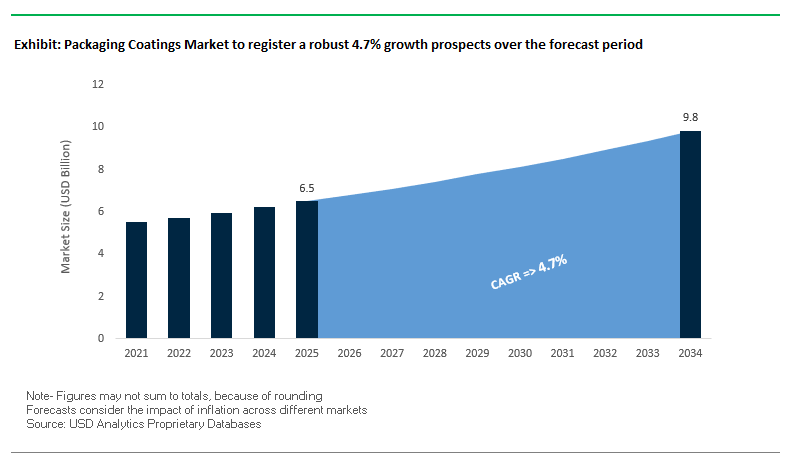

The global packaging coatings market is projected to grow from $6.5 billion in 2025 to $9.8 billion by 2034, reflecting a CAGR of 4.7%. This market is a critical segment in the packaging industry, providing protective, decorative, and functional coatings for metal, plastic, and glass substrates. Packaging coatings ensure product integrity, safety, and visual appeal, while addressing consumer expectations for convenience, sustainability, and smart packaging features.

Key Insights for Industry Professionals:

- Rising demand for barrier coatings: Increasing need for moisture, oxygen, and light protection extends shelf life and reduces food waste.

- Sustainability trends: Shift toward waterborne, bio-based, and energy-curable coatings compliant with BPX-free and ESG regulations.

- Enhanced consumer engagement: Coatings enable digital printing, custom finishes, and haptic effects for a premium unboxing experience.

- Smart and traceable packaging: Integration of QR codes, RFID tags, and other digital interfaces for real-time product tracking and authenticity verification.

- E-commerce growth influence: Increasing e-commerce penetration is driving demand for coatings that support premium appearance, durability, and digital interactivity.

Market Analysis: Recent Developments Highlight Focus on Sustainability, Technology, and Regional Expansion

The packaging coatings industry is evolving rapidly, with strategic acquisitions, technological innovations, and regional investments shaping the market landscape. In August 2025, reports highlighted the growing adoption of intelligent packaging solutions, where coatings incorporate sensing elements to ensure optimal product conditions during transit and storage. July 2025 marked the completion of the Amcor and Berry Global Group merger, creating a dominant packaging entity and driving demand for coatings across their flexible and rigid container lines.

During the same month, PPG Industries reported strong performance in its packaging coatings and specialty products segments, offsetting challenges in industrial coatings. Earlier in April 2025, International Paper completed its $9.9 billion acquisition of DS Smith, expanding its sustainable paper packaging portfolio and indirectly influencing coatings demand for corrugated and consumer packaging. In March 2025, PPG launched a new waterborne automotive coatings plant in Thailand, emphasizing sustainability in the APAC region. February 2025 saw Sherwin-Williams streamline its supply chain, leveraging scale to improve efficiency and service reliability.

Strategic moves in 2024 included Stahl Holdings acquiring WEILBURGER Graphics in September, enhancing its water-based and energy-cured coatings expertise, and AkzoNobel divesting its India business to JSW Group in July to optimize global focus. Axalta’s acquisition of The CoverFlexx Group in July 2024 further strengthened its industrial coatings portfolio.

Trends and Opportunities Transforming the Packaging Coatings Market

Accelerated Regulatory Phase-Out of BPA and PFAS in Food Contact Coatings

The packaging coatings market is facing a legislatively enforced material transformation, with global regulators accelerating the phase-out of Bisphenol-A (BPA) and per- and polyfluoroalkyl substances (PFAS) in food and beverage packaging. The European Commission has officially adopted a ban on BPA in coatings and varnishes used for metal packaging, including beverage cans and jar lids. This regulation, with an 18-month phase-out period, compels packaging suppliers and brand owners to rapidly adopt alternative chemistries. In parallel, regulatory pressure on PFAS is mounting across the U.S., with state-level bans in Minnesota, Oregon, and Rhode Island (effective January 2025) prohibiting intentionally added PFAS in food packaging. This fragmented patchwork of regulations forces multinational brands to adapt coatings that comply across multiple jurisdictions, raising the urgency for viable, PFAS-free alternatives. As a result, coatings manufacturers are entering a new era of chemistry substitution, where compliance, safety, and sustainability converge as market drivers.

Increased Demand for Water-Based and High-Solids Coatings Driven by VOC Compliance

Environmental policies aimed at reducing volatile organic compounds (VOCs) are reshaping the competitive landscape of packaging coatings. The U.S. EPA’s amendments to the National VOC Emission Standards for Aerosol Coatings, finalized recently, represent a broader push to curb solvent-based emissions across coatings applications. This regulatory direction is driving accelerated adoption of low-VOC, VOC-free, water-based, and high-solids formulations. Advances in polymer science are enabling water-based systems to meet or exceed traditional solvent-based performance. For example, aqueous polymeric dispersions such as polyvinyl alcohol (PVOH) and ethyl vinyl alcohol (EVOH) have been proven to deliver excellent oxygen and grease barrier properties, making them viable alternatives for food-contact packaging. Coatings producers are thus channeling R&D and capital investment into high-performance waterborne technologies, positioning them as the standard for future-proof, regulation-compliant packaging solutions.

Development of High-Barrier Functional Coatings for Fiber-Based Packaging

The packaging industry’s push toward plastic-free, fiber-based solutions opens a significant opportunity for coating manufacturers to bridge the performance gap in moisture, grease, and oxygen resistance. Fiber alone cannot replace flexible plastics or styrofoam without advanced coatings that ensure durability and product protection. Companies are responding with innovative formulations. Smart Planet Technologies has introduced a bio-based barrier coating for paper cups combining PLA resins with a mineral blend, reducing plastic content by 35–51% while improving recyclability and compostability. Similarly, UPM Specialty Papers and Eastman have collaborated on a compostable thin-film biopolymer coating that can be applied with existing extrusion equipment, enabling a “drop-in” solution for converters. This segment represents a high-growth frontier where bio-based and recyclable coatings will not only enable compliance but also define brand positioning in sustainable packaging.

Expansion of Active and Smart Coatings for Product Freshness and Traceability

Packaging coatings are moving beyond passive barriers to become functional enablers of freshness, safety, and consumer engagement. Active coatings with antimicrobial or oxygen-scavenging properties extend shelf life and reduce food waste, while smart coatings offer real-time insights into product condition. For instance, academic studies show that chitosan-based coatings can effectively inhibit the growth of E. coli, offering a natural, non-toxic way to enhance food safety. On the smart packaging front, researchers are developing pH-sensitive coatings with embedded microcapsules that change color as food approaches spoilage, providing consumers with visual freshness cues beyond static expiry dates. These innovations move coatings from being low-margin commodities to high-value, specialized components, integral to supply chain traceability and brand protection. As global brands seek differentiation, coatings with embedded freshness indicators, RFID functionality, or antimicrobial layers will unlock new revenue streams while advancing sustainability and consumer trust.

Competitive Landscape Highlights Key Players Driving Innovation and Sustainability in Packaging Coatings

The global packaging coatings market is shaped by leading players leveraging material science, technological expertise, and strategic acquisitions to deliver durable, sustainable, and high-performance coatings for diverse packaging substrates. These companies are investing in BPX-free formulations, waterborne and energy-curable coatings, and digital printing solutions to meet evolving market demands.

AkzoNobel N.V. Innovates BPX-Free Coatings to Meet Global Packaging Regulations

AkzoNobel N.V. is a global leader in paints and coatings, with a strong position in metal and consumer packaging coatings. In July 2025, AkzoNobel signed an agreement to sell its India business to JSW Group, optimizing its global portfolio. The company supplies high-performance coatings for beverage, food, aerosol, and general line cans, with a focus on BPX-free and sustainable solutions. AkzoNobel’s “Grows and Delivers” strategy emphasizes profitability, innovation, and leveraging its global footprint to deliver compliant, high-quality coatings.

The Sherwin-Williams Company Focuses on Customer-Centric Coating Solutions for Packaging

Sherwin-Williams is renowned for its broad coatings portfolio and strong global brand recognition. Despite a softer demand environment, its Q2 2025 financial report highlighted continued investments and restructuring initiatives to enhance efficiency. Sherwin-Williams offers liquid, powder, and e-coat solutions for packaging, improving durability, appearance, and functionality. The company’s strategy prioritizes customer productivity, streamlined supply chains, and faster market delivery.

PPG Industries, Inc. Drives Sustainable and High-Performance Packaging Coatings Growth

PPG Industries combines innovation-driven coatings expertise with a diverse product portfolio across metal, plastic, and glass packaging. In Q2 2025, PPG reported strong growth in its packaging coatings segment, supported by global manufacturing capabilities. The company’s offerings include waterborne, solvent-based, and UV/EB-curable technologies for food, beverage, personal care, and industrial packaging. PPG focuses on sustainable coatings development, protecting substrates while enhancing visual appeal and performance.

Axalta Coating Systems Ltd. Expands Industrial and Packaging Coatings Portfolio

Axalta Coating Systems is a global coatings supplier emphasizing high-performance and durable solutions. In July 2024, Axalta acquired The CoverFlexx Group, enhancing its industrial coatings presence. The company applies its expertise to packaging, offering advanced color-matching and durable coatings. Axalta’s strategy, Axalta 2026 A-Plan, focuses on operational excellence, sustainable innovation, and eco-friendly product development.

Kansai Paint Co., Ltd. Leads with High-Performance Coatings Supporting Sustainability

Kansai Paint, a leading Japanese coatings manufacturer, focuses on durable, weather-resistant, and environmentally conscious coatings. Its 2025 Medium-Term Management Plan emphasizes sustainability and global customer value. Kansai Paint supplies industrial and protective coatings suitable for packaging applications, ensuring extended material lifespan and reduced environmental impact. The company’s strategy revolves around continuous innovation, social responsibility, and creating sustainable value through coatings.

Packaging Coatings Market Share Insights

Metal Packaging Coatings Dominate Market Share by Substrate

Metal substrates account for the largest share at 40% of the packaging coatings industry in 2025, underscoring their indispensable role in food and beverage cans where coatings provide critical protection against corrosion, leaching, and contamination. The dominance of metal coatings is further reinforced by the global transition to BPA-NI (Bisphenol A non-intent) and NIAS-free chemistries, driven by consumer health concerns and stringent regulatory frameworks in North America, Europe, and Asia-Pacific. Paper and paperboard coatings follow with 25%, representing the fastest-growing segment as brand owners accelerate the shift from plastic to fiber-based packaging. Here, innovation is centered on water-based, compostable, and recyclable coatings that maintain grease, moisture, and oxygen resistance without disrupting recycling streams. Flexible packaging substrates (15%) remain integral for high-barrier films and pouches, with growth anchored in UV-curable and water-based coating technologies that deliver sustainability and process efficiency. Rigid plastics (12%) hold a stable position, particularly in caps and closures, where coatings enhance scratch resistance, decoration, and gas barrier performance while aligning with recyclability demands. Glass coatings (8%) represent a niche but high-value segment, where hot-end and cold-end processes enhance strength, lubricity, and production line efficiency, reducing breakage and maximizing throughput. Overall, metal and fiber substrates anchor market volume, while flexible and rigid plastics capture innovation in sustainable barrier and decorative applications.

Beverage Cans Continue to Lead Market Share by Application in Packaging Coatings

Beverage cans dominate the packaging coatings industry with a projected 35% share in 2025, supported by the global momentum towards aluminum cans as the most recyclable beverage format. The sheer scale of demand, extending beyond carbonated soft drinks into water, energy drinks, craft beer, and hard seltzers, ensures beverage can coatings remain the largest and most volume-intensive segment. Food cans (30%) form the second-largest application, defined by their technical complexity under retort sterilization and the accelerated replacement of epoxy liners with next-generation acrylic, polyester, and oleoresin coatings. Caps and closures (15%) are a strategically important niche, where coatings not only provide a protective and functional barrier but also enhance oxygen scavenging and aesthetics to maintain product freshness and brand visibility. Aerosols and tubes (12%) are a high-specification segment requiring coatings with exceptional chemical resistance to withstand aggressive formulations in personal care, household, and pharmaceutical applications. Industrial and specialty packaging (8%) rounds out the segment, with demand centered on drums, pails, and chemical containers, where coatings must guarantee durability and resistance against hazardous chemicals. Collectively, these applications highlight how beverage and food cans dominate by scale, while aerosols, closures, and specialty packaging drive technical innovation and regulatory-driven reformulation.

United States: PFAS-Free and Sustainable Coatings Drive Market Expansion

The U.S. packaging coatings industry is experiencing significant transformation due to state-level regulations banning PFAS (per- and polyfluoroalkyl substances) in food packaging. States including California, Connecticut, and New York have enacted such bans, prompting companies to develop PFAS-free barrier coatings. Technological advancements focus on high-performance, sustainable coatings, including BPA-free epoxy coatings for metal cans, and water-based and UV-cured coatings to reduce VOC (volatile organic compounds) emissions. Notably, Dow’s INNATE TF 220 recyclable resin for flexible packaging films, launched in July 2025, exemplifies this trend.

Corporate investments are also strong, with Sonoco acquiring Eviosys in June 2024 to enhance its technical and commercial presence in can coatings. Demand is primarily driven by the food and beverage sectors, where coatings are essential for preserving product quality, extending shelf life, and ensuring a premium unboxing experience. The e-commerce boom further reinforces the need for durable, high-performance coatings suitable for shipping and consumer-facing packaging.

Germany: Circular Economy and Advanced Films Shape Coatings Adoption

Germany operates under the EU Packaging and Packaging Waste Regulation (PPWR), which heavily influences the choice of packaging coatings to meet recyclability and recycled content targets. Updated ZSVR guidelines (effective 2026) require companies to adhere to practical, material-focused standards, promoting eco-friendly and sustainable coating solutions.

Technological innovation in Germany emphasizes ultra-thin, resource-saving, and recyclable films for food, beverage, and pharmaceutical applications. The country’s robust recycling infrastructure and deposit-return system for beverage containers encourage the adoption of coatings that support a circular economy. Key applications include canned goods, dairy products, pharmaceuticals, and cosmetics, where high-quality coatings ensure product safety, durability, and compliance with environmental regulations.

China: Dual-Carbon Targets and Automation Boost Sustainable Coatings

China’s dual-carbon strategy, targeting carbon peaking by 2030 and neutrality by 2060, drives the adoption of eco-friendly, water-based coatings to minimize VOC emissions. Government infrastructure investments also increase the need for protective coatings for packaging, especially in the rapidly expanding e-commerce and food processing sectors.

Technological advancements are focused on automation, AI, and intelligent manufacturing systems, with companies like Amcor and AkzoNobel expanding capacity and investing in R&D for advanced coating technologies. The growing consumer goods, electronics, and e-commerce markets are fueling demand for durable, automation-ready packaging coatings, capable of withstanding high-volume parcel deliveries while maintaining product quality.

India: Government Incentives and Circular Economy Initiatives Foster Coatings Innovation

India’s Make in India and Production Linked Incentive (PLI) programs encourage domestic investment in the packaging coatings industry, with a strong focus on circular economy practices and recyclable materials. Corporates are voluntarily taking measures to enhance packaging recyclability and reduce plastic footprints, reflecting sustainability commitments.

Investments in production facilities and R&D are increasing, supported by initiatives like the Huhtamaki Foundation’s “CloseTheLoop” program, which invests Rs. 10 crore (US$ 1.18 million) in recycling plants for post-consumer plastic waste. Demand is robust across the food and beverage and pharmaceutical sectors, where coatings are vital for brand presentation, product protection, and compliance with health standards. The growing online retail and supermarket sectors further underscore the importance of premium, sustainable packaging coatings.

Japan: Positive List Regulations and Bio-Based Coatings Promote High-Quality Packaging

Japan’s “positive list” system for food-contact packaging, effective June 1, 2025, specifies allowed substances in packaging, encouraging the use of approved, safe coatings and additives. Companies are focusing on high-performance, functional, and environmentally friendly coatings, including innovations like Toppan’s coreless organic interposer for advanced semiconductors, which often integrates coating technology advancements.

Japan’s sustainability targets, aiming for 46% GHG reduction by 2030 and net-zero emissions by 2050, drive the adoption of bio-polypropylene (bio-PP) in packaging, with plans to introduce 2 million tonnes per year by 2030. Key applications include ready-to-drink teas, coffee, and snack products, where consumers demand lightweight, durable, aesthetically pleasing, and sustainable coatings.

Brazil: Regulatory Reforms and Water-Based Coatings Enhance Food Packaging Safety

Brazil’s National Health Surveillance Agency (Anvisa) 2024 resolution revises technical regulations for food-contact coatings, introducing a positive list for authorized materials and new limits for heavy metals. The National Solid Waste Policy reinforces shared responsibility for the product lifecycle, encouraging manufacturers to adopt sustainable and recyclable coatings.

Technological innovation in Brazil includes water-based and BPA-free epoxy coatings, particularly for the canned food sector, ensuring compliance with both local health regulations and international export quality standards. Key applications are centered on the food and beverage industry, where coatings play a critical role in product safety, shelf life extension, and overall packaging performance, particularly for canned goods and functional beverages.

Packaging Coatings Market Report Scope

Packaging Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.5 Billion

|

|

Market Size (2034)

|

$9.8 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Resin (Epoxies, Acrylics, Polyurethane, Polyolefins, Polyester, Others), By Technology (Water-based, Solvent-based, Powder Coatings, UV-curable), By Substrate (Metal, Rigid Plastic, Glass, Paper & Paperboard, Flexible Packaging), By Application (Food Cans, Beverage Cans, Caps & Closures, Aerosols & Tubes, Industrial & Specialty Packaging), By End-Use Industry (Food & Beverage, Healthcare & Pharmaceutical, Personal Care & Cosmetics, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Jotun A/S, Axalta Coating Systems, Ltd., Henkel AG & Co. KGaA, Siegwerk Druckfarben AG & Co. KGaA, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., BASF SE, Hempel A/S, RPM International, Inc., Chugoku Marine Paints, Ltd., DIC Corporation, Dow Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Coatings Market Segmentation

By Resin

- Epoxies

- Acrylics

- Polyurethane

- Polyolefins

- Polyester

- Others

By Technology

- Water-based

- Solvent-based

- Powder Coatings

- UV-curable

By Substrate

- Metal

- Rigid Plastic

- Glass

- Paper & Paperboard

- Flexible Packaging

By Application

- Food Cans

- Beverage Cans

- Caps & Closures

- Aerosols & Tubes

- Industrial & Specialty Packaging

By End-Use Industry

- Food & Beverage

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Coatings Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- Jotun A/S

- Axalta Coating Systems, Ltd.

- Henkel AG & Co. KGaA

- Siegwerk Druckfarben AG & Co. KGaA

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- BASF SE

- Hempel A/S

- RPM International, Inc.

- Chugoku Marine Paints, Ltd.

- DIC Corporation

- Dow Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to provide actionable insights into the global packaging coatings market, combining primary research, secondary data, and advanced analytics. Primary research includes interviews with R&D specialists, packaging engineers, material scientists, and sustainability officers from leading packaging and coating manufacturers, covering applications in food & beverage, healthcare, personal care, and industrial packaging. Secondary research leverages corporate filings, industry reports, regulatory documents such as the EU Packaging and Packaging Waste Regulation (PPWR), U.S. state-level PFAS bans, and China’s dual-carbon initiatives, as well as press releases detailing strategic mergers, acquisitions, and technology launches. Market sizing and forecasts are developed using historical growth trends, substrate adoption patterns, and technological innovations such as water-based, UV-curable, and energy-cured coatings. USDAnalytics further evaluates sustainability trends, including bio-based, recyclable, and BPA/PFAS-free formulations, as well as smart and active coatings for freshness, traceability, and consumer engagement. Competitive landscape analysis highlights global leaders such as PPG Industries, AkzoNobel, Sherwin-Williams, Axalta, and Kansai Paint, examining their investment in R&D, regional expansion, regulatory compliance, and high-performance coating solutions, offering industry professionals strategic insights for product development, market entry, and growth planning.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.