Beverage Can Ends Market Overview: Recycling Leadership and Innovation in Consumer Convenience

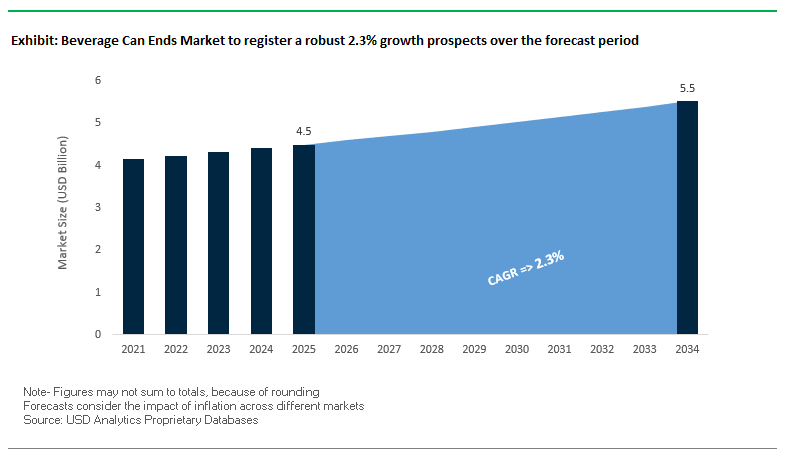

The beverage can ends market is forecasted to grow from USD 4.5 billion in 2025 to USD 5.5 billion by 2034, at a modest CAGR of 2.3%. Despite its specialized role, the segment is crucial in beverage packaging, driving differentiation, sustainability, and durability across global supply chains. For industry professionals, the question is not whether can ends are essential, but how advancements in coatings, lightweighting, and consumer-centric designs can strengthen brand value while reducing environmental impact. From premium formats to e-commerce durability, beverage can ends are emerging as a strategic enabler of circular economy goals and customer engagement strategies.

Key Insights for Industry Stakeholders

- Recyclability Standard: Aluminum can ends achieve over 95% recyclability, validated by the European Union’s Packaging & Packaging Waste Regulation draft.

- Dominance of Stay-on-Tabs: More than 40% of can ends worldwide are stay-on-tabs, offering convenience, safety, and global adoption in soft drinks, beer, and energy drinks.

- Durability for E-commerce: With direct-to-consumer beverage sales accelerating, can ends provide superior oxygen and UV protection to maintain product integrity during transit.

- Lightweighting Innovation: Ongoing design advancements reduce metal usage per unit, cutting both costs and carbon emissions, aligning with consumer and brand sustainability targets.

Market Analysis: Regulatory Endorsements, Mergers, and Product Innovations Define Growth

The past year highlighted sustainability milestones, industrial expansions, and corporate consolidation in the beverage can ends market. In August 2025, Ball Corporation completed the sale of a 41% stake in its Saudi Arabia joint venture to ORG Technology, reflecting a sharper focus on core growth areas. Similarly, in May 2025, Crown Holdings announced a new high-speed production line at its Ponta Grossa, Brazil facility to meet rising South American demand. During the same month, San Juan Beverage Company partnered with Crown Holdings to launch a new canned cocktail, underscoring the RTD beverage boom and its direct impact on can ends consumption.

Strategic realignments are also reshaping competitive positioning. In April 2025, the Amcor-Berry Global merger agreement created a packaging powerhouse with significant leverage in consumer and healthcare packaging industries heavily reliant on can end supply. Technological advancements gained traction in March 2025, when a materials science study introduced BPA-free coatings for can ends, addressing safety and compliance pressures. Regulatory drivers further strengthened the industry in January 2025, when the EU confirmed aluminum cans’ top-tier recyclability rating (95%), ensuring confidence among investors and policymakers.

Earlier developments signaled a decisive pivot towards lightweighting and portfolio expansion. In December 2024, a major European brewer shifted its entire beer portfolio from glass bottles to cans, significantly increasing can ends demand. In November 2024, Ardagh Group expanded its lightweight can end production in the U.S., targeting high-growth categories like energy drinks and flavored water. These movements collectively indicate that sustainability, RTD innovation, and regulatory validation are converging to define the trajectory of the beverage can ends industry.

Emerging Trends and Opportunities Transforming the Beverage Can Ends Market

Accelerated Adoption of Sustainable and Recyclable Easy-Open End Designs

Sustainability is redefining the beverage can ends market as manufacturers shift toward recyclable, mono-material solutions that align with both corporate ESG commitments and regulatory mandates. A breakthrough came in August 2025, when Novelis partnered with DRT Holdings to develop “uni-alloy” can ends, engineered from the same alloy as the can body. This innovation enables cans to be manufactured with up to 99% recycled content, slashing carbon footprints by more than 50%. Another critical advancement is the elimination of PVC sealants, which have long been a barrier to recyclability. Companies are replacing PVC with recyclable polymer-based sealants that maintain hermetic integrity while ensuring compatibility with recycling streams. Lightweighting continues to play a central role, as innovations in aluminum alloy compositions allow can ends to use thinner gauges without compromising structural strength. This strategy not only lowers material usage and transport costs but also enhances the overall sustainability profile of beverage cans, positioning them as leaders in the global circular packaging economy.

Integration of Smart and Connected Features for Consumer Engagement

Digital innovation is transforming beverage can ends into interactive, consumer-facing platforms. Laser-etched QR codes, serialized codes, and under-tab markings are increasingly deployed by brands for loyalty programs, promotions, and gamified marketing. Ball Corporation, for instance, offers unique etched codes under tabs, creating individual engagement opportunities for each can sold. Beyond marketing, smart codes are being used to enable supply chain transparency, allowing consumers to trace product origins, ingredients, and brand stories by scanning their cans. This feature is particularly valued in premium and craft beverage categories, where authenticity and provenance drive purchasing decisions. Additionally, can ends are evolving into branding canvases. Manufacturers offer custom colors, printed tabs, and decorative finishes that reinforce brand identity and enhance the consumer experience even before the can is opened. By merging sustainability with interactivity, beverage can ends are becoming powerful vehicles for both customer engagement and brand protection.

Development of Specialty Ends for the Growing Wine and Spirit Canning Segment

The rise of canned wine, spirits, and RTD cocktails has created a demand for can ends that address the unique requirements of these premium beverages. Unlike beer or soda, which are often consumed in one sitting, wines and spirits are consumed more gradually, driving demand for resealable can ends. Companies like Orora have pioneered patented resealable ends, enabling consumers to securely close cans without losing carbonation, a critical feature for spritzers and cocktails. Premium aesthetics are another opportunity, as high-value alcohol brands require packaging that communicates luxury. Custom-designed tabs, metallic finishes, and colored ends provide a more elevated look and feel while maintaining the portability and sustainability of cans. Additionally, innovations in pouring experience are being integrated into can end design, improving liquid flow to replicate the elegance of pouring from a bottle. These specialty ends are creating new revenue streams for manufacturers and offering alcohol brands a competitive edge in the fast-expanding canned wine and spirits market.

Penetration into Emerging Markets through Localized Production and Cost-Optimized Designs

The beverage can ends market is experiencing robust growth in Asia, Africa, and South America, where rising middle-class consumption is driving demand for affordable, high-quality packaging. To capture this momentum, manufacturers are prioritizing localized production, establishing new plants in high-demand regions such as India and Brazil. Localized operations reduce logistics costs, shorten lead times, and ensure supply resilience, all of which are critical for supporting rapid market expansion. For cost-sensitive segments, standardized, cost-optimized designs are being rolled out, focusing on efficiency without compromising product safety. Streamlined production processes and simplified end formats enable brands to offer canned beverages at competitive price points to a wider consumer base. Strategic partnerships with regional bottlers are also proving essential, allowing global manufacturers to adapt quickly to local consumer preferences and regulations. This dual focus on localization and affordability ensures that beverage can ends can capture long-term growth opportunities across the developing world.

Competitive Landscape: Global Leaders Driving Sustainability and Specialty Design

The beverage can ends market is consolidated, dominated by a handful of multinational leaders who combine large-scale operations, R&D expertise, and sustainability commitments. Differentiation comes through innovation in closures, lightweighting efficiency, and specialty decoration that enhances consumer experience.

Ball Corporation focuses on lightweighting and interactive consumer engagement

Ball Corporation is a global leader in aluminum packaging, offering innovative can ends and tabs with advanced finishes, colors, and laser-etched designs. In August 2025, it streamlined operations by selling 41% of its Saudi JV stake to ORG Technology. Ball’s strength lies in lightweighting advancements and interactive consumer features, such as etched codes for digital engagement. With end-to-end packaging integration from body to tab, Ball ensures quality consistency and supply reliability.

Crown Holdings Inc. leads with “SuperEnd” and “360 End” innovations

Crown Holdings remains at the forefront of consumer-focused innovations, including its SuperEnd (10% less metal use) and 360 End (full-aperture opening). In May 2025, it added a high-speed production line in Brazil, reinforcing its regional dominance. Its Global Vent technology further enhances the consumer pour experience. Crown is also renowned for its dedicated ends expertise, supporting beverage companies in optimizing filling line efficiencies while achieving sustainability goals.

Ardagh Group expands lightweight can ends for premium beverages

Ardagh Group combines metal and glass packaging expertise, positioning itself uniquely as a full-service supplier. With its “Twentyby30” roadmap, it prioritizes lightweighting and recycled content adoption. In November 2024, it expanded its lightweight can ends production in the U.S., specifically targeting energy drinks and flavored water. Its dual-material portfolio enables synergy for beverage brands seeking integrated glass and metal packaging solutions.

Envases Universales pioneers CDL-E lightweight ends

Envases Universales specializes in lightweight and specialty can ends, with its CDL-E end 10% lighter than standard formats. Innovation and R&D collaborations drive its cost-efficiency and sustainability focus. Envases has also diversified into larger 16 oz can formats, adapting to consumer preference shifts in RTD and craft beverages. Operational excellence and sustainability underpin its market positioning, making it a preferred partner for brands scaling eco-friendly solutions.

CAN-PACK S.A. excels in graphic customization and integrated services

CAN-PACK delivers comprehensive metal packaging solutions, with a reputation for high-quality graphic customization on can ends. Its ability to apply varied inks, textures, and finishes allows brands to differentiate in competitive retail environments. The company’s vertically integrated model, covering design, production, and logistics, enhances efficiency and scalability. This combination of flexibility, creative branding, and integrated service delivery strengthens CAN-PACK’s standing as a key global competitor.

Beverage Can Ends Market Share Insights

Market Share by Material Type in the Beverage Can Ends Industry

Aluminum dominates the global beverage can ends market with a staggering 92% share in 2025, establishing itself as the near-universal standard across all major beverage categories. Its widespread adoption is driven by its lightweight properties, malleability for precision scoring, corrosion resistance, and seamless compatibility with aluminum can bodies, creating a monomaterial packaging system that is highly recyclable and aligned with global circular economy mandates. This synergy between can body and end makes aluminum the most cost-efficient and sustainable option for high-volume industries like carbonated soft drinks (CSDs), beer, and ready-to-drink (RTD) cocktails. Moreover, aluminum’s recyclability rate far surpasses that of steel, reinforcing its dominance as governments and brands push aggressively toward closed-loop systems. Steel, by contrast, has been relegated to a minimal, niche role, primarily tied to legacy usage in specific regions or applications where steel-bodied cans persist. For beverage ends, steel’s drawbacks higher weight, corrosion risk, and more complex easy-open tab engineering have largely eliminated its relevance in mainstream markets, leaving aluminum as the clear global standard.

Market Share by Application in the Beverage Can Ends Industry

Carbonated soft drinks (CSDs) and alcoholic beverages together account for over two-thirds of global beverage can ends demand in 2025, holding 35% and 33% shares, respectively. This dominance reflects the massive global consumption volumes of CSDs and beer, both of which require highly standardized, high-speed produced ends for seamless integration into filling and seaming lines. Within alcoholic beverages, rapid growth in RTD cocktails and hard seltzers is reshaping demand, fueling higher production of specialized can ends optimized for these categories. Energy drinks form a disproportionately high-value segment, leveraging smaller format cans like 8.4 oz (250 ml), which require dedicated end sizes. While their absolute volume is lower, their specialized nature creates a profitable niche for suppliers. Fruit and vegetable juices represent a steady but challenging category, as higher acidity levels and pasteurization requirements demand more resistant linings and coatings to ensure safety and integrity, while also facing stiff competition from alternative packaging formats like cartons and PET bottles. Finally, other beverages including functional waters, cold brew coffee, and plant-based drinks serve as the innovation hub of the can ends industry. These categories often test new opening mechanisms, resealable tabs, or wider apertures for smoothies and protein shakes, making them critical incubators for design and technology that could scale to mainstream markets in the future.

United States Leads Beverage Can Ends Market with Innovation and Capacity Expansion

The United States remains at the forefront of the global beverage can ends market, with companies like Ball Corporation and Ardagh Group investing heavily in new production facilities to meet the surging demand for canned beverages. This demand is driven not only by soft drinks and beer but also by rapidly growing categories such as seltzers, ready-to-drink (RTD) cocktails, and craft beers. Innovation plays a pivotal role in this market, with Crown Holdings’ Infinity Can introducing a resealable end that delivers on-the-go convenience while serving as a sustainable alternative to single-use plastics.

Lightweighting is another defining trend in the U.S. beverage can ends market. Manufacturers are employing advanced alloys and design innovations to minimize aluminum use, thereby lowering costs and reducing carbon footprints. The diversification of can end formats, such as slim and sleek designs, caters to evolving consumer preferences and new beverage categories. Additionally, strategic partnerships with beverage brands to invest in recycling infrastructure are strengthening circular economy practices, ensuring a reliable supply of high-quality recycled aluminum for long-term growth.

China Expands Beverage Can Ends Production with High-Speed Automation and Sustainability Push

China’s beverage can ends market is undergoing rapid transformation fueled by the country’s massive beverage consumption and strong government support for sustainability. Manufacturers are deploying advanced high-speed production lines and automation to achieve large-scale, cost-effective manufacturing of beverage can ends. This efficiency is essential to meeting the ever-increasing demand from carbonated soft drinks, beer, and energy drink markets.

Technological innovation in can end printing is also emerging as a differentiator. With advancements enabling high-resolution graphics and QR codes on the underside of tabs, brands are turning can ends into marketing and consumer engagement tools. Furthermore, the industry is shifting from steel to aluminum due to its superior recyclability, lightweight properties, and consumer preference. Government policies that promote reduced plastic waste are further driving the adoption of aluminum beverage can ends, positioning China as both a high-volume producer and a sustainability leader.

Germany Strengthens Beverage Can Ends Market Through Recycling and Regulatory Compliance

Germany stands out in the beverage can ends market due to its robust recycling infrastructure and strict compliance with EU packaging regulations. The country’s deposit-return system (Pfandsystem) guarantees extremely high collection and recycling rates for aluminum cans and can ends, creating a closed-loop system that ensures a steady flow of recycled raw materials. This infrastructure is vital for achieving circular economy targets and reducing reliance on virgin aluminum.

Regulatory alignment with the European Union’s Packaging and Packaging Waste Regulation (PPWR) is accelerating the adoption of mono-material can ends and discouraging non-recyclable components. German manufacturers are also at the forefront of sustainability innovation, focusing on increasing the use of post-consumer recycled (PCR) content and designing alloys optimized for recyclability. These initiatives not only meet regulatory demands but also strengthen Germany’s role as a leader in sustainable beverage packaging technologies.

Brazil Emerges as a Global Leader with Record-High Recycling and Growing Investments

Brazil is one of the most dynamic markets for beverage can ends, boasting the highest aluminum can and can end recycling rate globally, often exceeding 95%. This exceptional recycling infrastructure ensures a stable and cost-effective raw material supply, giving the country a competitive edge in sustainable beverage packaging. The preference for aluminum packaging is further reinforced by consumer demand, as cans are valued for their convenience, rapid chilling properties, and strong sustainability credentials.

The market is also seeing significant investment from international companies. Global players like CAN-PACK are building new manufacturing facilities in Brazil to meet rising demand across the beer and soft drinks sectors. This combination of strong consumer preference, advanced recycling infrastructure, and growing industrial capacity firmly positions Brazil as a critical growth hub in the global beverage can ends market.

India’s Growing Urban Market Drives Demand for Beverage Can Ends

India’s beverage can ends market is expanding rapidly, fueled by rising urbanization and a growing middle class that increasingly prefers modern, convenient packaging formats. The shift toward canned beverages is creating strong demand for high-quality beverage can ends, making them a crucial component in the country’s evolving beverage industry.

Global companies are strengthening their presence in India to capture this opportunity. For instance, CAN-PACK has invested significantly in a new manufacturing facility in Uttar Pradesh, underscoring confidence in long-term market growth. With heightened consumer awareness around sustainability, aluminum can ends are gaining popularity as a recyclable and eco-friendly alternative to plastic closures. As both domestic and international beverage brands adopt canned formats, India is becoming a key growth destination in the global beverage can ends market.

Japan Pioneers Lightweight and Circular Solutions in Beverage Can Ends Market

Japan’s beverage can ends market is defined by a strong national commitment to recycling and cutting-edge innovation in lightweighting technologies. The country’s highly efficient recycling infrastructure ensures that a significant percentage of aluminum can ends are collected and reused, aligning perfectly with national sustainability policies.

Manufacturers such as Toyo Seikan and UACJ Corporation have taken a leadership role in advancing lightweighting technologies, with the development of “EcoEnd” can ends that use less material while maintaining durability and performance. The industry is also embracing the use of “Green Aluminum,” produced with renewable energy and a high proportion of recycled content, further reinforcing circular economy principles. These innovations not only reduce environmental impact but also help Japan maintain its position as a technological leader in the global beverage can ends industry.

Beverage Can Ends Market Report Scope

Beverage Can Ends Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.5 Billion

|

|

Market Size (2034)

|

$5.5 Billion

|

|

Market Growth Rate

|

2.3%

|

|

Segments

|

By Material Type (Aluminum, Steel), By Application (Alcoholic Beverages, Carbonated Soft Drinks, Fruit & Vegetable Juices, Energy Drinks, Other Beverages), By Product Type (Stay-on-Tab, Full Aperture Ends, Resealable Ends, Other Can Ends)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings, Inc., Ardagh Group S.A., CAN-PACK S.A., Silgan Holdings Inc., Toyo Seikan Group Holdings, Ltd., Novelis Inc., CPMC Holdings Limited, Showa Denko K.K., UACJ Corporation, Envases Group, Massilly Holding S.A.S., DRT Holdings, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Beverage Can Ends Market Segmentation

By Material Type

By Application

- Alcoholic Beverages

- Carbonated Soft Drinks

- Fruit & Vegetable Juices

- Energy Drinks

- Other Beverages

By Product Type

- Stay-on-Tab

- Full Aperture Ends

- Resealable Ends

- Other Can Ends

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Beverage Can Ends Market

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group S.A.

- CAN-PACK S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings, Ltd.

- Novelis Inc.

- CPMC Holdings Limited

- Showa Denko K.K.

- UACJ Corporation

- Envases Group

- Massilly Holding S.A.S.

- DRT Holdings, LLC

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global beverage can ends market, examining recent breakthroughs in lightweighting, sustainability, and specialty designs while assessing regulatory endorsements and strategic mergers that shape industry dynamics. The analysis reviews technological innovations such as BPA-free coatings, recyclable uni-alloy ends, and smart engagement features, highlighting their impact on brand differentiation, cost efficiency, and circular economy adoption. The report further highlights market expansion in premium and emerging segments, including RTD beverages, energy drinks, and canned wine, providing stakeholders with actionable insights on supply chain optimization, raw material sourcing, and industrial-grade applications. This report is an essential resource for manufacturers, investors, packaging engineers, and strategic planners seeking a comprehensive understanding of growth drivers, competitive positioning, and regional development patterns in the beverage can ends sector. It also evaluates the evolving adoption of interactive and sustainable can end designs across global markets, offering guidance on leveraging innovation to strengthen brand value and meet evolving consumer expectations.

Scope Highlights

- Segmentation: By Material Type (Aluminum, Steel), By Application (Alcoholic Beverages, Carbonated Soft Drinks, Fruit & Vegetable Juices, Energy Drinks, Other Beverages), By Product Type (Stay-on-Tab, Full Aperture Ends, Resealable Ends, Other Can Ends)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ companies including Ball Corporation, Crown Holdings, Ardagh Group, CAN-PACK, Silgan Holdings, Toyo Seikan, Novelis, CPMC Holdings, Showa Denko, UACJ Corporation, Envases Group, Massilly Holding, DRT Holdings, LLC.

Methodology

The beverage can ends market study employs a multi-step methodology integrating both primary and secondary research to ensure comprehensive and reliable insights. Primary research involves detailed interviews with industry stakeholders, including manufacturers, brand owners, packaging engineers, and distributors, to capture real-time trends, technological innovations, and market drivers. Secondary research encompasses an exhaustive review of company reports, regulatory publications, trade journals, and academic studies to validate market trajectories and competitive positioning. Quantitative models and forecasting techniques are applied to historical data from 2021 to 2024 to project growth patterns through 2034. Special attention is given to regional dynamics, sustainability initiatives, and product-specific adoption, ensuring the methodology aligns with the information needs of experienced industry professionals. Insights are triangulated across multiple sources to identify opportunities in material innovation, product customization, and regional expansion while highlighting challenges such as supply chain fragmentation, regulatory compliance, and environmental mandates.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.