Market Overview: Recyclability and Premiumization Driving Market Expansion

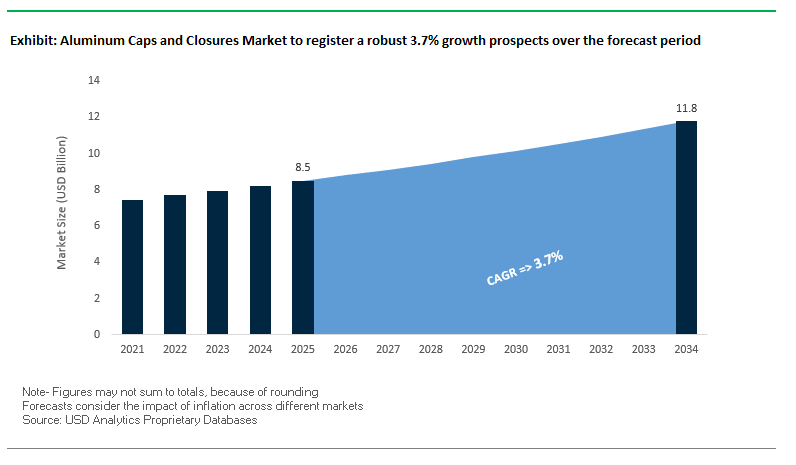

The global aluminum caps and closures market is valued at USD 8.5 billion in 2025 and is forecasted to reach USD 11.8 billion by 2034, expanding at a CAGR of 3.7%. Aluminum closures play a vital role across beverages, food, pharmaceuticals, and personal care sectors, where they provide tamper evidence, durability, and premium aesthetics. For industry buyers and professionals, the market answers key questions around sustainability, safety, and brand differentiation, making it a central part of packaging strategies worldwide.

A major driver is the material’s infinite recyclability, which aligns with corporate sustainability agendas and regulatory pushes for circular economy adoption. Tamper-evident ROPP caps remain the leading product format, ensuring safety and brand protection in pharmaceuticals, wine, and spirits. Premiumization is another strong force, as aluminum closures support custom embossing, decorative finishes, and branding features that enhance shelf presence. Screw caps dominate the market by volume, driven by consumer preference for convenience, resealability, and secure product protection.

Key Insights for Industry Professionals:

- 70%+ recycling rate in developed economies makes aluminum closures a circular economy champion.

- ROPP caps dominate with tamper-evident and anti-counterfeit benefits.

- Premium spirits, wines, and olive oils are driving decorative and embossed aluminum closure demand.

- Screw caps lead adoption due to ease of use and secure sealing across beverages.

Market Analysis: Expansions, Strategic Partnerships, and Innovation in Closures

The aluminum caps and closures industry has seen consistent investment and innovation across global regions, with key developments highlighting sustainability and premium functionality. In August 2025, Crown Holdings reported strong sales growth from beverage and food closures in North America and Europe, signaling resilient demand despite economic volatility. In the same month, Ball Corporation completed the sale of part of its Saudi Arabian joint venture, streamlining its global portfolio while doubling down on core packaging solutions.

July 2025 saw Ardagh Glass Packaging-Europe (AGP-Europe) launch a lightweight wine bottle, which drives new demand for compatible aluminum closures. Meanwhile, May 2025 marked Ball’s recognition with four EMBANEWS Awards for sustainable packaging innovation, highlighting its advancements in eco-friendly caps and closures. On the innovation side, Closure Systems International (CSI) introduced its Defender-Lok™ closures in April 2025, specifically targeting nutraceuticals with child-resistant yet senior-friendly designs.

The industry is also undergoing strategic expansions in Asia-Pacific and North America. Guala Closures invested in a new production line in China in March 2025, reflecting rising regional demand, while Amcor opened a new facility in Ohio in February 2025 to increase closure capacity for the North American market. Beyond expansions, Ball’s acquisition of Alucan in November 2024 broadened its portfolio into sustainable extruded aluminum aerosol and bottle technology.

Key Trends and Growth Opportunities Defining the Aluminum Caps and Closures Market

Lightweighting and Advanced Alloy Development for Sustainability and Cost Reduction

A prominent trend reshaping the aluminum caps and closures market is the aggressive push toward lightweighting and alloy innovation. Driven by rising raw material costs, logistics pressures, and sustainability mandates, manufacturers are engineering closures that use thinner gauges and harder tempers without compromising performance. Companies like Constellium are at the forefront, leveraging 8000-series alloys that enhance strength and barrier properties, enabling packaging producers to reduce aluminum usage while still ensuring integrity for food and pharmaceutical applications. This shift not only delivers cost savings through lower material input but also reduces the total weight of shipments, directly cutting transportation costs and carbon emissions. By aligning lightweighting with high-speed production efficiencies, closure producers are meeting brand-owner demands for reduced environmental impact while safeguarding critical performance attributes such as sealing strength and tamper resistance.

Integration of Smart and Tamper-Evident Features for Brand Protection and Consumer Engagement

Aluminum closures are evolving from static sealing devices into sophisticated platforms for security, traceability, and consumer interaction. With counterfeiting on the rise, particularly in high-value spirits and pharmaceuticals, manufacturers are embedding advanced tamper-evident technologies, holographic seals, and even unique “fingerprint” identifiers into closure designs. Beyond security, smart technologies such as QR codes and NFC tags are transforming closures into interactive gateways. Consumers can scan a cap to instantly verify authenticity, trace the product’s origin, or engage with a brand’s sustainability story. This not only fosters consumer trust but also allows brands to extend their marketing strategies directly through packaging, creating personalized promotions and collecting real-time customer insights. By integrating these features, closures are becoming multifunctional components that deliver both operational security and powerful direct-to-consumer engagement.

Expansion into Premium Non-Beverage Markets (Spirits, Gourmet Foods, Cosmetics)

The premium aesthetics and functional superiority of aluminum closures are unlocking growth beyond traditional wine and beer applications. High-value segments such as spirits, gourmet foods, and luxury cosmetics increasingly favor aluminum for its inert nature, barrier performance, and capacity for advanced decoration. In cosmetics, aluminum closures enhance both visual appeal and product safety, supporting deep drawing, anodizing, embossing, and multi-color finishes that deliver a premium shelf presence. Gourmet food producers benefit from aluminum’s superior barrier against oxygen and light, ensuring freshness and flavor retention, while spirits brands leverage tamper-proof, decorative closures to reinforce authenticity and exclusivity. The versatility in design and functional protection makes aluminum closures an ideal solution for premium positioning, where aesthetics, consumer experience, and integrity are equally critical.

Closed-Loop Recycling and High-Post-Consumer-Recycled (PCR) Content Initiatives

Sustainability imperatives are creating one of the most lucrative opportunities in the aluminum caps and closures market: the integration of high levels of post-consumer recycled (PCR) aluminum into product lines. Producing aluminum from recycled scrap reduces carbon emissions by over 90% compared to virgin metal, making PCR content a vital enabler for achieving corporate and regulatory climate goals. Leading producers are investing heavily in infrastructure to support this shift. Emirates Global Aluminium (EGA) is building the UAE’s largest aluminum recycling facility, expected to process up to 170,000 tons annually by 2026. At the same time, companies like CANPACK are collaborating through initiatives such as the Aluminium Recycling Coalition to boost regional collection rates and improve consumer recycling behavior. By closing the loop, manufacturers not only secure a sustainable raw material supply but also enhance brand credibility in markets where consumers and regulators increasingly demand proof of circularity.

Competitive Landscape: Leading Companies Driving Global Closure Innovation

The competitive landscape is defined by global leaders combining scale, sustainability, and advanced design capabilities to meet brand and consumer expectations for safety, aesthetics, and recyclability.

Guala Closures: Smart Closures and Asia-Pacific Expansion

Guala Closures is a top global player offering tamper-evident, non-refillable, and premium closures under brands like Divinum® and Wak®. A key innovation is its aluminum wine screw cap with integrated NFC technology, enabling anti-counterfeiting and consumer engagement. In March 2025, it expanded with a new production line in China to strengthen its Asia-Pacific footprint. The company focuses on sustainability, lightweighting, and digital-enabled smart packaging, positioning itself as a pioneer in connected closures.

Amcor plc: Expanding Closure Manufacturing in North America

Amcor, a global leader in sustainable packaging, provides closures under its STELVIN® brand, widely used in wine and spirits. In February 2025, Amcor opened a new Ohio facility dedicated to aluminum closures, highlighting its commitment to regional expansion. Its innovation pipeline includes tamper-evident closure designs that enhance product safety and consumer convenience. With strong R&D and a goal of 100% recyclable products by 2025, Amcor integrates sustainability and customization into its closure portfolio.

Crown Holdings, Inc.: Strong Growth in Beverage Closures

Crown Holdings manufactures a broad portfolio of metal packaging, including aluminum beverage and food closures. In July 2025, it reported a 9% income rise and 6% sales growth in its Americas beverage segment, underscoring rising demand for cans and closures. Crown’s strengths lie in its diverse global footprint and strong partnerships with beverage brands, supported by investments in manufacturing efficiency and innovative closure designs.

Closure Systems International (CSI): Specialized in Safety-Oriented Closures

CSI is a global closure solutions provider for beverages, food, and automotive applications. Its Defender-Lok™ line, introduced in April 2025, addresses OTC and nutraceutical packaging with closures that are both child-resistant and senior-friendly. CSI’s edge comes from its expertise in both closures and capping equipment, providing end-to-end solutions for brand owners. The company emphasizes innovation, safety, and process efficiency, ensuring compliance with stringent market requirements.

Ardagh Group S.A.: Low-Carbon Vision in Aluminum Closures

Ardagh Group, through its metal packaging division, is a major supplier of aluminum beverage cans and closures. In November 2024, it showcased its low-carbon packaging strategy, investing in renewable energy and efficient furnace designs to reduce emissions. Its long-term sustainability focus, combined with Virtual Power Purchase Agreements (VPPAs), aligns with its ambition to lead in decarbonized packaging. With a strong customer base in beverages, Ardagh delivers sustainable and scalable closure solutions to global brands.

Aluminum Caps and Closures Market Share Insights

ROPP Caps Lead Aluminum Caps and Closures Market Share by Product Type

By product type, ROPP (Roll-On Pilfer-Proof) caps dominate the aluminum caps and closures market in 2025, supported by their widespread use in the beverage industry, particularly for wine, spirits, and bottled water where tamper-evidence, resealability, and premium aesthetics are essential. Non-refillable closures represent the next significant share, driven by their adoption in alcoholic beverages and high-value products to prevent counterfeiting and ensure product authenticity. Easy open ends are steadily expanding their presence in the food and beverage sector, especially in canned foods and ready-to-drink beverages, where convenience and safety drive demand. Other closures, including specialty formats, serve niche applications across pharmaceuticals, cosmetics, and industrial packaging. The strong leadership of ROPP caps highlights the market’s focus on safety, consumer convenience, and premium brand positioning, while innovation in tamper-evidence and resealable formats continues to shape product type dynamics.

Beverages Dominate Aluminum Caps and Closures Market Share by End-Use Industry

By end-use industry, beverages account for the largest share of the aluminum caps and closures market in 2025, with massive demand from bottled water, carbonated soft drinks, beer, wine, and spirits. The sector relies heavily on aluminum closures for their durability, tamper resistance, and compatibility with high-speed filling lines, making them indispensable for both premium and mass-market beverages. Pharmaceuticals and healthcare represent another critical segment, where aluminum closures ensure sterility, tamper-evidence, and regulatory compliance for vials, syringes, and infusion bottles. The food industry also contributes significantly, leveraging easy open ends and specialty closures for canned foods, sauces, and condiments. Cosmetics and personal care utilize aluminum closures to enhance luxury branding, sustainability credentials, and consumer convenience for perfumes, lotions, and oils. Other industries, including household and industrial goods, account for a smaller share but highlight the versatility of aluminum closures across diverse applications. The dominance of beverages underscores the material’s essential role in global packaging, while rising demand in healthcare and cosmetics showcases diversification beyond traditional markets.

United States: Sustainable and Lightweight Aluminum Closures Drive Market Growth

The U.S. aluminum caps and closures market is expanding rapidly due to evolving consumer preferences for sustainable, convenient, and single-serve packaging, particularly in the beverage sector. The rise in eco-conscious consumer behavior is driving demand for recyclable and lightweight aluminum closures, with companies like Amcor investing in new facilities in Ohio dedicated to producing sustainable closure solutions.

Technological innovations, including lightweighting and enhanced tamper-evident designs, are shaping product offerings, ensuring both functionality and environmental responsibility. The Can Manufacturers Institute (CMI) reports that the average aluminum beverage can in the U.S. contains 71% recycled content, and new cans can be produced from recycled material in under 60 days. Strategic investments in recycling infrastructure, supported by the EPA’s $58 million allocation for community recycling projects, are further reinforcing market sustainability. Regulatory shifts, such as the removal of fill-size barriers by the Alcohol and Tobacco Tax and Trade Bureau in January 2025, have expanded the market for premium beverage closures, creating opportunities for innovative aluminum cap designs.

Germany: Circular Economy Leadership and Recyclable Aluminum Closures

Germany’s aluminum caps and closures industry is heavily influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates eco-friendly and highly recyclable packaging solutions. The country is a leader in the circular economy, achieving a 99% recycling rate for aluminum beverage cans, supported by efficient deposit return systems and strong consumer compliance.

Technological advancements are driving product innovation, with European smelters like Constellium and Novelis harmonizing alloy specifications to enable beverage cans with up to 100% recycled content, significantly reducing carbon emissions. Governmental mandates under the EU PPWR, which include waste reduction targets and increased recycled content requirements, are further shaping market developments, reinforcing Germany’s position as a hub for sustainable aluminum closures in Europe.

China: Industrial Expansion and E-commerce Fuel Demand for Tamper-Proof Closures

China’s aluminum caps and closures market is expanding in line with the country’s rapid industrialization and manufacturing growth, particularly in the beverage and e-commerce sectors. The demand for durable, reliable, and tamper-proof closures is rising as the market adapts to high-volume production and diverse product lines.

Governmental initiatives, such as the 2025–2027 Action Plan for the Aluminum Industry, aim to boost resource security, green development, and technological innovation, targeting an increase in recycled aluminum output to 15 million tonnes. Technological advancements, including automation, AI integration, and “5G plus industrial internet” systems, are optimizing production efficiency and flexible manufacturing capacity. The rapid growth of e-commerce in Tier 2 and Tier 3 cities is further increasing accessibility to beverage and personal care products, boosting the demand for secure and high-quality aluminum closures across multiple industries.

India: Sustainable Packaging and Beverage Growth Propel Market Expansion

India’s aluminum caps and closures market is driven by a combination of governmental sustainability initiatives and rising demand in the beverage sector. Policies such as the Plastic Waste Management (Amendment) Rules, aimed at phasing out certain single-use plastics, are creating a strong market preference for eco-friendly and reusable aluminum closures.

The rapid expansion of ready-to-drink (RTD) beverages, fueled by rising disposable incomes, urbanization, and a health-conscious younger demographic, is further catalyzing market growth. Strategic investments, including Ball Corporation’s expansion of aluminum can production facilities, are addressing the increasing demand. Additionally, the health and wellness trend is driving growth in pharmaceutical and nutraceutical applications, which are significant segments for aluminum closures in India.

Aluminum Caps and Closures Market Report Scope

Aluminum Caps and Closures Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2034)

|

$11.8 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Product Type (ROPP Caps, Non-Refillable Closures, Easy Open Ends, Other Closures), By End-Use Industry (Beverages, Pharmaceuticals & Healthcare, Food, Cosmetics & Personal Care, Other Industries), By Cap Type (Screw Caps, Crown Cork, Lug/Press Twist, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Guala Closures Group, Amcor plc, Crown Holdings Inc., Ball Corporation, Silgan Holdings Inc., Toyo Seikan Group Holdings Ltd., CANPACK Group, Nippon Closures Co., Ltd., O. Berk Company, Closure Systems International, Inc., Tecnocap S.p.A., Pelliconi & C. S.p.A., BERICAP Group, Federfin Tech S.r.l., Massilly Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aluminum Caps and Closures Market Segmentation

By Product Type

- ROPP Caps

- Non-Refillable Closures

- Easy Open Ends

- Other Closures

By End-Use Industry

- Beverages

- Pharmaceuticals & Healthcare

- Food

- Cosmetics & Personal Care

- Other Industries

By Cap Type

- Screw Caps

- Crown Cork

- Lug/Press Twist

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aluminum Caps and Closures Market

- Guala Closures Group

- Amcor plc

- Crown Holdings Inc.

- Ball Corporation

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings Ltd.

- CANPACK Group

- Nippon Closures Co., Ltd.

- O. Berk Company

- Closure Systems International, Inc.

- Tecnocap S.p.A.

- Pelliconi & C. S.p.A.

- BERICAP Group

- Federfin Tech S.r.l.

- Massilly Group

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global aluminum caps and closures market, exploring breakthroughs in lightweighting, high-performance alloy development, smart tamper-evident features, and sustainable post-consumer recycled (PCR) content initiatives. The analysis reviews market dynamics across beverages, pharmaceuticals, food, and personal care sectors, highlighting premiumization trends, circular economy adoption, and technological innovations that enhance product safety, brand differentiation, and supply chain efficiency. It highlights opportunities emerging from advanced coating technologies, digital-enabled closures, and expansion into non-beverage markets such as cosmetics and gourmet foods. This report is an essential resource for manufacturers, investors, and packaging professionals seeking insights into product types, end-use applications, regional growth patterns, and competitive strategies. By integrating historical data from 2021–2024 with forecasts through 2025–2034, and profiling 15+ leading companies, it provides actionable intelligence on production capacities, sustainability initiatives, and market innovations that are shaping the industry’s evolution.

Scope Highlights:

- Segmentation: By Product Type (ROPP Caps, Non-Refillable Closures, Easy Open Ends, Other Closures), By End-Use Industry (Beverages, Pharmaceuticals & Healthcare, Food, Cosmetics & Personal Care, Other Industries), By Cap Type (Screw Caps, Crown Cork, Lug/Press Twist, Others)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies including Guala Closures Group, Amcor plc, Crown Holdings Inc., Ball Corporation, and Closure Systems International, Inc.

Methodology

USDAnalytics applied a rigorous research methodology combining primary interviews with industry stakeholders, including manufacturers, brand owners, and distributors, with secondary research from corporate reports, regulatory filings, trade journals, and market publications. Market sizing and forecasting were performed using historical production, consumption, and trade data, supplemented by demand analysis across key end-use sectors such as beverages, pharmaceuticals, and cosmetics. Qualitative insights focused on technological innovations, premiumization, smart closures, and sustainability-driven practices, while quantitative evaluation analyzed production capacity, market share, and growth potential of leading global players. Regional analyses incorporated regulatory frameworks, recycling infrastructure, and consumer trends to identify opportunities for expansion, eco-friendly adoption, and advanced alloy application. This integrated approach ensures actionable intelligence for industry professionals navigating competitive dynamics, innovation trends, and sustainability mandates.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.