Pharmaceutical Caps and Closures Market Size, Overview, and Growth Outlook (2025–2034)

Pharmaceutical Caps and Closures Market Projected to Reach $5.2 Billion by 2034 Amid Rising Regulatory and Patient-Centric Demands

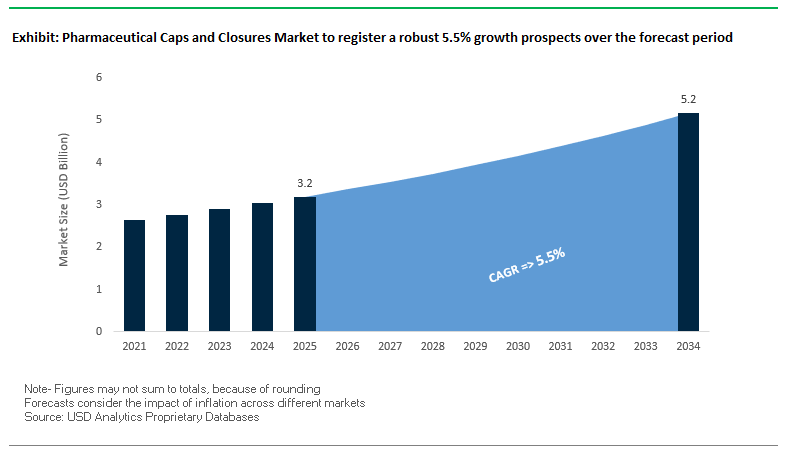

The Global Pharmaceutical Caps and Closures Market is anticipated to grow from $3.2 billion in 2025 to $5.2 billion by 2034, at a CAGR of 5.5%. The market encompasses a wide range of stoppers, caps, seals, and dispensing systems that ensure the safety, sterility, and efficacy of pharmaceutical products. The growth is driven by stringent regulatory compliance, rising demand for tamper-evident and child-resistant solutions, and innovations in patient-centric packaging.

Key Insights for industry professionals and buyers:

- Container Closure Integrity (CCI): Increasing focus on preventing microbial ingress and ensuring product stability across shelf life.

- Patient Safety and Ease of Use: Growth in advanced dispensing systems, including controlled-dosing droppers, pump sprays, and injectable device closures.

- Materials Innovation: High-performance polymers, specialized elastomers, and inert glass are critical for biologics and high-potency drugs.

- Digital and Smart Packaging: NFC tags and QR codes are being integrated into closures to enhance security, traceability, and patient adherence tracking.

- Sustainability Trends: Industry investment in eco-friendly materials and manufacturing processes aligns with global environmental standards.

Market Analysis: Market Expansion Driven by Regulatory Compliance, Sustainability Initiatives, and Strategic Manufacturing Investments

The pharmaceutical caps and closures industry has witnessed dynamic developments in recent years, fueled by regulatory mandates, patient safety priorities, and material innovation. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, enhancing its capabilities for the Latin American market. The same month, SCHOTT AG announced the addition of syringe and cartridge glass tubing in India, positioning itself as Asia’s largest producer of such components. Concurrently, Plastipak showcased sustainable, bio-based, and advanced barrier solutions at Drinktec in Munich, reflecting innovations adaptable for pharmaceutical applications. Regulatory pressures such as the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, underscore a broader trend toward safe and sustainable packaging materials, impacting pharmaceutical closure design as well.

Consumer and industry insights are shaping innovation in closures. Programs by the Pet Sustainability Coalition in July 2025 and studies highlighting consumer preference for “less-plastic” alternatives in June 2025 are accelerating the adoption of sustainable closures. Strategic investments in advanced manufacturing processes are evident, with West Pharmaceutical Services introducing a new automated molding cell in May 2025, highlighting a commitment to high-quality components. Similarly, Duni Group and other companies have made significant moves to reduce PFAS use in packaging, signaling cross-sector trends in material safety and sustainability.

Technological integration and product differentiation remain central to market growth. Companies are incorporating smart packaging technologies and improving material compatibility with biologics and sensitive drugs. The combined effect of regulatory compliance, sustainability mandates, and patient-centric innovation positions the pharmaceutical caps and closures market for steady growth at 5.5% CAGR through 2034, with an increasing emphasis on integrated, high-performance, and environmentally responsible solutions.

Transformative Trends and Emerging Opportunities in the Pharmaceutical Caps and Closures Market

Accelerated Adoption of Integrated Serialization Solutions

Serialization has become one of the most disruptive forces shaping the pharmaceutical caps and closures market, driven by regulatory mandates across major global markets. In the United States, the Drug Supply Chain Security Act (DSCSA) has reached its final stage, requiring interoperable electronic tracing of prescription drugs. While the FDA provided a stabilization period through November 2024 and partial exemptions into 2025, the enforcement deadline for manufacturers and repackagers to comply went into effect on May 27, 2025. This has shifted serialization requirements beyond the carton level, creating demand for integrated solutions within closures themselves to ensure end-to-end traceability. In Europe, the Falsified Medicines Directive (FMD) set a strong precedent by mandating unique identifiers and tamper-evident features on prescription drug packaging, fueling adoption of closures with breakaway rings and embedded security features. The industry is moving beyond traditional labels and cartons by embedding serialized 2D barcodes directly onto closures and developing tamper-evident caps that irreversibly indicate interference. For example, child-resistant closures now combine serialization codes with tamper tabs, providing both compliance and consumer protection. These innovations demonstrate how serialization is no longer confined to tracking systems but has become integral to closure design itself, making caps critical to compliance, safety, and supply chain transparency.

Strategic Material Shift Towards High-Performance Polymers and Composites

The increasing prevalence of advanced biologics, biosimilars, and mRNA-based medicines is transforming material requirements for pharmaceutical closures. Conventional plastics and glass are limited in protecting these sensitive drugs, which demand superior barriers against oxygen, moisture, and UV exposure. Advanced polymer composites and engineered nanomaterials are emerging as preferred solutions, providing enhanced stability and extended shelf life. Academic research highlights how polymer composites can significantly reduce adsorption, preventing drug loss from container-wall interaction and ensuring maximum potency. For biologics and vaccines requiring strict cold chain conditions, these polymers are engineered to maintain mechanical integrity and sealing ability even under extreme temperature fluctuations. For example, closures designed for ultra-cold storage of mRNA vaccines can withstand cracking risks and maintain airtight seals during transit. This shift not only safeguards drug efficacy but also reduces wastage and ensures compliance with pharmaceutical cold chain logistics standards. As biologics and precision medicines expand, high-performance polymer-based closures are expected to dominate, setting new benchmarks for barrier performance and material compatibility in the global pharmaceutical caps and closures market.

Expansion of Smart/Connected Closure Systems for Patient Adherence

The pharmaceutical sector is exploring smart closures as a powerful tool to improve adherence, traceability, and patient outcomes. In clinical trials, adherence tracking has historically relied on pill counts and self-reported diaries, both prone to inaccuracies. Smart closure systems equipped with NFC technology now automatically log each bottle opening, transmitting time-stamped data to mobile applications. This real-time tracking improves trial accuracy, reduces costs, and enhances regulatory confidence in trial data integrity. Beyond trials, connected closures are emerging in chronic disease management. For example, smart closures integrated with digital reminders—via flashing indicators or smartphone notifications—support patients in adhering to complex medication regimens. This is especially critical for therapies where missed doses carry severe health risks, such as HIV treatments, oncology drugs, or transplant medications. By bridging digital health with packaging innovation, smart closures are positioned to play a central role in adherence monitoring, outcome-based healthcare, and patient-centric drug delivery models.

Development of Monomaterial and Recyclable Closure Systems

The circular economy and Extended Producer Responsibility (EPR) regulations are accelerating the demand for recyclable pharmaceutical packaging. Traditional closures, often made with mixed materials such as polypropylene (PP) caps and polyethylene (PE) liners, are difficult to recycle and increase EPR compliance costs. The opportunity lies in designing monomaterial closure systems that are fully recyclable in existing infrastructure. Innovations such as single-resin closures, made entirely from PP or PE, simplify sorting processes and ensure compatibility with recycling streams. Additionally, brands are working with packaging suppliers to reduce the weight of closures, cutting virgin resin use while maintaining child resistance and tamper evidence. Several major pharmaceutical companies have already pledged to shift toward recyclable and lighter-weight packaging, reflecting growing alignment with sustainability goals. For example, collaborations are underway to develop all-PE containers with closures designed to be recycled alongside the bottle, creating an integrated circular system. This not only reduces EPR fees but also enhances brand reputation by aligning with global sustainability pledges, particularly as healthcare packaging faces mounting scrutiny over plastic waste.

Competitive Landscape: Leading Pharmaceutical Caps and Closures Companies Drive Market Innovation Through Materials Expertise and Patient-Centric Solutions

The global pharmaceutical caps and closures industry is defined by key players focusing on high-performance, durable, and increasingly sustainable solutions for drug containment and delivery.

Gerresheimer AG: Expanding Global Glass and Plastic Closure Capabilities for High-Precision Applications

Gerresheimer offers a wide portfolio of closures, including screw-on caps, stoppers, and dispensing devices such as inhalers and auto-injectors. In August 2025, the company expanded its India operations to produce high-precision syringe and cartridge glass tubing. Gerresheimer’s strengths include a global manufacturing footprint, integrated solutions, and commitment to sustainability, including sourcing 100% renewable electricity by 2030.

AptarGroup, Inc.: Innovating Dispensing and Closure Systems with Patient-Centric Technologies

Aptar provides dispensing closures, metered dose pumps, and specialized valves for oral, nasal, and topical drug delivery. In August 2025, the company partnered to develop new pet care solutions, showcasing its broad expertise in precision dispensing. Aptar’s strategy emphasizes patient-centric innovation, smart packaging, and sustainability initiatives. Its extensive patent portfolio underpins high-value, high-performance closure systems.

West Pharmaceutical Services, Inc.: Pioneering Integrated Containment and Delivery Systems for Injectable Medicines

West is a global leader in stoppers, seals, and advanced self-injection systems. The company’s “Simplify the Journey” program combines packaging, delivery systems, and regulatory support to accelerate product commercialization. Recent investments include a new automated molding cell in May 2025. West’s focus on patient safety, high-quality components, and innovation makes it a trusted partner for pharmaceutical and biotech companies worldwide.

SCHOTT AG: Strengthening Specialty Glass Solutions for Biologics and Injectable Packaging

SCHOTT provides glass vials, ampoules, and specialized closures. In August 2025, the company invested in India to produce syringe and cartridge glass tubing, enhancing supply for biologics in Asia. Its FIOLAX® glass is recognized globally for chemical inertness, stability, and quality, while its strategy emphasizes innovation, sustainability, and manufacturing footprint expansion.

Silgan Holdings Inc.: Delivering Rigid Packaging and Closure Solutions Across Pharmaceuticals and Healthcare

Silgan offers plastic and metal caps, closures, and dispensing systems for pharmaceuticals, OTC medications, and nutritional supplements. The company’s vertically integrated model ensures container-closure compatibility, simplifies supply chains, and supports consistent quality. Strategic focus lies in continuous product innovation, technological upgrades, and leadership in pharmaceutical packaging solutions.

Pharmaceutical Caps and Closures Market Share Insights, 2025-2034

CRCs Dominate Market Share by Product Type in Pharmaceutical Caps and Closures

Child-resistant caps (CRCs) account for the largest share at 28% of the pharmaceutical caps and closures market, underlining their status as a regulatory-mandated component across oral solid and liquid medications. Their widespread adoption is tied to strict legislation such as the U.S. Poison Prevention Packaging Act (PPPA) and equivalent frameworks in Europe and Asia, which require tamper-resistance and protection against accidental pediatric ingestion. Beyond regulatory necessity, manufacturers have invested heavily in improving usability, developing senior-friendly CRCs that balance accessibility with safety. Vials and stoppers represent the second-largest segment, with growth fueled by the surge in biologics and vaccines requiring aseptic parenteral packaging solutions. Screw caps, tamper-evident (TE) closures, and droppers support high-volume OTC and specialty drug categories, while snap-on caps, seals, and overcaps serve niche or secondary roles. Collectively, the hierarchy highlights how compliance, safety, and the rise of injectables are shaping the competitive balance of pharmaceutical closure types.

Bottles and Jars Lead Market Share by Application in Pharmaceutical Caps and Closures

Bottles and jars dominate with 45% share of pharmaceutical caps and closures applications, reflecting the high global consumption of tablets, capsules, and syrups as the most common drug delivery formats. Their prevalence ensures steady demand for CRCs and tamper-evident features, which are non-negotiable for patient safety and regulatory compliance. Vials and ampoules, holding 30% of the share, serve as the technological backbone of sterile injectables and high-value biologics, where container closure integrity (CCI) is critical to maintaining drug efficacy. Tubes remain essential for topical treatments such as dermatological and ophthalmic drugs, while syringes and cartridges gain traction as advanced platforms for biologics, prefilled formats, and emergency-use therapies like epinephrine auto-injectors. Sachets and pouches are smaller but growing rapidly for clinical trial kits and single-dose applications, particularly in cost-sensitive markets. The dominance of bottles and jars underscores how volume-driven oral dosage forms define the market, while sterile packaging formats capture the value edge.

United States Pharmaceutical Caps and Closures Market Driven by FDA Regulations and Innovation

The United States pharmaceutical caps and closures market is shaped heavily by FDA regulations on material compatibility and drug-device combination products, directly influencing closure design and manufacturing. A major focus is on child-resistant yet senior-friendly closures, exemplified by AptarGroup’s Defender-Lok line, which balances safety and accessibility. With the rise of biologics and specialty drugs, demand is increasing for sophisticated stoppers and seals for pre-filled syringes and vials to preserve sterility and extend shelf life.

Another key growth area is anti-counterfeiting closures integrated with serialized barcodes and RFID tags to comply with the Drug Supply Chain Security Act (DSCSA). Sustainability is also advancing, with companies developing closures made from recycled plastics and bio-based polymers to lower environmental impact. Additionally, the booming over-the-counter (OTC) pharmaceuticals market is fueling demand for tamper-evident closures that reassure consumer safety while maintaining usability.

Germany Pharmaceutical Caps and Closures Market Focused on Safety, Sustainability, and Lightweighting

The Germany pharmaceutical caps and closures market is at the forefront of sustainable material adoption, with widespread use of PET and HDPE closures due to their recyclability and protective barrier properties. German firms like Bericap GmbH & Co. KG are innovating with lightweight closure designs, reducing raw material consumption and transportation costs without compromising safety.

Compliance with stringent EU and national pharmaceutical packaging regulations ensures closures maintain drug integrity and patient safety. Increasing demand for child-resistant and tamper-evident closures reflects evolving safety requirements. Germany’s strong industrial base and R&D culture also drive continuous innovation, particularly in advanced closure systems that meet both safety and sustainability goals.

United Kingdom Pharmaceutical Caps and Closures Market Backed by EPR and Sustainable Manufacturing Initiatives

The United Kingdom pharmaceutical caps and closures market is shaped by the Extended Producer Responsibility (EPR) framework, which places the cost of packaging waste management on producers, pushing companies toward sustainable material adoption. The Sustainable Medicines Manufacturing Innovation Programme (SMMIP) is fostering greener solutions, including eco-friendly closure systems and sustainable chemistry in manufacturing.

There is growing momentum in smart closures that track patient adherence, particularly for chronic and complex treatments. UK companies are aligning with European Pharmacopoeia (Ph. Eur.) and United States Pharmacopeia (USP) standards to maintain quality and compliance. Circular economy initiatives are also gaining ground, with investments in the recycling of complex multi-material pharmaceutical packaging, positioning the UK as a progressive hub for sustainable closure innovation.

China Pharmaceutical Caps and Closures Market Expanding Under GMP and NMPA Oversight

The China pharmaceutical caps and closures market is governed by the National Medical Products Administration (NMPA), which has strengthened GMP guidelines for packaging material manufacturers. Since June 2025, packaging suppliers must work closely with drug marketing authorization holders (MAHs) to ensure quality management and compliance. This regulatory shift is enhancing accountability across the supply chain.

Market growth is driven by tamper-evident and child-resistant closures, essential for ensuring patient safety and drug authenticity. China’s rapidly expanding pharmaceutical sector is fueling demand for cost-effective yet high-quality caps and closures, especially in sterile injectables and specialty drugs. Domestic companies are scaling up advanced closure manufacturing capabilities, aligning with both safety requirements and global export standards.

India Pharmaceutical Caps and Closures Market Boosted by Domestic Manufacturing and Growing Demand

The India pharmaceutical caps and closures market is expanding under strict oversight from the Ministry of Health and Family Welfare and the CDSCO, which enforce rigorous safety and quality standards. Demand is particularly high in oral dosage forms, driving the adoption of screw-on and press-on closures for bottles.

Innovation is visible with companies like Bharat Rubber Works, showcasing a range of rubber stoppers, flip-off seals, and dosing closures at CPHI & PMEC India 2025. Growing consumer interest in nutraceuticals and OTC products is further boosting specialized closure demand. India’s Make in India initiative is encouraging domestic production of advanced pharmaceutical packaging components, positioning the country as a key supplier for both domestic and export markets.

Japan Pharmaceutical Caps and Closures Market Led by Smart and Eco-Friendly Solutions

The Japan pharmaceutical caps and closures market is being shaped by the country’s aging population and rising prevalence of chronic diseases, which increase demand for specialized closures for long-term therapies. Smart closures that track patient adherence and real-time usage data are emerging as valuable tools for healthcare providers.

Sustainability is also advancing, with companies developing biodegradable and recyclable closure materials to align with environmental policies. Japan’s stringent regulatory framework ensures that closures meet the highest standards of safety, security, and tamper evidence. Supported by government grants and industry incentives, Japanese firms are investing in eco-friendly closure systems that combine technological innovation with strong patient safety performance.

Pharmaceutical Caps and Closures Market Report Scope

Pharmaceutical Caps and Closures Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material (Plastic, Metal, Rubber, Glass, Others), By Product Type (Screw Caps, Snap-on Caps, CRC, TE Closures, Dropper Closures, Vials & Stoppers, Seals & Overcaps, Others), By Application (Bottles & Jars, Vials & Ampoules, Tubes, Containers & Jars, Syringes & Cartridges, Sachets & Pouches, Others), By End-Use Industry (Pharmaceutical & Biopharmaceutical, Nutraceuticals, OTC & Dietary Supplements)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AptarGroup, Inc., Gerresheimer AG, Berry Global, Inc., Bormioli Pharma S.p.A., Avanzato Packaging, Caps & Closures Pty Ltd., Amcor plc, Alpla Group, Rieke Packaging Systems (a part of TriMas Corporation), Shijiazhuang Jihong Pharmaceutical Packaging Co., Ltd., West Pharmaceutical Services, Inc., SKS Bottle & Packaging, Inc., Adelphi Healthcare Packaging, Bericap GmbH & Co. KG, SGD S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pharmaceutical Caps and Closures Market Segmentation

By Material

- Plastic

- Metal

- Rubber

- Glass

- Others

By Product Type

- Screw Caps

- Snap-on Caps

- CRC

- TE Closures

- Dropper Closures

- Vials & Stoppers

- Seals & Overcaps

- Others

By Application

- Bottles & Jars

- Vials & Ampoules

- Tubes

- Containers & Jars

- Syringes & Cartridges

- Sachets & Pouches

- Others

By End-Use Industry

- Pharmaceutical & Biopharmaceutical

- Nutraceuticals

- OTC & Dietary Supplements

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pharmaceutical Caps and Closures Market

- AptarGroup, Inc.

- Gerresheimer AG

- Berry Global, Inc.

- Bormioli Pharma S.p.A.

- Avanzato Packaging

- Caps & Closures Pty Ltd.

- Amcor plc

- Alpla Group

- Rieke Packaging Systems (a part of TriMas Corporation)

- Shijiazhuang Jihong Pharmaceutical Packaging Co., Ltd.

- West Pharmaceutical Services, Inc.

- SKS Bottle & Packaging, Inc.

- Adelphi Healthcare Packaging

- Bericap GmbH & Co. KG

- SGD S.A.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and systematic research methodology to deliver accurate and actionable insights into the Pharmaceutical Caps and Closures Market. Our approach integrates both primary and secondary research, including interviews with industry stakeholders such as closure manufacturers, pharmaceutical companies, regulatory authorities, and supply chain partners to capture first-hand insights on market trends, innovations, and compliance challenges. Secondary research sources, including verified trade publications, corporate annual reports, regulatory guidelines, and industry databases, are used to validate historical and current market data. Market sizing, CAGR projections, and segmentation analysis are derived using top-down and bottom-up approaches, factoring in regulatory mandates like the DSCSA, FMD, and EU PPWR, alongside consumer preferences for safety, usability, and sustainable closures. USDAnalytics also evaluates technological innovations such as smart and connected closures, high-performance polymers, and monomaterial designs, while analyzing regional market adoption patterns, end-use applications, and strategic corporate investments. This methodology ensures industry professionals gain a precise, forward-looking understanding of growth opportunities, material trends, and patient-centric packaging solutions, facilitating informed business and investment decisions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.