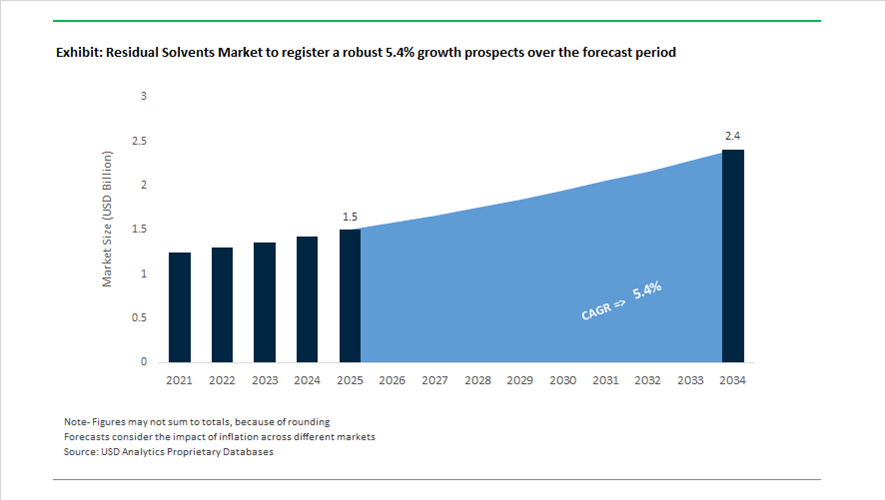

Residual Solvents Market Valued at $1.5 Billion in 2025, Projected to Reach $2.4 Billion by 2034 at 5.4% CAGR

The global residual solvents market is valued at $1.5 billion in 2025 and is projected to reach $2.4 billion by 2034, expanding at a CAGR of 5.4%. Growth is driven by tightening regulatory scrutiny over Class 1, Class 2, and Class 3 solvents, increased pharmaceutical manufacturing volumes, and expanding demand for residual solvent testing services, gas chromatography (GC) analysis, impurity profiling, GMP-compliant solvent validation, and low-VOC formulation development. As global API and generics production accelerates, especially in India and China, manufacturers are strengthening solvent recovery systems, validation protocols, and analytical infrastructure to meet evolving ICH, USP, and European Pharmacopoeia standards.

Regulatory revisions are reshaping compliance frameworks. In July 2025, the ICH Q3C Expert Working Group initiated a formal work plan to revise the Permitted Daily Exposure (PDE) limits for Dimethylformamide (DMF), Dichloromethane (DCM), and Ethylene Glycol (EtG). A restructured support document is expected to reach Step 4 adoption by December 2026, compelling pharmaceutical manufacturers to revalidate solvent residual thresholds across product portfolios. In parallel, the U.S. Pharmacopeia issued a Notice of Intent to Revise several monographs in July 2025, including Ascorbyl Palmitate and Olmesartan Medoxomil, with updates becoming official on February 1, 2026. These revisions emphasize tighter impurity profiling and solvent purity documentation. India’s ₹6,940 crore Production Linked Incentive scheme for APIs, implemented across 2024 and 2025, has further accelerated investment in advanced residual solvent testing laboratories to ensure export compliance with ICH Q3C guidelines.

Analytical capacity expansion is accelerating globally. Waters Corporation reported 10% growth in pharmaceutical sales in Q4 2024, driven by high-volume quality control for GLP-1 drugs and generic APIs, prompting expanded deployment of high-sensitivity solvent testing instruments into 2025. In 2025, Eurofins CDMO Alphora installed a Waters Acquity UPC2® Supercritical Fluid Chromatography system for complex impurity separations, progressing toward full GMP qualification within the same year. Eurofins expanded its global footprint in 2025 by establishing 14 new laboratories and adding 46,000 square meters of operational space, supporting large-scale residual solvent screening. In February 2026, Shimadzu launched the Nexera IC Ion Chromatograph with enhanced automation capabilities, building on prior AI-enabled LabSolutions MD systems to streamline impurity analysis workflows.

Industrial solvent reformulation trends complement pharmaceutical compliance. In April 2025, 3M introduced biodegradable solvent alternatives designed to replace high-VOC Class 2 solvents in industrial processes. In February 2025, Arxada launched Polyboost™, integrating quaternary ammonium chemistry into coatings while maintaining low-VOC solvent compliance. Additionally, Aditya Birla Chemicals’ June 2025 acquisition of Cargill’s specialty business in Georgia expanded its portfolio in solvent-related advanced materials, strengthening North American supply integration.

The residual solvents market is increasingly characterized by ICH Q3C PDE revisions, GMP-compliant impurity profiling, high-sensitivity GC and SFC analytical systems, API-focused laboratory expansion, biodegradable low-VOC solvent substitution, and regulatory-driven quality control modernization. As pharmaceutical production volumes grow and impurity thresholds tighten globally, advanced analytical infrastructure and solvent management technologies remain central to market expansion and regulatory adherence.

Key Trends and Monetizable Opportunities in the Residual Solvents Market

Compliance-Led Transition Toward Class 3 and Bio-Based “Green” Solvents

The residual solvents market is undergoing a structural reset as regulatory scrutiny tightens around solvent toxicity, worker exposure, and long-term patient safety. What was previously framed as a sustainability preference has now become a compliance-driven necessity across pharmaceutical, agrochemical, and specialty chemical supply chains. The endorsement of the ICH Q3C(R10) Concept Paper in January 2025 marked a decisive inflection point, signaling a reassessment of Permitted Daily Exposure limits for widely used solvents such as N,N-Dimethylformamide and Dichloromethane. With Dichloromethane facing potential reclassification into the highest-risk category, manufacturers are being forced to proactively reformulate processes to avoid future non-compliance, recalls, or regulatory delays.

This shift is accelerating the substitution of Class 2 solvents with Class 3 alternatives such as ethanol, ethyl acetate, and isopropyl alcohol. These solvents offer significantly lower toxicological risk while maintaining acceptable volatility and solvency profiles for most synthesis and purification steps. By 2025, qualification of Class 3 solvents has become a board-level priority for global pharmaceutical companies, particularly those supplying regulated markets in the United States, Europe, and Japan, where post-approval changes are increasingly costly and time-consuming.

Parallel to regulatory pressure, innovation in bio-based solvent chemistry is reshaping competitive differentiation. The commercialization of levulinate-ketal and biomass-derived solvent systems in late 2025 demonstrates that green solvents are no longer limited to niche applications. These next-generation alternatives are engineered to deliver comparable boiling points and drying behavior to petrochemical solvents while offering substantially higher biodegradability and lower life-cycle emissions. Their adoption is particularly strong in cosmetics and pharmaceutical intermediates, where brand owners face rising pressure to demonstrate measurable reductions in environmental footprint without compromising process reliability.

Ultra-High-Purity Solvents Become Non-Negotiable for Advanced Semiconductor and Battery Manufacturing

A second defining trend in the residual solvents market is the rapid escalation of purity requirements driven by advanced semiconductor nodes and next-generation lithium-ion battery manufacturing. The expansion of AI-centric computing, electric vehicles, and energy storage has pushed solvent specifications far beyond traditional electronic-grade standards. By 2025, leading-edge semiconductor fabrication facilities operating at 3nm and below require isopropyl alcohol and related solvents with moisture levels below 10 ppm and metal impurities measured in parts per trillion.

The transition to 300mm wafer processing has further amplified solvent demand intensity. Compared with legacy 200mm wafers, solvent consumption per production unit has increased by approximately 30%, directly magnifying the operational and financial impact of contamination events. Even trace ionic or metallic impurities can disrupt doping precision and yield performance, making ultra-high-purity residual solvents mission-critical inputs rather than interchangeable commodities.

This demand surge is reinforced by unprecedented capital investment. More than 200 billion dollars has been committed globally to new semiconductor fabrication facilities through 2030, with advanced logic nodes accounting for a rapidly growing share of installed capacity by the end of 2025. A similar purity-driven dynamic is unfolding in battery gigafactories, where solvent cleanliness directly influences electrode performance, cycle life, and safety. As a result, solvent suppliers with advanced purification, drying, and contamination control capabilities are capturing premium pricing and long-term supply agreements in both sectors.

Circular Economy Enablement Through NMP Recovery and Bio-Based Solvent Supply

The explosive growth of lithium-ion battery manufacturing has created a structurally attractive opportunity in solvent recovery and reuse, particularly for N-Methyl-2-pyrrolidone. As a critical solvent in electrode slurry preparation, NMP represents both a significant cost center and an environmental liability when discarded. By 2025, leading battery manufacturers have integrated industrial-scale solvent recovery systems directly into production lines, transforming residual solvent management into a source of operational resilience.

Advanced recovery architectures combining adsorption and membrane separation technologies are now achieving recovery efficiencies exceeding 99.9%. This allows producers to recirculate ultra-pure NMP back into the process loop while sharply reducing exposure to volatile raw material pricing and tightening environmental regulations. Beyond cost savings, these systems directly support corporate decarbonization strategies by lowering scope 3 emissions associated with solvent procurement and disposal.

At the same time, investments in bio-refinery infrastructure are expanding the supply of renewable solvent intermediates. Large-scale facilities commissioned since mid-2024 are leveraging biochemical and catalytic pathways to produce green olefins and multifunctional esters with carbon footprints roughly 30% lower than conventional fossil-based equivalents. For solvent suppliers, this convergence of recovery technology and bio-based production represents a scalable pathway to support Net-Zero commitments without compromising solvent performance or supply security.

Specialized Solvent Systems for Amorphous Solid Dispersion in Pharmaceuticals

The pharmaceutical industry’s shift toward poorly soluble active ingredients has unlocked a high-margin niche within the residual solvents market. Amorphous Solid Dispersion has become a primary formulation strategy for enhancing the bioavailability of BCS Class II compounds, placing new performance demands on solvent systems used in spray drying and hot-melt extrusion processes.

These advanced formulations require precisely engineered binary and ternary solvent blends that deliver controlled evaporation rates, predictable solubility behavior, and consistent interaction with polymer carriers. By 2025, pharmaceutical developers increasingly specify high-purity dichloromethane-methanol or acetone-water systems with tight impurity limits to prevent phase separation or recrystallization during processing. Any variability in solvent quality can directly compromise drug stability and clinical performance, elevating residual solvents from auxiliary inputs to critical quality enablers.

The next wave of ASD development is further intensifying this opportunity. Second-generation formulations incorporating highly viscous polymers demand solvent carriers capable of maintaining thermodynamic stability under more complex processing conditions. This has created demand for pre-blended, validated solvent systems supplied with comprehensive documentation and reproducibility data. For solvent producers, offering ready-to-use ASD solvent solutions reduces formulation complexity for drug developers while commanding premium margins tied to regulatory assurance and time-to-market acceleration.

Residual Solvents Market Share and Segmentation Insights

Class 2 Solvents Dominate Residual Solvent Analysis Due to Strict Pharmaceutical Regulatory Limits

Class 2 solvents accounted for 48.60% of the residual solvents market in 2025, reflecting their widespread use in pharmaceutical manufacturing, chemical synthesis, and active pharmaceutical ingredient (API) production. Common solvents such as acetonitrile, dichloromethane, methanol, toluene, and xylene fall within this category and are subject to strict regulatory control due to potential toxicity risks. The dominance of Class 2 solvents in residual solvent testing is closely tied to ICH Q3C guidelines, which define permissible daily exposure limits and require rigorous monitoring during pharmaceutical development and production. A key 2025 market driver is the strengthening of global regulatory harmonization, where pharmaceutical manufacturers must demonstrate consistent analytical compliance through validated testing methods to secure product approvals across international regulatory jurisdictions.

Pharmaceuticals & Biopharmaceuticals Lead Residual Solvent Testing Demand

Pharmaceuticals and biopharmaceuticals represent the largest end-user segment in the residual solvents market, accounting for 58.60% of total analytical demand in 2025. Drug manufacturers must conduct comprehensive residual solvent testing throughout drug development, scale-up, and commercial manufacturing to ensure patient safety and regulatory compliance. High-value pharmaceutical products justify extensive analytical quality control using techniques such as gas chromatography and advanced spectroscopic methods. A significant 2025 industry shift is the increasing adoption of continuous pharmaceutical manufacturing, which requires residual solvent monitoring to transition from batch-based testing to real-time or at-line analytical methods. This transition is accelerating the development of rapid gas chromatography techniques and process analytical technology (PAT) systems that enable real-time release testing and improved process control in continuous production environments.

Residual Solvents Market Competitive Landscape

The 2026 residual solvents market is defined by high-sensitivity headspace GC-MS/MS systems, automation-first lab workflows, and compliance with ICH Q3C(R8) and USP <467>. Growth is driven by helium replacement strategies, ultra-trace detection requirements, and expanding pharmaceutical and cannabis testing applications.

Agilent accelerates high-throughput residual solvent testing with dual-channel GC systems and helium-free workflows

Agilent Technologies Inc. is advancing residual solvent analysis through integrated Smart-Connected lab solutions and next-generation GC platforms. The Intuvo 9000 and 8890 GC systems enable simultaneous execution of USP <467> Procedures A and B, reducing analysis time by 50%. Validation of hydrogen and nitrogen carrier gases addresses the 2026 helium supply constraints while maintaining analytical accuracy using inert flow paths and advanced headspace sampling. Dedicated cannabis and hemp testing workflows expand application coverage for volatile impurities in regulated markets. The Technology Refresh Program supports laboratory upgrades with 21 CFR Part 11-compliant systems. Focus on automation and throughput enhances efficiency in pharmaceutical QA/QC environments.

Merck strengthens high-purity solvent leadership with SupraSolv and flexible supply formats for analytical precision

Merck KGaA is reinforcing its position in residual solvent testing through ultra-high-purity reagents and analytical-grade solvents. The SupraSolv® Headspace range ensures Class 1 solvent impurities remain below 1 µg/g, enabling high signal-to-noise ratios in GC detection systems. Strong demand from the $4.2 billion pharmaceutical solvent market supports growth in alcohol and ketone product segments. Expansion of flexible packaging formats, from ampoules to bulk delivery, supports scalability in biopharmaceutical manufacturing. UniSolv® simplifies laboratory workflows by offering a universal solvent solution across GC applications. Focus on purity and consistency supports ultra-trace detection in complex API matrices.

Shimadzu enhances ultra-trace solvent detection with NX-series headspace technology and AI-driven method automation

Shimadzu Corporation is advancing sensitivity and reproducibility in residual solvent analysis through its HS-20 NX series and Nexis™ GC-2030 platform. Carry-over reduction to one-tenth of conventional systems improves reliability in complex matrices such as DMF and DMSO. Area repeatability between 1% and 3% RSD over multiple runs demonstrates high analytical precision. Validated methods for Class 2 solvents, including CPME and TBA, support compliance with updated ICH guidelines. LabSolutions MD software automates method development and peak resolution for complex formulations. Integration of advanced pressure control and thermal uniformity enhances consistency in high-throughput laboratories.

Waters advances sensitivity with APGC-MS technology and automated quantitation for complex solvent matrices

Waters Corporation is enhancing residual solvent detection through Atmospheric Pressure Gas Chromatography coupled with mass spectrometry. The Xevo TQ-GC system provides higher sensitivity and reduced fragmentation compared to traditional ionization techniques, improving detection of trace-level impurities. Expansion into solvent recycling and purification supports sustainable laboratory operations. Financial solutions under Waters Capital facilitate adoption of advanced GC-MS/MS systems. MassLynx software automates quantitation workflows, reducing manual intervention in high-volume testing. Focus on analytical precision supports pharmaceutical and specialty chemical applications requiring ultra-low detection limits.

Thermo Fisher integrates green lab initiatives with automated headspace GC systems for regulatory compliance

Thermo Fisher Scientific is combining sustainability and analytical performance in residual solvent testing through its Greener Choice program. The TriPlus 500 headspace autosampler utilizes valve-and-loop technology to minimize dead volume and ensure accurate sample transfer. Integration with TRACE 1600 GC and Chromeleon CDS provides centralized data management and audit trail compliance for FDA-regulated labs. Investment in sustainable consumables reduces hazardous chemical usage in laboratory workflows. Supplier mandates for Scope 3 emissions align with broader sustainability goals across the analytical ecosystem. Focus on automation and compliance supports large-scale pharmaceutical testing operations.

Honeywell drives low-GWP solvent innovation with Solstice platform and analytical-grade chemical portfolio expansion

Honeywell International Inc. is strengthening its presence in residual solvent markets through the spin-off of Solstice Advanced Materials. The new entity integrates Fluka® and Hydranal® brands, providing high-purity reagents for analytical and titration applications. Solstice® solvents offer up to 99% reduction in global warming potential compared to traditional hydrocarbons. Strong intellectual property portfolio with over 5,700 patents supports innovation in environmentally compliant solvents. R&D capabilities with over 300 technologists enable development of customized solutions for regulatory-driven markets. Expansion into CO2 capture solvents and clean hydrogen applications aligns with evolving industrial and environmental requirements.

United States: Regulatory Convergence Driving Ultra-Trace Compliance Infrastructure

The United States residual solvents industry is undergoing a structural realignment driven by regulatory convergence and analytical precision requirements. Effective August 1, 2025, the United States Pharmacopeia formally aligned General Chapter <467> with ICH Q3C(R9), introducing new Class 2 solvents such as cyclopentyl methyl ether and tertiary-butyl alcohol, alongside the Class 3 solvent 2-methyltetrahydrofuran. This update has compelled pharmaceutical manufacturers to reassess solvent selection strategies across active pharmaceutical ingredient synthesis and downstream purification. In parallel, updated 2025 guidance from the U.S. Food and Drug Administration has accelerated a shift toward green chemistry, encouraging up to a 60% transition toward ethanol-water and bio-based solvent systems to reduce reliance on Class 1 solvents.

Compliance enforcement is reshaping capital allocation patterns across the analytical ecosystem. Major U.S. CROs and CDMOs increased capital expenditure on Headspace GC-MS platforms by approximately 15% in 2025 to support sub-10 ppm residual solvent detection. The Center for Drug Evaluation and Research reinforced this trend through the recertification of MAPP 5015.8, strictly enforcing permitted daily exposure limits of 50 mg per day for Class 3 solvents without additional justification. Growth in biologics and advanced therapies has further expanded demand for specialized residual solvent testing, with solvent impurity control becoming critical for viral vectors and cell therapies. In response, domestic suppliers such as Avantor and Honeywell introduced spectrophotometric-grade solvent lines in 2025 to reduce analytical baseline noise and enhance reproducibility in pharmaceutical quality control.

India: Export-Led Compliance and Vertical Integration of Solvent Control

India’s residual solvents landscape is anchored in its role as the global pharmaceutical manufacturing hub. With the domestic pharmaceutical sector approaching a $60 billion valuation by late 2025, demand for pharmacopoeia-grade solvent testing and purification has intensified across formulation and API facilities. Export orientation toward regulated markets has triggered a rapid expansion of analytical infrastructure. During 2024–2025, more than 120 laboratories achieved NABL accreditation under ISO 17025 specifically for residual solvent testing, reflecting heightened scrutiny from U.S. and European regulators.

Policy support has reinforced structural changes in solvent supply chains. Under the Production Linked Incentive scheme, Indian manufacturers have invested in backward integration for isopropanol and ethyl acetate, enabling tighter control of impurity profiles from feedstock to finished API. Sustainability considerations are also influencing solvent strategies. In 2025, major extractors transitioned to supercritical CO2 extraction to eliminate hexane residues in herbal and nutraceutical exports, aligning with zero-residue expectations in the European Union. Looking ahead, Indian CDMOs are preparing for blockchain-based Certificate of Analysis tracking in 2026, strengthening data integrity and traceability for residual solvent compliance across global supply chains.

China: Automated Monitoring and Purity Cross-Over from Electronics

China’s residual solvents industry is being reshaped by regulatory tightening and technology transfer from its semiconductor sector. In 2025, the National Medical Products Administration implemented Technical Guidelines for Impurity Research aligned with ICH principles, compelling pharmaceutical manufacturers to upgrade from manual sampling to automated headspace systems. This transition has raised baseline compliance costs but significantly improved consistency in residual solvent monitoring.

An important structural advantage lies in China’s electronic-grade solvent infrastructure. Leveraging ultra-high-purity solvent production developed for semiconductor fabrication, Chinese producers have repurposed these lines for pharmaceutical use, routinely achieving 99.999% purity. Regional modernization mandates in Zhejiang and Shandong chemical parks now require online gas chromatography monitoring to track VOC emissions during solvent recovery, further integrating environmental compliance with pharmaceutical quality systems. These measures position China as a supplier capable of meeting both high-purity and high-volume residual solvent control requirements.

Germany and the European Union: Risk-Based Enforcement and Green Solvent Leadership

Across Germany and the wider European Union, residual solvent management is increasingly governed by risk-based regulatory interpretation. In November 2025, the European Medicines Agency updated its ICH Q3C(R9) guidance, emphasizing product-specific risk assessments for unavoidable Class 2 solvent presence. This shift has placed greater responsibility on manufacturers to justify solvent choices through toxicological and exposure data rather than blanket compliance.

Regulatory tightening has created operational challenges. The European Directorate for the Quality of Medicines reported that over one-third of producers faced compliance hurdles in 2025 following revised permitted daily exposure values for ethylene glycol, triggering widespread method revalidation. At the same time, Europe continues to lead in green solvent adoption, recording a 15% increase during 2024–2025 in the use of ethyl lactate and bio-ethanol for pharmaceutical manufacturing. German-based innovators such as Merck KGaA are now setting analytical performance benchmarks for 2026, targeting limits of detection as low as 0.1 ppm for high-potency drug substances.

Residual Solvents Industry: Country-Level Compliance and Technology Snapshot

Residual Solvents Market County Level Snapshot

|

Region

|

Primary Regulatory Driver

|

Structural Impact on Residual Solvents

|

|

United States

|

USP <467> and FDA green chemistry guidance

|

Expansion of ultra-trace analytics and bio-based solvents

|

|

India

|

Export compliance and PLI-driven integration

|

Rapid lab accreditation and impurity-controlled solvent supply

|

|

China

|

NMPA impurity guidelines and VOC monitoring

|

Automation and UHP solvent crossover from electronics

|

|

Germany / EU

|

EMA risk-based enforcement and EDQM revisions

|

Green solvent leadership and tighter PDE validation

|

Residual Solvents Market Report Scope

Residual Solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Solvent Class (Class 1 Solvents, Class 2 Solvents, Class 3 Solvents, Unclassified Solvents), By Analytical Methodology (Gas Chromatography, Spectroscopic Methods, Gravimetric Analysis), By End-User Industry (Pharmaceuticals & Biopharmaceuticals, Food & Beverage, Cosmetics & Personal Care, Electronics & Semiconductors)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Merck KGaA, Thermo Fisher Scientific Inc., Avantor Inc., Honeywell International Inc., BASF SE, ExxonMobil Corporation, Clariant AG, Agilent Technologies Inc., Shimadzu Corporation, Tedia Company LLC, Loba Chemie Pvt. Ltd., Asahi Kasei Corporation, High Purity Laboratory Chemicals Pvt. Ltd., Tokyo Chemical Industry Co. Ltd., Spectrum Chemical Manufacturing Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Residual Solvents Market Segmentation

By Solvent Class

- Class 1 Solvents

- Class 2 Solvents

- Class 3 Solvents

- Unclassified Solvents

By Analytical Methodology

- Gas Chromatography

- Spectroscopic Methods

- Gravimetric Analysis

By End-User Industry

- Pharmaceuticals & Biopharmaceuticals

- Food & Beverage

- Cosmetics & Personal Care

- Electronics & Semiconductors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Residual Solvents Industry

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Avantor Inc.

- Honeywell International Inc.

- BASF SE

- ExxonMobil Corporation

- Clariant AG

- Agilent Technologies Inc.

- Shimadzu Corporation

- Tedia Company LLC

- Loba Chemie Pvt. Ltd.

- Asahi Kasei Corporation

- High Purity Laboratory Chemicals Pvt. Ltd.

- Tokyo Chemical Industry Co. Ltd.

- Spectrum Chemical Manufacturing Corp.

*- List not Exhaustive