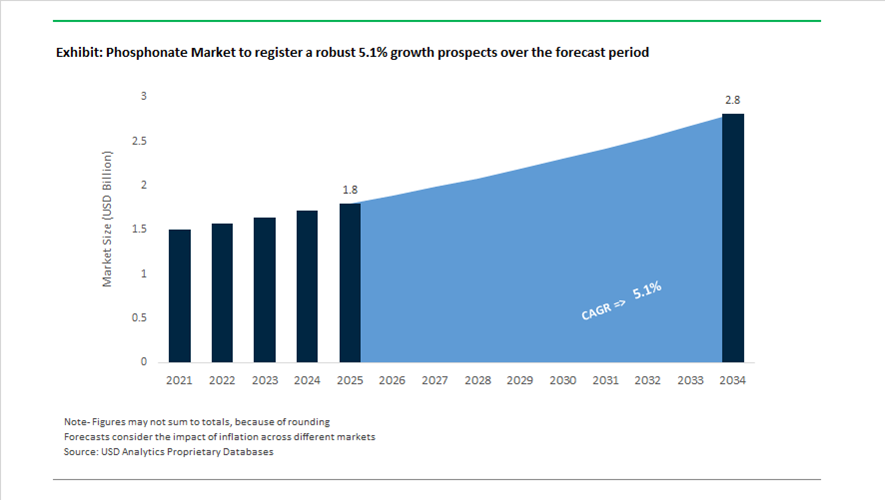

Phosphonate Market Size 2025–2034: $1.8 Billion to $2.8 Billion at 5.1% CAGR Driven by Water Treatment Chemicals, Scale Inhibitors, and Circular Phosphorus Technologies

The global phosphonate market is projected to grow from $1.8 billion in 2025 to $2.8 billion by 2034, registering a CAGR of 5.1%. The market for organophosphonates, including HEDP, ATMP, DTPMP, and related phosphonic acid derivatives, is expanding due to sustained demand in industrial water treatment, oil & gas production chemicals, detergents, pulp & paper processing, and specialty construction applications. Phosphonates remain essential as scale inhibitors, corrosion inhibitors, chelating agents, and threshold agents in high-alkaline and high-temperature environments. Increasing infrastructure investment in water reuse systems, refinery process optimization, and high-efficiency boiler treatment programs is reinforcing long-term phosphonate consumption trends.

Strategic consolidation in January 2024 reshaped global supply dynamics. PCBL Limited completed the ₹3,800 crore acquisition of Aquapharm Chemical Pvt. Ltd., integrating the AQUACID organophosphonate portfolio into its specialty chemicals platform. This transaction strengthens PCBL’s global presence in industrial water treatment chemicals and detergent phosphonates, while diversifying its revenue base beyond carbon black. In parallel, Italmatch Chemicals acquired a majority stake in Alcolina, expanding its Latin American footprint in bioethanol and sugar processing water treatment. These acquisitions signal increasing vertical integration in the phosphonate chemicals market, with producers seeking scale, regional proximity, and application-specific formulation capabilities.

Regulatory enforcement and pricing volatility influenced trade flows in 2025. In early 2025, the U.S. Department of Commerce reaffirmed anti-dumping duties on certain Chinese phosphonates, including HEDP and ATMP. This policy shift has redirected North American buyers toward Indian and domestic manufacturers to secure supply stability and mitigate tariff exposure. Throughout 2025, Italmatch USA implemented price increases ranging from 5% to 15% due to logistics inflation and solvent cost volatility linked to crude oil fluctuations. Market intelligence data in late 2025 and early 2026 indicated regional divergence, with APAC prices declining 3.34% amid Eastern China overcapacity, while U.S. prices remained stable due to balanced imports from Europe and India.

Sustainability and circular phosphorus initiatives are emerging as long-term structural drivers. Through 2024 and 2025, Italmatch advanced commercialization efforts under the EU-funded FlashPhos project, scaling a thermochemical technology to produce high-purity white phosphorus from sewage sludge. This circular economy model reduces dependence on mined phosphate rock and enhances feedstock security for phosphonate manufacturing. In July 2024, Zschimmer & Schwarz participated in the FlamenCo project to develop phosphonate-based flame retardants for rail vehicles, addressing the growing demand for non-toxic, halogen-free fire protection materials. Later in 2024, the company expanded its CUBLEN phosphonate portfolio to include chlorine-compatible, high-calcium-tolerance products tailored for industrial cleaning and high-temperature oilfield cement applications.

Advanced application research is extending phosphonate use into extreme environments. In November 2025, Kurita joined Japan’s space ecosystem collaboration for water treatment in post-ISS habitats, applying phosphonate-based scale inhibitors in closed-loop, high-recycling water systems. In December 2025, Kurita partnered with ispace to develop lunar water resource technologies, underscoring the adaptability of phosphonate chemistry under low-gravity and closed-system conditions. Supply normalization also supported downstream markets when BASF lifted Force Majeure declarations on affected aroma and care ingredients by January 15, 2026, restoring steady demand for phosphonate-based stabilizers and chelating agents used in consumer formulations.

Key Trends and High-Impact Opportunities in the Phosphonate Market

Strategic Pivot Toward High-Purity, Application-Specific Phosphonate Formulations

The phosphonate market is undergoing a structural transition away from bulk phosphonic acid sales toward high-purity, application-specific formulations designed to solve narrowly defined industrial problems. This shift reflects both margin pressure in commodity anti-scalants and rising demand from industries where process stability, impurity control, and regulatory compliance are non-negotiable.

A clear example of this premiumization trend is the expansion of phosphonate producers into formulated solutions for bio-energy and industrial process water. In January 2024, Italmatch Chemicals completed the acquisition of Alcolina, a Brazilian specialist in water treatment chemicals for bioethanol and sugar processing. This move positions phosphonates as performance-critical additives in fermentation and distillation systems, where scale control, metal passivation, and thermal stability directly affect plant uptime and yields. By targeting niche, formulation-led applications, suppliers reduce exposure to raw material price volatility while securing long-term customer contracts.

In parallel, industrial and institutional cleaning formulations are increasingly specifying electronic-grade phosphonates to protect automated, high-precision equipment. Compared to conventional commodity additives, these higher-purity grades deliver 15 to 20% greater performance stability in hard water environments, improving cleaning consistency in food processing, pharmaceuticals, and semiconductor-adjacent facilities. This reflects a broader “formulation-first” purchasing mindset, where customers prioritize lifecycle performance over unit cost.

Capital expenditure patterns reinforce this shift. Across Asia-Pacific, leading producers are upgrading manufacturing lines to support ultra-low chloride phosphonate production. These grades are essential for high-pressure boilers and closed-loop systems, where trace halides can accelerate stress corrosion cracking and significantly shorten asset lifespans. As a result, phosphonates are increasingly positioned as asset protection chemicals rather than simple scale inhibitors.

Integration of Phosphonates with Biocide Systems for Low-Impact Water Treatment

A second major trend is the repositioning of phosphonates as integral components of environmentally optimized water treatment programs. Rather than acting solely as scale inhibitors, phosphonates are now being formulated as stabilizers for oxidative biocides such as hydrogen peroxide and peracetic acid. This synergy enables operators to lower overall chemical dosages while maintaining microbial control, directly addressing tightening discharge limits across Europe and North America.

Research initiatives supported by Japan’s NEDO feasibility programs during 2024 and 2025 highlight the growing role of high-purity organophosphorus compounds in phosphorus recycling and halogen-free bleaching systems. These phosphonates stabilize peroxides in pulp, paper, and textile operations, reducing chemical decomposition and lowering the environmental footprint of traditionally water-intensive industries.

Desalination has emerged as a particularly attractive application area. In late 2024, Italmatch Chemicals and ACWA Power signed a memorandum of understanding to explore advanced phosphonate solutions for membrane stabilization in large-scale desalination plants. By improving membrane durability and reducing reliance on aggressive biocides, phosphonates support higher water recovery rates and longer maintenance intervals, which are critical for cost control in water-stressed regions.

Regulatory pressure is accelerating adoption. Updates to EU REACH and U.S. EPA frameworks in 2025 have increased compliance costs for systems reliant on heavy metals and legacy phosphates. In response, industrial cooling and water treatment operators are shifting toward synergistic phosphonate blends that enable up to 30% reductions in chlorine usage, lowering the formation of trihalomethanes and improving regulatory acceptance.

Enabling Ultra-High-Purity Semiconductor Cleaning and Etching Processes

The rapid advance toward sub-3nm semiconductor nodes and complex 3D architectures is creating a high-value opportunity for ultra-high-purity phosphonic acids. These reagents are now critical for selective etching and advanced wafer cleaning steps, where contamination control directly impacts chip yield and performance.

The semiconductor-grade phosphoric and phosphonic acid segment reached a targeted valuation of approximately $1.78 billion by late 2024, driven by demand for reagents with parts-per-billion impurity thresholds. Leading fabs in Taiwan and South Korea are increasingly specifying high-purity Amino Trimethylene Phosphonic Acid as a chelating agent in wet-cleaning formulations. This enables effective removal of metallic and particulate contaminants without damaging delicate silicon structures required for high-performance computing, artificial intelligence, and 5G applications.

Japan is emerging as a focal point for innovation in this space. In November 2024, Mitsui Chemicals announced a project aimed at refining phosphorus at the atomic and molecular level to produce ultra-high-purity organophosphorus compounds from waste streams. This initiative not only strengthens domestic supply security for semiconductor materials but also aligns with circular economy goals by converting industrial waste into strategic electronic-grade reagents.

Advanced Chelating Agents for Precision and Sustainable Agriculture

Sustainable agriculture represents a second major growth frontier for phosphonates, particularly as regulators and growers seek alternatives to traditional phosphate-heavy fertilization systems. Phosphonate-based chelates are gaining traction as high-efficiency micronutrient carriers that improve nutrient uptake while minimizing environmental runoff.

Comparative field studies conducted during 2024 and 2025 show that phosphonate chelates based on HEDP and DTPMP can enhance the bioavailability of iron and zinc by up to 15% compared with EDTA-based systems. This efficiency allows farmers to apply lower dosages, reducing soil fixation and improving nutrient use efficiency across diverse crop systems.

Regulatory alignment is reinforcing this shift. The EU Farm to Fork Strategy and new nutrient runoff controls introduced in North America in 2025 are accelerating adoption of smart fertilizer formulations that release nutrients in response to soil moisture and temperature triggers. Phosphonates play a central role in these systems by stabilizing micronutrients and controlling their release profile, helping maintain yields while reducing phosphate loads in surrounding water bodies.

Investment momentum underscores the scale of the opportunity. Global demand for high-efficiency specialty fertilizers surpassed 50 million metric tons by the end of 2024, driven by the expansion of automated fertigation and precision farming systems. For phosphonate producers, this creates a scalable, long-term market for chelating agents that serve as the functional backbone of next-generation liquid fertilizer solutions.

Phosphonate Market Share and Segmentation Insights

HEDP Leads Phosphonate Market Demand in Industrial Water Treatment and Scale Control Systems

HEDP accounted for 32.80% of the Phosphonate Market by type in 2025, reflecting its extensive use as a highly effective scale inhibitor and corrosion control agent in industrial water treatment programs. 1-Hydroxyethylidene-1,1-diphosphonic acid provides strong stability under harsh conditions including high temperatures and alkaline environments, making it suitable for cooling towers, boilers, and desalination systems. Its ability to prevent mineral deposition from calcium carbonate, calcium sulfate, and barium sulfate continues to support large-scale industrial demand. In 2025, the industry faces growing regulatory pressure to reduce phosphorus discharge, prompting chemical manufacturers to explore low-phosphorus and phosphorus-free alternatives while maintaining the cost-performance advantages that HEDP provides in most industrial treatment programs.

Scale and Corrosion Inhibition Drives Phosphonate Consumption in High-Cycle Industrial Water Systems

Scale and corrosion inhibition represented 58.60% of the Phosphonate Market by application in 2025, making it the dominant use of phosphonate chemistry across industrial infrastructure. Continuous chemical treatment is required in cooling towers, boilers, desalination plants, and oilfield operations to prevent mineral scale formation and metal corrosion that can reduce equipment efficiency and increase maintenance costs. Phosphonates remain widely used due to their strong complexation capability and long-term stability in harsh operating environments. In 2025, the shift toward high-cycle cooling tower operation to conserve water resources is increasing scale formation risks, driving demand for advanced phosphonate formulations capable of controlling mineral deposition under elevated concentration conditions.

Phosphonate Market Competitive Landscape

The global phosphonate market is defined by intensive R&D in sequestering agents, increasing demand for water treatment chemicals, and rising M&A activity aimed at building vertically integrated specialty chemical platforms. Competition is centered on green phosphonate innovation, scale-driven manufacturing, and application-specific performance across industrial water, energy, and materials sectors.

Italmatch Leads Sustainable Phosphonate Innovation with P-Free Antiscalants and Digital Dosing Technologies

Italmatch Chemicals Group is widely recognized for advanced phosphonate chemistry, anchored by its Dequest® product portfolio used in industrial water treatment and sequestering applications. The January 2024 acquisition of Alcolina expands its presence in Latin America’s bioethanol and sugar processing sectors. The Dequest® PB range introduces Carboxy Methyl Inulin (CMI)-based antiscalants designed as phosphorus-free or low-phosphorus solutions for Homecare and industrial applications under strict EU discharge regulations. Lumiclene® technology enables real-time polymer monitoring in cooling systems using fluorescence, improving dosing precision and reducing chemical consumption by up to 15%. Backward integration into phosphorus P4 and participation in the FlashPhos project support phosphorus recovery from sewage sludge. Product development focuses on sustainable phosphonate alternatives and smart water treatment chemistries.

PCBL Strengthens Global Phosphonate Leadership Through Aquapharm Acquisition and Green Chelate Development

PCBL Limited, through its acquisition of Aquapharm Chemicals in 2024, has emerged as the second-largest phosphonate producer globally outside China. The ₹3,800 crore ($450 million) acquisition transforms PCBL into a diversified specialty chemicals company with strong exposure to phosphonate-based water treatment solutions. The company operates manufacturing facilities across India, the USA, and Saudi Arabia, ensuring supply chain resilience and global distribution capability. Its portfolio of over 275 products includes key phosphonates such as HEDP and ATMP used in desalination and oilfield scale control. Aquapharm’s EBITDA margins exceeding 20% provide financial strength for R&D investments in biodegradable phosphonates and green chelating agents. Strategic focus targets FMCG, detergent, and industrial water treatment markets in Asia-Pacific.

LANXESS Expands High-Performance Phosphonate Additives for Flame Retardancy and Low-Emission Polymers

LANXESS AG leverages phosphonate chemistry in advanced material applications, particularly in flame retardants and polymer additives. The October 2025 launch of Levagard® 2100 introduces a reactive phosphonate flame retardant that chemically bonds with polymer matrices, reducing migration and lowering VOC emissions. Scopeblue-certified products incorporate at least 50% circular or bio-based raw materials, supporting carbon footprint reduction across customer value chains. The March 2026 price increase of 5% to 15% across phosphorus-based additives reflects rising raw material costs and investments in green energy infrastructure. Phosphonate-based additives are widely used in electric vehicle battery housings and high-performance insulation materials. Product strategy emphasizes halogen-free flame retardancy and sustainable polymer chemistry.

Shandong Taihe Scales Cost-Competitive Phosphonate Production with Automated Manufacturing and ZLD Technology

Shandong Taihe Water Treatment Technologies operates as a high-volume producer of phosphonate reagents with strong cost competitiveness driven by automation. The company runs more than 10 fully automated production units with an annual capacity exceeding 300,000 tonnes, supplying global distributors and municipal water treatment projects. Its portfolio includes over 300 water treatment chemicals, with advanced polymeric phosphonate formulations designed for high-pressure boiler and reverse osmosis systems. Export strategy diversification in 2025 targets Southeast Asia and the Middle East to offset trade barriers in the US and Europe. Proprietary zero-liquid-discharge (ZLD) technology supports compliance with stringent environmental regulations in industrial applications. Manufacturing scale and process efficiency enable competitive positioning in bulk phosphonate supply.

Solvay Focuses on High-Purity Phosphonates for Industrial Processing and Energy Transition Applications

Solvay S.A. remains active in phosphonate chemistry through its integration with peroxide and soda ash value chains, where phosphonates function as stabilizers and chelating agents. The company reported €4.3 billion in revenue in 2025 and is targeting €300 million in cost savings by 2026 to support investment in energy transition projects. Strategic capacity adjustments in Europe, including facilities in Spain, align production toward high-purity bicarbonates and lithium-ion battery processing chemicals. Solvay offers integrated chemical solutions combining phosphonate stabilizers with hydrogen peroxide for bleaching and disinfection applications. High-purity phosphonates are widely used in textile and pulp and paper industries to prevent metal-catalyzed degradation. Product strategy emphasizes specialty chemicals with higher margins and application-specific performance.

China – Price Rationalization Coupled With Green Manufacturing Discipline

China’s phosphonate industry in 2025 is characterized by price stabilization alongside tightening environmental governance. As of September 2025, phosphonate prices settled around USD 920 per metric ton, easing from earlier-year peaks as expanded domestic availability intensified competition within the Shandong and Jiangsu production clusters. This pricing normalization reflects a structurally well-supplied market where scale efficiencies are increasingly decisive, particularly for standard grades such as HEDP and ATMP used in water treatment and electronics cleaning.

Regulatory pressure is reshaping production economics. The 2025 Draft Environmental Code has accelerated the adoption of green chemistry practices in the Yangtze River Delta, mandating that new phosphonate facilities cut phosphorus-bearing wastewater volumes by 30% versus 2020 benchmarks. Leading producers, including Shandong Taihe Water Treatment Technologies and Changzhou Kewei Fine Chemicals, responded in 2025 by expanding high-purity phosphonate lines aimed at semiconductor wafer cleaning and electronics-grade applications. Under the national “AI + Petrochemicals” initiative, manufacturers are also deploying blockchain-enabled tracking of yellow phosphorus feedstocks to demonstrate ESG compliance for European exports. These measures align with the MIIT 2025–2026 Action Plan, which mandates 5% growth in specialty chemical value addition while offering tax incentives for phosphonate-enabled zero liquid discharge water treatment systems.

India – Cluster-Led Expansion and Agricultural Pull

India’s phosphonate market is transitioning from import reliance toward cluster-driven domestic capacity and application diversification. The NITI Aayog Chemical Industry Report 2025 identifies eight high-potential chemical clusters with integrated port connectivity, designed to accelerate exports of specialty chelation agents across the APAC region. Complementing this infrastructure push, the government proposed a new Opex subsidy scheme in July 2025 to incentivize incremental domestic production of critical phosphonates such as DTPMP, directly targeting supply concentration risks from single-source import markets.

Demand-side momentum is increasingly agriculture-led. In 2025, India recorded a 55% surge in sales of customized nutrient solutions, where phosphonates are used to stabilize micronutrients in high-alkalinity soils and improve nutrient-use efficiency. Industrial integration is also strengthening. Aquapharm Chemicals Pvt. Ltd. expanded its Pune R&D facilities in 2025 to develop next-generation biodegradable builders for the industrial and institutional cleaning segment, signaling a move toward higher-margin, formulation-driven growth.

United States – Infrastructure Demand and Water Treatment Synergies

The U.S. phosphonate industry is navigating cost pressures from trade policy while benefiting from infrastructure-led demand. In spring 2025, a new round of reciprocal tariffs on phosphate imports raised raw material costs for domestic producers, pushing U.S.-manufactured phosphonate prices upward by Q3 2025. This pricing environment is encouraging tighter feedstock sourcing strategies and selective pass-through to downstream users.

At the same time, macro demand drivers remain robust. U.S. Census Bureau updates in 2025 indicate double-digit growth in high-value construction activity, supporting phosphonate consumption as concrete retardants and performance admixtures in large-scale civil engineering projects. Environmental regulation is creating an additional demand vector. As the EPA tightens PFAS monitoring requirements into 2026, phosphonate-based antiscalants are being increasingly integrated into high-pressure reverse osmosis systems used for municipal “forever chemical” remediation, embedding phosphonates deeper into advanced water treatment architectures.

Italy – Regulatory-Driven Portfolio Upgrading Within the EU

Italy functions as a strategic phosphonate hub within Europe, anchored by globally active specialty chemical players and early regulatory adaptation. Italian producers are leveraging their strong presence in desalination and industrial cooling applications across EMEA, while repositioning portfolios in response to evolving EU chemical policy. The October 2025 updates to REACH Annex XVII accelerated the shift toward low-toxicity phosphonate formulations, particularly as replacements for traditional chelants in personal care and cosmetic applications.

Sustainability investment is reinforcing this transition. In 2025, the Bozzetto Group was highlighted as an ESG-driven specialty chemicals asset, with targeted investments in sustainable phosphonates for textile processing and water treatment. This positioning allows Italian suppliers to align with downstream customer requirements for regulatory certainty, traceability, and reduced environmental impact across EU markets.

Saudi Arabia – Desalination-Led Specialty Diversification

Saudi Arabia is leveraging its phosphate resource base to move decisively into downstream phosphonate specialties. In 2025, Ma’aden and regional partners initiated pilot projects using solar-powered electrolytic phosphorus production to establish a green phosphonate value chain aligned with the Kingdom’s large-scale seawater desalination requirements. These pilots aim to reduce the carbon intensity of antiscalants and chelation agents used in thermal and membrane desalination systems.

Industrial diversification is further supported by the expansion of Waad Al Shamal Phosphate City through 2026. New downstream units dedicated to specialty phosphonates are shifting Saudi Arabia’s export profile away from bulk fertilizers toward higher-margin technical reagents. This transition strengthens the Kingdom’s positioning as a strategic supplier to water-stressed regions while supporting broader economic diversification objectives.

Comparative Snapshot – Phosphonate Industry by Country

Phosphonate Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Primary Demand Driver

|

Structural Direction

|

|

China

|

Green compliance and scale

|

Electronics, ZLD water systems

|

Cost-efficient, regulation-led

|

|

India

|

Cluster expansion and agriculture

|

Nutrient stabilization, I&I cleaning

|

Import substitution, application-driven

|

|

United States

|

Infrastructure and remediation

|

Construction, PFAS removal

|

Demand-led, cost-sensitive

|

|

Italy

|

REACH-aligned specialization

|

Cooling, cosmetics, textiles

|

Regulation-driven upgrading

|

|

Saudi Arabia

|

Desalination and diversification

|

Water treatment

|

Resource-backed, specialty shift

|

Phosphonate Market Report Scope

Phosphonate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type (ATMP, HEDP, DTPMP, PBTCA, BHMT, Other Phosphonates), By Application (Scale & Corrosion Inhibition, Chelating & Sequestering, Bleach Stabilization, Concrete Retardation, Pharmaceutical Intermediates, Agricultural Protection), By End-Use Industry (Water Treatment, Industrial & Institutional Cleaning, Oil & Gas, Agriculture, Textile & Paper, Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Italmatch Chemicals S.p.A., Shandong Taihe Water Treatment Technologies Co. Ltd., Aquapharm Chemicals Private Limited, Zschimmer & Schwarz, Bozzetto Group, Changzhou Kewei Fine Chemicals Co. Ltd., Suez Water Technologies & Solutions, Solvay SA, Qingdao Jiahua Chemical Co. Ltd., Excel Industries Limited, Henan Pulis Chemical Co. Ltd., Lanxess AG, Lonza Group, Buckman Laboratories International Inc., Jianghai Environmental Protection Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phosphonate Market Segmentation

By Type

- ATMP

- HEDP

- DTPMP

- PBTCA

- BHMT

- Other Phosphonates

By Application

- Scale & Corrosion Inhibition

- Chelating & Sequestering

- Bleach Stabilization

- Concrete Retardation

- Pharmaceutical Intermediates

- Agricultural Protection

By End-Use Industry

- Water Treatment

- Industrial & Institutional Cleaning

- Oil & Gas

- Agriculture

- Textile & Paper

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Phosphonate Industry

- Italmatch Chemicals S.p.A.

- Shandong Taihe Water Treatment Technologies Co. Ltd.

- Aquapharm Chemicals Private Limited

- Zschimmer & Schwarz

- Bozzetto Group

- Changzhou Kewei Fine Chemicals Co. Ltd.

- Suez Water Technologies & Solutions

- Solvay SA

- Qingdao Jiahua Chemical Co. Ltd.

- Excel Industries Limited

- Henan Pulis Chemical Co. Ltd.

- Lanxess AG

- Lonza Group

- Buckman Laboratories International Inc.

- Jianghai Environmental Protection Co. Ltd.

*- List not Exhaustive