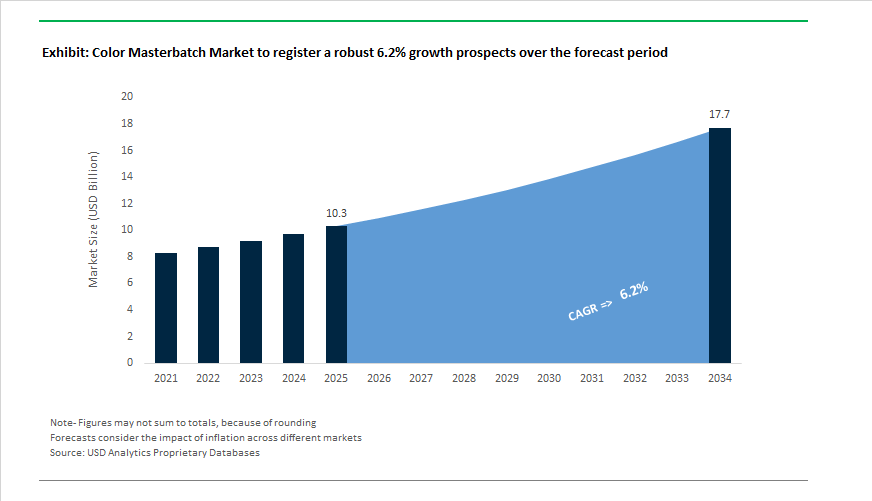

Color Masterbatch Market Outlook 2025–2034: $10.3 Billion to $17.7 Billion at 6.2% CAGR Driven by Sustainable Pigments and Functional Additives

The global Color Masterbatch Market is projected to grow from $10.3 billion in 2025 to $17.7 billion by 2034, registering a CAGR of 6.2%. Growth is being driven by expanding demand for customized polymer coloration, regulatory-driven reformulation, and the integration of functional additives into masterbatch systems for packaging, automotive, medical, electronics, and construction applications. Increasing pressure to eliminate PFAS, titanium dioxide, heavy metals, and high-carbon-intensity pigments is reshaping masterbatch design. At the same time, circular feedstock integration and recycled polymer compatibility are emerging as core differentiators for global compounders and pigment suppliers.

Strategic consolidation reshaped the pigment supply base in March 2025, when Sudarshan Chemical Industries Limited completed the acquisition of Germany-based Heubach Group. The transaction created the world’s second-largest pigment and colorant producer, expanding manufacturing capabilities across 19 international sites and strengthening the global supply of high-performance organic and inorganic pigments for color masterbatches. Earlier, in May 2024, Chroma Color Corporation acquired Approved Color LLC to expand its custom color concentrate portfolio and increase production capacity for consumer and industrial markets. These moves signal intensified competition and vertical integration across pigment sourcing and masterbatch compounding operations.

Sustainability-driven innovation accelerated across 2024–2026. In May 2024, Cabot Corporation introduced REPLASBLAK® circular black masterbatches featuring ISCC PLUS certified sustainable materials through EVOLVE® Sustainable Solutions, enabling automotive and packaging manufacturers to reduce product carbon footprint without sacrificing jetness or dispersion performance. Ampacet launched its HyperLustre TiO2-free PET collection during 2024–2025, delivering pearlescent effects while improving recyclability in high-speed recovery systems. In February 2026, Ampacet introduced Natura Jet at Plastindia 2026, utilizing naturally derived carbon instead of conventional carbon black for deep black injection-molded parts. Avient expanded its Hiformer™ Non-PFAS liquid masterbatch portfolio into Asia in January 2026, addressing regulatory pressure on fluorinated process aids in polyolefin film production. These launches underscore a structural transition toward low-toxicity, recyclable, and renewable-content color masterbatch formulations.

Functional performance and advanced materials integration further diversified the market landscape. In January 2025, Perpetuus Advanced Materials launched nano-engineered graphene masterbatches initially targeting tire manufacturing, with expansion planned into elastomers and industrial polymer applications during 2025. Broadway introduced GrapheneXcel masterbatches in September 2024, enhancing mechanical and thermal properties while enabling material downgauging in plastic components. Ampacet released ProVital™+ LaserMark in late 2024, compliant with ISO 10993 for medical device laser marking. In February 2026, Avient introduced Nymax™ REC recycled nylon masterbatches for fire-resistant building materials and GlideTech™ non-PFAS formulations for medical catheters, addressing lubricity and regulatory compliance requirements. LyondellBasell confirmed in January 2026 increased investment in its MoReTec-2 chemical recycling facility in Houston, securing high-purity circular feedstock supply for virgin-quality sustainable masterbatches. These developments position the color masterbatch market for steady mid-single-digit expansion through 2034, supported by circular raw materials integration, PFAS elimination, graphene-enhanced functionality, and healthcare-grade traceability requirements.

Color Masterbatch Market Trends and Drivers

Rapid Market Shift Toward PCR-Compatible and NIR-Detectable Masterbatches to Unlock Circular Economy Compliance

The Color Masterbatch Market is undergoing a structural pivot aligned with global sustainability mandates, extended producer responsibility (EPR) laws, and carbon-neutral packaging goals. A key material challenge—the inability of traditional carbon-black plastics to be identified by NIR sorting systems—is now being solved through innovation.

In October 2025, Ampacet introduced NIR-detectable black masterbatch engineered specifically for the U.S. food packaging stream. This innovation resolves a historically critical recycling barrier, where ~55% of black plastic packaging fell into residue streams due to optical sensor non-recognition. NIR-detectable masterbatch directly improves sorted yield, plastic recyclate availability, and brand-level circularity metrics, making it a procurement priority for FMCG and food-service packaging.

Meanwhile, brands requiring 100% recycled packaging claims are driving demand for pigment systems based on recycled carrier resins. In November 2025, Avient Corporation launched the PCR Color line, enabling colorization of PCR plastics without virgin resin dilution. This is strategically important in geographies like India, where 2025 EPR compliance is enforcing 30–60% PCR content in rigid plastics by 2028.

High-Temperature, Weatherable Masterbatches Enabling E-Mobility and 5G Infrastructure

Beyond packaging, masterbatches are expanding into mission-critical engineering materials—particularly where thermal stability, UV resistance, and color fastness are linked directly to product performance.

In September 2025, global demand modeling identified the EV automotive sector—especially EV interiors and high-voltage enclosures—as one of the fastest-growing end-users of specialty color masterbatch. New formulations like Dainichiseika’s Cool Black masterbatches incorporate infrared reflectance, helping reduce cabin heat load and extend EV driving range by up to ~20% in harsh climates, aligning directly with OEM electrification efficiency KPIs.

Simultaneously, 5G exterior housings and solar structures require masterbatches compatible with polyphthalamide (PPA) and other engineering resins. These next-generation color concentrates maintain UV stability and mechanical integrity under prolonged outdoor exposure, commanding premium pricing in the US$2,800–$4,200/ton range due to the inclusion of UV stabilizers, anti-weathering packages, and flame-retardant additives.

Invisible Fluorescent Markers for AI-Sorting, Traceability, and Anti-Counterfeit Authentication

A high-margin opportunity is emerging in intelligent masterbatches, where colorants are engineered to be machine-visible but human-invisible—transforming the role of masterbatch from aesthetics to data-carrier and traceability enabler.

The PRISM smart-sorting initiative (2025 trials) demonstrated that fluorescent-encoded masterbatch enables 95–99% purity recovery at scale, processing up to 4.4 tonnes/hr—a breakthrough that allows food-grade polymers to be recovered separately from non-food polymers. This provides recycled feedstock cost savings and packaging reusability—critical for FMCG companies facing rising PCR-pricing volatility.

Additionally, chemical taggant-embedded masterbatches are rapidly gaining adoption in pharmaceuticals and premium electronics as a digital polymer fingerprint. Adoption is accelerating particularly in India, where July 2025 mandates require QR-coded traceability on all plastic packaging, creating a parallel market for polymer-level authentication solutions embedded directly within the resin.

Masterbatches for Additive Manufacturing (3D Printing) – Tailored for Engineering-Grade Filaments

The industrialization of 3D printing (FDM, SLS) is unlocking a new demand curve where precise pigment dispersion, high-temperature resistance, and bio-compatibility are differentiators.

In November 2025, demand for masterbatches for carbon-fiber nylon and ASA filaments surged as aerospace and automotive enterprises scaled additive prototypes requiring >150°C thermal stability. Poor pigment dispersion has historically clogged printer nozzles—putting filament-grade masterbatch at the center of printer-line productivity metrics.

Meanwhile, bio-based 3D printing materials are now a commercial category. In December 2025, DIC Corporation commercialized biomass-based pigment masterbatch optimized for PLA and PHA filaments, contributing to the projected US$3.5-billion global eco-3D materials market in 2025. These innovations support fully renewable filament supply chains, helping manufacturers reach net-zero materials goals without compromising filament coloration.

Competitive Landscape of the Color Masterbatch Market

The Color Masterbatch Market is led by vertically integrated polymer majors and specialty color innovators advancing PFAS-free processing aids, PCR-compatible pigments, and digitally enabled color development. Competitive differentiation centers on sustainable black masterbatches, NIR-sortable formulations, functional hybrid concentrates, and rapid custom color matching for healthcare, EV components, packaging, and infrastructure plastics. Market leaders are accelerating localized production in high-growth regions, embedding real-time color management on factory floors, and expanding bio-based and circular portfolios. Strategic priorities increasingly include medical-grade compliance, recyclable aesthetics, and fast-turn prototyping to shorten product development cycles.

Avient accelerates sustainable masterbatch innovation with digital color creation platforms

Avient has emerged as the industry’s sustainability powerhouse following its rebrand from PolyOne and acquisition of Clariant’s masterbatch business. Its portfolio spans OnColor™ solid and liquid colorants, Mevopur™ medical-grade solutions, and Artisan™ pre-colored thermoplastics for paint replacement. In early 2026, Avient launched GlideTech™, a non-PFAS processing aid for medical catheters and flexible films, eliminating legacy “forever chemical” additives. At Plastindia 2026, Avient showcased its local-to-global strategy targeting India with EV and 5G infrastructure materials. Its Digital Color Choice initiative, powered by ColorMatrix™ Select, enables real-time liquid color creation and rapid prototyping, compressing development cycles from weeks to days.

Ampacet leads aesthetic differentiation with TiO2-free effects and in-line color control

Ampacet dominates aesthetic masterbatch solutions for consumer packaging and retail, known for HyperLustre™ and Artemis™ collections delivering metallic and pearlescent effects without titanium dioxide. In 2025 to 2026, Ampacet introduced Natura Jet, a natural-carbon-based black masterbatch achieving deep piano-black finishes while improving recyclability versus petroleum-derived blacks. Its LIAD Smart in-line color management integrates directly with injection molding equipment to deliver real-time correction and up to 50% cost savings. Ampacet also commands the Healthcare ProVital™ segment, supplying ISO 10993-compliant masterbatches for pharmaceutical primary packaging and medical devices, reinforcing its leadership in high-impact, regulated applications.

LyondellBasell integrates polymer science with PCR masterbatches and NIR-sortable blacks

LyondellBasell leverages its scale as a leading polymer producer to deliver vertically integrated Polybatch® masterbatches alongside its Circulen Recover, Revive, and Renew sustainable resin portfolio. A key innovation is CirculenRecover MB, a masterbatch using 100% post-consumer recycled carrier resin for blow-molded bottles, maximizing recycled content in finished packaging. LYB also leads in NIR-sortable black technology, enabling near-infrared detection of black plastics in recycling streams, removing a long-standing barrier to circularity. At Plastindia 2026, the company announced a Full Portfolio Approach for AfMEI, combining high-performance virgin polymers with localized masterbatch production.

Cabot advances circular carbon black with REPLASBLAK for low-footprint deep blacks

Cabot sets the global benchmark in carbon black masterbatches, controlling quality from raw carbon feedstock to finished pellets. In February 2026, Cabot completed the acquisition of Mexico Carbon Manufacturing, strengthening supply chain resilience across the Americas. Its REPLASBLAK™ series introduces circular carbon black derived from end-of-life tires, allowing OEMs to achieve deep black aesthetics with significantly lower carbon footprints. Cabot remains the market leader in conductive masterbatches for electronics shielding, automotive applications, and high-voltage cable jacketing. With a market capitalization near USD 3.93 billion, Cabot’s 2026 strategy prioritizes high-purity performance chemicals over commodity grades.

Tosaf delivers rapid custom colors and hybrid functional masterbatches worldwide

Tosaf is a global specialist recognized for doorstep service and high-speed custom color matching across niche and industrial plastics. Its functional masterbatches combine color with UV stabilization, antimicrobial performance, and anti-fog or anti-static properties. Operating 17 production plants and advanced color labs, Tosaf typically delivers custom matches within 2 to 5 days, among the fastest turnaround times in the industry. In 2026, Tosaf expanded its renewables portfolio with biodegradable and compostable masterbatches meeting stringent OK Compost certifications. Guided by its Local Care, Global Standards strategy, Tosaf tailors formulations to regional polymers and environmental regulations through its Tosaf Color Service.

Color Masterbatch Market Share and Segmentation Insights

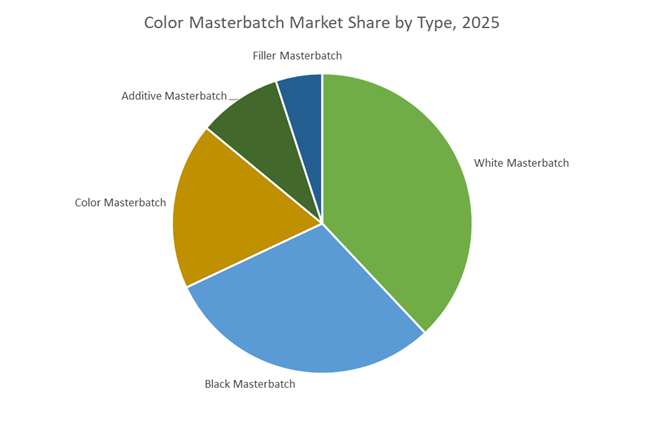

Type-Based Segmentation: White Masterbatch Leads Volume While Additive Grades Drive Functional Growth

White masterbatch commands 38% market share in 2025, anchored by titanium dioxide formulations that deliver opacity, brightness, and UV protection across films, rigid packaging, and molded plastic products. It is widely used as a base layer for printing and branding, making it indispensable in high-volume packaging applications. Black masterbatch follows as the second-largest segment, supported by carbon black’s UV-blocking performance and cost efficiency in automotive parts, construction pipes, cables, and agricultural films, alongside rising demand for matte black finishes in consumer electronics. Color masterbatch represents a higher-value segment, enabling brand-specific aesthetics in consumer goods, toys, and packaging where visual differentiation drives sales. Additive masterbatch is the fastest-growing category, incorporating UV stabilizers, anti-blocking, anti-static, flame-retardant, and antimicrobial functions to meet demand for high-performance plastics. Filler masterbatch, primarily calcium carbonate-based, supports cost reduction and dimensional stability in non-critical applications such as bags and molded commodities.

Application Landscape: Packaging Dominates as Construction and Automotive Demand Performance Grades

Packaging accounts for 52% of global color masterbatch consumption, spanning rigid bottles and caps to flexible films and pouches that rely on white for opacity, black for UV protection, and color masterbatch for brand identity. Building and construction represents the second-largest application, utilizing masterbatches in PVC pipes, window profiles, decking, and roofing membranes, where black provides weather resistance and white aids heat reflectance. Consumer goods depend heavily on color masterbatch for aesthetic appeal and consistent shade matching across toys, electronics housings, and furniture. Automotive and transportation applications require thermally stable, UV-resistant masterbatches for interior and exterior components, with additive grades delivering impact resistance and durability. Agriculture relies on white and black masterbatches in greenhouse and mulch films to regulate light and soil temperature. Textile and fibers, while smaller, are growing as dope-dyed synthetic fibers gain traction for water and energy savings.

United States Color Masterbatch Market: Medical-Grade Innovation, Paint-Replacement Thermoplastics, and Smart Packaging Leadership

The United States Color Masterbatch Market is increasingly defined by high-value specialty masterbatches, medical-grade formulations, and advanced pre-colored thermoplastics designed to replace conventional automotive painting processes. In February 2026, Avient Corporation projected a recovery in adjusted EPS to between $2.93 and $3.17 for 2026, driven by prioritizing high-profit portfolios such as automotive paint-replacement color masterbatches. This strategic pivot reflects a broader U.S. industry focus on margin expansion through functional color concentrates and engineered thermoplastic compounds rather than commodity pigment volumes.

In early 2026, Ampacet Corporation introduced its ProVital+ medical-grade masterbatch range at MD&M West, compliant with ISO 10993 and European Pharmacopoeia standards for pharmaceutical primary packaging. Sustainability and regulatory alignment are accelerating innovation, with growing adoption of PTFE-free and non-halogenated flame-retardant masterbatches amid state-level PFAS scrutiny. Integration of Industry 4.0 technologies, including LIAD Smart gravimetric feeders, demonstrated up to 50% cost savings through precision dosing and real-time quality monitoring. Additionally, NFC-enabled smart packaging masterbatches are gaining traction in the nutraceutical sector, while laser-marking masterbatches for high-contrast coding on medical devices and transparent or dark polymer substrates represent a rapidly expanding application segment within the U.S. specialty color masterbatch market.

China Color Masterbatch Market: 15th Five-Year Plan Modernization and High-Dispersion Black Masterbatch Breakthroughs

China’s Color Masterbatch Market is transitioning from volume-driven production to quality-first, high-efficiency manufacturing under the formalization of the 15th Five-Year Plan in March 2026. Structural upgrades and digitalization of chemical manufacturing are central to this strategy. In September 2025, the Ministry of Industry and Information Technology of China launched a work plan targeting over 5% annual growth in chemical industry value-added output, specifically incentivizing specialty colorants for high-end polyolefin applications.

A self-sufficiency mandate requiring up to 50% domestic equipment sourcing for certain expansions is stimulating development of advanced extrusion and masterbatch compounding lines. Infrastructure growth at Huizhou Dayawan Petrochemical Industrial Park is expanding capacity for high-purity polyethylene and polypropylene carrier resins, critical for high-dispersion color masterbatch production. Domestic manufacturers have achieved breakthroughs in high-jetness black masterbatches using naturally derived carbon sources to meet Green Transformation targets. Under the Internal Circulation strategy, China is redirecting export reliance toward its vast domestic consumer electronics and automotive markets, both major consumers of specialty color masterbatches with enhanced UV stability, conductivity, and aesthetic performance.

Germany Color Masterbatch Market: Circular Economy Compliance, rPCF Portfolios, and PPWR-Driven Food-Grade Reformulation

Germany stands at the forefront of the Color Masterbatch Market in Europe, driven by stringent circular economy mandates and the implementation of the EU Packaging and Packaging Waste Regulation. European Commission Regulation EU 2025/351, effective March 2025, established new benchmarks for recycled plastics in food-contact materials, compelling redesign of food-grade color masterbatches to ensure compliance with recyclability and migration standards.

At K 2025, BASF introduced its rPCF portfolio, offering color masterbatches produced using renewable feedstocks under the Biomass Balance approach to reduce product carbon footprint. German specialists such as Lifocolor have developed holographic effect masterbatches and TiO2-free colorants that maintain premium aesthetics while ensuring recyclability. Adoption of the PACIFIC app for standardized product carbon footprint data exchange is enhancing supply chain transparency among converters and brand owners. Investments in chemical recycling facilities, including MoReTec-1, are supplying circular polymers that serve as next-generation carrier resins for sustainable masterbatch solutions. German companies are also shaping global design trends with biodegradable polymer-compatible shades such as Pink Blush and Autumn Gold, reinforcing their leadership in eco-conscious color innovation.

India Color Masterbatch Market: PLI-Fueled Electronics Growth and Export-Driven Specialty Compounding

India’s Color Masterbatch Market is gaining momentum as government-backed manufacturing incentives and FDI inflows accelerate domestic demand for specialty polymer colorants. The Production Linked Incentive Scheme received a substantial budget increase for 2025 to 2026, targeting global leadership in electronics and automotive manufacturing, both key end-use sectors for color masterbatches. By late 2025, realized investments under PLI surpassed ₹2 lakh crore, equivalent to over $24 billion, stimulating demand for high-performance color concentrates in white goods, telecom equipment, and automotive components.

Plastindia 2026 served as a strategic showcase for global players such as Avient Corporation and Ampacet Corporation, highlighting Made in India metallic effect masterbatches and artisan pre-colored thermoplastics. Infrastructure expansion through Bulk Drug Parks and electronics clusters is generating a 12 to 15% increase in demand for high-purity additive masterbatches for specialized packaging applications. The Department of Commerce’s flagship initiative for FY 2025 to 2031, with a ₹25,060 crore outlay, reinforces export ambitions in chemical intermediates and polymer additives. Indian manufacturers are adopting gravimetric vibratory feeders for micro-additive precision, targeting global medical molding and high-accuracy polymer processing markets, positioning India as a cost-competitive yet technologically advancing masterbatch export hub.

Thailand Color Masterbatch Market: Record FDI, Recycled Polypropylene Investments, and High-Tech Supply Chain Relocation

Thailand’s Color Masterbatch Market is benefiting from unprecedented foreign direct investment and supply chain diversification. In 2025, investment pledges reached a record 1.88 trillion baht, approximately $60 billion, representing a 67% year-over-year increase, with significant allocation to the petrochemicals and chemicals sector. The Thailand Board of Investment approved 267 petrochemical and chemical projects in 2025, including initiatives focused on recycled polypropylene and specialty polymer preforms.

Geopolitical supply chain shifts have positioned Thailand as a preferred destination for advanced electronics and automotive component manufacturing, sectors requiring sophisticated color-matching masterbatch services with high thermal stability and UV resistance. Expansion of digital infrastructure and AI capabilities is generating new demand for high-performance masterbatches in 5G equipment and fiber optic cable jacketing. Following the World Economic Forum 2026, over $16 billion in new and planned investments were confirmed for advanced manufacturing and sustainable plastic solutions. Growth in specialty food additives and ingredients packaging is further driving demand for high-barrier, shelf-stable color masterbatch formulations, solidifying Thailand’s role as a strategic Southeast Asian hub for high-tech and sustainable color masterbatch production.

Color Masterbatch Market Report Scope

Color Masterbatch Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.3 Billion

|

|

Market Size (2034)

|

$17.7 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Type (Color Masterbatch, White Masterbatch, Black Masterbatch, Additive Masterbatch, Filler Masterbatch), By Carrier Polymer (Polypropylene, Polyethylene, Polyvinyl Chloride, Polyethylene Terephthalate, Engineering Plastics, Bio-based Polymers), By Application (Packaging, Automotive and Transportation, Building and Construction, Consumer Goods, Agriculture, Textile and Fibers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avient Corporation, Ampacet Corporation, LyondellBasell Industries N.V., Cabot Corporation, BASF SE, Clariant AG, Plastiblends India Limited, Tosaf Compounds Ltd., Americhem Inc., A. Schulman LLC, Delta Tecnic S.A., Gabriel-Chemie GmbH, Hubron International Limited, Penn Color Inc., Plastika Kritis S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Color Masterbatch Market Segmentation

By Type

- Color Masterbatch

- White Masterbatch

- Black Masterbatch

- Additive Masterbatch

- Filler Masterbatch

By Carrier Polymer

- Polypropylene

- Polyethylene

- Polyvinyl Chloride

- Polyethylene Terephthalate

- Engineering Plastics

- Bio-based Polymers

By Application

- Packaging

- Automotive and Transportation

- Building and Construction

- Consumer Goods

- Agriculture

- Textile and Fibers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Color Masterbatch Industry

- Avient Corporation

- Ampacet Corporation

- LyondellBasell Industries N.V.

- Cabot Corporation

- BASF SE

- Clariant AG

- Plastiblends India Limited

- Tosaf Compounds Ltd.

- Americhem Inc.

- Schulman LLC

- Delta Tecnic S.A.

- Gabriel-Chemie GmbH

- Hubron International Limited

- Penn Color Inc.

- Plastika Kritis S.A.

*- List not Exhaustive