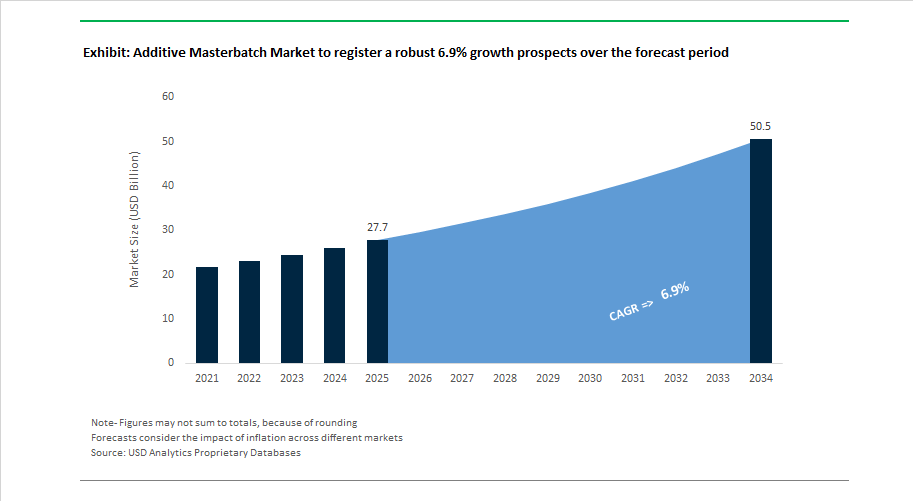

Market Overview: Additive Masterbatch Market Expansion to $50.5 Billion by 2034 Driven by Circular Plastics, High-Performance Additives, and Regulatory-Led Reformulation

The global additive masterbatch market is forecast to grow from $27.7 billion in 2025 to $50.5 billion by 2034, registering a 6.9% CAGR, supported by accelerating demand for functional polymer additives in packaging, agriculture films, automotive plastics, healthcare polymers, and specialty PET applications. Additive masterbatches are increasingly engineered for UV stabilization, oxygen scavenging, antimicrobial performance, light diffusion, flame retardancy, and recyclability enhancement, reflecting a decisive shift from commodity coloration toward performance-driven formulations. Market growth is strongly aligned with circular economy mandates, PFAS phase-outs, downgauging strategies, and higher adoption of recycled polymers (rPET, rPE), which require compatibilizers, stabilizers, and processing aids to maintain mechanical integrity and optical clarity. The industry landscape is therefore evolving toward technology-intensive specialty masterbatches designed to solve recyclability, durability, and regulatory compliance challenges across polymer value chains.

Innovation momentum accelerated in May 2024, when Cabot Corporation launched REPLASBLAK universal circular black masterbatches with ISCC PLUS certified content derived from mechanically recycled polymers, addressing sustainability requirements in automotive and packaging applications. Performance enhancement through advanced nanomaterials gained traction in January 2025, as Gerdau Graphene expanded global distribution of Poly-G™ graphene-enhanced PE masterbatch, enabling up to 50% strength improvements and material downgauging. Healthcare-focused functionality emerged in January 2025 with Ampacet introducing ProVital+ GermsClean antimicrobial masterbatch for medical-grade plastics. Specialty additives for recyclability advanced further in July 2025, when Avient Corporation launched ColorMatrix™ Amosorb™ Oxyloop-1, an oxygen scavenger designed to protect contents while enabling high-rPET PET packaging without haze formation. Circular processing solutions strengthened in late 2025 as Ampacet rolled out ReVive™ 311 compatibilizer masterbatch for recycling multi-layer plastic scrap back into high-quality PE film.

Strategic consolidation and regional specialization are reshaping competitive structures. In May 2025, Delta Tecnic acquired Impact Formulators Group (IFG), enhancing capabilities in UV stabilizers and flame-retardant additives, followed by exclusive negotiations in November 2025 to acquire Polytechs, expanding its European specialty additives footprint. Geographic expansion intensified in August 2025, when Sukano AG partnered with PlastiColors to establish PET additive production in Africa for UV and light-shielding masterbatches. Regulatory-driven reformulation accelerated through 2025–2026 as the impending EU PFAS ban pushed manufacturers toward acrylic- and silicone-based processing aids. This shift is reflected in product pipelines showcased at Plastindia in February 2026, where Ampacet presented application-driven masterbatches including anti-virus, anti-static, and greenhouse film stabilizers. Production optimization for medical and pharma packaging advanced in January 2026 with Americhem expanding clean-room additive manufacturing. Recycling infrastructure alignment further intensified in early 2026 as Cabot and Ampacet reported record demand for NIR-detectable carbon-free black masterbatches, enabling automated sorting of black plastics—an essential step in closing polymer circularity gaps.

Strategic Industry Trends and High-Value Opportunities Shaping the Additive Masterbatch Market

Market Trend: Formula Redesign to Reduce Titanium Dioxide Dependency and Improve Carbon Efficiency

One of the most structural shifts in the additive masterbatch market is the transition away from Titanium Dioxide (TiO₂), driven by price volatility, EU anti-dumping measures on Chinese TiO₂ under Regulation (EU) 2025/4, and the desire to lower embodied carbon in plastics. This is no longer simply a cost-avoidance trend; it reflects a broader reframing of masterbatch as a carbon-engineered component in manufacturing.

Chemours’ Ti-Pure TS-1510 pigment release in 2025 is a pivotal commercial signal. The grade allows up to 6% lower net carbon footprint and 30% faster compounding throughput due to optimized bulk density. This design also enables 50% lower warehouse space and logistics load, which is increasingly relevant as resin and pigment freight rates fluctuate. Parallel innovation is emerging through bio-based opacity systems, such as Kaneka’s Green Planet polymers showcased at Expo Osaka 2025. These help converters maintain surface brightness and opacity while materially reducing TiO₂ loading, a transition that is expected to reshape white masterbatch cost structures globally.

Market Trend: Masterbatch Producers Becoming Direct Automotive OEM Development Partners

A powerful new paradigm is reshaping the automotive materials supply chain. Additive masterbatch producers are moving upstream into OEM-led design collaboration, bypassing Tier 1 and Tier 2 intermediaries to co-engineer components aligned with fuel economy and EV performance targets.

Clariant’s recognition as a Schneider Electric Outstanding Supplier demonstrates this industry realignment. By delivering halogen-free flame retardants such as Exolit OP directly into EV thermal system architectures, suppliers are repositioning themselves as strategic innovation partners, not commodity vendors. Weight-reduction mandates are accelerating adoption of foaming and lightweighting agents like Hydrocerol, enabling up to 20% part-weight reduction in molded vehicle interiors, which supports compliance with U.S. CAFE’s 54.5 mpg fleet-wide mandate.

The NORMA Group’s €30 million contract for 1.4 million lightweight EV thermal tubes per year signals that thermoplastic solutions enhanced with specialized additive masterbatches are becoming mission-critical for heat-resistant, chemically stable materials at reduced wall thickness. As OEMs continue consolidation and platform sharing, additive providers that offer co-development and long-duration supply guarantees will gain competitive advantage.

Market Opportunity: Masterbatch as an Enabler for Recycled-Content Compliance in Packaging and Circular Plastics

The most immediate and scalable expansion avenue for additive masterbatch demand comes from circular economy legislation, particularly the EU Packaging and Packaging Waste Regulation (PPWR) taking effect February 11, 2025. The regulation mandates higher recycled-content usage and introduces fines for packaging that fails to meet 2030 recyclability standards.

Functional masterbatches such as BASF’s IrgaCycle XT 034 are proving commercially relevant by stabilizing degraded PCR, even enabling reuse of bumper-scrap polyolefin that contains inks, paints, and adhesive residues. In parallel, Avient’s Amosorb oxygen scavenger technology gives converters the ability to produce 100% rPET food-grade packaging with virgin-equivalent shelf life, which is now a compliance enabler rather than a premium feature.

A major shift is also unfolding in masterbatch design philosophy: additive packages now must avoid interference with NIR sorting systems to qualify for “Designed for Recycling” status. This creates a lucrative pathway for producers that can supply monomaterial-compatible additive systems optimized for PP, PE, and PET recycling plants at scale.

Market Opportunity: High-Performance Additive Packages for Battery Housing and Component Plastics

The electrification of mobility and the rise of giga-factory construction is opening a premium high-margin segment in the additive masterbatch market: plastics engineered for thermal stability, insulation, and flame retardance in next-generation lithium-ion battery designs.

At Chinaplas 2025, Avient presented Colorant Chromatics formulations for PEEK and polysulfone, enabling components that can survive 150°C sterilization and 1,000 autoclave cycles, attributes especially valued in industrial-grade or long-cycle EV battery systems. Fraunhofer IWU’s evolving cell-housing concepts using hybrid materials like phase-change polymers and aluminum-foam blends require additive packages that preserve UL 94 V-0 compliance while maintaining polymer-metal bonding integrity.

Additive innovation is also reaching the production floor. Technologies like Evonik’s TEGO Surten E improve conductive additive dispersion, enabling battery manufacturers to lower cost-per-kWh via improved electrode uniformity and faster cell production. This positions masterbatch formulations to become an embedded performance enabler in the EV supply chain rather than simply a plastics additive.

Additive Masterbatch Market Share and Segmentation Insights

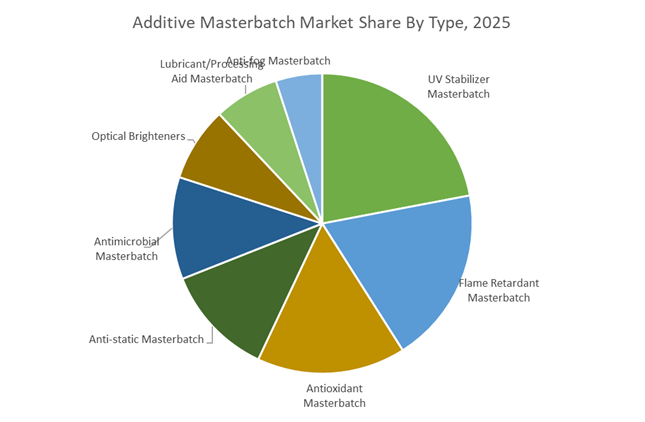

Market Share by Type: UV Stabilizer Masterbatch Leads as Flame Retardants Gain Momentum

UV stabilizer masterbatch holds the largest share of the additive masterbatch market at approximately 22% in 2025, reflecting explosive growth in outdoor plastic applications including agricultural films, outdoor furniture, and automotive exterior components, where durability standards make UV protection essential. Flame retardant masterbatch ranks second and is accelerating, supported by rising demand from EV battery components, data center cabling, and interior construction materials, with manufacturers increasingly adopting halogen-free and mineral-based flame retardant systems. Antioxidant and anti-static masterbatches maintain steady uptake across automotive and electronics packaging, while antimicrobial masterbatch recorded a structural step-change post-pandemic, remaining elevated due to hygiene-driven design in public transport, HVAC systems, and food-contact materials. Optical brighteners and lubricant/processing aid masterbatches support recycled plastics aesthetics and processing efficiency. Anti-fog masterbatch remains the smallest segment, largely confined to food packaging films and greenhouse covers, although EU food waste regulations are creating moderate incremental demand.

Market Share by End-Use Industry: Packaging Dominates While Electronics Delivers Fastest Growth

Packaging commands a dominant 41% share of global additive masterbatch consumption in 2025, driven by UV stabilizers in beverage bottles, anti-static additives for electronic component packaging, and optical brighteners that restore “virgin-like” appearance in recycled-content materials. Automotive represents the second-largest end-use, as lightweight polymer substitution for fuel efficiency and EV range expands component volumes, with under-hood applications requiring high-load antioxidant masterbatches for thermal stability. Building & construction maintains consistent demand for flame-retardant and UV-resistant plastics in profiles and panels. Healthcare/medical remains smaller than anticipated due to stringent regulatory approvals for Class II and III devices, concentrating growth in non-implantable products such as tubing and housings. Electrical & electronics exhibits the highest growth rate, as component miniaturization increases heat density, boosting flame retardant usage, while 5G infrastructure drives anti-static demand. Agriculture stays stable, anchored by UV and anti-fog masterbatches for greenhouse films.

Additive Masterbatch Market Competitive Landscape: Sustainability-Driven Innovation and Circular Polymer Integration

The Additive Masterbatch Market is evolving through regulatory-driven reformulation, advanced dosing technologies, and circular polymer integration. Leading producers are investing in PFAS-free processing aids, ISCC PLUS-certified recycled carriers, NIR-sortable colorants, and halogen-free flame retardants to align with global sustainability standards such as EU PPWR. Growth is concentrated in automotive lightweighting, food-grade rPET packaging, agricultural films, and EV battery components. Vertical integration with base resins, AI-enabled quality control, and regional production expansion are redefining competitive dynamics across Europe, North America, and Asia-Pacific.

Avient Corporation embeds sustainability into advanced additive masterbatch innovation

Avient Corporation positions sustainability at the core of its additive masterbatch strategy, focusing on enhancing post-consumer recycled resin performance. In July 2025, the company launched oxygen scavenger additives designed to maintain clarity and food-contact compliance in 100% rPET packaging. Avient doubled European additive capacity with a new Brembate, Italy facility to accelerate innovation for automotive and healthcare sectors. Its portfolio includes Smartbatch™ multifunctional solutions, Cesa™ flame retardants, and OnColor™ NIR-sortable black colorants that enable recycling of traditionally undetectable plastics. This integrated approach strengthens its leadership in sustainable packaging and high-performance polymer modification.

Ampacet Corporation advances precision additive dosing with Industry 4.0 integration

Ampacet Corporation is known for technical agility and Industry 4.0-driven additive dosing solutions. At Plastindia 2026, the company highlighted LIAD Smart integration for real-time quality control and precision dosing in masterbatch manufacturing. Its ProVital+ medical-grade range complies with ISO 10993 standards for pharmaceutical packaging and medical devices. Ampacet also introduced Natura Jet, a natural-source black masterbatch delivering deep aesthetics without conventional carbon black. The company maintains strong vertical integration in agricultural films, supplying anti-virus and light-diffusion additives that extend greenhouse cover life and irrigation durability across global agribusiness markets.

Clariant AG pioneers PFAS-free processing aids and halogen-free flame retardants

Clariant AG leads green chemistry innovation with its AddWorks® PPA line, launched in June 2025 as a PFAS-free polymer processing aid alternative for polyolefin extrusion. The company formed a strategic joint venture with FUHUA to produce advanced halogen-free flame retardants targeting China’s EV and construction sectors. Clariant maintains integrated production of Exolit® flame retardants and Licocene® performance waxes across Europe and Asia. Strategically aligned with EU Packaging and Packaging Waste Regulation compliance, Clariant is transitioning toward fully recyclable and non-toxic additive formulations, strengthening its regulatory-ready product portfolio.

LyondellBasell Industries integrates circular resins with high-performance additive systems

LyondellBasell Industries leverages its global resin footprint to dominate high-volume additive masterbatch markets. The integration of KARO 5.0 technology at its Akron facility accelerated R&D and testing for oriented film masterbatches during 2024–2025. The company’s Circulen resins are pre-formulated with internal additive packages, offering turnkey sustainable manufacturing solutions. With strategic divestments in Europe to strengthen Circular and Low Carbon Solutions, LYB is targeting automotive lightweighting and EV thermal endurance applications. Its scale integration across refining, chemicals, and polymers ensures cost efficiency and formulation consistency.

Cabot Corporation redefines carbon black masterbatches with circular and graphene-enhanced solutions

Cabot Corporation sets the benchmark in carbon black masterbatches, advancing toward mass-balanced and circular black additives in 2026. The Replasblak® series incorporates ISCC PLUS-certified mechanically recycled polymers as carrier resins. Cabot remains a global leader in UV protection and conductivity additives for wire, cable insulation, and automotive exterior components. Through partnerships with graphene technology firms, the company is commercializing graphene-enhanced black masterbatches to improve strength and thermal conductivity. Its high-jetness black solutions serve premium cosmetics and luxury packaging markets where aesthetics and performance converge.

Plastika Kritis S.A. expands multifunctional agricultural masterbatches across emerging markets

Plastika Kritis S.A. is a regional leader specializing in additive masterbatches for agricultural and infrastructure applications. The company’s self-sufficiency in raw materials enables competitive pricing in calcium carbonate and talc filler masterbatches. It leads globally in multifunctional agricultural additives, including thermal-control and anti-dripping agents for greenhouse films. As of 2026, Plastika Kritis is aggressively expanding into Africa and Latin America to capture infrastructure-driven demand. The expansion of its Global Colors network ensures localized production of customized additive blends for regional packaging and industrial manufacturers.

China Additive Masterbatch Market: Policy-Enforced Sustainability and High-Tech Masterbatch Scaling

China’s additive masterbatch market is being redefined by policy enforcement under the 14th Five-Year Plan for the Chemical Industry, particularly the “Action on Whole Chain Treatment of Plastic Pollution (2021–2025).” This framework mandates a rapid transition toward biodegradable, recyclable, and performance-optimized masterbatches across packaging, agriculture, and construction plastics. Infrastructure-linked enforcement measures—such as the 2025 prohibition on ultra-thin agricultural mulch films below 0.01 mm—are forcing manufacturers to adopt high-performance additive masterbatches that maintain mechanical strength, UV resistance, and tear integrity at reduced material thicknesses.

On the technology front, domestic producers such as Shandong Rike Chemical and Blue Ridge have shifted toward digitally enabled “smart masterbatches,” using process automation to achieve ultra-precise dispersion of UV stabilizers, antioxidants, and flame retardants. The electric vehicle boom is a major demand catalyst, driving consumption of halogen-free flame retardant masterbatches for battery enclosures and lightweight interior components. Agricultural innovation is also accelerating, with graphene-enhanced polyethylene masterbatches gaining traction for greenhouse films due to their superior gas barrier and UV performance. Sustainability leadership is further reinforced by milestones such as LyondellBasell’s Dalian facility operating on 100% renewable electricity as of April 2025, setting a regional benchmark for low-carbon masterbatch manufacturing.

United States Additive Masterbatch Market: Trade Protection, PFAS Elimination, and Medical-Grade Expansion

The United States additive masterbatch market is increasingly shaped by trade policy, healthcare expansion, and chemical safety regulation. In early 2025, tariff adjustments on specialty pigments and flame-retardant chemistries raised import duties by up to 10 percentage points, accelerating supplier requalification in favor of domestic masterbatch producers. This shift has strengthened local supply chains while increasing investment in high-value, application-specific additive systems.

Healthcare plastics represent one of the fastest-growing segments. LyondellBasell’s October 2025 expansion of its Purell healthcare polymers portfolio brought medical-grade polyolefin masterbatch technologies closer to US-based syringe, IV bottle, and diagnostic device manufacturers. Parallelly, PFAS-free transitions are reshaping product design; Avient launched Mevopur™ non-PFAS low-retention additives in late 2025 to comply with state-level bans, particularly for medical pipette tips. Sustainability transparency is also advancing, with ISO 14067-certified Product Carbon Footprint calculators becoming standard practice. In packaging and electronics, new PCR-rich masterbatches introduced in 2025 now incorporate up to 98% recycled polycarbonate, enabling circularity without compromising performance.

Germany Additive Masterbatch Market: Regulatory Benchmarking and Circular Masterbatch Leadership

Germany remains Europe’s innovation and compliance benchmark for additive masterbatches, supported by strong regulatory alignment and advanced processing infrastructure. The K 2025 Trade Fair in Düsseldorf served as the global launch platform for next-generation low-halogen and halogen-free flame retardant masterbatches, including Ampacet’s Halolite 527 and Halofree 533, engineered to meet EN 50642 requirements. These developments directly address the forthcoming 2026 revisions to European chemical safety standards, positioning German suppliers ahead of regulatory enforcement.

Medical plastics are another growth vector. At Medica 2025, German manufacturers showcased antimicrobial masterbatches designed to suppress bacterial growth in high-touch medical device housings, reflecting rising infection-control standards across European healthcare systems. Circular economy policy is equally influential; universal circular black masterbatches such as Cabot’s REPLASBLAK—featuring ISCC PLUS-certified sustainable content—are gaining adoption across automotive and consumer goods. Industrially, German processors are emphasizing micro-dosing technologies to reduce additive waste in high-speed extrusion, improving yield and cost efficiency in automotive and industrial applications.

India Additive Masterbatch Market: Infrastructure Demand, Localization, and Bio-Based R&D Momentum

India’s additive masterbatch market is expanding rapidly on the back of infrastructure investment, petrochemical integration, and policy-driven localization. The National Infrastructure Pipeline is fueling sustained demand for anti-corrosive, UV-stabilizing, and antioxidant masterbatches used in PVC and CPVC pipes for water, sanitation, and urban development projects. Concurrently, downstream polypropylene expansions by state-owned majors such as Indian Oil Corporation Limited are strengthening localized supply chains for additive compounding.

Packaging represents a major consumption driver, as the food and beverage sector shifts toward premium, shelf-life-extending solutions. Anti-fog and antioxidant masterbatches are increasingly deployed to maintain clarity and freshness in packaged produce. Policy incentives under the Production Linked Incentive (PLI) scheme are accelerating R&D investments, with companies such as Plastiblends India expanding into bio-based additives. In parallel, India’s startup ecosystem is attracting venture capital into climate-tech ventures focused on plastic waste upcycling through advanced additive packages, adding an innovation layer to the domestic masterbatch landscape.

South Korea Additive Masterbatch Market: Electronics, Batteries, and Digitally Optimized Production

South Korea’s additive masterbatch industry is strongly aligned with advanced electronics, semiconductors, and energy storage applications. Chemical majors such as LG Chem are prioritizing antistatic and conductive masterbatches for clean-room environments used in semiconductor fabrication. Battery technology is another focal area, with rapid innovation in acrylic-based binders and additive concentrates for lithium-ion battery separators, supporting thermal stability and cycle life improvements.

From a trade perspective, South Korean producers are leveraging Free Trade Agreements to dominate exports of high-clarity clarifier masterbatches to Southeast Asia, particularly for food packaging and consumer goods. Digitally, the sector is adopting AI-driven polymerization control and digital twin technologies—implemented at sites such as Borealis—to enhance batch-to-batch consistency and reduce formulation variability, strengthening Korea’s position in precision masterbatch manufacturing.

Luxembourg / Europe Additive Masterbatch Market: Sustainable Scale-Up and Medical Compliance Hub

The Luxembourg-centered European hub plays a strategic role in scaling sustainable and medical-grade masterbatch solutions across the EMEA region. In August 2025, Avient extended its Edgetek™ REC PC solutions across EMEA, delivering recycled content levels of up to 98% while preserving near-virgin mechanical performance. This addresses growing demand from electronics and automotive OEMs seeking verified circular materials.

Specialty medical grades are another priority, with Mevopur™ chemical foaming agents enabling up to 20% material reduction in medical injection molding—directly supporting European pharmaceutical packaging mandates. At the infrastructure level, regional players are investing heavily in converting masterbatch extrusion lines to all-electric drives, aligning production assets with the European Green Deal’s carbon reduction targets and reinforcing Europe’s role as a sustainability-driven masterbatch innovation hub.

Comparative Overview: Strategic Positioning by Country in the Additive Masterbatch Industry

Additive Masterbatch Market County Level Snapshot

|

Country / Region

|

Core Demand Drivers

|

Strategic Industry Impact

|

|

China

|

Plastic pollution policy, EV growth, agriculture films

|

Volume scale with high-performance, low-carbon shift

|

|

United States

|

Tariffs, PFAS bans, healthcare plastics

|

Domestic sourcing and premium medical-grade masterbatches

|

|

Germany

|

REACH updates, circular economy, medical devices

|

Regulatory leadership and advanced specialty formulations

|

|

India

|

Infrastructure build-out, packaging growth, PLI incentives

|

Localization and bio-based innovation momentum

|

|

South Korea

|

Semiconductors, batteries, digital manufacturing

|

Precision additives for high-tech applications

|

|

Luxembourg / Europe

|

Circular PC, medical compliance, green energy

|

Regional sustainability and healthcare masterbatch hub

|

Additive Masterbatch Market Report Scope

Additive Masterbatch Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.7 Billion

|

|

Market Size (2034)

|

$50.5 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type (Antimicrobial Masterbatch, Antioxidant Masterbatch, Flame Retardant Masterbatch, UV Stabilizer Masterbatch, Anti-static Masterbatch, Optical Brighteners, Anti-fog Masterbatch, Lubricant/Processing Aid Masterbatch), By Carrier Resin (Polyethylene, Polypropylene (PP), Polystyrene (PS), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Engineering Plastics, Bio-based/Biodegradable Polymers), By End-Use Industry (Packaging, Automotive, Building & Construction, Agriculture, Healthcare/Medical, Electrical & Electronics, Consumer Goods & Textiles), By Form (Granule, Pellet, Powder, Liquid/Slurry)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avient Corporation, LyondellBasell Industries N.V., Clariant AG, Ampacet Corporation, BASF SE, Cabot Corporation, LG Chem Ltd., Plastiblends India Limited, Tosaf Group, Penn Color, Inc., Shandong Rike Chemical Co., Ltd., Hubron International, Plastika Kritis S.A., Americhem, Inc., A. Schulman

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Additive Masterbatch Market Segmentation

By Type

- Antimicrobial Masterbatch

- Antioxidant Masterbatch

- Flame Retardant Masterbatch

- UV Stabilizer Masterbatch

- Anti-static Masterbatch

- Optical Brighteners

- Anti-fog Masterbatch

- Lubricant/Processing Aid Masterbatch

By Carrier Resin

- Polyethylene

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Polyethylene Terephthalate (PET)

- Engineering Plastics

- Bio-based/Biodegradable Polymers

By End-Use Industry

- Packaging

- Automotive

- Building & Construction

- Agriculture

- Healthcare/Medical

- Electrical & Electronics

- Consumer Goods & Textiles

By Form

- Granule

- Pellet

- Powder

- Liquid/Slurry

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Additive Masterbatch Market

- Avient Corporation

- LyondellBasell Industries N.V.

- Clariant AG

- Ampacet Corporation

- BASF SE

- Cabot Corporation

- LG Chem Ltd.

- Plastiblends India Limited

- Tosaf Group

- Penn Color Inc.

- Shandong Rike Chemical Co. Ltd.

- Hubron International

- Plastika Kritis S.A.

- Americhem Inc.

- Schulman

*- List not Exhaustive