Organic Rheology Modifiers Market Driven by Bio-Based Acrylic Conversion and High-Performance Personal Care Innovation

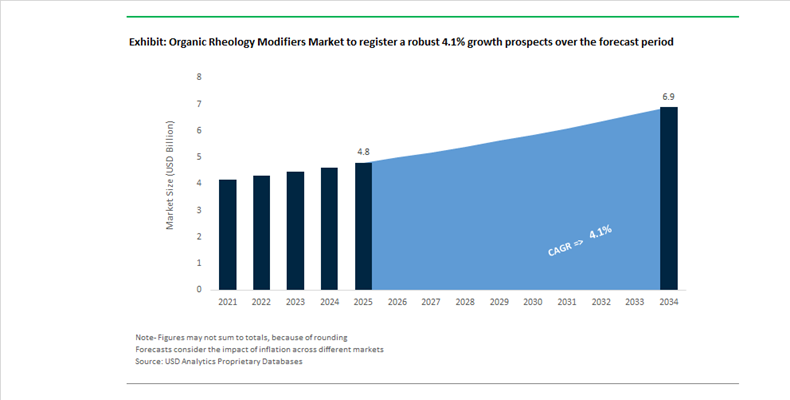

The Organic Rheology Modifiers Market Valued at $4.8 Billion in 2025 Projected to Reach $6.9 Billion by 2034 at 4.1% CAGR is undergoing structural transformation driven by bio-based feedstock adoption, sustainable polymer engineering, and localized innovation investments. Organic rheology modifiers, including acrylic thickeners, associative polymers, polyurethanes, and organo-modified clays, are critical for viscosity control, shear stability, suspension performance, and texture optimization across paints, coatings, adhesives, pharmaceuticals, and personal care formulations. The 2024 to 2026 period marks a decisive pivot toward biodegradable polymers, reduced VOC content, and renewable carbon integration without compromising rheological performance under complex formulation conditions.

In March 2025, Lubrizol launched Carbopol® BioSense, the first readily biodegradable polymer within its flagship Carbopol portfolio. Developed in collaboration with Suzano, this 98% natural-origin rheology modifier leverages responsibly sourced eucalyptus pulp feedstock. The innovation directly addresses rising demand for sustainable thickeners in skin care and sun care formulations, where biodegradability and sensory performance are increasingly scrutinized. In April 2025, Arkema transitioned its European acrylic thickeners portfolio to bio-based feedstocks, introducing up to 30% bio-based content and achieving up to 25% carbon footprint reduction. This move strengthens Arkema’s position in architectural coatings and adhesives while maintaining viscosity stability and film-forming integrity. In October 2025, BASF finalized the sale of its decorative paints business to Sherwin-Williams, redirecting capital toward upstream specialty additives such as Rheovis® rheology modifiers and Licity® binders aligned with its Green Transformation strategy.

Asia-Pacific capacity expansion accelerated in late 2025. In November 2025, Clariant inaugurated a CHF 80 million care chemicals facility in Daya Bay, China. The site significantly increases regional production of Aristoflex™ organic rheology modifiers for pharmaceutical, home care, and personal care markets. The same month, Clariant introduced Aristoflex™ SUN, engineered to enhance SPF stability in high-oil-load sunscreen formulations while maintaining light skin feel. In October 2025, Elementis launched the BENTONE® ULTIMATE series, featuring organically modified hectorite clays activated by a 100% natural system for oil-phase rheology control in premium cosmetics. Elementis had earlier expanded its industrial portfolio in March 2024 with RHEOLATE® 125 P and 185 P, VOC-free ASE and HASE thickeners for paper and cardboard coatings, improving water retention and flow control.

Strategic restructuring and innovation localization define competitive positioning. In December 2025, Arkema proposed divesting its plastic additives and MBS business to Praana, expected to close in Q1 2026, further concentrating on coating solutions and specialty rheology technologies. In 2024, Ashland introduced Texturpure™ SA-2, a salt-tolerant, cold-processable rheology modifier targeting rinse-off formulations as a biodegradable alternative to legacy synthetic polymers. Lubrizol expanded its regional R&D footprint with a Singapore innovation hub in July 2025 and a Shanghai innovation center in February 2026, reinforcing a local-for-local strategy in Asia. In October 2025, Croda International received recognition for Natrineo™ CR8, a naturally derived emulsifier and rheology modifier supporting advanced neurocosmetic and skin-repair applications.

Across coatings, cosmetics, adhesives, and pharmaceutical formulations, the shift toward renewable carbon indices, PFAS-free chemistries, and low-carbon acrylic systems is redefining product development pipelines. Manufacturers are prioritizing associative thickener efficiency, shear-thinning precision, and electrolyte tolerance to meet increasingly complex formulation requirements in high-growth end-use sectors.

Organic Rheology Modifiers Market Trends and Opportunities

Trend: Mandatory Reformulation for Zero-VOC Waterborne Architectural Coatings

Global architectural coatings manufacturers are being forced into accelerated reformulation cycles as air quality regulations tighten across North America and Europe. Updated limits under the California Air Resources Board and parallel enforcement through the EU Industrial Emissions Directive have effectively closed the door on solvent-based rheology control systems. As a result, organic rheology modifiers have shifted from performance enhancers to compliance-critical formulation components, particularly in waterborne interior and exterior coatings.

As of January 2025, CARB Suggested Control Measures lowered allowable VOC limits to 50 g/L for flat coatings and 150 g/L for non-flat high-gloss applications in several high-population districts. These thresholds cannot be achieved using legacy solvent-borne thickeners without sacrificing application properties. Hydrophobically Modified Ethoxylated Urethanes and Hydrophobically Modified Alkali-Swellable Emulsions are therefore seeing mandatory adoption, as they deliver shear-responsive viscosity control, superior spatter resistance, and film build while remaining zero-VOC. Industrial formulation data from 2024–2025 shows that modern HEUR systems can improve flow and leveling by 15% to 20% versus early-generation waterborne thickeners, restoring the “brush-drag” and aesthetic finish expected in premium residential paints.

In Europe, regulatory pressure is extending beyond VOCs into raw material composition. ECHA reporting in late 2025 confirms that several monomers historically used in acrylic-based thickeners have entered the Community Rolling Action Plan for substance evaluation. This has triggered a strategic pivot toward acrylate-free, bio-based alkyd hybrids and silicate-compatible organic modifiers designed to meet EU Ecolabel indoor air quality benchmarks. For coatings suppliers, rheology modifiers are now directly linked to ESG positioning, lifecycle carbon reduction, and regulatory durability rather than short-term formulation flexibility.

Trend: Precision Texture Control in Plant-Based Meat and Dairy Analogues

As the plant-based food sector matures, texture and mouthfeel have become the primary differentiators replacing early-stage novelty. Organic rheology modifiers are now engineered as multifunctional structural systems that replicate the thermogelation, fat melt, and bite characteristics of animal-derived products without triggering clean-label concerns.

Methylcellulose remains a cornerstone of this transition. A 2025 comparative study demonstrated that a 3 g per 100 g methylcellulose system can act as a standalone functional binder in plant-based burgers, delivering thermal gelation during cooking while reducing additive complexity. This capability allows manufacturers to shorten ingredient lists, directly addressing consumer resistance to ultra-processed food perceptions. In parallel, enzymatic cross-linking approaches are gaining traction. Developments announced in 2024–2025 show how protein networks can be cross-linked with sugar beet pectin using enzymatic pathways, improving juiciness and chew while avoiding synthetic stabilizers.

Dairy alternatives present a different rheological challenge centered on long-term suspension stability and low-pH tolerance. High-purity organic hydrocolloids are increasingly used to maintain uniform viscosity in plant-based milks and yogurts, preventing sedimentation of pea or soy proteins across extended shelf lives. These rheology systems are becoming central to premium product positioning, particularly in refrigerated dairy analogues where visual consistency and mouthfeel are decisive purchase factors.

Opportunity: Rheological Engineering for High-Solid Battery Electrode Slurries

The global expansion of lithium-ion battery gigafactories is creating a high-margin demand environment for organic rheology modifiers capable of operating under extreme solid-loading conditions. Battery electrode slurries routinely exceed 60% solids by weight, placing unprecedented stress on viscosity control, particle suspension, and coating uniformity.

Research published in early 2025 highlights the central role of Carboxymethyl Cellulose in stabilizing graphite and silicon-rich anode slurries. Advanced organic modifiers are now used to precisely tune yield stress, ensuring that dense active materials remain suspended during mixing and coating while still flowing under shear. This balance is essential for defect-free electrode layers in high-energy-density cells. Thixotropic recovery has emerged as a critical performance metric. Data from high-speed coating trials in 2025 shows that slurries with optimized organic rheology modifiers can regain structural integrity immediately after shear, reducing coating defects by up to 90% and significantly lowering scrap rates.

Rheological metrology itself is becoming a strategic differentiator. Battery research institutions have identified slurry rheology control as a priority for nickel-rich NMC cathodes, which require stable performance in high-pH aqueous systems. This creates a specialized opportunity for suppliers able to deliver battery-grade organic thickeners with consistent molecular weight distribution, impurity control, and electrochemical compatibility.

Opportunity: Biodegradable Drift Control Agents for Precision Agriculture

Agricultural spraying regulations are tightening rapidly as governments seek to reduce off-target pesticide movement and environmental exposure. Organic rheology modifiers are emerging as critical drift control agents that improve spray droplet stability while remaining biodegradable and microplastic compliant.

The U.S. EPA’s final Insecticide Strategy released in April 2025 under the Endangered Species Act introduced mandatory mitigation menus that explicitly reward the use of drift-reduction adjuvants. This regulatory framework has immediately increased demand for organic polymer-based modifiers that increase droplet size and suppress fine mist formation without interfering with active ingredient performance. In Europe, parallel restrictions on synthetic microplastics are accelerating adoption of bio-derived alternatives.

Innovation in bacterial cellulose production represents a structural inflection point. Scaled commercial production announced in mid-2025 positions bacterial cellulose as a drop-in rheology modifier for seed coatings, fertilizer encapsulation, and spray adjuvants. Its biodegradability and shear-stable viscosity profile align directly with upcoming EU microplastic bans. At the same time, the rapid adoption of UAV-based spraying systems has created a niche requirement for low-foam, high-precision organic rheology modifiers that maintain droplet spectra under high-pressure, low-volume application conditions. With more than a quarter of U.S. farms now using precision agriculture tools, this segment represents a fast-growing convergence of agri-chemistry and digital farming through 2026.

Organic Rheology Modifiers Market Share and Segmentation Insights

Synthetic Organic Rheology Modifiers Lead Market Demand with Precision Viscosity Control in Advanced Formulations

Synthetic organic modifiers accounted for 58.60% of the Organic Rheology Modifiers Market by origin in 2025, reflecting their widespread adoption in performance-critical formulations across multiple industries. Acrylic polymers, polyurethane thickeners, hydrophobically modified ethoxylates, and associative rheology modifiers provide precise viscosity control, predictable flow behavior, and consistent product stability. These properties are essential in applications such as paints and coatings, cosmetics, and pharmaceutical formulations where controlled rheology directly influences application performance and product quality. In 2025, innovation in bio-based synthetic hybrid rheology modifiers is gaining momentum, with manufacturers incorporating renewable monomers into polymer architectures to increase renewable carbon content while maintaining the performance characteristics required for high-performance industrial and consumer formulations.

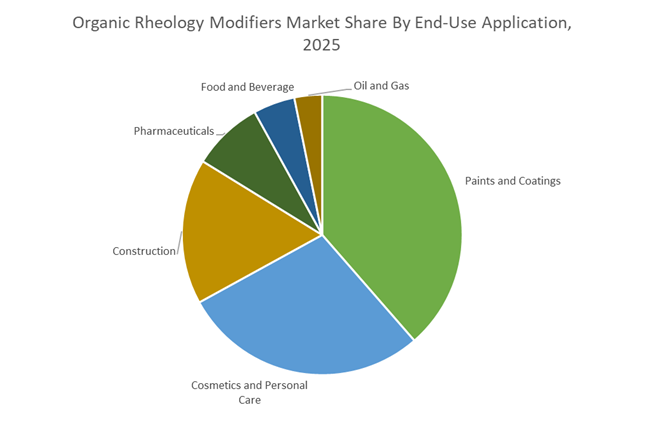

Paints and Coatings Segment Dominates Organic Rheology Modifier Consumption in Waterborne Coating Systems

Paints and coatings represented 38.60% of the Organic Rheology Modifiers Market by end-use application in 2025, making it the largest demand segment due to the critical role rheology modifiers play in coating formulation. These additives control application properties such as brushability, roller spatter resistance, sag control, leveling behavior, and storage stability in architectural and industrial coatings. The large global production volume of decorative and protective coatings continues to drive consumption of advanced rheology modifier technologies. A major industry trend in 2025 is the low-VOC coating transition, where waterborne paint formulations rely heavily on associative thickeners and polymer-based rheology modifiers to achieve optimal high-shear viscosity and application performance without the use of volatile organic solvents.

Organic Rheology Modifiers Market Competitive Landscape

The Organic Rheology Modifiers Market is highly competitive, driven by bio-based rheology additives, AI-enabled formulation technologies, and regional capacity expansion. Key players are leveraging sustainable chemistries, vertical integration, and advanced polymer engineering to capture demand across coatings, personal care, adhesives, and construction chemicals.

BASF scales AI-driven rheology modeling and Asia-Pacific coatings expansion

BASF SE is consolidating its leadership in organic rheology modifiers through a dual strategy of digital formulation and sustainable additive innovation. The integration of AI-assisted rheology simulation tools into R&D enables precise viscosity prediction in waterborne coatings, reducing formulation time and improving performance consistency. Its portfolio of polyurethane-based thickeners and acrylic associative rheology modifiers is optimized for low-VOC, high-efficiency coatings, aligning with tightening environmental regulations. Strategically, BASF’s local-for-local manufacturing model is expanding production and technical support capabilities in Asia-Pacific, particularly in China and India, where construction chemicals demand is accelerating. This regional expansion enhances supply chain agility and customer proximity. The company’s focus on eco-friendly rheology additives positions it strongly in next-generation architectural and industrial coatings markets.

Elementis leverages hectorite assets and acquisition-led clean beauty expansion

Elementis PLC is strengthening its competitive edge by combining unique raw material control with targeted acquisition strategy in natural rheology modifiers. The acquisition of Alchemy Ingredients introduces advanced oil- and water-gelling technologies such as Sucragel and Clearthix, significantly enhancing its clean beauty and personal care portfolio. Backed by consistent R&D investment of 2.5% to 3% of revenue, the company is aligning its entire innovation pipeline with sustainability benchmarks by 2026. Ownership of a high-grade hectorite mine in California provides a critical feedstock advantage for premium hybrid organic-inorganic rheology solutions. Additionally, expansion of technical service centers in Mumbai and Shanghai strengthens localized formulation support for emerging markets. This integrated approach enables Elementis to capture growth in both high-performance coatings and premium skincare applications.

Arkema advances bio-based acrylic thickeners with vertically integrated supply chain

Arkema S.A. is accelerating its transition toward bio-based rheology modifiers, particularly through the conversion of its European acrylic thickener portfolio under Rheotech, Thixol, and Viscoatex brands. With up to 30% bio-based content and a 25% reduction in product carbon footprint, these additives maintain performance parity in coatings and adhesives applications. The launch of CRAYVALLAC SLW highlights Arkema’s focus on high-performance industrial rheology modifiers with enhanced sag resistance. A key competitive differentiator is its vertically integrated supply chain, supported by bio-sourced ethyl acrylate production in Carling, France. This ensures raw material security and cost efficiency while supporting sustainability goals. Arkema’s strategy positions it strongly in regulatory-driven markets demanding low-carbon, high-performance specialty materials.

Lubrizol expands biodegradable polymer portfolio and IMEA production capacity

The Lubrizol Corporation is reinforcing its position in organic rheology modifiers through innovation in biodegradable polymers and strategic geographic expansion. The introduction of Carbopol BioSense Polymer, derived from eucalyptus, delivers high-performance rheology control with biodegradability, targeting premium personal care applications. Its partnership with Zhejiang Fulai New Material supports development of bio-based coatings for sustainable packaging, expanding into adjacent high-growth sectors. The company’s Shanghai Innovation Center enhances R&D collaboration across Asia-Pacific, accelerating product commercialization. Concurrently, capacity expansion at its Dahej, India facility strengthens supply to the IMEA region, addressing rising demand in coatings and specialty additives. This integrated strategy of innovation, partnerships, and regional manufacturing scale enhances Lubrizol’s competitive positioning.

Clariant builds multifunctional rheology systems for high-value personal care applications

Clariant AG is differentiating through multifunctional organic rheology modifiers that combine performance enhancement with formulation efficiency. Aristoflex SUN exemplifies this strategy by delivering both rheology control and SPF boosting in sun care formulations, targeting high-margin personal care segments. The commissioning of its CHF 80 million Care Chemicals facility in Daya Bay, China, significantly expands production capacity and regional supply capabilities. Clariant’s Licocare RBW additives, based on renewable rice bran wax, have secured EU approval for food-contact applications, broadening its sustainable additives portfolio. Integration of Lucas Meyer Cosmetics enables the company to offer complete formulation systems that combine actives with advanced rheology control. This positions Clariant strongly in premium, innovation-driven specialty chemicals markets.

Germany – Bio-Based Conversion and Polymer-Level Regulatory Leadership

Germany is setting the technical and regulatory benchmark for organic rheology modifiers through accelerated bio-based feedstock adoption and early compliance with evolving EU chemical legislation. In June 2025, BASF SE completed the transition to bio-based ethyl acrylate for its Rheovis® portfolio at the Ludwigshafen site, achieving up to 35% biogenic content under ASTM D6866-18 without compromising viscosity control, flow leveling, or shear-thinning performance. This move positions Germany at the forefront of drop-in sustainable rheology modifiers for architectural coatings, adhesives, and construction chemicals, where performance parity with fossil-based thickeners is non-negotiable for professional formulators.

Decarbonization is being institutionalized at the product level. BASF’s 2025–2026 roadmap targets a 30% reduction in Product Carbon Footprint for HASE rheology modifiers through the Biomass Balance approach, integrating certified renewable feedstocks upstream rather than reformulating end products. Regulatory pressure reinforces this shift. The REACH Revision 2025 introduces polymer registration thresholds above one tonne per year, directly affecting complex organic rheological additives that were previously exempt. German manufacturers are leading dossier preparation and hazard evaluation for these polymers, reducing future compliance risk for downstream customers. In parallel, industry commitments to operate specialty resin and dispersion assets on 100% green electricity by the end of 2025 further strengthen Germany’s positioning as the compliance-driven innovation center for organic rheology modifiers in Europe.

United States – Clean Beauty Pull and Functional Polymer Replacement

The United States organic rheology modifiers market is being reshaped by biodegradability requirements and functional replacement of legacy polyacrylates. In late 2025, The Lubrizol Corporation introduced Carbopol® BioSense, a readily biodegradable organic rheology modifier derived from responsibly sourced eucalyptus. The product directly targets the clean beauty and personal care segments, where sensory performance, yield stress control, and biodegradability are increasingly assessed together by brand owners and regulators.

At the same time, technical modernization is accelerating across formulation platforms. Ashland Inc. announced a strategic shift away from conventional crosslinked carbomers toward Texturpure™ SA-2, a multifunctional organic modifier designed for rinse-off systems with enhanced salt and heat tolerance. This transition reflects broader formulation challenges created by low-VOC and solvent-restricted environments. Infrastructure investment supports these changes. During 2025, U.S. producers expanded continuous flow reactor capacity to manufacture high-purity HEUR rheology modifiers for architectural coatings, improving molecular weight control and batch-to-batch consistency. Regulatory signals also matter. The EPA’s Technology Transitions under the AIM Act for 2025–2026 are indirectly influencing rheology selection, as formulators seek thickeners that remain stable in next-generation low-GWP solvent and refrigerant systems.

China – Specialty Scale-Up for EV, Solar, and Advanced Films

China’s organic rheology modifiers industry is transitioning from volume-oriented dispersions toward high-purity, application-specific additives aligned with electric mobility, solar energy, and advanced films. In March 2025, Arkema completed a major expansion at its Changshu site, increasing specialty organic chemical capacity by 2.5 times, including rheology modifiers tailored for EV components and photovoltaic encapsulants. These applications require precise viscosity control under thermal cycling and long-term UV exposure, elevating demand for advanced organic modifiers over inorganic alternatives.

Global producers are reinforcing local-for-local strategies. BASF SE inaugurated a new production line in late 2025 dedicated to low-VOC and low-CO₂ dispersions engineered specifically for Asian architectural coatings, reflecting region-specific climate and application needs. The Lubrizol Corporation expanded its Shanghai footprint with a Paint Protection Film production line and a Film Center of Excellence, integrating organic rheology modifiers to enhance film clarity, flow uniformity, and self-healing performance. Looking ahead, the MIIT 2026 industrial plan prioritizes breakthroughs in electronic-grade rheological additives for semiconductor packaging and display manufacturing, signaling a move into ultra-high-purity, contamination-sensitive niches.

India – Capacity Build-Out and Bio-Derived Innovation

India is emerging as a high-growth production and innovation base for organic rheology modifiers, supported by domestic manufacturing policy and construction-led demand. In late 2025, The Lubrizol Corporation announced the doubling of capacity at its Dahej facility, focusing on specialty polymers and rheological solutions aligned with the Atmanirbhar Bharat initiative. This expansion strengthens local supply of thickeners and flow modifiers for coatings, sealants, and infrastructure chemicals, reducing dependence on imports.

Innovation support is widening. The expansion of the government-backed Science and Technology Clusters initiative toward 25 sites by 2026 is enabling R&D on lignin-based and starch-derived organic modifiers for construction and infrastructure applications, where cost efficiency and sustainability are both critical. Export competitiveness is also shaping investment decisions. Indian manufacturers such as Aditya Birla Chemicals upgraded performance additives units in 2025 to comply with European Ecolabel requirements, ensuring that domestically produced organic rheology modifiers meet stringent environmental and performance benchmarks for global coatings markets.

Türkiye – Regional Supply Anchor with Certified Low-Carbon Output

Türkiye is positioning itself as a strategic regional hub for organic rheology modifiers serving the Middle East and Northwest Africa. In October 2025, BASF SE commissioned a new production line at its Dilovası site, expanding availability of low-VOC dispersions and rheology-modifying additives tailored for regional construction, infrastructure, and industrial coatings demand. This investment strengthens supply security for fast-growing markets that previously relied on longer import routes from Western Europe.

Sustainability credentials are embedded from the outset. The Dilovası facility operates under the Biomass Balance approach, enabling customers to source organic rheology modifiers with certified reduced carbon footprints without altering formulation performance. This capability is increasingly relevant for large infrastructure projects in the region that now specify carbon-accounted materials as part of tender requirements, giving Türkiye a differentiated role in the regional value chain.

Comparative Country Snapshot – Organic Rheology Modifiers

Organic Rheology Modifiers Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Technology Focus

|

Competitive Position

|

|

Germany

|

Bio-based feedstocks and REACH revision

|

HASE, bio-acrylates, PCF reduction

|

Global compliance and innovation leader

|

|

United States

|

Clean beauty and polymer replacement

|

Biodegradable carbomers, HEUR

|

Formulation-driven specialty market

|

|

China

|

EV, solar, and advanced films

|

High-purity, low-VOC modifiers

|

Scale with specialty upgradation

|

|

India

|

Domestic manufacturing and construction

|

Bio-derived thickeners, export-grade additives

|

Fast-growing production hub

|

|

Türkiye

|

Regional supply security

|

Mass balance, low-carbon dispersions

|

Emerging hub for MENA markets

|

Organic Rheology Modifiers Market Report Scope

Organic Rheology Modifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$6.9 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Origin (Natural Organic Modifiers, Synthetic Organic Modifiers), By Functionality (Thickening Agents, Stabilizers and Emulsifiers, Suspending Agents, Gelling Agents), By End-Use Application (Paints and Coatings, Cosmetics and Personal Care, Pharmaceuticals, Construction, Oil and Gas, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Ashland, Lubrizol, Arkema, Dow, Evonik Industries, Croda International, Wacker Chemie, Solvay, Shin-Etsu Chemical, Clariant, CP Kelco, Kraton, DuPont, Aditya Birla Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Rheology Modifiers Market Segmentation

By Origin

- Natural Organic Modifiers

- Synthetic Organic Modifiers

By Functionality

- Thickening Agents

- Stabilizers and Emulsifiers

- Suspending Agents

- Gelling Agents

By End-Use Application

- Paints and Coatings

- Cosmetics and Personal Care

- Pharmaceuticals

- Construction

- Oil and Gas

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Rheology Modifiers Industry

- BASF

- Ashland

- Lubrizol

- Arkema

- Dow

- Evonik Industries

- Croda International

- Wacker Chemie

- Solvay

- Shin-Etsu Chemical

- Clariant

- CP Kelco

- Kraton

- DuPont

- Aditya Birla Chemicals

*- List not Exhaustive