Ink Additives Market to Reach $8.3 Billion by 2034 at 6% CAGR as PFAS-Free, Bio-Based, and Digital Printing Solutions Redefine Formulation Standards

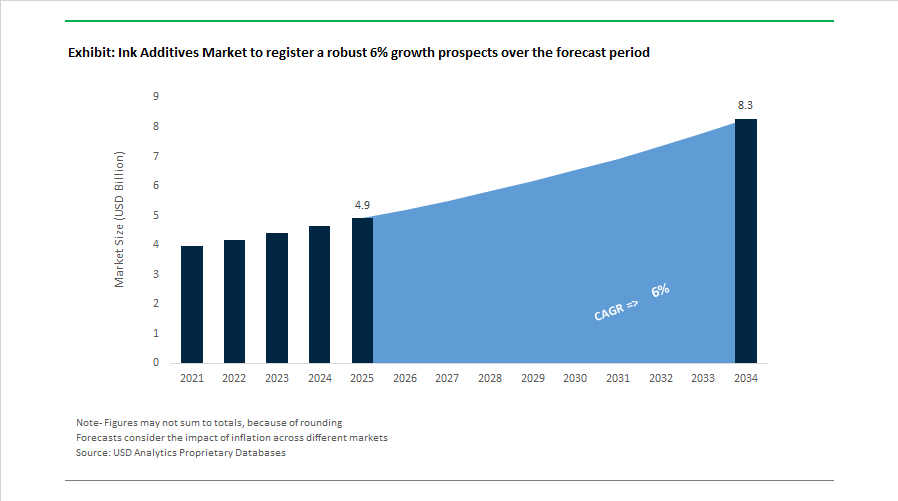

The Ink Additives Market is projected to grow from $4.9 billion in 2025 to $8.3 billion by 2034, registering a CAGR of 6%, driven by regulatory reformulation, mass-balanced raw material adoption, and the rapid shift toward high-resolution digital and UV-curable printing technologies. Between 2024 and 2026, the market experienced structural change as leading additive suppliers accelerated PFAS elimination programs, expanded bio-attributed portfolios, and strengthened regional innovation capabilities across Asia-Pacific and Europe. Sustainability certification, food-contact compliance, and compatibility with inkjet and LED curing platforms have become critical differentiators in the competitive landscape.

In February 2024, Heubach Group and Evonik announced a strategic partnership to develop eco-friendly gel and additive systems tailored for the Chinese printing market, aligning pigment chemistry with additive stabilization under tightening environmental regulations. In March 2024, Ideal Chemi Plast, a subsidiary of DIC Corporation, commenced operations at a new high-tech coating resins and additives facility in Maharashtra, India, supported by a regional Application Lab focused on graphic arts and packaging inks. On November 28, 2024, Clariant finalized its transition to a fully PFAS-free additive portfolio ahead of schedule, introducing products such as Ceridust 8330 for enhanced rub resistance and Licocare RBW VITA derived from rice bran wax with a renewable carbon index of at least 98%. In August 2024, BYK Additives issued a directive confirming the phase-out of all PFAS-containing defoamers, surface additives, and wax additives, with final shipments scheduled for December 2025, replaced by a fluorine-free portfolio engineered to maintain performance parity.

The market’s decarbonization agenda intensified in 2025. In March 2025, Evonik Coating Additives introduced its first ISCC PLUS-certified mass-balanced ink additives under the eCO label, including TEGO® Wet 270 eCO and TEGO® Foamex 812 eCO, enabling formulators to reduce Scope 3 emissions without reformulating existing systems. In May 2025, Evonik launched four AERODISP® waterborne dispersions based on SiO2 and Al2O3 particles, which by early 2026 were widely adopted in ink receptive coatings to improve dot sharpness and resolution in high-speed inkjet printing. During 2025, Evonik also introduced TEGO® Wet 288, a high-performance wetting additive compatible with waterborne and UV-cured inks and formulated to meet global food-contact compliance standards. In September 2025, INX International unveiled its “Safe and Sustainable” series at K 2025, including low-migration dual-cure inks free of barium, ITX, benzophenone, and BPA, targeting sensitive food packaging and toy applications.

Capacity expansion and geographic diversification accelerated across regions. On May 1, 2025, INX International completed the acquisition of Servicom New Zealand and Galaxy Inks & Coatings Australia, strengthening its Oceania footprint and localized additive-driven ink support. In November 2025, Sun Chemical expanded perylene pigment capacity at Ludwigshafen, Germany, including specialized surface-treated grades requiring advanced additive stabilization for high-transparency digital inks. Between July 2025 and February 2026, Lubrizol inaugurated innovation centers in Singapore and Shanghai to accelerate development of hyperdispersants and surface modifiers optimized for Asia-Pacific regulatory and climate conditions. In late 2025, Fine Organic Industries incorporated Fine Organics Americas LLC to establish its first U.S. manufacturing presence and simultaneously expanded in the UAE, reinforcing global supply of bio-based slip and anti-static additives for printing applications.

Ink Additives Market Trends and Opportunities

High-Speed Water-Based Reformulation for Recyclable Mono-Material Packaging

The global Ink Additives Market is undergoing a structural transformation as brand owners and converters accelerate the shift toward recyclable mono-material packaging formats such as all-PE and all-PP films. While these substrates support circular economy goals, their inherently low surface energy has created a critical performance gap for water-based inks, particularly at industrial press speeds exceeding 250,000 impressions per hour. This has elevated advanced wetting agents, defoamers, and dispersants from optional formulation components to mission-critical additives.

A decisive inflection point occurred in September 2024 when Evonik Coating Additives launched TEGO® Wet 570 Terra and TEGO® Wet 580 Terra. These 100% natural biosurfactants were specifically engineered to deliver high-dynamic wetting on difficult plastic films without compromising foam control or ink stability. Their market uptake reflects a broader industry pivot toward mass-balanced, low-carbon additives that enable sustainability gains without forcing costly ink re-qualification cycles for converters.

Regulatory pressure is reinforcing this transition. Updated U.S. EPA benchmarks for 2025 confirm that water-based pigment inks can reduce VOC emissions by up to 90% versus solvent-based systems. As a result, approximately 40% of new printing presses commissioned globally during 2024–2025 were designed explicitly for eco-ink compatibility. This hardware shift structurally locks in long-term demand for high-performance water-based ink additives.

Performance barriers are also narrowing. Historically, slow drying limited water-based adoption in high-speed packaging. However, 2025 press data show that when non-PTFE waxes and next-generation dispersants are optimized together, water-based inks can achieve drying efficiency comparable to solvent systems. Converters are reporting up to 20% total cost savings by eliminating explosion-proof drying tunnels and reducing energy intensity, making water-based reformulation both an environmental and economic imperative.

Strategic Scaling of Energy-Curable Additive Systems for Food and Digital Print

Energy-curable inks are transitioning from niche to mainstream across labels, metal packaging, and premium commercial print. By 2025, UV-LED and Electron Beam technologies accounted for more than 56% of global UV ink revenue, driven by energy savings of 60–65% compared to mercury lamps and sharply lower heat loads on substrates. This shift has placed additive performance, rather than press hardware, at the center of competitive differentiation.

Additive suppliers are responding with highly specialized synergists and reactive diluents that deliver full cure at lower LED energy outputs. These packages are essential for ensuring instant cure, scuff resistance, and adhesion consistency in high-throughput digital and flexographic environments.

Safety-driven reformulation is accelerating adoption further. In June 2025, INX International highlighted its GelFlex™ EB ink series, an electron-beam-curable system that completely eliminates photoinitiators. This technology directly addresses migration concerns under the EU Packaging and Packaging Waste Regulation, making it particularly attractive for infant formula packaging and retort pouches where compliance thresholds are exceptionally strict.

Sustainability alignment is now extending into energy-curable systems. In July 2025, Sun Chemical introduced SunCure Advance ECO, a UV-sheetfed ink platform containing 25–30% bio-renewable content. This launch demonstrated that UV inks can now deliver high-gloss, abrasion-resistant performance while supporting soy certification and circular economy objectives, expanding the addressable market for bio-based UV additives.

Conductive Additives Enabling Printed Electronics and Smart Packaging

A high-growth opportunity is emerging as inks evolve from decorative layers into functional electronic components. The rapid scale-up of printed electronics, RFID tags, and flexible sensors is driving demand for conductive additives such as silver flakes, copper nanoparticles, and graphene dispersions.

Global retail inventory mandates pushed RFID tag production to an estimated 38 billion units in 2025. This unprecedented volume is forcing formulators to adopt silver-thrifting strategies and copper-based conductive additives that preserve conductivity while cutting material costs by as much as 70%. These additives are increasingly critical for maintaining margin viability in high-volume smart packaging applications.

Performance benchmarks continue to improve. By 2025, advanced screen-printing lines were processing up to 8,000 wafers per hour using conductive pastes optimized to viscosities around 250 Pascal-seconds. In healthcare, next-generation conductive inks demonstrated impedance stability below 50 Ohms over 14 days of continuous skin contact, enabling reliable use in wearable glucose monitors and biosensors.

Automotive electrification is further expanding this opportunity. OEMs are replacing traditional copper wiring with printed silver and carbon tracks in seat heaters, defoggers, and sensors. In 2025 vehicle platforms, this additive-enabled substitution reduced vehicle weight by an average of 2.5 kilograms, directly supporting EV range extension and lightweighting targets.

Durable Antimicrobial and Anti-Viral Ink Additives for Regulated Packaging

Heightened hygiene awareness has transformed antimicrobial ink additives into a structurally embedded demand driver rather than a temporary response. These chemistries are increasingly specified in pharmaceutical, food, education, and consumer packaging where surface hygiene contributes to brand trust and regulatory compliance.

In pharmaceutical packaging, antimicrobial inks are being integrated into primary and secondary packs to maintain contamination-free external surfaces throughout distribution. Additives such as encapsulated silver ions and controlled-release quaternary compounds are being tailored to deliver long-lasting efficacy without compromising print durability or regulatory migration limits.

Food packaging represents another high-value use case. Antimicrobial additives are helping inhibit yeast and fungal growth on packaging surfaces, directly supporting shelf-life extension in ready-to-eat segments. This functionality aligns closely with Zero-Waste initiatives by reducing premature spoilage and downstream food loss.

Regulatory tightening is shaping innovation priorities. As U.S. FDA, EU, and WHO frameworks increasingly restrict PFAS, triclosan, and other legacy biocides, the market is opening for clean-label antimicrobial additives. Suppliers capable of delivering 99.9% antimicrobial efficacy while meeting strict migration and toxicity thresholds are positioned to capture premium, compliance-driven demand across global packaging markets.

Ink Additives Market Share and Segmentation Insights

Dispersing and Wetting Agents Anchor Ink Additives Formulation Through Advanced Pigment Stabilization

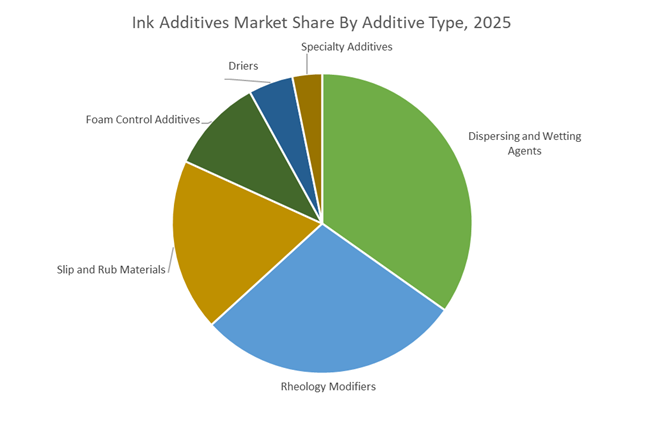

Dispersing and wetting agents represented 34.80% of the Ink Additives Market share in 2025, making them the most widely used additive class in modern ink formulation technologies. These additives play a critical role in pigment stabilization, particle dispersion, and substrate wetting, ensuring uniform color development and preventing pigment agglomeration during printing operations. In commercial and industrial printing systems, dispersants enable pigments to remain evenly suspended within ink formulations, maintaining consistent viscosity, color strength, and print clarity across different printing technologies such as flexographic, gravure, offset, and digital inkjet printing. The importance of dispersing agents has increased significantly with the expansion of high-resolution digital printing and advanced inkjet technologies, which require extremely fine pigment particles to pass through microscopic nozzles without clogging. In 2025, additive manufacturers are focusing on polymeric dispersants engineered for nanoparticle stabilization, enabling higher pigment loading, improved color saturation, and enhanced jetting reliability in inkjet inks used in packaging, labels, and industrial printing applications.

Packaging Industry Generates the Largest Demand for Ink Additives in Global Printing Applications

Packaging accounted for 52.80% of the Ink Additives Market share in 2025, positioning it as the dominant end-use sector for printing ink formulations. Packaging materials such as flexible films, pressure-sensitive labels, folding cartons, and corrugated containers require high-performance inks for product branding, regulatory labeling, traceability information, and consumer communication. The rapid expansion of e-commerce logistics, consumer packaged goods, and flexible packaging technologies continues to drive ink consumption, which directly increases demand for functional ink additives that control viscosity, pigment dispersion, slip properties, and drying performance. Ink additives enable printing systems to deliver consistent adhesion, color vibrancy, scratch resistance, and surface durability across packaging substrates including plastics, paperboard, metal foils, and laminates. In 2025, the packaging sector has also accelerated demand for low-migration and food-contact-compliant ink additives, as regulatory authorities impose strict standards on packaging inks used for food, beverages, pharmaceuticals, and personal care products. Additive manufacturers increasingly develop migration-free dispersants, slip agents, and photoinitiator alternatives designed to meet global food safety regulations while maintaining high print quality and process efficiency.

Competitive Landscape in Ink Additives Market

ALTANA AG Through BYK Sets the Benchmark in Specialty Ink Additives

ALTANA AG’s BYK division remains a technical leader in specialty ink additives, emphasizing high-value formulation chemistry and localized R&D proximity. In December 2025, ALTANA secured a €300 million credit line from the European Investment Bank to accelerate sustainable research programs through 2026 and beyond, reinforcing its carbon-neutral production roadmap. The company reported 2024 sales exceeding €3 billion, reflecting 16% growth, and operates 66 production sites globally with strong expansion in South America and Asia. BYK is scaling its Cubic Ink portfolio, including advanced UV-curing resins for industrial 3D printing and packaging inks recognized with the 2025 ALTANA Innovation Award. With approximately 7% of annual sales allocated to research and development, the division is advancing digital-specific surfactants that enhance dot sharpness, pigment wetting, and high-resolution inkjet performance while reducing formulation carbon intensity.

Evonik Industries AG Expands TEGO Portfolio and Regional Technical Coverage

Evonik Industries AG maintains leadership in specialty silica and surfactant-based ink additives, particularly under its TEGO brand. In February 2026, the company announced a restructuring of its North American distribution network to deepen technical coverage and improve responsiveness for coatings and printing ink customers. The TEGO Dispers 695 additive is engineered to optimize pigment stabilization in premium inkjet and flexographic ink systems, enhancing color strength and long-term dispersion stability. Evonik is actively promoting its TEGO eCO portfolio, which incorporates mass-balanced renewable raw materials to reduce product carbon footprint in industrial ink formulations. Its 2026 localization strategy in Asia includes new specialty facilities and regional innovation hubs to serve high-growth packaging markets in India and China, strengthening technical collaboration with converters and brand owners.

BASF SE Leverages Dispersion Technology and Sustainable Resin Transparency

BASF SE sustains cost and scale advantages in ink-relevant dispersions and acrylic resin technology through its integrated Verbund production infrastructure. On March 2, 2026, the company implemented price increases of up to $100 per metric ton for butyl acrylate and 2-ethylhexyl acrylate in Asia-Pacific, reflecting feedstock and energy cost pressures impacting ink binder systems. In February 2026, BASF expanded dispersions capacity at its Mangalore, India facility to support paper and flexible packaging ink manufacturers. Its VALERAS portfolio enhances sustainability transparency by documenting environmental performance across Acronal and Basonal resin systems. With a projected 2026 adjusted EBITDA between €6.2 billion and €7.0 billion, BASF is prioritizing high-margin industrial solutions and next-generation waterborne acrylic dispersions tailored for low-VOC ink applications.

Dow Inc. Accelerates Silicone Surface Modifier Innovation

Dow Inc. is executing its Transform to Outperform roadmap to improve profitability and simplify operations across its materials science portfolio, targeting $2 billion in near-term operating EBITDA improvements by 2028. The company operates in 29 countries with approximately 34,600 employees and aims for a $500 million in-year EBITDA uplift in 2026. Dow holds a strong position in silicone-based surface modifiers, with DOWSIL additives widely used to control slip, foam, mar resistance, and leveling in UV-curable and flexographic ink systems. Following recognition for earning the most Edison Awards in the industry for eight consecutive years, Dow is directing 2026 investments toward REVOLOOP recycled plastic resins and sustainable solvent-borne technologies. Its focus on silicone chemistry and formulation control supports high-speed printing stability and improved surface aesthetics in packaging and commercial print applications.

Lubrizol Corporation Strengthens Hyperdispersant and PFAS-Free Portfolio

Lubrizol Corporation, a Berkshire Hathaway company, is advancing polymer engineering solutions for inkjet, textile, and industrial printing markets. At the American Coatings Show 2026, the company presented its updated One Lubrizol identity alongside 100% active polymeric dispersants designed to enhance pigment dispersion efficiency. Its Solsperse Hyperdispersants and Diamond Dispersions lines are critical for stabilizing nano-sized pigments in digital textile inks and high-resolution card and paper printing. Lubrizol’s 2026 PTFE-free transition strategy introduces advanced wax additives that deliver surface protection and abrasion resistance without fluorinated materials, aligning with tightening global PFAS regulations. The opening of a new office in Bangkok supports local-for-local growth across Southeast Asia’s expanding digital print and industrial coatings markets, reinforcing regional technical support capabilities.

Clariant Drives Margin Expansion Through Circular Additive Solutions

Clariant continues to enhance profitability in the ink additives market through portfolio optimization and sustainability-driven innovation. The company achieved a 42% free cash flow conversion in 2025 and projects a 2026 EBITDA margin near 18% before exceptional items. Its Adsorbents and Additives business unit is targeting growth in coatings and adhesives applications across EMEA and APAC, emphasizing material circularity and bio-based feedstock integration. Clariant aims to reduce Scope 1 and Scope 2 emissions by 46.9% by 2030, with 2026 marking the rollout of new renewable raw material frameworks for industrial additives. Operational efficiency programs delivered CHF 50 million in savings during 2025, with an additional CHF 30 million expected in 2026, reinforcing resilience amid volatile raw material markets and supporting sustainable dispersant and rheology modifier development.

United States Ink Additives Market: Stability-Driven Capacity, Low-VOC Compliance, and Digital Print Acceleration

The United States ink additives industry is being reshaped by durability requirements, tightening VOC regulation, and the rapid scaling of digital printing platforms. In March 2025, BASF announced a major expansion of aminic antioxidant capacity at its Puebla site serving the North American corridor. Scheduled for completion in 2026, the investment responds to rising demand for high-stability additives used in industrial inks, where oxidative resistance and color integrity are essential for long production runs and extended shelf life. This capacity build aligns with broader formulation shifts as U.S. producers redesign ink systems to withstand higher shear, faster curing, and more aggressive substrates.

Regulatory pressure is accelerating reformulation across the sector. To exceed updated EPA Lowest Additive Concentration thresholds and meet 2026 enforcement phases targeting a 20% VOC reduction in commercial printing, U.S. formulators are rapidly adopting bio-based surfactants and low-emission dispersants. Innovation is extending beyond compliance. In late 2025, Afton Chemical launched the HiTEC 35701 series, introducing solvent-additive packages designed for electric vehicle component marking inks that require copper protection and dielectric stability in both liquid and vapor phases. Digital printing is another growth vector. Lubrizol released the Noverite GP250B rheology modifier in 2025, engineered for high-shear industrial inkjet heads to enable faster throughput in e-commerce packaging. Sustainability is reinforcing differentiation as Clariant opened an Innovation Center in Charlotte to develop PFAS and PTFE-free texturing agents ahead of 2026 state-level restrictions, while federal antimicrobial packaging guidance for 2025–2026 has increased adoption of silver-ion and copper-based additives in food-grade inks for high-traffic logistics environments.

China Ink Additives Market: Policy-Led Upgrading, Standards Enforcement, and Smart Manufacturing

China’s ink additives industry is advancing through state-directed upgrading, environmental standards, and digitally enabled production ecosystems. Under the MIIT petrochemical work plan for 2025–2026, the chemical sector is targeted for sustained value growth, with explicit direction to upgrade traditional products into high-end electronic chemicals and advanced ink additives. This policy emphasis is driving investment toward dispersants, wetting agents, and defoamers that meet the performance needs of electronics, packaging, and specialty printing applications.

Regulatory enforcement is tightening timelines. From June 1, 2026, GB 30981.1-2025 will impose stricter limits on harmful substances in industrial coatings and inks, pushing manufacturers toward water-soluble and high-solid additive systems. Strategic collaboration is supporting this transition. Heubach and Evonik finalized a partnership during 2024–2025 to develop eco-friendly gel solutions tailored to regulatory expectations in the Pearl River Delta. Supply chain dynamics are also shifting. Export controls introduced in April 2025 on samarium, gadolinium, and terbium have affected availability of rare-earth inputs for magnetic and security ink additives, prompting reformulation and sourcing realignment. At the same time, BASF is scaling methyl glycol and glycol ether production at the Zhanjiang Verbund site to stabilize supply of high-efficiency wetting agents. By 2026, major chemical parks in Anhui and Guangdong are implementing AI-enabled Smart Park initiatives, using real-time IoT monitoring to cut the carbon intensity of surfactant and defoamer production by approximately 15%.

Germany Ink Additives Market: Mass-Balanced Sustainability and High-Performance Specialties

Germany’s ink additives landscape is defined by certified sustainability, advanced stabilization chemistries, and premium specialty materials. In March 2025, Evonik Coating Additives introduced mass-balanced products TEGO Wet 270 eCO and TEGO Foamex 812 eCO, produced with ISCC PLUS certified raw materials. These additives enable printers and converters to lower Scope 3 emissions while maintaining identical wetting and defoaming performance, supporting compliance with European sustainability reporting expectations.

Performance innovation remains a parallel priority. BASF is preparing to showcase the next evolution of its VALERAS platform at K 2025, highlighting HALS solutions that protect industrial prints from extreme UV exposure and chemical stress in agrochemical packaging. Decarbonization milestones are reinforcing Germany’s leadership position. The ALTANA Group, including its BYK additives business, is on track to achieve CO2 neutrality in Scope 1 and 2 operations by the end of 2025 through expanded renewable electricity and photovoltaic capacity. Specialty applications are also expanding. Cubic Ink scaled production of UV-curing resins in 2025 for medical technology and audiology, with materials such as Mold 3100 VP meeting stringent cytotoxicity requirements. These developments position Germany as a hub for sustainable, high-performance ink additive innovation.

Ink Additives Industry: Country-Level Strategic Snapshot

Ink Additives Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Core Additive Focus

|

Structural Direction

|

|

United States

|

Low-VOC regulation and digital print growth

|

Antioxidants, rheology modifiers, PFAS-free texturing

|

Stability and compliance-led reformulation

|

|

China

|

Policy-driven upgrading and standards enforcement

|

Water-based dispersants, wetting agents

|

Value-added transition with smart manufacturing

|

|

Germany

|

Certified sustainability and specialty performance

|

Mass-balanced additives, HALS, UV-curing resins

|

Low-carbon, high-margin innovation

|

Ink Additives Market Report Scope

Ink Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.9 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Additive Type (Dispersing and Wetting Agents, Rheology Modifiers, Foam Control Additives, Slip and Rub Materials, Driers, Specialty Additives), By Technology (Water-Based, Solvent-Based, UV-Cured, Digital and Specialty Inks), By Printing Process (Flexography, Gravure, Lithographic and Offset, Digital Inkjet, Screen Printing), By End-Use Industry (Packaging, Publishing, Commercial Printing, Textiles, Industrial and Security Printing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, ALTANA AG, Lubrizol Corporation, Clariant AG, Dow Inc., DIC Corporation, Arkema S.A., Elementis PLC, Ashland Inc., Shamrock Technologies, Münzing Chemie GmbH, Croda International PLC, Toyo Ink SC Holdings, Sakata Inx Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ink Additives Market Segmentation

By Additive Type

- Dispersing and Wetting Agents

- Rheology Modifiers

- Foam Control Additives

- Slip and Rub Materials

- Driers

- Specialty Additives

By Technology

- Water-Based

- Solvent-Based

- UV-Cured

- Digital and Specialty Inks

By Printing Process

- Flexography

- Gravure

- Lithographic and Offset

- Digital Inkjet

- Screen Printing

By End-Use Industry

- Packaging

- Publishing

- Commercial Printing

- Textiles

- Industrial and Security Printing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ink Additives Industry

- BASF SE

- Evonik Industries AG

- ALTANA AG

- Lubrizol Corporation

- Clariant AG

- Dow Inc.

- DIC Corporation

- Arkema S.A.

- Elementis PLC

- Ashland Inc.

- Shamrock Technologies

- Münzing Chemie GmbH

- Croda International PLC

- Toyo Ink SC Holdings

- Sakata Inx Corporation

*- List not Exhaustive