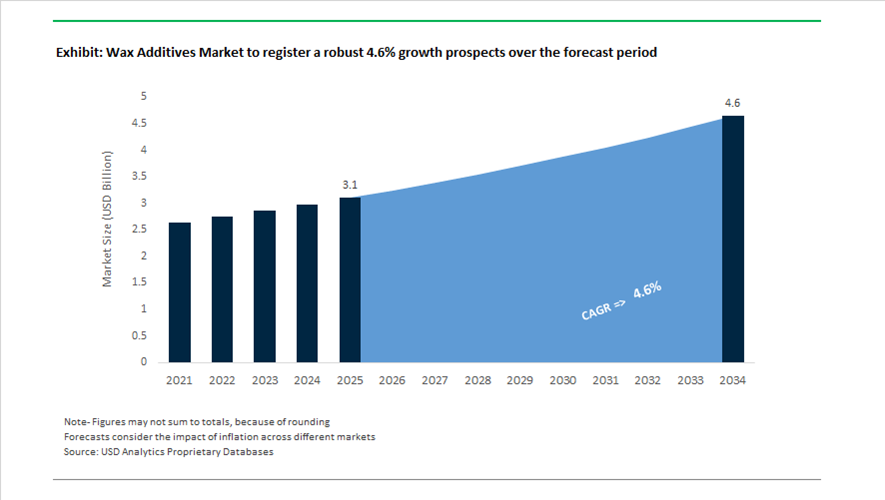

Wax Additives Market Overview 2025–2034: $3.1 Billion to $4.6 Billion at 4.6% CAGR Anchored in PFAS-Free Surface Modifiers and Bio-Attributed Polyethylene Waxes

The Wax Additives market is valued at $3.1 billion in 2025 and is projected to reach $4.6 billion by 2034, expanding at a CAGR of 4.6%. Demand is driven by the need for surface modifiers, slip agents, matting additives, scratch-resistant coatings, processing aids for engineering plastics, and rheology-modifying wax dispersions across paints, inks, adhesives, sealants, and polymer compounding. Regulatory pressure targeting fluorinated chemistries and “forever chemicals” is accelerating the transition toward PTFE-free, PFAS-free, renewable, and bio-attributed wax additives. At the same time, growth in e-mobility, advanced packaging, and aerospace sealants is reinforcing demand for high-performance polyethylene waxes, polybutadiene modifiers, and specialty wax emulsions.

In 2024, R&D investments and portfolio repositioning intensified. In November 2024, Mitsui Chemicals completed its Creative Integration Lab in Japan, a dedicated innovation hub focused on circular materials including mass-balance sourced Prasus™ bio-attributed polyethylene waxes. Throughout 2024 and late 2025, Lubrizol expanded its Lanco™ surface modifier portfolio, introducing PTFE-free wax additives that replicate fluoropolymer-level scratch and rub resistance in wood and powder coatings. These formulations address tightening global restrictions on fluorinated additives while maintaining abrasion resistance and texture control in architectural and industrial coatings. In January 2025, Evonik highlighted expansion of its COMB-polymers platform, viscosity modifiers engineered to interact with base oil wax fractions to improve fuel economy in automotive lubricants, targeting €100 million in mid-term sales in Asia.

Strategic consolidation reshaped competitive positioning in 2025. In March 2025, Sudarshan Chemical finalized its acquisition of the Heubach Group, integrating wax-based pigment preparations and dispersants into a broadened additives portfolio for coatings and inks. In October 2025, Honeywell completed the spin-off of its Advanced Materials division into Solstice Advanced Materials, forming an independent specialty chemical company managing industrial-grade wax additives and fluorine-related materials. That same month, Clariant announced capacity expansion at its Daya Bay site in China, supporting additive portfolios used in e-mobility applications where wax processing aids are critical for injection-molded battery housings and electrical components. In 2025, Evonik established Shanghai production for POLYVEST® ST-E 60, enhancing regional supply of polybutadiene-based additives used to improve moisture barrier performance and electrical insulation in coatings and adhesives.

Product innovation accelerated into 2026 with a clear sustainability orientation. In February 2026, Clariant showcased Licocare RBW Vita at PaintIndia, a renewable rice bran wax derivative delivering slip and matting effects with a reduced carbon footprint compared with petroleum-based waxes. Clariant also introduced Ceridust 8170 M, a PFAS/PTFE-free additive for powder coatings designed to create fine textures while meeting emerging environmental safety standards. In January 2026, Mitsui Chemicals consolidated marketing of high-performance resins through Polyplastics, enabling focus on core polyethylene wax R&D and global distribution optimization. In February 2026, Evonik announced plans for new hydroxyl-terminated polybutadiene production in Asia, strengthening supply chains for wax-compatible additives used in aerospace sealants and advanced elastomer systems.

The wax additives market is advancing toward bio-based polyethylene waxes, fluorine-free surface modifiers, renewable rice bran wax derivatives, high-performance polybutadienes, and e-mobility processing aids. Coatings durability enhancement, sustainable polymer processing, fuel-efficiency lubricants, and advanced adhesive systems remain the primary demand pillars supporting steady expansion through 2034.

Trends and Opportunities in the Wax Additives Market

Trend 1: Strategic Enablement of Waterborne Systems for Industrial Coatings

The global transition toward waterborne industrial coatings has created a critical performance gap that advanced wax additives are now required to close. As OEMs eliminate solvent-based basecoats to reduce hazardous air pollutants and meet tightening VOC regulations, wax additives play a decisive role in delivering surface protection, slip, and abrasion resistance without compromising optical clarity.

In early 2025, Shamrock Technologies expanded its BioSLIP® micronized wax portfolio specifically for waterborne industrial and coil coatings. These bio-based wax additives are engineered to deliver mar and scratch resistance comparable to solvent systems while maintaining high gloss retention, a requirement for automotive interior trims and metal packaging applications. This directly addresses a long-standing barrier to full waterborne adoption in high-wear industrial environments.

In parallel, tire and rubber manufacturers across Asia are accelerating the replacement of paraffin waxes with Fischer-Tropsch waxes. Technical performance data published in late 2024 confirms that FT waxes exhibit superior oxidation stability and reduced migration under thermal cycling. This significantly improves ozone crack resistance and extends tire service life, making FT wax additives a strategic input for premium and electric vehicle tire formulations where durability expectations are materially higher.

Trend 2: Transition to Bio-Based and Circular Feedstock Waxes

Sustainability mandates from multinational brand owners are forcing wax additive suppliers to decouple from petroleum feedstocks and demonstrate measurable carbon footprint reductions. This has accelerated commercial scaling of waxes derived from agricultural by-products and renewable biomass.

In October 2024, Clariant highlighted its Licocare RBW Vita rice bran wax range, which delivers a Renewable Carbon Index above 98% and achieves up to 80% lower carbon footprint compared to fossil-based montan waxes. These wax additives retain high hardness and gloss performance, allowing coatings and plastics manufacturers to meet Scope 3 emissions targets without sacrificing surface durability or processing stability.

Further reinforcing this shift, Arkema introduced a new generation of bio-based specialty additives in April 2025, including wax dispersions integrated with bio-sourced acrylic technologies. Derived from sugarcane and beetroot biomass, these wax systems enable architectural and industrial coating formulators to reduce Product Carbon Footprint while preserving anti-blocking behavior, rheology control, and film integrity. This trend signals that bio-based wax additives are moving from niche sustainability claims into mainstream industrial qualification.

Opportunity 1: High-Performance Wax Additives for Compostable Flexible Packaging

Global regulatory and brand commitments to fully recyclable or compostable packaging are creating a high-value opportunity for wax additives that deliver barrier performance without disrupting biodegradation pathways. Traditional fluorinated or high-molecular-weight waxes are increasingly disqualified under updated certification standards.

In 2025, compostability certification bodies mandated wax-coated papers and biopolymers to contain less than 100 ppm total fluorine and achieve over 90% disintegration in commercial composting environments. This has driven rapid adoption of fully linear, low-molecular-weight bio-based waxes that maintain grease resistance and water vapor barriers while remaining compostable. Empirical studies show that beeswax-based and similar bio-wax coatings can improve barrier performance by approximately 77% versus uncoated substrates.

Beyond packaging, bio-based wax nanoemulsions are gaining traction as edible and antimicrobial barrier coatings. Research published in September 2024 demonstrates that wax nanoemulsions with particle sizes between 20 and 200 nanometers enhance shelf life of perishable foods by combining moisture control with antimicrobial functionality. This positions wax additives as central components in plastic-free food preservation systems.

Opportunity 2: Specialized Processing Aids for Industrial Additive Manufacturing

Additive manufacturing is emerging as a structurally attractive growth segment for specialty wax additives, particularly in polymer extrusion and precision casting workflows. In 3D printing filaments, wax additives are increasingly specified as multifunctional processing aids rather than simple lubricants.

Industrial benchmarks released in May 2025 confirm that polypropylene wax additives reduce melt-phase internal friction during filament extrusion, resulting in more stable flow, improved dimensional accuracy, and approximately 20% reduction in surface defects. Additionally, these waxes act as nucleating agents, reducing shrinkage and warping during cooling, a persistent challenge in large-format and high-precision prints.

In aerospace and medical casting applications, wax-polymer hybrid filaments are gaining adoption for lost-wax investment casting. Additive manufacturing briefings from 2024 show that specialized wax formulations enable residue-free burnout, reducing post-processing labor by up to 50% and significantly improving dimensional accuracy of titanium and high-performance alloy components. This positions wax additives as enablers of scalable, high-tolerance additive manufacturing rather than consumable auxiliaries.

Wax Additives Market Share and Segmentation Insights

Product Type Market Share: Synthetic Waxes Lead with Tailored Performance and Micronization Advances

Synthetic waxes dominate the wax additives market with a 42.80% share in 2025, supported by their engineered properties, consistent quality, and versatility across coatings, inks, and plastics applications. Polyethylene, polypropylene, and Fischer Tropsch waxes provide controlled slip, abrasion resistance, and surface protection. Petroleum-based, natural, and semisynthetic waxes serve additional formulation needs with varying cost and performance profiles. A key trend is the advancement of micronized synthetic waxes, where controlled particle sizes in the 5 to 20 micron range enable improved surface uniformity, enhanced scratch resistance, and optimized dispersion without compromising transparency in high-performance formulations.

Application Market Share: Paints and Coatings Lead with Surface Performance and Waterborne Compatibility

Paints and coatings account for 42.80% of the wax additives market in 2025, driven by the need for enhanced surface properties such as slip resistance, matting, scratch resistance, and water repellency in architectural, industrial, and automotive coatings. Printing inks, plastics, adhesives, and personal care applications contribute to diversified demand. A key growth driver is the shift toward waterborne coatings, where wax additives are increasingly formulated as aqueous dispersions and emulsions to ensure compatibility with low-VOC systems. This supports performance optimization while aligning with environmental regulations and evolving coating technology requirements.

Wax Additives Market Competitive Landscape

The Wax Additives market in 2026 is defined by formula cleanliness, Product Carbon Footprint optimization, and rapid transition to water-based systems, with bio-based micronized waxes and AI-driven formulation tools enabling sustainable coatings, packaging, and automotive surface modification applications.

Clariant Leads Bio-Based Wax Additives with Food-Contact Approval and PFAS-Free Processing Aids

Clariant AG is advancing leadership in the Wax Additives market through renewable feedstock innovation and regulatory-compliant formulations. Its Licocare RBW rice bran wax series received EU approval for food-contact plastics, supporting sustainable packaging applications in PET, PLA, and PVC. The AddWorks PPA portfolio eliminates PFAS while improving extrusion efficiency by preventing die build-up and surface defects. Operational savings from its performance program are being reinvested into green chemistry R&D for coatings and inks. The company maintains strong financial stability with projected EBITDA margins around 18% in 2026. This focus on bio-based waxes and compliance-driven innovation strengthens its competitive positioning.

Honeywell Expands High-Performance Wax Additives with Industrial Backlog and Polyolefin Expertise

Honeywell International is strengthening its position in the Wax Additives market through advanced polyolefin wax technologies and strong industrial demand. Its Titan™ and A-C® wax additive lines are widely used in coatings, PVC processing, and technical plastics for lubrication and surface enhancement. A record $37 billion backlog supports continued investment in advanced materials and sustainable additives. The A-C® 316 and 307 series remain benchmarks for high-speed processing and equipment protection. Strategic portfolio restructuring, including the Aerospace spin-off, enables focused growth in specialty additives. This combination of scale, performance, and financial strength reinforces Honeywell’s market presence.

BASF Strengthens Integrated Wax Additives Supply with Verbund Efficiency and Portfolio Optimization

BASF SE is reinforcing its role in the Wax Additives market through integrated production and strategic portfolio restructuring. The Zhanjiang Verbund site provides a cost-efficient base for producing wax dispersion precursors, improving supply chain resilience in Asia-Pacific. The separation of its coatings business allows BASF to focus on upstream additive chemistry while maintaining downstream exposure. Cost reduction initiatives exceeding €2.3 billion support profitability amid volatile raw material markets. The Industrial Solutions segment is expected to see earnings growth driven by demand in automotive and electronics sectors. This integrated approach enhances BASF’s competitiveness in high-performance wax additives.

Lubrizol Accelerates Water-Based Wax Dispersion Innovation with High-Solids and Digital Formulation Tools

Lubrizol Corporation is advancing in the Wax Additives market through high-solids dispersions and digital formulation optimization. The Lanco™ Glidd series enables water-based coatings to achieve solvent-like mar and rub resistance without VOC emissions. Expansion of its Shanghai Film Center supports automotive applications such as paint protection films with enhanced durability and self-healing properties. Bio-based polymer innovations are being adapted for eco-friendly coating formulations. Its Decision Science platform reduces formulation development time by up to 40% through predictive modeling. This focus on waterborne performance and digital tools strengthens Lubrizol’s position in sustainable coatings.

Mitsui Chemicals Drives Specialty Wax Innovation with Metallocene Catalysis and Bio-Attributed Grades

Mitsui Chemicals is strengthening its competitive position in the Wax Additives market through specialty wax innovation and portfolio transformation. Its Hi-Wax™ series supports polyurethane processing and high-performance coating applications with superior thermal stability. Capacity expansion at Yeosu enhances supply for polyurethane systems and downstream additive demand. The company is introducing ISCC PLUS-certified bio-attributed waxes to meet global circular economy requirements. Its strategic shift toward specialty chemicals focuses on ICT and mobility applications. Proprietary metallocene catalysis enables precise molecular control, delivering enhanced transparency and heat resistance in advanced formulations.

India Wax Additives Market Emerging as a Multi-Segment Growth and Manufacturing Hub

India’s wax additives market is transitioning from fragmented supply to integrated, technology-driven manufacturing, supported by capacity expansion, regulatory tightening, and diversified end-use demand. In March 2025, Gulbrandsen announced a significant expansion at its Dahej facility to add new specialty polyethylene wax capacity alongside a functional polymers plant scheduled to be operational by mid-2026. This investment strengthens India’s position in high-performance wax additives used in coatings, plastics processing, and packaging. Parallel innovation is visible in agri-food applications. In April 2024, the Indian Council of Agricultural Research launched a wax-coating technology for tapioca that extends shelf life to two months, highlighting the growing role of wax additives in post-harvest preservation and food security.

Upstream purity and natural wax supply are also improving. Numaligarh Refinery Limited integrated a 5G captive network into its wax production units by 2025 to optimize paraffin wax purity for food packaging and cosmetics. On the natural wax side, government-backed funding through the National Bee Board enabled the establishment of formal beeswax processing units, supporting clean beauty and pharmaceutical-grade applications. Market reach is expanding internationally. Gandhar Oil Refinery broadened its Divyol brand distribution to more than 100 countries in 2025, leveraging facilities in Western India and Sharjah. Regulatory discipline is tightening further. The Bureau of Indian Standards has introduced stricter benchmarks for personal care waxes, compelling domestic producers to invest in advanced purification ahead of 2026 compliance deadlines.

China Wax Additives Market Driven by Water-Based Systems and Automotive Innovation

China’s wax additives market is being reshaped by large-scale chemical investments, environmental mandates, and advanced mobility requirements. In late 2025, BASF reached mechanical completion of its acrylics complex at the Zhanjiang Verbund site, establishing a core Asian production hub for high-performance water-based Joncryl wax emulsions serving packaging and paper applications. This localized capacity supports China’s shift toward low-VOC, aqueous formulations under tightening green manufacturing policies.

Innovation intensity remains high. At CHINACOAT 2025 in Shanghai, domestic and international suppliers unveiled radar-transparent metallic wax dispersions designed to ensure compatibility with autonomous vehicle sensors, signaling the convergence of wax additives with advanced driver-assistance technologies. Regulatory pressure is accelerating structural change. Under the 14th Five-Year Plan, China’s 2026 VOC emission standards are driving furniture and leather clusters in Zhejiang to replace solvent-borne wax pastes with aqueous dispersions. Supply chain resilience is also being addressed. Nippon Seiro announced strategic partnerships with Chinese producers to stabilize access to high-melting-point Fischer–Tropsch waxes, reinforcing China’s role as both a consumption and synthesis center for performance wax additives.

Germany Wax Additives Market Focused on Sustainability and Functional Performance

Germany’s wax additives market is increasingly defined by sustainability-led innovation and high-value applications rather than commodity volumes. At the K 2025 trade fair in Düsseldorf, German chemical leaders showcased the evolution of the VALERAS platform, highlighting wax additives engineered to enable mechanical recycling of multilayer plastics. These solutions address circular economy objectives by improving processability and surface properties of recycled polymers.

Regulatory alignment is reshaping formulations. By 2025, German manufacturers completed the phase-out of PTFE-based wax blends, replacing them with micronized polyethylene waxes that deliver comparable slip and abrasion resistance without fluorinated chemistries. Industry restructuring has also altered the competitive landscape. The 2024–2025 insolvency and acquisition of Heubach Group by Sudarshan led to a realignment of specialized pigment–wax masterbatch production in Germany, now focused on premium automotive and architectural coatings. Investment in advanced functionality continues. Altana, through its ECKART division, secured European Investment Bank financing in late 2025 to expand R&D into wax-based effect pigments that enhance durability and weather resistance of sustainable coatings.

United States Wax Additives Market Anchored in Electronics, Coatings, and Regulatory Compliance

The United States wax additives market is benefiting from innovation in water-based systems, semiconductor expansion, and stringent food-contact regulations. In 2025, Honeywell expanded its A-C Performance Additives portfolio with low-density polyethylene copolymers designed for water-based floor polishes, delivering high gloss and color stability without yellowing. These developments align with growing demand for non-solvent, low-odor maintenance products.

Electronics manufacturing is adding a high-purity demand layer. The expansion of semiconductor fabrication under the CHIPS Act during 2025–2026 has increased consumption of ultra-pure wax additives in photoresists and electronic-grade adhesives. Coatings applications remain strong. AkzoNobel completed a $55 million expansion of its High Point, North Carolina wood coatings campus, deploying wax-enhanced matting agents for premium furniture finishes. Regulatory compliance continues to shape product development. In 2025, BASF introduced Joncryl Wax 30 to the U.S. market as a food-contact-compliant solution meeting FDA 21 CFR requirements, enabling converters to replace reclassified components without compromising performance.

Summary of Country-Level Wax Additives Market Dynamics

Wax Additives Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Application Focus

|

Strategic Market Position

|

|

India

|

Capacity expansion and regulatory tightening

|

Coatings, food preservation, personal care

|

Global manufacturing and export hub

|

|

China

|

Green manufacturing and automotive innovation

|

Packaging, NEV coatings, furniture

|

Scale-driven innovation market

|

|

Germany

|

Sustainability and recycling enablement

|

Automotive, architectural coatings

|

High-value functional technology leader

|

|

United States

|

Electronics expansion and water-based coatings

|

Semiconductors, floor and wood coatings

|

Innovation-led, compliance-focused market

|

Wax Additives Market Report Scope

Wax Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Synthetic Waxes, Natural Waxes, Petroleum-Based Waxes, Semisynthetic Waxes), By Form (Micronized Wax, Aqueous Dispersions and Emulsions, Solvent-Based Dispersions, Solid and Pastille), By Functionality (Slip and Rub Resistance, Matting and Gloss Control, Anti-Blocking and Surface Protection, Rheology Modification, Wetting and Dispersing), By Application (Paints and Coatings, Printing Inks, Plastics and Rubber, Adhesives, Personal Care and Cosmetics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Clariant AG, Honeywell International Inc., The Lubrizol Corporation, Mitsui Chemicals Inc., Solenis, Evonik Industries AG, Altana AG, Sudarshan Chemical Industries Limited, Sasol Limited, Exxon Mobil Corporation, Nippon Seiro Co. Ltd., Micro Powders Inc., Petróleo Brasileiro S.A., Sinopec Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wax Additives Market Segmentation

By Product Type

- Synthetic Waxes

- Polyethylene Waxes

- Polypropylene Waxes

- Fischer–Tropsch Waxes

- Amide Waxes

- Natural Waxes

- Petroleum-Based Waxes

- Semisynthetic Waxes

By Form

- Micronized Wax

- Aqueous Dispersions and Emulsions

- Solvent-Based Dispersions

- Solid and Pastille

By Functionality

- Slip and Rub Resistance

- Matting and Gloss Control

- Anti-Blocking and Surface Protection

- Rheology Modification

- Wetting and Dispersing

By Application

- Paints and Coatings

- Printing Inks

- Plastics and Rubber

- Adhesives

- Personal Care and Cosmetics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Wax Additives Market

- BASF SE

- Clariant AG

- Honeywell International Inc.

- The Lubrizol Corporation

- Mitsui Chemicals Inc.

- Solenis

- Evonik Industries AG

- Altana AG

- Sudarshan Chemical Industries Limited

- Sasol Limited

- Exxon Mobil Corporation

- Nippon Seiro Co. Ltd.

- Micro Powders Inc.

- Petróleo Brasileiro S.A.

- Sinopec Group

*- List not Exhaustive