Triclosan Market Overview 2025–2034: $88.4 Million to $129.1 Million at 4.3% CAGR Amid Regulatory Contraction and Medical-Grade Realignment

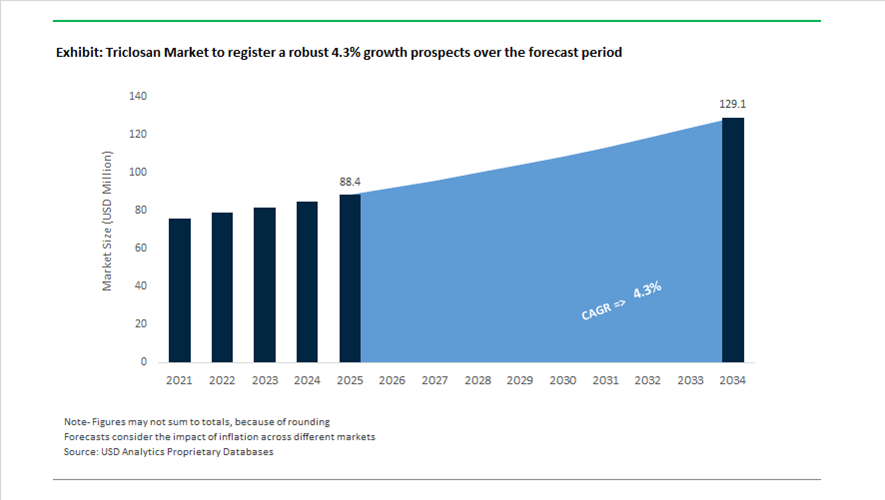

The global Triclosan market is valued at $88.4 million in 2025 and is projected to reach $129.1 million by 2034, expanding at a CAGR of 4.3%. Triclosan, a broad-spectrum antimicrobial agent widely used in oral care products, surgical sutures, antiseptic gels, plastic additives, and industrial coatings, is undergoing structural transformation driven by tightening cosmetic regulations and a strategic pivot toward medical-grade and industrial applications. The market is increasingly segmented between highly regulated consumer formulations and comparatively resilient pharmaceutical, healthcare, and polymer additive uses. Growth through 2034 is expected to be concentrated in surgical infection control, antimicrobial materials for durable plastics, and specialty industrial coatings rather than mass-market personal care.

Regulatory compression in consumer cosmetics accelerated between 2024 and 2025. Under Regulation (EU) 2024/996, new concentration limits capped Triclosan at 0.3% in toothpastes, soaps, and deodorants. As of December 2024, non-compliant products could no longer be placed on the EU market, with a final sell-off deadline of October 2025. In early 2025, European toothpaste manufacturers were mandated to update packaging with a warning restricting use in children under three years of age. During 2024 and 2025, several jurisdictions aligned their cosmetic ingredient hotlists with EU standards, requiring cessation of production and distribution of Triclosan-containing cosmetics in certain emerging markets by January 2026. By mid-2025, major suppliers including Vivimed Labs and Cayman Chemical reported R&D realignment toward naturally derived antimicrobial alternatives to address increasing clean-label demand and regulatory scrutiny. In August 2025, Kumar Organic Products updated its technical dossier for Triclosan 5000, emphasizing compliance with revised global purity thresholds and reinforcing its positioning in regulated oral care applications.

Medical and pharmaceutical-grade applications remain comparatively stable and are driving incremental value capture. In September 2024, Johnson & Johnson Services launched its ETHICON Plus suture portfolio featuring enhanced antimicrobial coatings designed to reduce surgical site infections in high-risk procedures. In January 2025, B. Braun SE acquired a European med-tech startup focused on sensor-integrated smart sutures, technologies that frequently incorporate antimicrobial coatings historically based on Triclosan chemistry. Throughout 2025, pharmaceutical manufacturers expanded output of Triclosan-based surgical hand scrubs and antiseptic gels, where regulatory allowances differ from consumer soap bans. Industrial repositioning is also evident. In February 2026 at Plastindia, BASF highlighted antimicrobial additives for long-life plastics and plasticulture applications, where Triclosan derivatives are used to inhibit fungal degradation in agricultural films and durable polymers. In January 2026, Kumar Organic Products showcased its antimicrobial portfolio at HPCI India, signaling a strategic shift toward industrial coatings and medical-grade segments. Meanwhile, Vantage Specialty Chemicals initiated financial restructuring in September 2025 and filed trade cases in January 2026, indicating broader capital reallocation away from commodity antimicrobial agents toward core surfactant and bio-based chemistries.

Regulatory Exit, Clinical Concentration, and Post-Triclosan Innovation Pathways in the Triclosan Market

Regulatory Sunset Accelerates the Structural Exit of Triclosan from Consumer Goods

The Triclosan market has entered an irreversible contraction phase in consumer-facing applications, driven by synchronized regulatory enforcement rather than voluntary reformulation. While the U.S. FDA’s 2016 ban removed triclosan from soaps, 2025 represents the decisive inflection point for Europe and the United Kingdom. Under Commission Regulation (EU) 2024/996, a hard compliance deadline of October 31, 2025 now applies, prohibiting the continued sale of cosmetic products containing triclosan unless they meet highly restrictive Annex V conditions. Critically, this mandate applies retroactively to products placed on the market before December 31, 2024, forcing brand owners and private-label manufacturers to fully liquidate or destroy legacy inventory.

Regulatory audit data from late 2025 confirms the scale of this exit, with triclosan removed from approximately 95% of mainstream toothpaste and mouthwash formulations across North America and Europe. These products have transitioned toward stannous fluoride systems, zinc-based actives, and essential-oil-derived phenols that align with clean-label disclosure requirements and endocrine safety expectations. For chemical suppliers, this has collapsed historical high-volume demand channels, compressing the consumer triclosan market into residual, tightly policed niches while accelerating delisting across retail and mass-market personal care.

Consolidation of Residual Demand into Professional Medical and Surgical Applications

As consumer usage is legislated out, triclosan’s remaining relevance is becoming increasingly concentrated within professional healthcare environments where clinical efficacy, not consumer perception, determines value. Regulatory bodies including the European Chemicals Agency and the U.S. EPA continue to differentiate between high-frequency consumer exposure and controlled, essential clinical use cases. Within these tightly regulated boundaries, triclosan retains a defensible position due to its well-documented 12-hour residual antibacterial activity, a performance benchmark that most botanical alternatives have yet to match under sterile, high-risk conditions.

In 2025, triclosan remains specified in select professional-grade surgical scrubs and healthcare personnel hand rubs used in operating theaters and intensive care units. More strategically, its role in medical device coatings continues to underpin residual market demand. Innovations highlighted in December 2025 emphasize triclosan-impregnated sutures and catheters, particularly for cardiovascular and orthopedic procedures. Clinical outcomes data indicates that such devices can reduce the incidence of Surgical Site Infections by up to 30% in specific applications. While silver ions, antimicrobial peptides, and nanostructured surfaces are gaining traction, triclosan remains a reference compound in non-absorbable sutures due to its predictable release kinetics and long-standing clinical validation.

Opportunity: Rapid Scaling of Green, Botanical, and Peptide-Based Antimicrobials

The regulatory vacuum created by triclosan’s withdrawal has catalyzed one of the most active innovation cycles in antimicrobial chemistry in decades. Investment is flowing into plant-derived phenolics, fermentation-based actives, and bioengineered antimicrobial peptides designed to deliver broad-spectrum efficacy without persistence or endocrine disruption risks. In February 2025, the launch of the $50 million Gram-Negative Antibiotic Discovery Innovator by the Gates Foundation, Novo Nordisk Foundation, and Wellcome underscored the strategic urgency of replacing legacy biocides with safer, resistance-aware alternatives.

This innovation wave is rapidly translating into commercial cosmetic and personal care formulations. In November 2025, Cosphatec introduced Cosphaderm HAP, a nature-identical antimicrobial that combines preservation efficacy with antioxidant benefits and a neutral sensory profile. Such actives directly target the green antimicrobial segment, valued at $4.78 billion in 2025 and expanding at close to 10% annually. Unlike triclosan, these next-generation preservatives are being designed for multifunctionality, enabling brands to simplify ingredient lists while meeting regulatory, sustainability, and consumer transparency requirements simultaneously.

Opportunity: Encapsulated and Non-Leaching Antimicrobials for Industrial Preservation

In industrial applications such as paints, coatings, plastics, and HVAC systems, the replacement of triclosan is not about elimination but containment. Manufacturers now require antimicrobial solutions that deliver long-term protection without environmental leaching, addressing the very pathways that led to triclosan’s regulatory downfall. Advanced encapsulation technologies are emerging as a critical enabler in this transition. In January 2025, Spray-Tek secured a U.S. patent for a biodegradable biopolymer-based core–shell microencapsulation platform that enables controlled release while ensuring the carrier material itself degrades safely.

Parallel to encapsulation, polymer-bound antimicrobials are gaining strategic importance as the EU’s Biocidal Products Regulation undergoes comprehensive review in late 2025. These zero-leach systems chemically anchor antimicrobial functionality to polymer chains, ensuring the active never migrates into water systems. Applications in conveyor belts, HVAC coils, and industrial surfaces are scaling rapidly, as they provide compliance-ready preservation without recurring regulatory risk. For industrial formulators, this marks a shift from additive-based biocides toward structural antimicrobial design, fundamentally redefining how long-term microbial control is achieved in durable goods.

Triclosan Market Share and Segmentation Insights

Grade Market Share: Industrial Grade Leads Amid Regulatory Constraints on Consumer Applications

Industrial grade triclosan dominates the market with a 52.80% share in 2025, driven by its continued use in industrial preservatives, polymer additives, and controlled antimicrobial applications where regulatory restrictions are less stringent. Pharmaceutical and cosmetic grades have experienced declining demand due to tightening regulations on triclosan use in personal care products across major markets. The industry has undergone structural contraction, with production and consumption increasingly concentrated in industrial applications. A key trend is regulatory-driven market realignment, where manufacturers focus on compliant regions and applications, maintaining demand stability in industrial and specialty chemical segments.

Application Market Share: Textiles and Plastics Segment Leads with Antimicrobial Performance Requirements

Textiles and plastics account for 34.80% of the triclosan market in 2025, supported by demand for antimicrobial functionality in consumer and industrial materials. Applications include odor-control textiles, medical fabrics, and antimicrobial-treated plastics used in consumer goods and equipment. Industrial and home care, healthcare and medical, paints and coatings, and personal care segments contribute additional demand, though at reduced levels due to regulatory limitations. A key growth trend is the increasing demand for antimicrobial textiles, particularly in sportswear, workwear, and healthcare environments, where performance benefits such as odor control and microbial resistance sustain triclosan usage despite regulatory pressures.

Triclosan Market Competitive Landscape

The triclosan market in 2026 is shaped by regulatory-compliant, application-specific formulations, with strong emphasis on MoCRA and EU Annex V adherence. Growth is driven by micro-encapsulation technologies enabling controlled-release antimicrobial performance in medical devices, HVAC systems, and industrial coatings where biofilm resistance is critical.

BASF Repositions Toward Industrial Biocides and Low-VOC Antimicrobial Dispersions

BASF is strengthening its position in the triclosan market by pivoting toward industrial-grade antimicrobial solutions aligned with evolving global regulations. The expansion of its dispersion facility in Durban enhances supply of high-performance biocides across EMEA, particularly for coatings and construction applications. Its Tinuvin® and Irgastab® platforms are increasingly integrated with antimicrobial systems to extend polymer durability in harsh environments. BASF’s €6.2–€7.0 billion EBITDA outlook supports continued investment in low-VOC and low-odor antimicrobial dispersions. The company leverages its Verbund integration to ensure consistent supply of high-purity triclosan intermediates. This positions BASF as a reliable partner for industrial antimicrobial formulations requiring regulatory compliance and long-term performance.

Vivimed Labs Focuses on Pharmaceutical-Grade Triclosan and Emerging Market Expansion

Vivimed Labs remains a key global supplier of pharmaceutical-grade triclosan, targeting high-purity applications in surgical scrubs and antiseptic formulations. Its manufacturing infrastructure supports stringent quality requirements for healthcare-grade antimicrobials. The company is actively restructuring its financial profile while expanding exports to Southeast Asia’s growing hygiene market. Vivimed is advancing “Triclosan-Plus” formulations that combine traditional actives with bio-based boosters to optimize efficacy at lower concentrations. Its Hyderabad R&D center plays a central role in developing next-generation antimicrobial blends. The company is also expanding into industrial coatings where triclosan functions as a durable surface biocide for high-contact environments.

Salicylates and Chemicals Strengthens Dual-Track Preservative Strategy with Regulatory-Compliant Triclosan

Salicylates and Chemicals is leveraging a dual-track strategy combining synthetic triclosan with natural preservative systems to address diverse regulatory and consumer demands. Its updated preservative selection guides highlight triclosan’s efficacy against gram-positive and gram-negative bacteria in topical and cosmetic formulations. The company ensures full compliance with EU and APAC standards, including updated safety regulations for consumer products. Its triclosan portfolio is widely used in water-based formulations such as aftershaves and cleansing products to prevent microbial spoilage. Integration of QA documentation and regulatory support enhances its appeal to multinational FMCG clients. The firm continues to position triclosan as a high-performance preservative for heavy-duty antimicrobial applications.

Kumar Organic Expands High-Purity Triclosan for Medical Textiles and Antimicrobial Plastics

Kumar Organic is advancing its leadership in pharmaceutical-grade triclosan through investments in high-purity, low-impurity synthesis technologies. Its products meet stringent dioxin-free requirements demanded by premium cosmetic and healthcare markets. The company is a major supplier for medical textiles and alcohol-free surgical disinfectants, where long-lasting antimicrobial action is critical. Expanded regulatory support enables clients to navigate EPA and global antimicrobial compliance frameworks. Kumar Organic is also scaling triclosan-based masterbatches for plastics, targeting antimicrobial consumer goods such as gym equipment and kitchenware. Its integrated manufacturing and compliance capabilities position it strongly in regulated global markets.

Cayman Chemical Dominates High-Purity Analytical Triclosan for Research and Regulatory Testing

Cayman Chemical leads the analytical and R&D segment by supplying ultra-high-purity triclosan for scientific and regulatory applications. Its ≥98% purity crystalline triclosan is widely used in toxicology and microbiome research, supporting studies across leading academic institutions. The company’s deuterated Triclosan-d3 standard is essential for LC-MS/MS environmental monitoring of wastewater and soil contamination. Nitrogen-packaged formulations ensure chemical stability for sensitive laboratory use. Cayman also supplies reference materials for medical device manufacturers to validate antimicrobial safety under ISO 10993 standards. Its portfolio underpins global research, compliance testing, and pharmaceutical development involving triclosan chemistry.

China Triclosan Market Driven by Scale Economics and Specialty Grade Migration

China remains the world’s primary manufacturing base for triclosan, with 2025 marking a decisive shift from volume-led production toward grade optimization and logistics intelligence. The large-scale capacity expansion completed by Shandong-based producers in early 2025 has consolidated China’s leadership in industrial-grade triclosan used in plastic masterbatches, antimicrobial coatings, and construction additives. At the same time, the Ministry of Industry and Information Technology has embedded triclosan into its 2025–2026 green manufacturing agenda, incentivizing partial substitution of traditional chlorinated phenol pathways with cleaner antimicrobial synthesis routes to reduce halogenated waste streams.

China’s downstream diversification has also widened. Updated late-2025 guidance from the Ministry of Agriculture and Rural Affairs has enabled controlled use of triclosan-based formulations in niche antifungal crop protection, expanding non-cosmetic consumption. On the higher end of the value chain, producers such as Jiangsu Huanxin have scaled 99% plus purity pharmaceutical-grade triclosan for export-oriented medical device coatings in Southeast Asia. Facing U.S. tariff pressure in 2025, Chinese suppliers are increasingly prioritizing low-impurity, application-specific grades and AI-enabled logistics hubs in Shandong, strengthening resilience in European construction and medical equipment supply corridors.

India Triclosan Market Anchored in Healthcare Expansion and Regulatory Convergence

India’s triclosan market trajectory is increasingly shaped by healthcare infrastructure growth and tighter regulatory harmonization. Under the government’s PLI framework for bulk drugs, domestic antimicrobial manufacturers have modernized triclosan production lines to reduce dependence on imported intermediates while improving batch consistency for regulated applications. This capacity upgrade cycle coincides with a ₹25,000 crore public investment push into hospital infrastructure announced in late 2025, which has materially increased demand for triclosan-infused surgical scrubs, antiseptic washes, and controlled clinical hygiene products.

Beyond healthcare, India has emerged as a formulation hub for triclosan-treated technical textiles. In 2025, export-focused mills in the Gujarat–Maharashtra corridor integrated triclosan-based antimicrobial finishes for athletic wear and performance socks supplied to Middle Eastern markets with strict hygiene performance benchmarks. On the regulatory front, India is converging with global norms. The Central Drugs Standard Control Organisation and the Food Safety and Standards Authority of India both tightened triclosan purity and concentration thresholds in 2025–2026, effectively segmenting the market into pharmaceutical-grade, industrial-contact, and textile-grade supply streams.

European Union Triclosan Market Defined by Restriction-Driven Substitution

The European Union represents the most restrictive triclosan regulatory environment globally, with 2025 serving as a structural inflection point rather than a cyclical adjustment. Enforcement of Regulation (EU) 2024/996 from October 2025 has capped triclosan concentration at 0.3% in soaps and toothpastes while mandating explicit warning labels. Simultaneously, the EU-wide ban on triclosan in mouthwash has eliminated an entire consumer-use segment, forcing German and French formulators to pivot toward botanical and enzyme-based antimicrobial alternatives.

This regulatory tightening has been reinforced by the European Chemicals Agency classification of triclosan as an environmental endocrine disruptor, which has accelerated substitution strategies across EU chemical clusters. France’s Law No. 2025-188 has further raised compliance costs by imposing stricter discharge controls on persistent pollutants, compelling remaining triclosan producers to install advanced oxidative wastewater treatment systems. As a result, the EU triclosan market is rapidly contracting toward tightly controlled industrial and legacy healthcare niches rather than consumer-facing applications.

United States Triclosan Market Sustained by Medical Use Amid Policy Pressure

In the United States, triclosan demand persists primarily through regulated healthcare channels, even as consumer applications remain structurally constrained. The Food and Drug Administration continues to prohibit triclosan in consumer hand soaps, but its 2025–2026 review cycle has reaffirmed triclosan’s role in surgical scrubs, preoperative antiseptics, and wound-care formulations where clinical efficacy remains critical. This has preserved a stable, compliance-driven demand base for pharmaceutical-grade triclosan.

However, regulatory scrutiny is intensifying. Implementation of the Modernization of Cosmetics Regulation Act has expanded adverse-event reporting and facility registration obligations, raising compliance costs for manufacturers and brand owners. At the same time, academic toxicity research published in 2025 has influenced state-level policy discourse, particularly in California and New York, around triclosan-free labeling. In response, U.S. specialty chemical firms and antimicrobial technology providers are actively developing nature-inspired and heavy-metal-free alternatives as strategic hedges, signaling that triclosan’s long-term position will remain confined to narrowly defined, medically justified use cases.

Comparative Snapshot: Triclosan Market by Country

Triclosan Market County Level Snapshot

|

Region

|

Primary Demand Driver

|

Regulatory Posture

|

Market Direction

|

|

China

|

Plastics, coatings, medical devices

|

Managed substitution, grade control

|

Scale with specialty-grade pivot

|

|

India

|

Healthcare, technical textiles

|

Alignment with global limits

|

Controlled expansion

|

|

European Union

|

Residual healthcare, industrial legacy

|

Highly restrictive

|

Structural contraction

|

|

United States

|

Surgical antiseptics

|

Tight oversight, selective allowance

|

Stable but policy-sensitive

|

Triclosan Market Report Scope

Triclosan Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$88.4 Million

|

|

Market Size (2034)

|

$129.1 Million

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Grade (Industrial Grade, Pharmaceutical Grade, Cosmetic Grade), By Functionality (Antimicrobial Preservatives, Disinfectants and Sanitizers, Pesticide and Fungicide Agents, Polymer Additives), By Application (Personal Care and Cosmetics, Healthcare and Medical, Industrial and Home Care, Textiles and Plastics, Paints and Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Kumar Organic Products Limited, Jiangsu Huanxin High-Tech Materials Co. Ltd., Vivimed Labs Limited, Shandong Aoyou Biological Technology Co. Ltd., Salicylates and Chemicals Pvt. Ltd., Spectrum Chemical Manufacturing Corp., Merck KGaA, Sino Lion USA Ltd., Cayman Chemical Company, Dev Impex, Xian MEHECO Technology Co. Ltd., Yasho Industries Limited, BOC Sciences, Jiaxing Midas Fine Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Triclosan Market Segmentation

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Cosmetic Grade

By Functionality

By Application

- Personal Care and Cosmetics

- Healthcare and Medical

- Industrial and Home Care

- Textiles and Plastics

- Paints and Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Triclosan Market

- BASF SE

- Kumar Organic Products Limited

- Jiangsu Huanxin High-Tech Materials Co. Ltd.

- Vivimed Labs Limited

- Shandong Aoyou Biological Technology Co. Ltd.

- Salicylates and Chemicals Pvt. Ltd.

- Spectrum Chemical Manufacturing Corp.

- Merck KGaA

- Sino Lion USA Ltd.

- Cayman Chemical Company

- Dev Impex

- Xian MEHECO Technology Co. Ltd.

- Yasho Industries Limited

- BOC Sciences

- Jiaxing Midas Fine Chemical Co. Ltd.

*- List not Exhaustive