Market Overview: Bio-Based QACs, Clean-Label Food Protection, and EU BPR Reformulation Shape Antimicrobial Preservative Market Growth

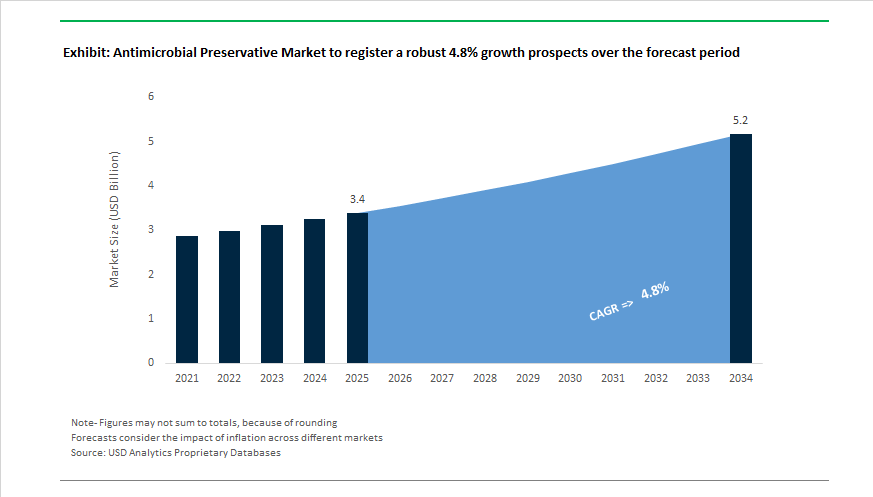

The antimicrobial preservative market stands at $3.4 billion in 2025 and is projected to reach $5.2 billion by 2034, expanding at a 4.8% CAGR. Growth is being driven by the shift toward clean-label preservatives, bio-based antimicrobial agents, multifunctional preservative blends, cosmetic preservation systems, food-grade mold inhibitors, and low-toxicity quaternary ammonium compounds. Demand is rising across personal care formulations, plant-based foods, meat preservation, dairy alternatives, antimicrobial packaging films, and household care products, where manufacturers must balance microbial control with evolving environmental and human-safety standards. Market direction is increasingly influenced by EU Biocidal Products Regulation (BPR) compliance, AMR stewardship policies, botanical preservation chemistry, and reduced reliance on petroleum-derived phenolics.

Sustainability-led chemistry transformation began gaining industrial momentum in March 2024 when Dow and SABIC formed a collaboration to commercialize bio-based preservatives for cosmetics and home care using renewable feedstocks. In January 2024, Kobo Products launched PreservEssence, a 100% plant-derived multifunctional preservative system combining antimicrobial efficacy with skin-conditioning properties. During 2024, Ashland introduced Rokonsal J, a synergistic preservative platform designed to reduce active dosage levels through booster technologies. The same year, Brenntag strengthened its natural antimicrobial portfolio by acquiring Kemin’s food preservation business, expanding distribution of natural antioxidants and mold inhibitors across Europe and North America. DuPont introduced the plant-based SafeShield range in 2024, targeting meat and poultry processors seeking alternatives to synthetic benzoates and nitrites.

Regulatory and market modernization accelerated in April 2025 when BASF received EU approval for Myrtec MX, a natural-origin cosmetic preservative system aligned with the clean beauty movement. In March 2025, Kerry Group launched a botanical preservative platform for plant-based dairy alternatives. Packaging and preservation technologies converged in May 2025 when Amcor completed its merger with Berry Global, strengthening antimicrobial film capabilities for shelf-life extension. India’s National Action Plan on AMR 2.0 launched in November 2025, introducing stricter labeling and regulatory oversight for antimicrobial agents. In February 2026, startup OleQuat unveiled next-generation olefinic QACs with improved biodegradation and lower aquatic toxicity. BioVeritas confirmed plans in 2025 to commission its commercial upcycling plant by 2026, producing biomass-derived mold inhibitors for bakery and meat applications. EU implementation of updated BPR purity standards in 2025 further drove reformulation across isothiazolinone-based systems, pushing manufacturers toward low-migration, eco-friendly antimicrobial preservative technologies.

Trends and Opportunities Reshaping Commercial Adoption and Regulatory Strategy in the Antimicrobial Preservative Market

Regulatory Phase-Out of Legacy Preservatives Restructuring Product Portfolios

Regulatory tightening is no longer limited to maximum allowable content. Entire molecule classes are being removed from market eligibility, forcing immediate reformulation cycles across personal care, home care, pharmaceuticals, and industrial process chemicals. Under EU Regulation 2024/996, cosmetics linked to Annex II banned lists cannot be sold in the EU after May 1, 2025, and substances such as Triclosan and Triclocarban face full withdrawal from most personal care formulas by October 31, 2025.

In the United States, the FDA MoCRA framework has rewritten compliance expectations. Rather than relying on historical toxicology exemptions, brands must demonstrate “reasonable certainty of no harm”, which has driven a surge of 20% more stability and challenge testing for formulas containing Propylparaben, Butylparaben, and phenolic preservatives. At the same time, supply chains are responding to mitigation technologies that eliminate consumer-exposed biocides. LANXESS Klarix XIT, for example, enables use of CIT/MIT only during manufacturing, then chemically neutralizes residues to zero before product finishing. This changes the preservative cost model and prolongs the lifecycle of certain legacy actives.

Preservative-Free Marketing Shifting Into Multi-Functional Protection Systems

A central shift is that preservation is being embedded into multi-functional ingredient systems rather than positioned as a standalone additive. This aligns with Clean Beauty but is now backed by performance data and renewable carbon accountability. Formulation strategies are increasingly relying on glycol-boosted systems (Pentylene Glycol, Caprylyl Glycol) or renewable acid complexes, where Clariant’s Nipaguard SCE Vita (100% Renewable Carbon Index) demonstrates that high-water-activity formulas can remain micro-stable without parabens or isothiazolinones.

Multi-functional systems are also becoming brand-differentiated sensory assets. Early-2025 launches of “Purisafe” self-preserving systems are marketed simultaneously for skin barrier efficacy, halal purity compliance, and antimicrobial function, positioning preservation within emotional-benefit narratives (“skin-mind balance”) while still meeting hard regulatory compliance around bacterial challenge testing.

Preservation Solutions Compatible with Natural and Organic Certification Systems

The fastest-growing commercial segment is COSMOS- and NATRUE-approved antimicrobial preservatives, driven by the rise of oil-rich, high-water-activity creams that traditionally experienced rapid microbial spoilage. As industrial players reconfigure supply chains, Benzyl Alcohol and Benzoic Acid capacity is expanding within LANXESS’s Flavors & Fragrances division to support nature-identical demand.

A powerful commercial lever is ingredient origin storytelling. Symrise’s Embrace Natura Award 2025 recognizes upcycling-based antimicrobial systems that reduce carbon footprint. Meanwhile, medical-grade crossovers are accelerating: Schülke & Mayr’s acquisition of Redditch Medical (September 2025) reflects consolidation toward high-purity antimicrobial inputs used in cleanroom cosmetics and wound-care-adjacent innovations—a premium category with significantly better margins.

Industrial-Grade Antimicrobial Preservatives Free of Formaldehyde, Metals, and Sensitizers

Industrial markets are undergoing a parallel transformation as water-based paints, adhesives, and metalworking fluids increase susceptibility to bacterial degradation. Effective in-can protection without formaldehyde releasers or heavy metals is now a procurement prerequisite.

A notable competitive differentiator is chemical stability under harsh processing conditions. LANXESS’s CDP hygiene model (Control – Detect – Prevent) illustrates a shift toward plant-level antimicrobial systems like Preventol OX, which treat water and equipment instead of putting biocide directly into end-products. At the same time, BASF Coatings is reinforcing supply chain resilience by scaling renewable-energy-powered dispersant production, a prerequisite for long-life water-based primers requiring 12–24 month in-can stability.

The automotive and aerospace sectors are driving another high-margin frontier: boric-acid-free, formaldehyde-free metalworking fluids, where alkanolamine-buffered antimicrobial systems simultaneously stabilize alkalinity and biological load, creating a dual-function value proposition that strongly influences OEM qualification and tooling uptime.

Antimicrobial Preservative Market Share and Segmentation Insights

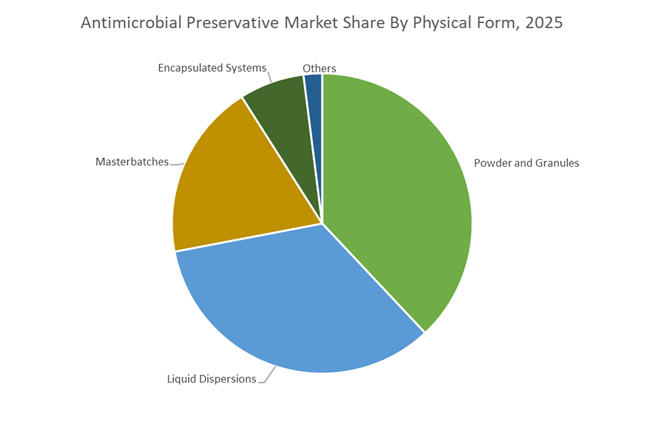

Market Share by Physical Form: Powders Lead Volume While Encapsulated Systems Redefine Performance

Powder and granule formats account for approximately 38% of antimicrobial preservative demand in 2025, retaining leadership due to low logistics cost, long shelf life, and compatibility with dry blending in paints, construction mixes, pharmaceutical tablets, and polymer compounding. Sodium benzoate, potassium sorbate, calcium propionate, and silver–zinc zeolites dominate this category, particularly in emerging markets where cold-chain infrastructure is limited. Liquid dispersions follow closely, favored in water-based paints, adhesives, sealants, and personal care for dust-free handling and automated dosing, with isothiazolinones (BIT, MIT, CMIT) and organic acids leading volumes. Masterbatches remain critical for plastics, enabling safe incorporation into PE, PP, and PET for medical devices and food packaging. Encapsulated preservative systems are the fastest-growing segment, enabling controlled release, thermal stability during extrusion, and reduced leaching in long-life coatings and textiles, despite higher unit costs.

Market Share by Application Method: Bulk Integration Dominates as Controlled Release Gains Regulatory Momentum

Bulk integration represents roughly 47% of antimicrobial preservative usage in 2025, serving as the gold standard for plastics, rubber, sealants, paints, and adhesives where protection must extend throughout the material matrix. This method is mandatory for medical implants, food-contact polymers, and marine coatings, preventing both bio-deterioration and surface microbial growth. Surface coatings rank second, widely applied in architectural paints, wood preservation, leather finishing, and antimicrobial touchpoint treatments, but face durability limits from abrasion and wash-off. Controlled release systems are gaining rapid traction, particularly in marine antifouling, medical device coatings, and agricultural films, optimizing efficacy while reducing total biocide loading. Vapor phase systems remain niche, used for electronics storage, museum preservation, HVAC sanitation, and emerging active food packaging. Regulatory frameworks such as EU BPR and EPA FIFRA are accelerating the shift away from topical dosing toward controlled delivery technologies with stronger IP protection.

Antimicrobial Preservative Market Competitive Landscape

The antimicrobial preservative market in 2026 is defined by safe-by-design chemistry, microbiome-friendly preservation systems, AI-driven formulation efficiency, and mass-balance bio-based feedstocks. Leading suppliers are competing on low-VOC technologies, paraben-free and formaldehyde-free actives, multifunctional preservation blends, and regulatory-ready solutions for cosmetics, coatings, agriculture films, and industrial applications. Strategic priorities include localized production, EU Cosmetics Regulation compliance, organic farming compatibility, and skin-barrier-safe antimicrobial systems. Innovation is increasingly centered on minimum inhibitory concentration (MIC) optimization, synergistic booster platforms, and traceable raw-material sourcing, positioning antimicrobial preservatives as critical enablers of clean-label personal care, green construction, and next-generation hygiene formulations.

Safe-by-design and mass-balance bio preservation anchor growth at BASF SE

BASF has integrated antimicrobial preservatives into its VALERAS® portfolio, emphasizing safe-by-design chemistry and localized supply chains. In January 2026, the company launched Near-Zero SVOC dispersion technology for interior coatings, eliminating semi-volatile organic compounds while maintaining high antimicrobial efficacy. Its Tinuvin® NOR® platform supports greenhouse and mulch films with heavy-metal-free resistance to chemical and microbial degradation in organic farming. BASF expanded European capacity in 2025 for nature-inspired multifunctional preservatives to meet tightening EU Cosmetics Regulation for baby care and sensitive skin. Strategically, BASF is transitioning its HyGentic® line to mass-balance bio-based feedstocks, enabling customers to claim reduced fossil-carbon content across cosmetic and packaging applications.

Microbiome-friendly preservation systems drive innovation at Lonza / Arxada

Lonza, through Arxada, leads the antimicrobial preservative market with microbiome-friendly preservation platforms targeting reduced single-active loads. Its 2026 One Lonza Strategy prioritizes Microbial Control Solutions, focusing on skin-compatible antimicrobial systems. Early 2026 saw successful integration of the Vacaville mammalian facility, strengthening pharmaceutical-grade preservative manufacturing capabilities. Key offerings include new preservative blends that eliminate pathogens while preserving beneficial skin bacteria, supporting advanced cosmetic and dermatological formulations. Through the Lonza Engine, the company combines automated high-throughput screening with regulatory consulting to accelerate commercialization. This vertically integrated model positions Arxada as a preferred CDMO partner for complex, globally compliant antimicrobial preservative formulations.

Nature-identical chemistry reshapes clean-label preservation at Ashland Inc.

Ashland has repositioned itself as a life sciences leader, blending pharmaceutical-grade stability with consumer sensory performance. Its Optiphen™ and Rokonsal™ brands are 100% paraben-free and formaldehyde-free, approved across major markets including Japan and China. In 2025/26, Ashland introduced sensiva™ sc 50 natural, delivering gentle antimicrobial protection alongside deodorizing and skin-conditioning benefits. The company’s strength lies in nature-identical chemistry, producing COSMOS- and ECOCERT-compliant organic acids for eco-conscious formulations. Strategically, Ashland is strengthening backward integration to ensure full traceability for its Phyteq™ raspberry n multifunctional line, reinforcing supply-chain transparency across premium personal care preservatives.

AI-driven MIC optimization accelerates efficiency at Clariant AG

Clariant differentiates through digital innovation, deploying robotics and AI to identify minimum inhibitory concentrations for hyper-efficient preservation. Its AMICA robotic platform in Frankfurt now tests antimicrobial performance at ten times conventional speeds, dramatically shortening formulation cycles. The Velsan® SC synergistic booster series allows formulators to reduce traditional preservative loads by up to 50% while expanding broad-spectrum efficacy. Clariant’s purpose-led strategy emphasizes micro-protection for toddlers and sensitive skin users. Through its online Antimicrobial Selector, the company provides real-time compatibility data across pH ranges and ingredient systems, enabling faster development of low-exposure, high-performance antimicrobial preservative solutions.

Synergy mapping and eco-actives define protection science at Symrise AG

Symrise blends fragrance expertise with microbiology to deliver advanced antimicrobial preservatives under its Hogo protection framework. Hydrolite® 5 green, the first sugar-cane-derived 1,2-alkanediol, provides moisturization while boosting preservation efficacy. In late 2025, Symrise launched SymGuard® CD for topical, oral, and intimate hygiene applications with an eco-friendly profile. Its patented Symocide PS® offers an all-in-one replacement for traditional preservatives. Leveraging four decades of skin science, Symrise applies synergy mapping to create Smart DEO actives that prevent odor at the source without organohalogens, strengthening its leadership in clean-label cosmetic preservation.

Industrial-scale, low-VOC preservation leadership at LANXESS AG

LANXESS dominates industrial antimicrobial preservatives with its Preventol® range, protecting paints, coatings, and adhesives against bacterial and in-can fungal growth. The integration of Emerald Kalama Chemical expanded its benzoic acid and sodium benzoate capacity for food and beverage preservation. In 2025, LANXESS ramped up low-VOC production across Asia-Pacific to support green building code expansion in Singapore and China. Its eco-conscious innovation strategy focuses on preservatives that retain performance through multiple freeze-thaw cycles, a critical requirement for construction materials and infrastructure coatings. This industrial-scale expertise positions LANXESS as a cornerstone supplier for long-life preservation systems.

China Antimicrobial Preservative Market: Standards Enforcement and Industrial-Scale Green Chemistry Deployment

China’s antimicrobial preservative landscape has been fundamentally reshaped by regulatory enforcement and industrial localization. The full implementation of the revised GB 2760-2024 national standards on October 1, 2025 redefined permitted dosage limits and application scopes across more than 25 antimicrobial categories. This overhaul has rapidly shifted demand away from conventional synthetic benzoates toward naturally derived systems, particularly nisin-based preservatives aligned with food safety and export compliance requirements.

Industrial scale-up has reinforced this transition. In late 2025, BASF inaugurated its expanded Verbund site in Zhanjiang, strengthening localized production of high-purity propionic acid for bakery and animal feed stabilization across East Asia. Parallel innovation is emerging from state-backed research. The Chinese Academy of Sciences announced a mid-2025 pilot for graphene-oxide antimicrobial coatings in grain storage silos, reducing preservative dosage requirements by 22%. Policy incentives under updates to the 14th Five-Year Plan further support Zero-VOC liquid dispersions, favoring water-borne organic acids. Meanwhile, MIIT-backed active packaging pilots and copper-free agricultural sprays underscore China’s pivot toward integrated, environmentally safer preservation systems.

India Antimicrobial Preservative Market: AMR Policy Alignment and Rapid Uptake of Natural Preservatives

India’s antimicrobial preservative strategy is increasingly aligned with public health and antimicrobial resistance mitigation. The launch of the National Action Plan on AMR 2.0 (2025–2029) in late 2025 mandates a reduction in antibiotic-class preservatives in animal husbandry, accelerating adoption of phytogenic and fermentation-derived antimicrobial additives. This policy shift has had immediate downstream effects across food, feed, and pharmaceutical value chains.

Investment in pharmaceutical-grade capacity is a defining feature. Lonza expanded its Vantocil™ manufacturing footprint in India in early 2025 to serve rising demand for sterile preservatives in ophthalmic and injectable formulations. Regulatory pressure from the Food Safety and Standards Authority of India further reinforced this trend. Its 2025 Additive Safety Compendium reclassified 18 synthetic preservatives as High Observation, triggering a reported 35% surge in nisin and natamycin usage. Complementing this, innovation in biodegradable antimicrobial packaging and zinc pyrithione alternatives within the Gujarat chemical corridor highlights India’s movement toward safer, application-specific preservation chemistries.

United States Antimicrobial Preservative Market: Approval Acceleration and Advanced Material Substitution

The United States market is being shaped by regulatory modernization and material science substitution. The implementation of PRIA 5 by the U.S. Environmental Protection Agency in January 2025 significantly accelerated approval timelines for reduced-risk antimicrobial biopesticides, improving predictability for preservative innovation pipelines. This has encouraged formulators to prioritize biologically derived and lower-toxicity systems.

PFAS-free transitions are now a central strategic theme. Milliken & Company announced a complete phase-out of PFAS-based processing aids in antimicrobial textiles by late 2025, replacing them with metal-organic framework technologies. Federal procurement policy reinforced this shift. Under the 2025 Executive Order on Advancing Biotechnology, agencies began prioritizing citric-acid-based disinfectants over quaternary ammonium compounds. Innovation is also extending into medical and packaging domains, with FDA-cleared light-activated antimicrobial films and venture-backed plant-based antibacterial superabsorbent polymers addressing sterilization and moisture-control challenges without legacy preservatives.

Germany Antimicrobial Preservative Market: Circularity, Enzyme Systems, and Aerospace-Grade Compliance

Germany’s antimicrobial preservative ecosystem is being redefined by circular economy mandates and high-specification industrial standards. From early 2026, the German Packaging Act requires antimicrobial additives in food-contact materials to be fully recyclable without contaminating post-consumer resin streams. This requirement is pushing suppliers toward non-migratory, low-toxicity preservative systems compatible with mechanical recycling.

At the technology level, Evonik Industries launched its TEGO® Guard series in late 2025, leveraging enzyme-based mechanisms to selectively disrupt biofilms in HVAC and cooling tower systems. Germany’s influence also extends into aerospace and infrastructure. Collaborative certification efforts with Airbus finalized silver-ion-free antimicrobial sheets for aircraft interiors, while the Federal Ministry of Education and Research invested €45 million in smart preservation sensors for automated dosing in water recycling systems. These initiatives position Germany at the intersection of sustainability, precision dosing, and regulatory leadership.

United Kingdom Antimicrobial Preservative Market: Bio-Waste Valorization and Healthcare-Driven Compliance

The United Kingdom is emerging as a niche innovator in bio-derived antimicrobial preservatives and responsible manufacturing. In late 2025, the startup HUID commercialized antimicrobial packaging derived from repurposed onion skins, offering a fiber-based alternative to synthetic preservative films. This development reflects a broader UK focus on agricultural waste upcycling and natural antimicrobial compounds.

Healthcare policy is another defining lever. Enforcement of NHS requirements for pharmaceutical suppliers to comply with the BSI Kitemark for minimized antimicrobial resistance in manufacturing effluents has elevated process-level scrutiny. As a result, UK suppliers are increasingly differentiating on effluent safety and lifecycle impact rather than preservative potency alone.

Country-Level Strategic Shifts in the Antimicrobial Preservative Industry

Antimicrobial Preservative Market County Level Snapshot

|

Country / Region

|

Primary Policy or Market Driver

|

Strategic Direction

|

|

China

|

National standards overhaul and green incentives

|

Natural preservatives, active packaging, Zero-VOC systems

|

|

India

|

AMR policy and food safety reclassification

|

Nisin, natamycin, phytogenic and biodegradable systems

|

|

United States

|

PRIA 5 acceleration and PFAS bans

|

Reduced-risk biopesticides, MOF and plant-based technologies

|

|

Germany

|

Circular economy and high-spec industrial standards

|

Enzyme-based, recyclable, silver-free preservatives

|

|

United Kingdom

|

Bio-waste valorization and NHS compliance

|

Natural fiber-based packaging and low-AMR manufacturing

|

Antimicrobial Preservative Market Report Scope

Antimicrobial Preservative Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Synthetic Preservatives, Natural and Bio Based Preservatives, Inorganic Preservatives), By Physical Form (Liquid Dispersions, Powder and Granules, Masterbatches, Encapsulated Systems), By Application Method (Surface Coatings, Bulk Integration, Controlled Release Systems, Vapor Phase Systems), By End Use Industry (Food and Beverage, Healthcare and Pharmaceutical, Cosmetics and Personal Care, Industrial and Construction, Textiles and Plastics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Lonza Group, Dow Inc, International Flavors and Fragrances, Kerry Group, Corbion, Milliken and Company, Microban International, DSM Firmenich, Clariant AG, Akzo Nobel, Archroma, Lanxess AG, Thor Group, Ashland Inc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antimicrobial Preservative Market Segmentation

By Product Type

- Synthetic Preservatives

- Natural and Bio Based Preservatives

- Inorganic Preservatives

By Physical Form

- Liquid Dispersions

- Powder and Granules

- Masterbatches

- Encapsulated Systems

By Application Method

- Surface Coatings

- Bulk Integration

- Controlled Release Systems

- Vapor Phase Systems

By End Use Industry

- Food and Beverage

- Healthcare and Pharmaceutical

- Cosmetics and Personal Care

- Industrial and Construction

- Textiles and Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Antimicrobial Preservative Industry

- BASF SE

- Lonza Group

- Dow Inc

- International Flavors and Fragrances

- Kerry Group

- Corbion

- Milliken and Company

- Microban International

- DSM Firmenich

- Clariant AG

- Akzo Nobel

- Archroma

- Lanxess AG

- Thor Group

- Ashland Inc

*- List not Exhaustive