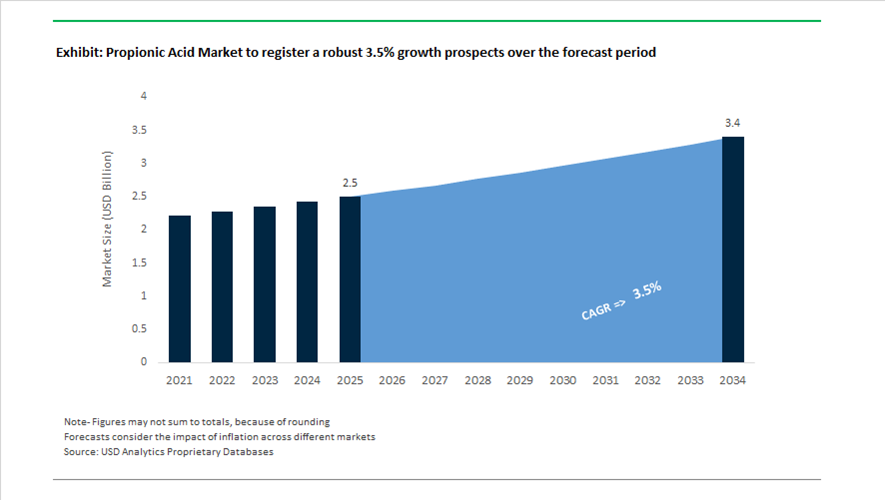

Propionic Acid Market Valued at $2.5 Billion in 2025, Projected to Reach $3.4 Billion by 2034 at 3.5% CAGR

The global propionic acid market is valued at $2.5 billion in 2025 and is projected to reach $3.4 billion by 2034, expanding at a CAGR of 3.5%. Growth is supported by sustained demand for food-grade propionic acid, calcium and sodium propionates, grain preservatives, animal feed acidifiers, and mold inhibitors across bakery, livestock nutrition, silage treatment, and pharmaceutical applications. Regulatory restrictions on antibiotic growth promoters and heightened food safety standards continue to reinforce the importance of propionic acid as a non-antibiotic antimicrobial preservative. At the same time, decarbonization pressures are reshaping procurement preferences toward bio-based and low-carbon propionic acid solutions.

Sustainability initiatives accelerated in 2024. BASF introduced propionic acid with a cradle-to-gate product carbon footprint of zero using a biomass-balance approach, replacing fossil-based feedstocks with renewable raw materials at the start of the production chain. This “Zero PCF” propionic acid positions BASF as a first mover in carbon-neutral food and feed preservatives. During 2024 and 2025, BASF secured ISCC PLUS certification for multiple core production sites, including McIntosh, Alabama and Kaisten, Switzerland, enabling broader commercialization of bio-based preservatives with traceable carbon accounting. Supply stability also improved in May 2024 when OQ Chemicals lifted force majeure declarations at its Oberhausen and Marl facilities in Germany following a synthesis gas disruption, restoring full operational capacity for key propionic acid precursors.

Operational realignments intensified in 2025. In February 2025, Perstorp expanded its Pro-Environment portfolio through mass-balance integration of renewable raw materials and ISCC PLUS-certified biogas and bio-circular methanol. This move supports downstream animal protein producers seeking reduced Scope 3 emissions in feed formulations. In early 2025, BASF transitioned its European Performance Materials sites to renewable electricity, lowering the carbon intensity of propionic acid production used in food and feed preservation. In August 2025, Perstorp implemented a global rightsizing initiative, reducing its workforce by 8% to address high energy costs and margin pressure in Europe while protecting long-term competitiveness.

Strategic restructuring extends into 2026. In January 2026, Dow unveiled its “Transform to Outperform” plan targeting $2 billion in EBITDA improvements through automation and AI-driven process optimization across chemical operations. Although company-wide, the initiative reinforces digital chemical dosing and operational efficiency across industrial acid production, including propionic acid systems.

The propionic acid market is increasingly characterized by zero-carbon-footprint propionic acid, ISCC PLUS-certified bio-based preservatives, renewable electricity integration, mass-balance methanol feedstocks, force majeure-driven supply stabilization, and AI-enabled production optimization strategies. Sustainability credentials, feedstock volatility management, and operational efficiency upgrades continue to shape competitive positioning across global food, feed, and specialty chemical applications.

Key Trends and High-Impact Opportunities in the Propionic Acid Market

Strategic Capacity Consolidation and Onshoring to Strengthen Agricultural Resilience

The propionic acid market is undergoing a decisive structural shift as food security, post-harvest loss prevention, and agricultural resilience move to the top of national policy agendas. Propionic acid has evolved from a routine preservative into a strategic agri-input, particularly for grain storage and animal feed protection. To reduce exposure to volatile trans-continental supply chains, producers are accelerating localized capacity expansion across Asia-Pacific and Europe, aligning production closer to end-use agricultural corridors.

In January 2025, BASF announced a targeted expansion of propionic acid production at its integrated Verbund sites in Germany and Nanjing, China. These expansions are designed to support fast-growing regional demand for feed preservatives and grain storage chemicals. The Nanjing facility is engineered to operate on 100% renewable electricity across its amine and organic acid portfolio, delivering an estimated 4% reduction in Product Carbon Footprint. This design directly addresses customer requirements for supply security and lower Scope 3 emissions while insulating regional feed producers from global logistics disruptions.

Beyond multinational investments, regional players across China, India, and Southeast Asia collectively added more than 70 kilotons of new annual propionic acid capacity between 2023 and 2025. This onshoring momentum closely mirrors government-led food security initiatives. In India, propionic acid consumption has increased sharply alongside the expansion of scientific grain storage capacity to 80.7 million metric tons. Calcium and ammonium propionate are now standard mold inhibitors across buffer stock infrastructure, making localized propionic acid supply a non-negotiable input for national food stability strategies.

Formulation Shift Toward Calcium Propionate for Clean-Label and Functional Bakery Applications

The bakery and processed food sectors are driving a second major trend through reformulation strategies that prioritize clean-label positioning without sacrificing shelf life. Calcium propionate is increasingly displacing sodium-based preservatives due to its dual functionality as both an antimicrobial agent and a nutritional fortifier.

Commercial bakery reformulation data from 2025 indicates that nearly 30% of new premium bakery product launches in North America now incorporate calcium propionate. Its ability to inhibit mold-forming organisms such as Bacillus mesentericus extends shelf life while allowing brands to remove artificial preservative claims from ingredient labels. Simultaneously, calcium propionate enables fortification messaging by contributing dietary calcium, aligning with consumer demand for functional nutrition.

Regulatory certainty is reinforcing this adoption curve. Under 21 CFR 184.1221, the U.S. FDA continues to classify calcium propionate as Generally Recognized as Safe with usage governed only by current Good Manufacturing Practice. This reaffirmed GRAS status in late 2025 provides manufacturers with regulatory clarity at a time when alternative preservatives such as benzoates and parabens face rising scrutiny from regulators and retailers alike.

Propionic Acid as a Renewable C3 Platform for Bio-Based Polymers and Coatings

One of the most transformative opportunities for the propionic acid market lies in its emergence as a renewable C3 platform chemical. Advances in microbial fermentation and catalytic upgrading are enabling propionic acid to displace petroleum-derived monomers in specialty polymers, coatings, and bioplastics.

By early 2025, fermentation-based production routes had achieved process yields exceeding 85%, while overall productivity improved by more than 35% compared to 2019. These gains have narrowed the cost differential between bio-based and fossil-derived propionic acid, making renewable cellulose acetate propionate commercially viable for high-margin applications such as premium eyewear, consumer electronics housings, and luxury accessories.

Carbon performance has become a decisive purchasing criterion. In November 2024, The Carbon Trust certified multiple BASF intermediates, including propionic acid, as having a substantially lower carbon footprint than fossil-based market benchmarks. This certification functions as a commercial enabler for downstream polymer producers supplying ESG-driven brands in automotive interiors, consumer electronics, and sustainable packaging.

Expansion into High-Purity Pharmaceutical and Cosmetic Preservation Systems

The pharmaceutical and personal care sectors represent a structurally attractive opportunity for high-purity propionic acid and its salts. Heightened regulatory scrutiny across Europe and Asia is accelerating the replacement of traditional preservatives with low-toxicity, multifunctional alternatives.

In 2025, adoption of pharma-grade propionic acid increased by approximately 12% as manufacturers increasingly utilized it as a biodegradable solvent, pH adjuster, and antimicrobial stabilizer in oral liquid and topical formulations. Its favorable toxicological profile supports compliance with updated pediatric safety and ingredient transparency requirements under EU Regulation EC No 1223/2009.

In cosmetics, regulatory pressure is even more pronounced. The EU Omnibus VII Regulation, entering into force in September 2025, restricts a wide range of legacy cosmetic preservatives. This has triggered rising demand for propionic acid as a microbiome-compatible ingredient that inhibits bacterial growth while maintaining skin-friendly pH levels. Its multifunctionality aligns strongly with skin-minimalism and microbiome-support trends, positioning propionic acid as a future-proof preservative solution for premium skincare and personal hygiene brands.

Propionic Acid Market Share and Segmentation Insights

Oxo Process Dominates Industrial Propionic Acid Production Due to Cost Efficient Petrochemical Integration

The Oxo process accounted for 58.60% of the Propionic Acid Market by production process in 2025, reflecting its efficiency and scalability in large scale chemical manufacturing. This process involves hydroformylation of ethylene followed by oxidation to produce propionic acid with high yield and consistent product quality. Availability of ethylene feedstock from steam crackers and petrochemical complexes supports widespread adoption of the Oxo process across global production facilities. The process also benefits from mature industrial technology and integrated petrochemical infrastructure. In 2025, process integration with upstream petrochemical operations is improving production economics, enabling manufacturers to optimize feedstock utilization, energy efficiency, and operational cost competitiveness in synthetic propionic acid production.

Agriculture Sector Drives Global Propionic Acid Consumption for Grain and Feed Preservation

Agriculture represented 42.80% of the Propionic Acid Market by end user industry in 2025, supported by the compound’s critical role in grain preservation and livestock feed protection. Propionic acid and its salts are widely used to prevent mold formation and mycotoxin contamination in stored grains, silage, and compound feed formulations. The global scale of crop production and livestock farming continues to generate strong demand for effective antifungal preservatives. In 2025, increasing adoption of high moisture grain harvesting practices is expanding agricultural demand, as farmers apply propionic acid treatments to stabilize grain quality during storage while reducing energy intensive drying operations across modern agricultural supply chains.

Propionic Acid Market Competitive Landscape

The 2026 propionic acid market is characterized by a shift toward bio-attributed intermediates, high-purity pharmaceutical-grade acids, and circular production models. Competitive dynamics are shaped by carbon footprint transparency (PCF), molecular recycling, and pricing strategies amid feedstock volatility and tightening regulatory frameworks.

BASF expands high-purity propionic acid supply through Verbund scale and carbon transparency

BASF SE leverages its Verbund-integrated production network to sustain cost leadership while expanding into low-carbon propionic acid solutions. The company reported €6.6 billion EBITDA in 2025, with 2026 growth supported by increased demand for feed additives and industrial intermediates. The Zhanjiang Verbund site strengthens supply of high-purity propionic acid to Asia-Pacific animal nutrition and pharmaceutical markets. Decarbonization efforts include renewable electricity integration and Product Carbon Footprint (PCF) data to support compliance with green labeling standards. Backward integration into oxo-synthesis ensures large-scale and stable production of propionic acid and salts. Core demand remains concentrated in grain preservation and clean-label food applications.

Eastman strengthens specialty propionic acid portfolio with molecular recycling and CAP derivatives

Eastman Chemical Company is advancing its circular economy strategy by integrating molecular recycling into its propionic acid and derivatives portfolio. The company generated $8.8 billion in revenue in 2025 while focusing on high-margin derivatives such as cellulose acetate propionate (CAP) for electronics and automotive coatings. A $0.10/kg price increase in 2026 reflects tightening supply-demand dynamics and rising feedstock costs. Its Kingsport facility contributed $60 million in incremental earnings through methanolysis technology, enabling production of recycled-content chemicals. Structural cost reductions of $125–$150 million are being implemented to maintain competitiveness against Asian producers. Emphasis on specialty acids and sustainable packaging applications supports long-term margin expansion.

Dow optimizes propionic acid production through AI-driven efficiency and high-purity applications

Dow Inc. is restructuring its operations to enhance efficiency and value in propionic acid production through its “Transform to Outperform” program. The company reported $40.0 billion in 2025 net sales and is targeting $2 billion in EBITDA improvement supported by AI-driven process optimization. Focus on FAMI-QS grade propionic acid enables penetration into high-growth sectors such as semiconductor processing and specialty dye intermediates. A projected $500 million EBITDA uplift in 2026 is driven by productivity improvements rather than volume expansion. Distribution network restructuring under a $1 billion cost-saving plan reduces operational complexity across Latin America and EMEA. High-purity chemical positioning supports growth in advanced industrial and pharmaceutical-grade applications.

Celanese strengthens acetyl chain competitiveness with pricing discipline and pharmaceutical intermediates

Celanese Corporation is enhancing its propionic acid business through acetyl chain integration and targeted pricing strategies. The company reported $9.5 billion in 2025 revenue and generated $773 million in free cash flow through cost optimization and inventory management. A global price increase in March 2026 addresses margin pressure from energy and feedstock volatility. Production prioritization at low-cost U.S. Gulf Coast facilities improves operational efficiency while limiting exposure to high-cost European assets. Strong capabilities in propionic anhydride production support applications in pharmaceuticals and fragrance intermediates. Material science expertise enables differentiation in high-value downstream applications.

Perstorp advances renewable propionic acid with mass-balance chemistry and animal nutrition leadership

Perstorp is expanding its renewable propionic acid portfolio through its Pro-Environment platform and integration with Petronas Chemicals Group. A global price increase in 2026 reflects rising input costs linked to geopolitical disruptions and energy market volatility. Mass-balance production enables substitution of fossil-based feedstocks with renewable alternatives, reducing carbon footprint across propionate derivatives. Strong presence in animal nutrition supports demand for antibiotic-free feed preservation and gut health solutions. Expansion into dielectric fluids for data centers highlights diversification into high-growth digital infrastructure markets. Integration with Petronas enhances feedstock flexibility and access to Asia-Pacific specialty chemical demand.

Daicel advances biomass-based propionic acid derivatives through digital manufacturing and sustainability leadership

Daicel Corporation is positioning itself in high-performance propionic acid derivatives through its acetyl chain expertise and biomass chemistry strategy. The company reported ¥583.0 billion in net sales for FY2026, supported by recovery of its carbon monoxide plant operations. Under DAICEL VISION 4.0, the company is integrating internal carbon pricing to accelerate development of eco-friendly cellulose acetate and acid derivatives. Recognition with an EcoVadis Gold Medal strengthens credibility in sustainability-driven markets across Europe and the U.S. Digital transformation initiatives, including the Mixing Concierge™ platform, improve manufacturing efficiency in complex chemical processes. Focus on electronics and healthcare applications supports demand for high-purity and performance-driven derivatives.

United States: Trade Realignment, Clean-Label Demand, and Packaging-Led Differentiation

The United States propionic acid industry in 2025 is navigating a complex mix of trade friction, regulatory clarity, and downstream innovation. The provisional antidumping duty imposed by China on U.S.-origin propionic acid has compelled domestic producers to recalibrate export strategies, with a pronounced pivot toward Latin American and Southeast Asian food preservation markets where calcium propionate demand remains structurally strong. This redirection is supported by regulatory certainty at home. The U.S. Food and Drug Administration’s reaffirmation of the GRAS status for propionic acid and its salts has reinforced its role as a preferred clean-label mold inhibitor in industrial bakery applications, particularly as sodium reduction initiatives gain momentum across packaged foods. Despite this regulatory tailwind, pricing dynamics softened in September 2025, with domestic prices stabilizing near $742 per metric ton as agricultural demand temporarily cooled under inflationary pressure on livestock feed consumption.

Strategic capital allocation and logistics resilience are shaping competitive positioning. In February 2025, Eastman Chemical executed a senior note offering to support expansion within its Specialty Materials division, which manages higher-margin propionic derivatives. This strategy has translated into downstream innovation, notably Eastman’s collaboration with Sealed Air to commercialize lightweight protein trays using cellulose acetate propionate as a recyclable alternative to polystyrene. At the same time, U.S. producers have invested in port-adjacent storage and handling infrastructure to mitigate West Coast congestion risks, preserving export continuity for liquid organic acids even amid softer near-term pricing.

China: Capacity Expansion Meets Oversupply and Regulatory Tightening

China remains the most capacity-driven propionic acid market globally, characterized by aggressive buildout followed by corrective pricing pressure. In January 2025, the BASF–Sinopec joint venture finalized plans to expand propionic acid and propionic aldehyde capacity at Nanjing, targeting the fast-growing domestic grain preservation and livestock feed segments. More broadly, China added over 70 kilotons per annum of new capacity between 2023 and late 2025, largely centered on oxo-process routes that capitalize on abundant domestic propylene. While this expansion strengthened self-sufficiency, it also contributed to structural oversupply as downstream feed and agriculture demand slowed.

Regulatory and environmental controls have added another layer of complexity. Mid-2025 carbon output restrictions temporarily constrained operating rates at several plants in Shandong and Jiangsu, tightening supply in the short term but not fully offsetting excess capacity. By September 2025, domestic prices declined to around $828 per metric ton, reflecting this imbalance. Concurrently, China’s 2025 Chemical Safety Roadmap enforced stricter GHS labeling and traceability for propionic acid, particularly in the herbicide value chain. These measures are raising compliance costs but improving transparency and acceptance of Chinese exports in regulated international markets.

Germany: Renewable Power, Regulatory Leadership, and Specialty Migration

Germany’s propionic acid industry is increasingly defined by sustainability leadership and a shift toward high-purity specialty applications. By January 2025, BASF completed the transition of its European production assets to 100% renewable electricity, including propionic acid units. This move significantly lowers the carbon-to-product footprint of propionic-based animal nutrition and food preservation solutions, aligning with the EU Green Deal’s Chemicals Strategy for Sustainability. Germany’s regulatory environment continues to set the pace within the EU, which accounts for nearly half of global demand, by enforcing stricter authorization and compliance standards for food-contact preservatives.

On the innovation front, German producers have reallocated R&D budgets toward ultra-pure propionic acid grades tailored for pharmaceutical intermediate synthesis. This shift is driven by rising demand for non-steroidal anti-inflammatory drug manufacturing, where impurity control is critical. In parallel, major chemical hubs are piloting ISCC PLUS-certified biogas and other bio-circular feedstocks, enabling the production of propionic acid with verified reductions in fossil resource intensity. These initiatives collectively position Germany as a premium supplier in regulated food, pharma, and nutrition markets rather than a volume-driven exporter.

India: Agrochemical Exports and Feed Infrastructure as Structural Demand Drivers

India’s propionic acid market is benefiting from its expanding role as a global agrochemical export hub and sustained investment in livestock infrastructure. During 2024 and 2025, Indian herbicide exports grew by more than 30%, supported by the Production Linked Incentive scheme for specialty chemicals. As propionic acid is a foundational intermediate in several herbicide formulations, this export momentum is translating into steady upstream demand. Regulatory modernization is also underway. The Ministry of Environment is finalizing the Indian Chemicals Management and Safety Rules, which will mandate registration and safety data sheets for propionic acid from 2026, signaling a shift toward EU-style chemical governance.

Long-term feed demand provides an additional anchor. Under the Animal Husbandry Infrastructure Development Fund, India invested roughly ₹15,000 crore by 2025 to modernize feed mills and cold-chain infrastructure. This has created a durable consumption base for propionic acid-based mold inhibitors used to stabilize compound feed under tropical storage conditions. Together, export-oriented agrochemicals and domestic livestock investment are insulating India’s propionic acid demand from short-term global price volatility.

Sweden: Bio-Circular Leadership and Animal Nutrition Specialization

Sweden occupies a strategic niche in the propionic acid industry through bio-circular innovation and animal nutrition specialization. In February 2025, Perstorp expanded its Pro-Environment portfolio, applying mass-balance methodologies to produce propionic acid derived from renewable bio-methanol and bio-propylene. Early 2025 ISCC PLUS certification across Perstorp’s facilities has validated these products as drop-in equivalents to fossil-based material, enabling customers to reduce Scope 3 emissions without altering formulations.

Beyond sustainability, Sweden is a development hub for performance-driven feed solutions. Propionic acid derivatives are increasingly deployed in synergistic gut-health systems designed to improve feed conversion ratios in European poultry and swine production. This focus on functional outcomes rather than commodity volumes reinforces Sweden’s role as a center for innovation and formulation expertise within the broader European propionic acid landscape.

Country-Level Snapshot: Propionic Acid Industry

Propionic Acid Market County Level Snapshot

|

Country / Region

|

Strategic Emphasis

|

Implication for Propionic Acid

|

|

United States

|

Trade diversification, clean-label foods, circular packaging

|

Stable bakery demand, growth in value-added derivatives

|

|

China

|

Capacity expansion, safety regulation

|

Oversupply-driven price pressure with higher compliance

|

|

Germany

|

Renewable power, regulatory leadership

|

Premium, low-carbon and pharma-grade propionic acid

|

|

India

|

Agrochemical exports, livestock infrastructure

|

Structurally rising demand for intermediates and feed preservatives

|

|

Sweden

|

Bio-circular feedstocks, animal nutrition

|

Sustainability-led differentiation and specialty solutions

|

Propionic Acid Market Report Scope

Propionic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Production Process (Oxo Process, Reppe Process, By-Product Process, Biomimetic Fermentation), By Product & Derivatives (Propionic Acid, Calcium Propionate, Sodium Propionate, Propionic Anhydride, Cellulose Acetate Propionate, Herbicides), By End-User Industry (Agriculture, Food & Beverage, Pharmaceuticals, Personal Care, Industrial)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Eastman Chemical Company, Perstorp Holding AB, Dow Chemical Company, Sinopec Group, Sasol Limited, Celanese Corporation, Daicel Corporation, Corbion NV, OQ Chemicals GmbH, AFYREN SA, Macco Organiques s.r.o., Yancheng Huade Biological Engineering Co. Ltd., Niacet Corporation, Otto Chemie Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Propionic Acid Market Segmentation

By Production Process

- Oxo Process

- Reppe Process

- By-Product Process

- Biomimetic Fermentation

By Product & Derivatives

- Propionic Acid

- Calcium Propionate

- Sodium Propionate

- Propionic Anhydride

- Cellulose Acetate Propionate

- Herbicides

By End-User Industry

- Agriculture

- Food & Beverage

- Pharmaceuticals

- Personal Care

- Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Propionic Acid Industry

- BASF SE

- Eastman Chemical Company

- Perstorp Holding AB

- Dow Chemical Company

- Sinopec Group

- Sasol Limited

- Celanese Corporation

- Daicel Corporation

- Corbion NV

- OQ Chemicals GmbH

- AFYREN SA

- Macco Organiques s.r.o.

- Yancheng Huade Biological Engineering Co. Ltd.

- Niacet Corporation

- Otto Chemie Pvt. Ltd.

*- List not Exhaustive