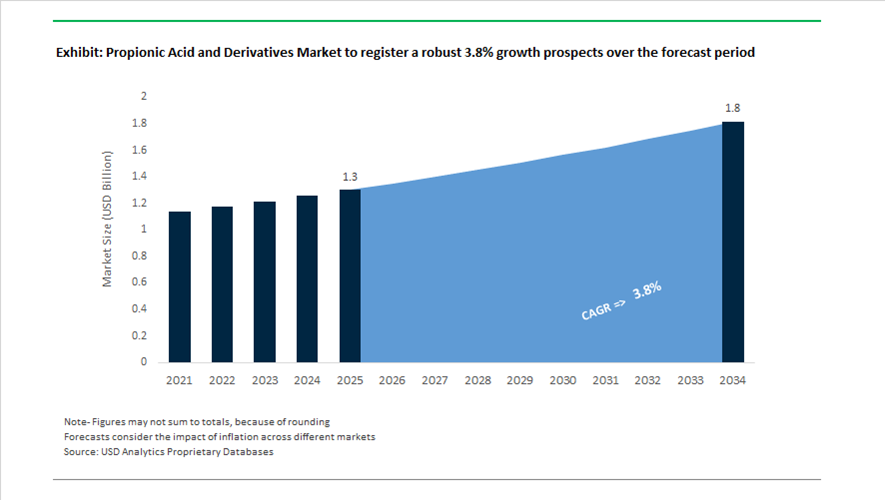

Propionic Acid and Derivatives Market Valued at $1.3 Billion in 2025, Projected to Reach $1.8 Billion by 2034 at 3.8% CAGR

The global propionic acid and derivatives market is valued at $1.3 billion in 2025 and is projected to reach $1.8 billion by 2034, expanding at a CAGR of 3.8%. Demand is primarily driven by increasing consumption of grain preservatives, animal feed acidifiers, calcium and sodium propionate salts, cellulose acetate propionate (CAP), and antimicrobial food additives across livestock nutrition, bakery products, pharmaceuticals, and specialty coatings. Regulatory restrictions on antibiotic growth promoters in animal feed and heightened food safety standards are strengthening the role of propionic acid as a non-antibiotic preservation solution. At the same time, carbon footprint transparency and renewable feedstock integration are reshaping production economics.

Supply stability improved in 2024 following upstream disruptions. In February 2024, Addcon launched ADDCON XL Forte in Southeast Asia, a liquid acidifier blend targeting Gram-positive and Gram-negative bacteria in animal drinking water systems. In May 2024, OQ Chemicals lifted force majeure declarations on n-propionaldehyde and related oxo intermediates at its Oberhausen and Marl facilities after a synthesis gas supply interruption, restoring full capacity for key precursors used in propionic acid manufacturing. In June 2024, Kemin Industries introduced FORMYL in the U.S. market, intensifying competition among non-antibiotic antimicrobial acidifiers and prompting renewed focus on propionate-based formulations. During 2024 and into 2025, Perstorp expanded Gastrivix™ Avi, a synergistic blend of valeric and butyric esters, reinforcing a broader shift toward combining propionic acid with other short-chain fatty acids to enhance gut morphology and feed conversion ratios in poultry production.

Decarbonization strategies gained momentum in 2025. In January 2025, BASF announced increased global propionic acid production capacity at its Ludwigshafen and Nanjing Verbund sites to meet rising feed preservation demand. Earlier, BASF introduced PA ZeroPCF, offering propionic acid with a cradle-to-gate product carbon footprint of zero using biomass-balanced feedstocks. In February 2025, Perstorp expanded its ISCC PLUS-certified organic acid portfolio through mass-balance renewable raw materials, enabling feed producers to align with net-zero commitments. In April 2025, OQ Chemicals implemented global price adjustments for oxo intermediates including propionaldehyde, reflecting volatility in ethylene and energy costs. In December 2025, Celanese achieved ISCC Carbon Footprint Certification linked to its Texas carbon capture and utilization facility, converting CO₂ emissions into methanol feedstocks used in acetyl-chain derivatives including propionic acid-based products.

Corporate restructuring and energy transition initiatives extend into 2026. In October 2025, Daicel announced reorganization of its engineering plastics business effective April 2026, aiming to more tightly integrate cellulose acetate propionate production with its core materials portfolio. In late 2025 and early 2026, BASF transitioned multiple European performance chemical units, including propionic acid production, to renewable electricity under its “Winning Ways” strategy, lowering the carbon intensity of food and feed preservatives.

The propionic acid and derivatives market is increasingly characterized by non-antibiotic feed acidifiers, biomass-balanced Zero-PCF propionic acid, ISCC PLUS-certified organic acids, oxo-intermediate price volatility, cellulose acetate propionate integration, and carbon capture-enabled acetyl derivatives. Regulatory pressure on antibiotic use, sustainability-driven procurement standards, and feedstock cost management continue to shape competitive positioning across global food, feed, and specialty materials markets.

Strategic Trends and High-Value Opportunities in the Propionic Acid and Derivatives Market

Strategic Scaling of Localized Capacity to Safeguard Global Food and Feed Security

Propionic acid and its derivatives have evolved from routine preservatives into system-critical inputs for global food security and animal nutrition. By 2025, post-harvest grain losses in major agricultural economies such as India were estimated at close to 7%, materially impacting national food inflation and buffer stock management. This structural challenge is driving chemical producers to prioritize localized propionic acid capacity rather than relying on import-dependent supply chains exposed to freight volatility and geopolitical risk.

In January 2025, BASF announced a strategic production realignment to expand propionic acid output at its integrated Verbund sites in Germany and China. These expansions are specifically calibrated to meet rising demand for calcium and ammonium propionate in compound feed and grain storage, where mold inhibition directly correlates with livestock productivity and feed conversion efficiency. Notably, BASF’s German operations now run on 100% renewable electricity, reinforcing the role of propionic acid as both a food security and low-carbon chemical.

At the national level, policy-driven storage expansion is reinforcing demand visibility. Government disclosures from March 2025 show that the Food Corporation of India scaled its scientific storage capacity to 80.7 million metric tons. Propionic acid derivatives are embedded across this infrastructure as first-line antifungal agents for wheat and rice preservation, reducing spoilage risk during long storage cycles and stabilizing domestic supply. As a result, propionates are increasingly treated as strategic inputs rather than discretionary additives across food and feed value chains.

Commercialization of Bio-Based Propionic Acid through Industrial Fermentation

A structural inflection point is underway as bio-based propionic acid transitions from pilot-scale innovation to commercial reality. The industry is gradually decoupling from propylene-based oxo routes in favor of fermentation pathways that utilize agricultural co-products and sidestream biomass, aligning with circular economy and Scope 3 emission reduction targets.

In December 2025, AFYREN achieved a global first by bringing 100% bio-based propionic acid to market through its NEOXY biorefinery in France. Its partnership with Esse Skincare introduced a COSMOS-certified propionic acid for microbiome-friendly skincare formulations, positioning the molecule as a naturally occurring metabolite rather than a synthetic preservative. Life-cycle assessments indicate a materially lower carbon footprint compared to petrochemical propionic acid, strengthening adoption among premium personal care brands.

From an economic standpoint, fermentation viability has improved sharply. Strategic R&D data released in late 2025 shows process yields exceeding 85%, with fermentation productivity improving by approximately 35% since 2019. These gains have narrowed the cost differential with fossil-based propionic acid at a time when oxo-alcohol feedstocks face recurring price shocks linked to energy markets and regional conflicts. As a result, bio-based propionic acid is no longer positioned solely as a sustainability premium but as a resilient alternative with improving cost competitiveness.

Propionates as Sustainable Solvents and Intermediates in the Pharmaceutical Value Chain

Regulatory pressure on halogenated and toxic solvents is reshaping solvent selection in pharmaceutical manufacturing, creating a high-margin opportunity for propionic acid and its esters as biodegradable, low-toxicity alternatives. Propionic acid is increasingly utilized as a key intermediate in the synthesis of non-steroidal anti-inflammatory drugs and select antibiotic classes, where its reactivity and favorable safety profile enable cleaner reaction pathways.

Research published during 2024–2025 demonstrates that reactive extraction of propionic acid using natural diluents such as alsi oil can achieve extraction efficiencies exceeding 92%. This approach eliminates reliance on hazardous solvents like benzene, supporting regulatory compliance while reducing worker exposure risks. As regulatory scrutiny intensifies across API manufacturing hubs in India, Europe, and Southeast Asia, such solvent substitution pathways are becoming commercially attractive rather than experimental.

Beyond human pharmaceuticals, adjacent markets are amplifying demand. The U.S. pet care sector, projected to reach USD 250 billion by 2030, is increasingly adopting high-purity propionic acid as a safe antimicrobial component in specialty animal health and hygiene formulations. Its favorable toxicological profile and proven efficacy against mold and bacteria position propionic acid as a preferred preservative in premium veterinary and pet nutrition products.

Non-Phthalate Plasticizers for Cellulose-Based and Bio-Derived Materials

The global phase-down of phthalates in sensitive applications is unlocking a structurally durable growth opportunity for propionate-based plasticizers, particularly cellulose acetate propionate. These materials offer a rare combination of flexibility, transparency, impact resistance, and regulatory compliance in applications where skin contact and food safety are critical.

In November 2025, specialty materials developers in the eyewear segment highlighted the commercial success of bioplastics that blend cellulose acetate with vegetable-origin propionate esters. Products such as M49 bioplastics are now used in premium frames and accessories, delivering hypoallergenic performance and compostability while meeting the aesthetic and durability requirements of luxury markets.

Regulatory momentum is reinforcing this shift. EFSA updates released in December 2025 prioritized propionate-based materials for reassessment as safer alternatives to traditional phthalates in food contact materials. This has accelerated R&D into active packaging solutions that combine propionate polymers with bio-based antimicrobials, such as cinnamic acid, to extend the shelf life of high-value perishables like berries. As food safety, sustainability, and consumer transparency converge, propionate-based plasticizers are emerging as a compliant and commercially scalable solution across packaging and specialty materials.

Propionic Acid and Derivatives Market Share and Segmentation Insights

Propionic Acid Leads Global Demand as Core Antifungal Agent for Grain Preservation

Propionic acid accounted for 52.8% of the Propionic Acid and Derivatives Market by product type in 2025, reflecting its role as the primary compound used in agricultural preservation and industrial chemical synthesis. The chemical is widely applied for mold inhibition in grain storage and animal feed protection due to its strong fungicidal and bactericidal activity. It also serves as a critical feedstock for manufacturing propionate salts and propionic esters used in food preservation, pharmaceuticals, and specialty chemicals. Increasing global grain production and storage capacity continue to sustain strong demand for propionic acid solutions. In 2025, growing reliance on high moisture grain preservation technologies is strengthening market demand, enabling farmers to harvest crops earlier and maintain safe storage conditions without extensive grain drying operations.

Animal Feed and Grain Preservation Segment Drives Global Consumption of Propionic Acid

Animal feed and grain preservatives represented 42.80% of the Propionic Acid and Derivatives Market by application in 2025, supported by the widespread use of propionic acid in protecting stored grains and livestock feed from fungal contamination. The compound is highly effective in preventing mold growth and maintaining feed quality during long term storage and transportation. Large scale livestock production and global feed manufacturing continue to drive consistent consumption across agricultural markets. In 2025, increasing focus on mycotoxin prevention in animal nutrition is influencing preservative strategies, with propionic acid treatments widely used to inhibit toxin producing fungi that can impact livestock health, productivity, and feed safety across global agricultural supply chains.

Propionic Acid and Derivatives Market Competitive Landscape

The 2026 propionic acid and derivatives market is shaped by strategic shifts toward low-carbon production, specialty derivative expansion, and integrated supply chains. Leading companies are competing through pricing discipline, sustainable chemistry platforms, and high-purity applications across animal feed preservatives, food additives, and advanced industrial coatings.

BASF accelerates Asia-Pacific expansion with low-carbon propionic acid and integrated feedstock advantage

BASF SE sustains market leadership through its Verbund-integrated production model, enabling superior cost efficiency and large-scale propionic acid output. The company recorded €6.6 billion EBITDA in 2025, with 2026 growth supported by rising demand in animal feed preservatives and industrial intermediates. Its Zhanjiang Verbund facility strengthens supply to Asia-Pacific, particularly in animal nutrition and pharmaceutical-grade propionic acid. Decarbonization efforts focus on renewable energy integration and Product Carbon Footprint (PCF) transparency to address Scope 3 emission requirements. Strong backward integration into oxo-chemicals ensures stable raw material access and competitive pricing. Core revenue streams remain anchored in grain preservation and bakery additives while expanding into sustainable chemical solutions.

Eastman prioritizes high-margin propionic acid derivatives through circular economy technologies

Eastman Chemical Company is repositioning toward specialty propionic acid derivatives with a focus on margin expansion and sustainability. The company generated $8.8 billion in 2025 revenue, with growth driven by cellulose acetate propionate (CAP) used in advanced coatings and electronics. A $0.10/kg price increase in 2026 reflects supply tightening and feedstock inflation across North America. Portfolio transformation emphasizes non-phthalate plasticizers and antimicrobial preservatives aligned with regulatory frameworks such as EU REACH and FDA compliance. Carbon renewal technology (CRT) supports bio-attributed propionic acid production for premium personal care and feed applications. Strategic emphasis on specialty chemicals reduces exposure to commodity price volatility.

Dow strengthens high-purity propionic acid portfolio through digital optimization and specialty applications

Dow Inc. is restructuring its propionic acid operations under a productivity-led model focused on digitalization and specialty applications. The company reported $40.0 billion in 2025 revenue and targets EBITDA expansion through AI-enabled process optimization across carboxylic acids production. Strong positioning in FAMI-QS grade propionic acid supports demand in semiconductor processing and dye intermediates requiring high purity. Operational improvements prioritize efficiency gains over volume expansion, supported by a $1 billion cost reduction program. Distribution network optimization enhances competitiveness in Latin America and EMEA markets. Focus on high-specification industrial applications strengthens value realization across the propionic acid portfolio.

Celanese enhances propionic acid profitability through acetyl chain optimization and disciplined pricing

Celanese Corporation is leveraging its acetyl chain integration to improve cost competitiveness and margin stability in propionic acid derivatives. The company reported $9.5 billion in 2025 revenue and generated $773 million in free cash flow through cost controls and inventory optimization. Global price increases in 2026 address energy and feedstock volatility impacting acid production economics. Manufacturing strategy prioritizes low-cost U.S. Gulf Coast assets while reducing exposure to higher-cost European operations. The Eco-CC portfolio introduces bio-attributed and recycled-content derivatives targeting adhesives and coatings markets. Operational discipline and portfolio optimization support stable performance in a volatile macro environment.

Perstorp advances bio-attributed propionic acid through renewable feedstocks and animal nutrition leadership

Perstorp is advancing renewable propionic acid production through its Pro-Environment platform and integration with Petronas Chemicals Group. Pricing actions in 2026 reflect rising input costs linked to global energy and raw material volatility. Mass-balance technology enables transition from fossil-based to renewable feedstocks, reducing carbon intensity across propionate derivatives. Strong positioning in animal nutrition supports demand for feed preservatives and antibiotic-replacement solutions in livestock production. Integration with Petronas enhances feedstock access and expands reach in Asia-Pacific specialty chemicals markets. Sustainability-led differentiation aligns with increasing demand for low-carbon and traceable propionic acid solutions.

Germany: Verbund Optimization and Low-Carbon Propionates as a Competitive Lever

Germany remains a technology and sustainability anchor for the propionic acid and derivatives industry, underpinned by large-scale integrated production and advanced catalyst innovation. In January 2025, BASF successfully commissioned expanded propionic acid capacity at its Ludwigshafen Verbund complex, engineered to supply high-purity preservatives required by Europe’s long-life bakery and packaged food segments. The scale advantages of the Verbund model enable tighter heat and material integration, improving cost efficiency while maintaining consistent quality for calcium and sodium propionate applications. This production expansion is strategically aligned with rising regulatory scrutiny on food waste reduction, where propionic acid-based mold inhibitors play a critical role in extending shelf life without compromising label compliance.

Germany is also emerging as a testbed for low-emission synthesis routes. As part of the 2025–2026 methane pyrolysis collaboration between BASF and ExxonMobil, a demonstration plant announced in November 2025 will produce 2,000 metric tons of low-carbon hydrogen annually. This hydrogen serves as a key feedstock for oxo-intermediates and propionic acid derivatives, materially lowering Scope 1 emissions. Complementing this, German propionic acid units transitioned to 100% renewable electricity in early 2025, while BASF’s December 2025 unveiling of 3D-printed catalyst geometries improved throughput and selectivity in propionic acid synthesis. Achieving ISCC PLUS certification for bio-circular propionates in late 2025 further positions Germany as a premium supplier for sustainable food packaging and mass-balance compliant preservative systems under evolving EU REACH frameworks.

China: Capacity Expansion, Traceability Mandates, and Agrochemical Pull

China’s propionic acid industry is driven by scale expansion, regulatory tightening, and strong agrochemical demand fundamentals. In late 2025, the BASF–SINOPEC joint venture marked its 25th anniversary by breaking ground on a major propionic acid expansion in Nanjing, targeting domestic grain preservation and feed applications. This investment reflects China’s structural reliance on organic acids to reduce post-harvest losses in cereals and oilseeds, particularly as national food security priorities intensify.

Regulation is reshaping operating practices. The Ministry of Industry and Information Technology issued a draft mandatory national standard in August 2025 enforcing “One Enterprise, One Product, One Code” safety labeling, significantly improving traceability for hazardous chemicals such as propionic acid. A subsequent October 2025 update simplified labeling for packages below 5 mL, facilitating the distribution of high-concentration derivatives for laboratory and pharmaceutical use. On the demand side, China’s export dominance in herbicides remains a critical driver. Customs data for Q1 2024–2025 showed 1.57 million tons of herbicide exports, up 31.47% year on year, sustaining robust consumption of propionic acid intermediates. Simultaneously, ZLD enforcement in Jiangsu and Shandong during early 2025 has forced producers to adopt advanced wastewater treatment and byproduct recovery, raising compliance costs but improving long-term environmental acceptance.

United States: Pricing Discipline and Circular Packaging Applications

The United States propionic acid and derivatives market in 2025 has been characterized by pricing discipline, inventory rationalization, and innovation in sustainable packaging. In April 2025, Eastman Chemical implemented an off-list price increase of $0.15 per pound for organic acid derivatives, citing elevated logistics costs and geopolitical uncertainty. This move signaled a shift toward margin protection rather than volume-led growth, particularly in mature preservative applications.

Operational efficiency has also improved. During Q3 2025, U.S. chemical producers collectively reduced inventories by approximately $200 million, streamlining propionic acid supply chains and improving cash flow resilience. Downstream innovation is creating new outlets for derivatives. In September 2025, Eastman partnered with Sealed Air to launch a recyclable protein tray using cellulose acetate propionate as a functional substitute for polystyrene. In parallel, the ramp-up of molecular recycling platforms in 2025 has unlocked new bio-content streams for specialty propionic esters used in automotive interiors and consumer goods. Regulatory pressure is reinforcing formulation efficiency, as EPA reviews of herbicide application rates in 2025–2026 are driving demand for more concentrated propionic-based actives to reduce runoff and total chemical load.

India: Agrochemical Scale-Up and Pharmaceutical Localization

India’s propionic acid market is closely tied to agrochemical expansion and pharmaceutical localization. According to the India Brand Equity Foundation, the domestic agrochemical sector is projected to reach $14.5 billion by 2028, supporting sustained demand for propionic acid as a building block for fungicides and preservative formulations. This growth is reinforced by India’s role as a global supplier of crop protection products, where cost-effective organic acids are essential intermediates.

Policy-driven pharmaceutical growth is adding a second demand pillar. Under the Bulk Drug Production Linked Incentive scheme, India became a net exporter of bulk drugs in 2025, increasing domestic consumption of pharma-grade propionates used in anti-inflammatory and analgesic formulations. Reflecting this shift, Celanese expanded its Indian operations in May 2024 to strengthen regional technical services across the Acetyl Chain, which includes propionic acid derivatives. By March 2025, domestic value addition in pharmaceuticals reached 83.70%, accelerating localization of intermediates such as calcium and sodium propionate and reducing import dependency.

Sweden and the European Union: Animal Nutrition and Bio-Circular Integration

Sweden and the wider European Union are positioning propionic acid derivatives within animal nutrition and bio-circular chemical platforms. In July 2025, Perstorp released trial data for Gastrivix™ Avi, a synergistic blend of valeric and butyric acid derivatives that improves poultry feed conversion ratios by optimizing intestinal morphology. Such performance-driven formulations are gaining traction as EU livestock producers face pressure to improve efficiency while reducing antibiotic use.

Sustainability credentials are becoming a differentiator. In 2025, Perstorp successfully integrated bio-circular methanol and propylene into its production cycle, enabling commercial launch of low-carbon propionic acid grades aligned with EU climate targets. This strategy was strengthened by Perstorp’s December 2024 acquisition of OQ Chemicals Nederland B.V., which expanded its specialty chemicals footprint and reinforced access to sustainable preservative markets across Europe. Together, these developments underscore the EU’s focus on high-value, environmentally differentiated propionic acid derivatives rather than pure capacity expansion.

Country-Level Snapshot: Propionic Acid and Derivatives Industry

Propionic Acid and Derivatives Market County Level Snapshot

|

Region

|

Strategic Focus

|

Industry Implication

|

|

Germany

|

Verbund expansion, green hydrogen, catalyst innovation

|

Premium, low-carbon propionates for food and packaging

|

|

China

|

Capacity scale, traceability, herbicide exports

|

High-volume demand with rising compliance intensity

|

|

United States

|

Pricing discipline, circular packaging

|

Value-added derivatives and margin-focused growth

|

|

India

|

Agrochemicals, pharma localization

|

Strong pull for fungicide and pharma-grade propionates

|

|

Sweden / EU

|

Animal nutrition, bio-circular feedstocks

|

Sustainability-led differentiation in derivatives

|

Propionic Acid and Derivatives Market Report Scope

Propionic Acid and Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$1.8 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Product Type (Propionic Acid, Propionates, Propionic Esters, Other Derivatives), By Application (Food Preservatives, Animal Feed & Grain Preservatives, Herbicides & Pesticides, Pharmaceuticals, Personal Care & Cosmetics, Industrial Applications), By Source & Production Method (Synthetic, Bio-Based)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Eastman Chemical Company, Perstorp Holding AB, Celanese Corporation, Dow Chemical Company, Kemin Industries Inc., Daicel Corporation, Sasol Limited, Merck KGaA, Hawkins Inc., Yancheng Huade Biological Engineering Co. Ltd., Shanghai Jianbei Organic Chemical Co. Ltd., Niacet Corporation, Prathista Industries Limited, A.M. Food Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Propionic Acid and Derivatives Market Segmentation

By Product Type

- Propionic Acid

- Propionates

- Propionic Esters

- Other Derivatives

By Application

- Food Preservatives

- Animal Feed & Grain Preservatives

- Herbicides & Pesticides

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Applications

By Source & Production Method

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Propionic Acid and Derivatives Industry

- BASF SE

- Eastman Chemical Company

- Perstorp Holding AB

- Celanese Corporation

- Dow Chemical Company

- Kemin Industries Inc.

- Daicel Corporation

- Sasol Limited

- Merck KGaA

- Hawkins Inc.

- Yancheng Huade Biological Engineering Co. Ltd.

- Shanghai Jianbei Organic Chemical Co. Ltd.

- Niacet Corporation

- Prathista Industries Limited

- A.M. Food Chemical Co. Ltd.

*- List not Exhaustive