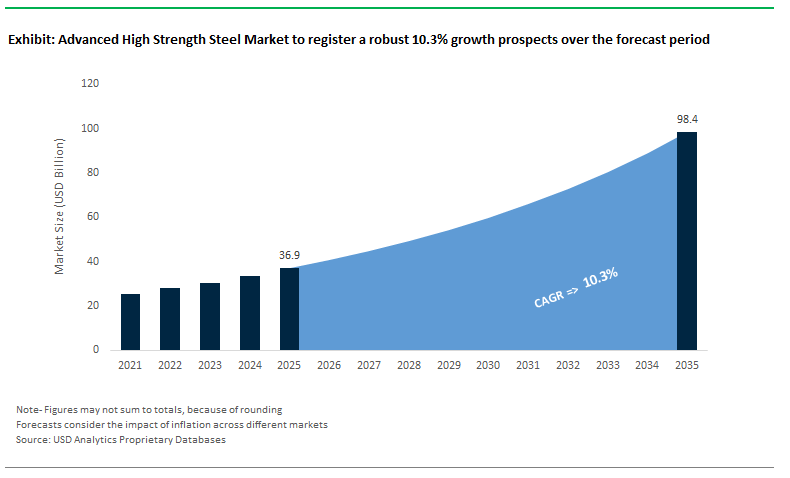

The Advanced High Strength Steel (AHSS) Market, valued at USD 36.9 billion in 2025, is projected to reach USD 98.4 billion by 2035, expanding at a strong CAGR of 10.3%. The industry’s momentum is rooted in automotive lightweighting mandates, electrification, and rising crash-safety expectations. Replacing conventional mild steel in a standard four-door vehicle with AHSS can reduce structural weight by up to 25%, enhancing fuel efficiency and reducing GHG emissions-two metrics OEMs are under increasing pressure to improve.

Market Analysis: Strategic Developments Redefining AHSS Capacity, Innovation, and Regional Supply Chains

The AHSS market landscape experienced major structural shifts in 2025, driven by consolidation, high-value capital investments, and strategic expansions targeting automotive and EV applications. In June 2025, ArcelorMittal finalized the acquisition of Nippon Steel’s 50% stake in the AM/NS Calvert joint venture for approximately USD 1.55 billion, securing full ownership of one of the most technologically advanced finishing facilities in the United States. This move significantly strengthens ArcelorMittal’s AHSS production and finishing capabilities in the North American automotive supply chain. Following this, July 2025 marked a transformational moment as Nippon Steel completed its USD 14.9 billion acquisition of U.S. Steel, ensuring long-term access to domestic AHSS manufacturing assets at a time when supply chain localization has become strategically critical. In the same month, AM/NS India commissioned a new Continuous Galvanising Line (CGL)-India’s first capable of producing the highest-strength steel grades required for automotive crash and structural elements-directly improving domestic OEM sourcing capabilities.

Parallel to these expansions, the AHSS ecosystem saw notable investment in advanced electrical steels and transformative manufacturing technologies. In February 2025, ArcelorMittal Calvert announced a USD 1.2 billion investment into a dedicated Non-Grain-Oriented Electrical Steel (NOES) facility, strengthening the supply base for EV traction motors, transformers, and high-efficiency electrical systems. Academic innovation contributed to material science breakthroughs: in January 2025, researchers at Seoul National University demonstrated how laser surface texturing (LST) significantly improves metal-polymer bonding strength, enabling next-generation multi-material automotive designs. This innovation strengthens AHSS integration with composite and polymer structures-a core requirement for vehicle lightweighting.

Looking further back, November 2024 saw JSW Steel introduce 100 new steel grades, notably including several new AHSS variants aimed at high-value automotive applications. In October 2024, AISI recognized General Motors, Magna, and Shape Corp. for the innovative use of AHSS in the GMC Hummer SUV, particularly highlighting UHSS applications in crash management. Cleveland-Cliffs followed in August 2024 with capacity expansions for hot-stamped and press-hardened steel, reinforcing domestic supply for U.S. OEMs adapting to stringent crash and safety regulations.

AHSS Market Growth Driven By Lightweighting, Crash Safety, and EV Structural Requirements

Automakers are rapidly transitioning toward Third Generation AHSS, such as Q&P steels, owing to their 18% higher uniform elongation compared with first-generation DP grades at the same 980 MPa UTS. Ultra High Strength Steels (UHSS), particularly in A/B-pillar reinforcements, are proving essential to improving body-in-white energy absorption by over 35%, directly influencing occupant safety in high-speed collisions. The acceleration of EV adoption adds new structural requirements; AHSS grades above 1,200 MPa are now standard for battery enclosures, optimizing fire protection, intrusion resistance, and weight neutrality.

At the buyer level, decision-makers are prioritizing formability, multi-phase microstructure control, crashworthiness, corrosion resistance, and compatibility with mixed-material body structures. Suppliers capable of supporting next-generation EV platforms, high-speed hot-stamping workflows, and digital-twin-driven quality control are gaining a competitive edge. On the other hand, material innovations in martensitic, complex phase, TRIP, and Q&P steels are expanding the performance envelope for both internal combustion and electrified vehicle architectures.

Key Insights for Product Manufacturers

- Vehicle lightweighting impact: Up to 25% structural weight reduction via AHSS substitution supports GHG reduction and improved fuel efficiency.

- 3rd Gen AHSS transformation: Q&P steels offer 18% higher uniform elongation versus DP 980 MPa grades, enhancing formability.

- Crash safety multiplier: UHSS deployment increases energy absorption of BIW structures by 35%+, improving high-speed collision survivability.

- EV battery safety: Martensitic and complex phase steels deliver >1,200 MPa strength required for thermal and intrusion protection in EV packs.

- Strong OEM pull: Regulations around passive safety, decarbonization, and EV efficiency continue to accelerate AHSS demand globally.

Advanced High Strength Steel Market: Trends and Opportunities

Strategic Shift Toward 3rd Generation AHSS and Press-Hardened Steel Architectures

Automotive lightweighting strategies are no longer centered on material substitution alone but on microstructure-led performance optimization, accelerating the transition toward 3rd Generation Advanced High Strength Steel (AHSS) and press-hardened steel (PHS). Unlike 1st Gen Dual-Phase or TRIP steels, 3rd Gen AHSS leverages Quenching & Partitioning (Q&P) and Medium-Manganese (Med-Mn) metallurgical routes to break the historical strength–ductility trade-off. According to 2025 technical benchmarks released by WorldAutoSteel, multiple 3rd Gen grades consistently achieve ~1200 MPa tensile strength while maintaining elongation in the 30–37% range—nearly double that of DP steels at comparable strength levels. This materially expands cold-forming feasibility for complex load paths such as B-pillars, roof rails, and crash boxes, reducing reliance on energy-intensive hot stamping.

Formability-linked safety performance is emerging as a key differentiator. Independent evaluations published in October 2025 demonstrate that 1180 MPa 3rd Gen AHSS exhibits hole expansion ratios around 40%, a critical metric for edge cracking resistance and crash energy absorption. These properties are directly translating into OEM adoption. United States Steel Corporation has scaled production of its XG3™ platform specifically for EV body-in-white architectures, while ArcelorMittal and Nippon Steel are rapidly deploying Fortiform®-class grades across global platforms. OEM feedback cited by suppliers indicates structural mass reductions of 15–20% versus legacy AHSS while preserving top-tier IIHS crash ratings—positioning 3rd Gen AHSS as a core enabler of EV range extension without sacrificing passive safety.

Reshoring of High-Value AHSS Production Driven by Policy and Supply-Chain Risk

Advanced high strength steel is increasingly classified as strategic industrial infrastructure, prompting governments to realign fiscal and industrial policy toward domestic capacity expansion. In India, the April 2025 revision of the Domestically Manufactured Iron and Steel Products (DMI&SP) policy mandates a minimum 50% domestic value addition for government-funded infrastructure and energy projects, directly incentivizing local AHSS melt-shop and rolling investments. This policy is complemented by the Production-Linked Incentive (PLI) Scheme for Specialty Steel, under which 35 companies committed approximately ₹25,200 crore in capital expenditure by early 2025 to establish domestic lines for automotive-grade AHSS and electrical steels.

In the United States, industrial policy alignment between the CHIPS and Science Act and Department of Energy decarbonization programs is reshaping steel investment priorities. Over $500 million in DOE grants have been earmarked for low-emission steelmaking, with projects such as U.S. Steel’s Big River 2 facility integrating advanced casting and rolling technologies optimized for high-end AHSS. Europe is pursuing a parallel “strategic autonomy” agenda. According to September 2025 disclosures from EUROFER, producers are prioritizing Direct Reduced Iron (DRI) assets to secure low-carbon feedstock for premium AHSS. Notably, thyssenkrupp Steel signed a long-term agreement in December 2025 with TSR Group to secure high-grade recycled inputs (TSR40), reinforcing the link between reshoring, circularity, and specialty steel competitiveness.

Integrated AHSS Battery Enclosure Systems Emerging as a Core EV Opportunity

Battery enclosure design has become one of the most steel-intensive opportunity areas within electric vehicle platforms, as OEMs reassess aluminum-heavy architectures in light of cost volatility, crash performance, and recyclability constraints. Advanced high strength steel—particularly martensitic, UHSS, and press-hardened grades—offers a compelling combination of thermal shielding, intrusion resistance, and structural integration. The global Steel E-Motive (SEM) initiative validated a coverless battery carrier frame concept utilizing AHSS that delivered 37% mass savings relative to incumbent benchmarks and reduced manufacturing costs by 27%, while simultaneously improving resistance to road-debris impact and floor intrusion.

From a safety standpoint, recent 2025 academic evaluations confirm that UHSS cross-members and rockers can withstand extrusion and puncture forces aligned with tightening national regulations on thermal runaway containment. Beyond compliance, OEMs are optimizing NVH and durability performance at the system level. Multi-objective optimization studies conducted in 2024 identified advanced cold-rolled steel variants exhibiting minimal deformation under vertical impact and emergency braking, maintaining stable resonance frequencies (~315 Hz) critical for long-term fatigue resistance. Steelmakers are now commercializing this insight through “ready-to-assemble” battery envelopes, using PHS to form a rigid safety cage around lithium-ion modules. This architectural shift typically adds ~85 kg of steel per vehicle compared with ICE platforms, creating a structurally embedded demand lever for AHSS that scales directly with EV penetration rather than vehicle volume alone.

Specialized AHSS for Hydrogen Transport and Storage Infrastructure

The build-out of hydrogen economies is creating a high-barrier opportunity for steel producers capable of engineering resistance to hydrogen embrittlement (HE)—a failure mode that has historically constrained steel use in high-pressure hydrogen environments. Advanced AHSS solutions now focus on ultra-clean chemistries, refined grain structures, and precipitate engineering to inhibit hydrogen diffusion and crack initiation. In August 2024, ArcelorMittal launched its HyMatch® family, a suite of steels specifically engineered for hydrogen pipelines and transport systems. These grades are designed to comply with ASME B31.12 Option B standards, enabling both new hydrogen-ready pipelines and the repurposing of existing natural gas infrastructure.

Scientific validation is reinforcing commercial momentum. A 2024 peer-reviewed synthesis highlighted that nanoscale precipitates act as effective hydrogen traps, preventing migration to grain boundaries and sharply reducing brittle fracture risk—now considered a baseline requirement for next-generation AHSS in hydrogen service. On the deployment side, industrial pilots are already underway. Jindal Stainless is collaborating with Punjab Energy Development Agency on green hydrogen systems that demand advanced austenitic and high-nickel stainless steels capable of operating at cryogenic temperatures down to –253°C. As hydrogen infrastructure scales, these specialized AHSS and stainless platforms position steel not as a legacy material, but as a critical enabler of the energy transition.

Advanced High Strength Steel (AHSS) Market Share Analysis

Market Share by Grade: Dual Phase (DP) Steels Anchor the Commercial Core of the AHSS Market

Dual Phase (DP) steels account for an estimated 33.2% share of the global Advanced High Strength Steel (AHSS) market, reflecting their position as the most commercially scalable and economically balanced AHSS grade for automotive OEMs and Tier-1 suppliers. DP steels dominate because they consistently deliver the industry’s required “sweet spot” between high tensile strength, superior formability, and cost-efficient mass reduction, making them compatible with high-volume vehicle platforms rather than niche or premium-only applications. Modern DP grades such as DP980 and DP1180 routinely exceed 1,000 MPa tensile strength, enabling significant gauge reduction while maintaining crash energy absorption—an outcome that directly aligns with tightening global safety regulations and fuel efficiency mandates. From a manufacturing economics standpoint, DP steels are optimized for cold forming, avoiding the capital-intensive hot-stamping lines required for press-hardened or fully martensitic steels. This preserves existing stamping infrastructure, shortens production cycles, and materially lowers per-unit manufacturing costs, which is critical as OEMs balance lightweighting targets against margin pressure. Third-generation DP steels further reinforce market share by offering higher “reserve ductility,” which reduces edge cracking and lowers scrap rates during complex stamping operations—an operational benefit that directly improves plant-level yield. When evaluated against aluminum, DP-based AHSS delivers a 2.1–3.5x cost advantage per unit of structural safety achieved, allowing automakers to meet weight reduction and crash performance benchmarks without triggering major material cost inflation. This combination of scalable strength, forming flexibility, and cost-to-weight efficiency explains why DP steels remain the dominant grade as AHSS adoption accelerates across both internal combustion and electric vehicle architectures.

Market Share by Application: Body-in-White (BIW) Structures Drive the Largest Share of AHSS Demand

The Body-in-White (BIW) segment commands approximately 41.3% of total AHSS demand, positioning it as the single largest application area and the structural backbone of AHSS market growth. BIW structures are the primary focus of lightweighting strategies because they account for a substantial portion of a vehicle’s total mass while directly influencing crashworthiness, torsional rigidity, and occupant safety. As electric vehicle penetration increases, BIW lightweighting has become even more critical, given the direct relationship between structural mass, battery size requirements, and driving range. Optimized AHSS and ultra-high-strength steel (UHSS) mixes in BIW designs have demonstrated nearly 20% mass reduction, translating into material savings of roughly 35–40 kg per vehicle without compromising structural integrity. OEMs are also rapidly adopting multi-part integration (MPI) strategies in BIW construction, using laser-welded AHSS door rings, side frames, and underbody modules to replace older multi-bracket assemblies—an approach that reduces part count, improves dimensional accuracy, and enables significant weight savings at scale. In EV-specific BIW architectures, AHSS has emerged as a preferred material for battery protection zones, where its high puncture resistance allows thinner designs than aluminum while meeting stringent side-impact and intrusion prevention requirements. The application of third-generation AHSS in BIW pillars and load paths further improves structural efficiency, enabling slimmer A- and B-pillars that enhance driver visibility without sacrificing safety performance. Collectively, these factors make BIW the structural and economic center of gravity for AHSS adoption, firmly anchoring its leading market share as automakers redesign vehicle platforms for electrification, safety compliance, and cost discipline simultaneously.

Market Share by Application, 2025.png)

Competitive Landscape: Leading Companies, Product Portfolios, and Strategic Positioning

The competitive arena for Advanced High Strength Steel is shaped by aggressive capacity expansion, proprietary metallurgy innovation, and deep integration with global automotive OEMs. Companies are differentiating through 3rd Generation AHSS, advanced hot-stamping solutions, digital-twin-enabled quality control, decarbonized steelmaking, and EV-centric material portfolios. With automotive lightweighting, crashworthiness, and electrification driving most purchasing decisions, leading steel manufacturers are prioritizing metallurgical advancements that combine high tensile strength with superior formability and fatigue resistance.

Arcelormittal - Expanding Global AHSS Leadership Through Strategic Acquisitions

ArcelorMittal offers an extensive AHSS portfolio under Usibor, Ductibor, and MartINsite, covering PHS, DP, and martensitic grades designed for robust automotive safety structures. The company’s acquisition of full ownership of AM/NS Calvert for ≈USD 1.55 billion strengthens its high-quality finishing capabilities in the United States, positioning the facility as a core hub for AHSS production. ArcelorMittal is recognized as a pioneer in Third Generation AHSS tailored for EV platforms, optimizing crash absorption to counterbalance battery weight. The company is investing over USD 3 billion into Calvert, including a new Electric Arc Furnace (EAF) to supply lower-CO₂ steel aligned with OEM sustainability targets.

Nippon Steel Corporation - Strengthening North American Presence With U.S. Steel Acquisition

Nippon Steel brings decades of expertise in high-performance automotive steels with proprietary grades known for superior weldability and elongation-key to complex automotive stamping. The company’s landmark USD 14.9 billion acquisition of U.S. Steel massively expands its production base and AHSS supply chain footprint in North America. Nippon Steel is a global leader in TWIP steels, offering high ductility for high-stress structural components. Its strategic focus includes co-developing advanced steels with Asian automotive OEMs, accelerating the deployment of Q&P steels in mainstream vehicle models.

POSCO - Advancing AHSS Microstructure Control and EV-Optimized Steel Solutions

POSCO is renowned for precision automotive flat products enabled by its proprietary Continuous Annealing Line (CAL), delivering tight control over multi-phase microstructures in AHSS. Its product lineup includes specialized lightweight EV steels engineered for battery enclosures and high-voltage motor components requiring corrosion-resistant coatings. POSCO is expanding capacity through a new state-of-the-art steel plant in South Korea, purpose-built for EV and autonomous car applications. Investments in edge formability improvements for 3rd Gen AHSS reflect its commitment to solving one of the most persistent challenges in stamping ultra-high-strength components.

JFE Steel Corporation - Innovating TRIP and Hot-Stamping Steels For Lightweight Structures

JFE Steel leads in TRIP steel development, leveraging retained austenite to achieve high strength and improved work-hardening-ideal for chassis and suspension parts. The company is also advancing high-formability hot-stamping steels that enable thinner-gauge materials without compromising crash performance. Its integrated automotive solutions include galvannealed and electro-galvanized AHSS designed for superior corrosion resistance in harsh environments. JFE’s adoption of advanced digital twin technologies has resulted in a remarkable 99.8% quality conformity rate, elevating reliability for complex AHSS grades.

SSAB AB - Driving The Global Transition To Fossil-Free AHSS

SSAB is recognized for high-performance steel brands such as Docol (automotive AHSS) and Strenx (structural UHSS), meeting extreme-strength requirements across industries. The company leads the groundbreaking Hybrit initiative, transitioning toward hydrogen-reduced, fossil-free AHSS production with near-zero CO₂ emissions. SSAB offers one of the broadest ranges of cold-formed AHSS with tensile strengths up to 1,700 MPa, supporting extreme lightweighting in roll-formed components. To sharpen its focus, SSAB has divested non-core assets, allocating over 65% of capital expenditure to premium AHSS and wear steel segments.

India’s Advanced High Strength Steel (AHSS) market is being structurally reshaped by targeted industrial policy under the Production Linked Incentive (PLI 1.2) scheme for specialty steel. The third round of PLI, launched in late 2024, has repositioned AHSS as a strategic input for automotive safety, electric mobility, and infrastructure resilience rather than a niche premium product. By explicitly incentivizing advanced grades such as coated AHSS, wear-resistant steels, and high-strength automotive sheets, the policy is catalyzing large-scale capacity additions and technology upgrades across domestic mills. Investment traction from leading producers such as JSW Steel and Tata Steel underscores a decisive shift toward localized, value-added steelmaking. The planned expansion by ArcelorMittal Nippon Steel India further signals India’s ambition to integrate green steel routes with AHSS output, positioning the country as a cost-competitive yet technologically credible supplier of advanced automotive and structural steels.

South Korea’s Post-Steel City Transition and AI-Integrated AHSS Manufacturing

South Korea’s AHSS strategy reflects a deliberate transition from volume-driven steelmaking to high-value, technology-intensive production. National roadmaps for materials, parts, and equipment (MPE) are embedding AI-driven process control, hydrogen-ready reduction, and battery-compatible steel development into the country’s industrial fabric. Pohang’s evolution into a “post-steel city” exemplifies this shift, where legacy blast furnace expertise is being redeployed toward low-carbon AHSS tailored for electric vehicles and energy storage systems. Financial guarantees for exporters and targeted R&D funding for special carbon steels are stabilizing supply chains while enabling rapid grade innovation. South Korea’s tight integration between steel producers and global automotive OEMs ensures that new AHSS grades are optimized for export platforms, reinforcing the country’s role as a precision supplier in global vehicle value chains.

United States’ CHIPS-Style Steel Renaissance for EV and Defense Applications

The United States AHSS market is increasingly shaped by strategic autonomy concerns and decarbonization-linked procurement policies. Federal funding programs targeting lightweight materials for EV range extension are accelerating demand for multiphase and third-generation AHSS grades in battery enclosures, crash structures, and chassis components. Trade protection measures, including sustained tariffs on select steel imports, are reinforcing domestic production of cold-rolled and coated AHSS. Major producers such as Cleveland-Cliffs and Nucor are upgrading electric arc furnace infrastructure to deliver high-purity, low-emission AHSS aligned with Buy Clean mandates. This policy–industry alignment positions the U.S. as a premium market focused on security of supply, performance reliability, and carbon intensity reduction.

National Strategic Development Matrix: Advanced High Strength Steel Market

Advanced High Strength Steel Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

2025 Key Policy or Investment Trigger

|

Core AHSS Application Focus

|

|

India

|

PLI-led localization

|

PLI 1.2 specialty steel incentives

|

Automotive safety, EV structures

|

|

South Korea

|

AI & hydrogen transition

|

MPE roadmap and post-steel clusters

|

EV bodies, battery-compatible steels

|

|

United States

|

Supply chain security

|

DOE VTO funding and import tariffs

|

EV frames, defense-grade AHSS

|

|

EU (Germany & France)

|

Green Deal & CBAM

|

RFCS funding and SMAP rollout

|

Low-carbon automotive structures

|

|

China

|

High-end substitution

|

14th Five-Year Plan capacity upgrades

|

Gen III AHSS for autos & aerospace

|

|

Japan

|

Materials DX & neutrality

|

AI-based AHSS simulation platforms

|

Lightweight, high-reliability vehicles

|

European Union (Germany & France): Green Steel Taxonomy Driving Circular AHSS

In the European Union, particularly Germany and France, AHSS development is inseparable from the Green Deal and carbon regulation architecture. Large-scale funding through the Research Fund for Coal and Steel and coordinated policy under the Steel and Metals Action Plan are accelerating the transition toward hydrogen-ready and electrified steelmaking. Full implementation of the Carbon Border Adjustment Mechanism (CBAM) has further incentivized European producers to prioritize circular AHSS with high recycled content and certified low emissions. Automotive OEMs are increasingly specifying near-zero-carbon AHSS for safety-critical components, reinforcing Europe’s leadership in sustainability-driven material differentiation rather than cost competition.

China’s High-End Substitution Strategy and Export Repositioning

China’s AHSS market is entering a phase of qualitative transformation, moving away from sheer output dominance toward high-end substitution in automotive and aerospace applications. Under the concluding 14th Five-Year Plan, legacy capacity is being replaced with advanced continuous annealing and quenching lines capable of producing complex phase and martensitic steels. While maintaining a significant steel trade surplus, China’s export strategy in 2025 is increasingly focused on Gen III AHSS supplied to ASEAN and MENA markets, where demand for cost-efficient yet high-performance automotive steels is rising. This dual approach-domestic substitution of imports and selective high-value exports-anchors China’s competitiveness in the global AHSS landscape.

Japan’s Materials DX Platform and Carbon-Neutral Structural Steels

Japan’s Advanced High Strength Steel market is defined by precision metallurgy and digital transformation. The expansion of the Materials DX Platform is enabling AI-driven simulation of crash performance and microstructural behavior, shortening development cycles for next-generation AHSS. Steelmakers are integrating these digital tools with carbon-neutral branding strategies to deliver lighter, stronger steels that directly support automotive decarbonization goals. The strategic shift by Nippon Steel toward carbon-neutral AHSS underscores Japan’s focus on reliability, lifecycle performance, and long-term OEM partnerships rather than aggressive capacity growth.

Advanced High Strength Steel Market Report Scope

Advanced High Strength Steel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$36.9 Billion

|

|

Market Size (2035)

|

$98.4 Billion

|

|

Market Growth Rate

|

10.3%

|

|

Segments

|

By Grade/Type (Dual Phase Steel, TRIP Steel, Complex Phase Steel, Martensitic Steel, Press Hardened Steel, TWIP Steel, Ferritic-Bainitic Steel, Hot-Formed Steel, Others), By Vehicle (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), By Application (Body-in-White, Chassis & Suspension, Closures, Bumpers & Intrusion Beams, Seat Structures, Energy Absorption Systems, Battery Enclosures, Construction & Infrastructure), By Coating Type (Galvanized, Galvannealed, Electro-Galvanized, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ArcelorMittal, China Baowu Steel Group, Nippon Steel Corporation, POSCO Holdings, Tata Steel Limited, United States Steel Corporation, JFE Steel Corporation, ThyssenKrupp AG, Hyundai Steel Company, JSW Steel Limited, Shougang Group, Gestamp Automoción S.A., Nucor Corporation, Acerinox S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced High Strength Steel (AHSS) Market Segmentation

By Grade / Type

- Dual Phase Steel

- Transformation-Induced Plasticity Steel

- Complex Phase Steel

- Martensitic Steel

- Press Hardened Steel

- Twinning-Induced Plasticity Steel

- Ferritic-Bainitic Steel

- Hot-Formed Steel

- Others

By Vehicle

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

By Application

- Body-in-White

- Chassis and Suspension

- Closures

- Bumpers and Intrusion Beams

- Seat Structures

- Energy Absorption Systems

- Battery Enclosures

- Construction and Infrastructure

By Coating Type

- Galvanized

- Galvannealed

- Electro-Galvanized

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced High Strength Steel (AHSS) Market

- ArcelorMittal

- China Baowu Steel Group Corporation

- Nippon Steel Corporation

- POSCO Holdings

- Tata Steel Limited

- United States Steel Corporation

- JFE Steel Corporation

- ThyssenKrupp AG

- Hyundai Steel Company

- JSW Steel Limited

- Shougang Group

- Gestamp Automoción S.A.

- Nucor Corporation

- Acerinox S.A.

*- List not Exhaustive