Market Overview: Algae Omega 3 Ingredients Market to Reach $3.5 Billion by 2034 as Fermentation Scale-Up, Regulatory Access, and Aquafeed Integration Accelerate Adoption

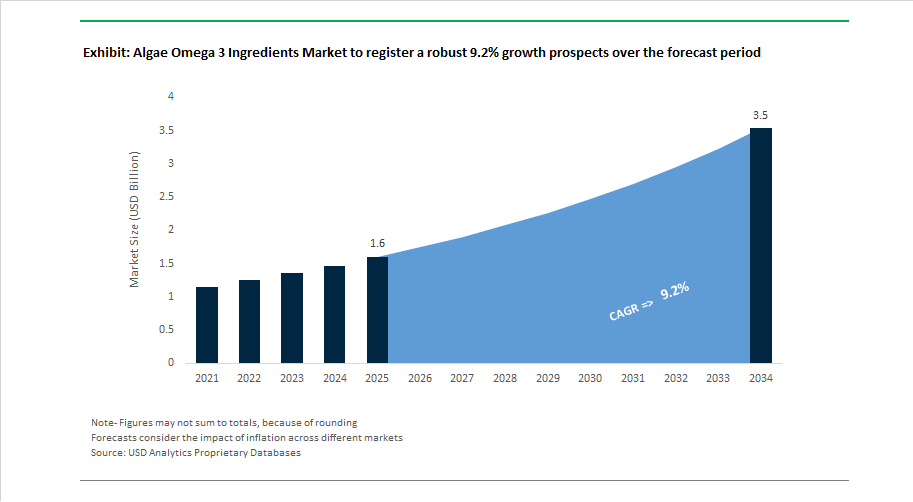

The global algae omega 3 ingredients market is projected to grow from $1.6 billion in 2025 to $3.5 billion by 2034, advancing at a 9.2% CAGR supported by rising demand for DHA and EPA-rich algal oil across infant nutrition, maternal health supplements, functional beverages, sports nutrition, aquafeed, and premium pet food formulations. Algae-derived omega 3 ingredients are gaining preference over fish oil due to vegetarian sourcing, contaminant-free purity, stable supply chains, and lower marine ecosystem impact. Industrial fermentation platforms, precision extraction technologies, and improved lipid yield optimization are enabling scalable production of long-chain fatty acids while reducing carbon intensity. Growth is further driven by regulatory approvals in key markets, intellectual property protection for proprietary processing methods, and increasing use of algae oil as a direct substitute for marine-derived lipids in aquaculture and companion animal nutrition.

Production scalability and technology innovation strengthened in October 2024 when MiAlgae secured £14 million in Series A funding to expand its circular production model using distillery by-products. In November 2024, Veramaris reported a 61% surge in algae oil output while lowering greenhouse gas emissions, demonstrating industrial maturity of fermentation-based production. Intellectual property consolidation occurred in March 2025 as DSM-Firmenich won a UK High Court patent case protecting high-purity DHA extraction processes. Market access expanded in July 2025 when Corbion secured regulatory approvals from China’s GACC for AlgaPrime and AlgaVia products. Further innovation followed in August 2025 as Corbion partnered with BRAIN Biotech to optimize fermentation yields of EPA. Logistics efficiency improved in September 2025 with Veramaris establishing bulk algae oil storage infrastructure in the Netherlands to support large-scale aquafeed deliveries.

Market maturity and demand diversification accelerated through 2026. Industry analysis released in November 2025 projected global algal oil production growth of 80% by 2030, essential to closing structural omega 3 supply deficits. Facility expansion gained momentum in January 2026 when MiAlgae broke ground on its large-scale Grangemouth plant, and leadership transition at Veramaris marked a shift toward deep-tier partnerships in aquafeed supply chains. Consumer health innovation expanded in February 2026 as Aker BioMarine introduced Revervia, a fermentation-based DHA product targeting India’s vegetarian supplement market. Pet nutrition demand also surged in February 2026, with algae recognized as a primary ingredient for contaminant-free DHA supply. These developments position algae omega 3 ingredients as a rapidly scaling, sustainable alternative supporting nutritional security and marine resource conservation.

Strategic Market Trends and High-Value Growth Opportunities Transforming the Algae Omega-3 Ingredients Market

The Algae Omega-3 Ingredients Market is transitioning from niche supplement sourcing toward mainstream integration into pharmaceuticals, clinical nutrition, infant formula, sports nutrition, and functional foods. As global concerns about marine sustainability intensify and clinical evidence continues validating the cardiovascular and cognitive benefits of omega-3s, algae-derived DHA and EPA are emerging as biosecure, scalable, and regulation-friendly lipid sources. The industry is pivoting toward precision fermentation, regulatory-accelerated market access, and controlled-environment production models, which significantly increase output reliability and purity. This structural redefinition is enabling algae omega-3 suppliers to compete directly with—and in some cases outperform—fish-oil-based supply chains.

Market Trend: Industry Shift Toward Heterotrophic Fermentation for Scalable, Contaminant-Free Omega-3 Production

One of the most consequential technological transitions is the accelerated movement away from phototrophic (pond-based) algae growth. Open-air systems create variability in output, risk microbial contamination, and require climate-dependent operations. To solve these constraints, leading manufacturers are investing aggressively in tank-based, heterotrophic fermentation, which provides total environmental control.

While open systems typically yield 0.5–4 g/L biomass, heterotrophic processes routinely reach over 75 g/L, representing nearly a 20-fold productivity increase and enabling scalable commercial supply. Veramaris’ Blair, Nebraska plant reached full-scale output capacity for the first time in 2024, delivering a 61% increase in algae oil production year-over-year. Perhaps the most disruptive efficiency metric is speed: heterotrophic algae can move from starter cell to highly refined omega-3 oil in approximately 25 days, compared with the two-year biological cycle associated with fish oil sourcing. This accelerated cycle allows producers to align inventory with seasonal spikes in infant formula and dietary supplement demand without dependence on fishing quotas or marine harvest conditions.

Market Trend: Regulatory Fast-Tracks Unlock New Food, Infant, and Supplement Categories

Regulatory approvals are now the commercial gatekeeper accelerating algae omega-3 penetration across consumer and clinical nutrition categories. China has emerged as one of the highest-potential regions: in July 2025, the GACC and NMPA granted full registrations for Corbion’s AlgaPrime DHA and AlgaVia DHA, authorizing legally compliant distribution for human nutrition and animal feed. This is a major milestone given China’s rising functional food market and its rapidly expanding prenatal supplement segment.

In Europe, EFSA’s updated infant-formula guidelines (2024) allowing algae-derived EPA inclusion up to 0.5% of total fatty acids have driven formulation revisions among leading brands. China simultaneously shortened its approval timeline from 24 months to 12 months for algae omega-3 health-food registrations and eliminated mandatory domestic clinical trials if an FDA or EFSA safety dossier is provided. Collectively, these shifts are reducing time-to-market for algal DHA/EPA and, critically, are opening doors for price-competitive food-grade supply chains, not just supplement-grade inputs.

Market Opportunity: Pharmaceutical-Grade EPA for Cardiovascular and Metabolic Disorder Treatment

A rising clinical-health opportunity lies in algae-sourced omega-3 ingredients designed for prescription-level EPA concentration. With the American Heart Association advising triglyceride-lowering EPA supplementation for roughly one in four U.S. adults, pharmaceutical demand is shifting toward ultra-pure, contaminant-free algal EPA. Heavy metal contamination in marine-harvested fish oil has amplified clinical preference for alternative inputs.

DSM-Firmenich and BASF Pharma Solutions are expanding Active Pharmaceutical Ingredient portfolios, with innovations like life’s OMEGA O3020, a high-potency EPA-DHA product engineered to match the ratio profile of fish oil while offering twice the potency in capsule form. Because algae oil production avoids mercury exposure, oxidation-risk purification steps can be skipped, reducing costs and enabling API-grade powders and oils that support new drug formats, including triglyceride-lowering softgels and metabolic disorder therapeutics. As global cardiovascular burden rises, algae Omega-3 suppliers that secure GMP certification and pharmaceutical dossier readiness will capture high-margin recurring contracts.

Market Opportunity: Stabilized Omega-3 Formats Enabling Gummies, Chewables, Bars, and Dairy Alternatives

A major demand wave is emerging in pill-alternative delivery systems, particularly gummies, chews, fortified bars, and plant-based dairy. The shift is driven by consumer pill fatigue, as well as pediatric and prenatal preferences for better-tasting, experience-based nutrition formats. However, DHA/EPA typically oxidize quickly, creating rancidity and taste challenges. Stabilization technologies are therefore becoming a competitive differentiator.

TopGum’s OMG3! platform (May 2025) uses liquid microencapsulation to embed algal DHA within confectionery matrices, eliminating sensory drawbacks and retaining active concentrations. Meanwhile, supercritical CO₂-extracted algae powders commercialized by Youchang Industry are engineered for 95% EPA/DHA retention even during heat-stress storage in tropical climates. These powders disperse readily in liquids, extending use cases to smoothies, plant-based milks, gel snacks, and energy bars. DSM-Firmenich’s life’sDHA B54-0100 specifically targets brands reformulating into "candyceutical" lines that blend nutrition and indulgence.

The Algae Omega-3 Ingredients Market is evolving into a dual-track ecosystem: high-purity pharmaceutical omega-3 oils supporting chronic-disease treatments, and stabilized functional-food ingredients designed for mass-market adoption. Firms that can scale heterotrophic fermentation, secure regulatory approvals in China and the EU, and commercialize shelf-stable DHA/EPA formats will capture the steepest growth trajectory through 2030.

Algae Omega 3 Ingredients Market Share and Segmentation Insights

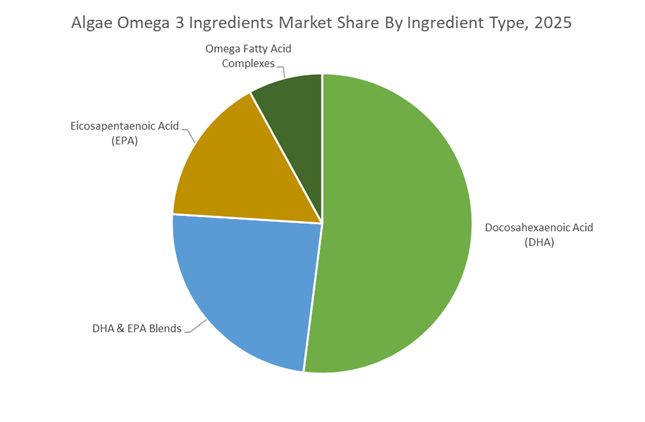

Market Share by Ingredient Type: DHA Dominates While DHA & EPA Blends Accelerate

Docosahexaenoic acid (DHA) accounts for approximately 52% of the global algae omega 3 ingredients market in 2025, reflecting its central role in brain development, cognitive performance, and visual health. DHA is the mandated omega-3 fortification standard in infant formula across major regulatory markets, creating structurally stable demand. Algal DHA has achieved near price parity with fish oil alternatives while offering superior oxidative stability and freedom from marine contaminants such as mercury and PCBs, strengthening its appeal in clean-label formulations. DHA & EPA blends rank second and represent the fastest-growing segment, supported by adult cardiovascular and prenatal supplement demand as fermentation technologies narrow the algal EPA cost gap. Standalone EPA remains high value but capacity constrained due to complex biosynthesis in specialized strains. Omega fatty acid complexes form the smallest niche, positioned as premium vegan full-spectrum alternatives with limited mass-market penetration.

Market Share by End-Use Industry: Dietary Supplements Lead While Aquaculture Drives Structural Shift

Dietary supplements represent roughly 41% of algae omega 3 ingredient consumption in 2025, making them the largest and most brand-driven segment. Growing preference for vegan, plant-based, and ocean-friendly certifications has accelerated substitution from fish oil to algal oil in adult cognitive, prenatal, and heart health formulations. Infant nutrition ranks second and remains the most stable segment, with algal DHA embedded in nearly all premium formulas under regulatory mandates in China, the EU, and the US. Aquaculture and animal feed is the fastest-growing segment, as salmon producers integrate algal oils to reduce dependence on wild-caught fish oil while maintaining EPA/DHA levels. Functional food and beverages show gradual adoption through microencapsulation technologies, while pharmaceuticals and clinical nutrition remain small but high purity segments constrained by regulatory and bioequivalence requirements.

Competitive Landscape: Precision Fermentation and Sensory Innovation Powering the Algae Omega-3 Ingredients Market

The Algae Omega-3 Ingredients Market is shifting rapidly toward fermentation-derived EPA/DHA, high-potency concentrates, and sensory-neutral formulations tailored for human nutrition, infant formula, aquaculture, pet food, and functional beverages. Competitive differentiation now centers on proprietary microalgal strains, closed-loop fermentation, organoleptic optimization, and deep vertical integration from cell culture to refined oil. Leading producers are scaling indoor production, expanding into pet and flexitarian nutrition, and embedding sustainability through renewable feedstocks and solvent-free processing, positioning algae omega-3 as a strategic alternative to marine-derived oils.

dsm-firmenich sets industry benchmarks with dual EPA+DHA algae platforms

dsm-firmenich has consolidated leadership following its merger, combining biotechnology scale with global distribution. Its life’s® portfolio remains the reference standard, with life’s®OMEGA becoming the first commercial plant-based omega-3 delivering both EPA and DHA from a single algal source. In late 2025, the company launched life’sDHA® B54-0100, enabling smaller capsules and easier inclusion in pill-fatigued markets. Strategically, dsm-firmenich is repositioning its Veramaris joint venture with Evonik Industries AG to target premium pet nutrition with 60% EPA+DHA potency. Deep vertical integration, from NASA-derived microalgal strains to indoor fermentation, enables rapid 25-day production cycles.

Corbion transforms algae omega-3 into a profitable specialty nutrition pillar

Corbion has pivoted decisively toward specialty nutrition under its BRIGHT 2030 roadmap, turning algae omega-3 into a core profit driver by 2025 following divestment of non-core emulsifiers. Through its AlgaPrime™ DHA platform, Corbion is a primary supplier to global aquaculture, reducing dependence on wild forage fish. The company is now expanding beyond oils into broader human and pet nutrition applications. Its backbone fermentation technology uses 98% renewable raw materials and has achieved net-zero targets ahead of peers, reinforcing Corbion’s position as a sustainability-first algae omega-3 producer.

Polaris leads sensory-neutral algal oils for infant and clinical nutrition

Polaris specializes in high-end lipochemistry, emphasizing taste, stability, and purity for demanding pharmaceutical and infant applications. Its Omegavie® Algae oils, produced from Schizochytrium sp., leverage patented Qualitysilver® technology to prevent oxidation. In 2025, Polaris introduced the Sensory® line with ultra-neutral flavor profiles for gummies and functional foods. Following the merger of its Alesco unit into PharmaNutra, Polaris is expanding into Sucrosomial® delivery systems to enhance nutrient absorption. The company dominates European infant and clinical nutrition segments where non-GMO status and heavy-metal-free purity are mandatory.

Mara Renewables Corporation scales solvent-free fermentation through global refining partnerships

Mara Renewables has evolved from a research-focused biotech into a global supplier, supported by a $9.1 million investment from S2G Ventures in late 2025. The company maintains a strategic go-to-market partnership with Thai Union, refining crude algal oil at Thai Union’s Rostock facility for European customers. Mara operates closed-loop, solvent-free fermentation producing GRAS-certified oils that integrate cleanly into nutritional beverages. Its competitive edge lies in an extensive IP portfolio and proprietary Atlantic microalgal strains delivering consistent, high-quality DHA.

GC Rieber VivoMega executes dual-track marine and algal concentration strategy

GC Rieber VivoMega has successfully transitioned from fish oil leadership to a dual-source omega-3 model incorporating high-concentration algal oils. In early 2026, the company opened an expanded Kristiansund facility to scale algal output for flexitarian markets. Its ability to offer both marine and algal concentrates enables customers to balance cost and vegan requirements with a single supplier. Under its “Mastering the Molecule” strategy, GC Rieber applies the same concentration expertise used in fish oils to algae, supported by AI-driven quality control meeting GOED and EFSA traceability standards.

ADM integrates algae omega-3 across global health and nutrition platforms

ADM leverages its agricultural scale to embed algae omega-3 into Health & Wellness and Animal Nutrition portfolios. The company supplies high-DHA algal oils and powders for fortification in plant-based proteins and functional beverages, aligning with its Regenerative Nutrition strategy to reduce food-chain carbon intensity. ADM’s integration capabilities allow conversion of algal DHA into powders, emulsions, and softgels at industrial scale. In 2025, ADM introduced nano-emulsion DHA formats, significantly improving shelf stability in clear beverages, strengthening its role as a formulation partner for global FMCG and nutrition brands.

United States Algae Omega 3 Ingredients Market: Domestic Fermentation Defense and Medical-Grade Validation

The United States is strengthening downstream integration and intellectual property protection to secure premium algae omega-3 supply. In early 2025, dsm‑firmenich opened a state-of-the-art premix facility in the Kansas Animal Health Corridor. The site is designed to integrate Veramaris Pets and DHAgold algae-based omega-3 into fast-growing pet nutrition lines, improving formulation control and speed to market for high-value applications.

Policy and legal actions reinforce domestic capacity. A revised tariff regime in 2025 applied countervailing duties to select imported microbial oils to protect U.S. fermentation assets. In March 2025, dsm-firmenich successfully defended a landmark patent in the UK High Court against Mara Renewables, preventing unauthorized use of algal processing technology that enables DHA concentrations exceeding traditional fish oil potency by more than twofold. Regulatory reformulation is accelerating after the U.S. Food and Drug Administration revoked authorization for FD&C Red No. 3 in dietary supplements in January 2025, pushing omega-3 softgels toward cleaner, algae-derived ingredients ahead of 2027. Clinical evidence presented at U.S. forums in 2025 validated high-dose algal DHA at 3,000 to 4,000 mg for inflammation and anxiety management, catalyzing a new wave of medical-grade products.

Netherlands Algae Omega 3 Ingredients Market: Bulk Logistics Breakthrough and Carbon-Efficient Scaling

The Netherlands is anchoring Europe’s algae omega-3 supply through logistics innovation and sustainability credentials. In September 2025, Veramaris partnered with Merwetank B.V. to construct a specialized bulk algae oil storage tank in Dordrecht near Rotterdam. Operational by mid-Q4 2025, the facility enables the first bulk shipments of algae oil directly to coastal aquafeed factories, removing drum-based transport constraints.

Performance and sustainability reinforce expansion. Corbion, headquartered in Amsterdam, earned a Gold Medal from EcoVadis in 2025 for carbon management across AlgaPrime DHA and AlgaVia lines. Corbion reported strong first-half 2025 financial performance driven by aquaculture and pet nutrition demand. The new storage infrastructure is projected to reduce logistics-related carbon emissions by 30 percent, improving cost efficiency and environmental outcomes for large feed producers.

Norway Algae Omega 3 Ingredients Market: Aquafeed Substitution and Circular Carbon Utilization

Norway is redefining omega-3 sourcing for aquaculture through algae-based substitution supported by policy and science. In December 2025, the Centre for Feed Innovation confirmed that algal oil can fully replace fish oil in commercial salmon diets without compromising growth or omega-3 retention, marking a structural shift in feed formulation.

Circular economy execution strengthens adoption. A 2025 collaboration between UiT The Arctic University of Norway and Finnfjord captured 300,000 tonnes of CO₂ annually to cultivate microalgae that are processed into omega-3-rich feed. Research from Nofima in June 2025 demonstrated up to 15% algae inclusion in salmon feed with a documented sea-lice reduction effect. Government backing integrates algal oil into the national sustainable feed strategy and supports ASC-MSC certified algae oils to close the sector’s omega-3 gap.

China Algae Omega 3 Ingredients Market: Regulatory Gatekeeping and Production Technology Upgrade

China is expanding access while tightening quality thresholds for algae omega-3. In July 2025, Corbion secured approvals from the General Administration of Customs of China to sell algae-derived DHA for both human and animal nutrition, unlocking broad downstream adoption.

Standards are rising. The State Administration for Market Regulation issued updated standards in late 2025 that impose stricter heavy-metal limits for algae oils used in infant formula. To comply and scale, domestic producers are transitioning from open-pond systems to closed photo-bioreactor technology, targeting higher purity and faster harvest cycles in 2026. This shift positions China as both a major consumption market and an emerging high-quality producer.

Canada Algae Omega 3 Ingredients Market: Biorefinery R&D and Clean-Label Differentiation

Canada’s strategy emphasizes innovation depth and clean-label positioning. Federal funding continues to support Integrated Microalgae Biorefinery projects that co-extract omega-3 fatty acids with high-value co-products such as astaxanthin, improving project economics and resilience.

Commercial diversification is advancing. Mara Renewables expanded clean-label algae oil production in 2025 to serve the fast-growing vegan dietary supplement segment in North America. This approach positions Canada as an innovation-led supplier focused on premium and plant-based nutrition rather than volume-driven output.

Country-Level Positioning in the Algae Omega-3 Ingredients Industry

Algae Omega-3 Ingredients Market County Level Snapshot

|

Country

|

Strategic Focus

|

Implication for Adoption

|

|

United States

|

IP enforcement, clinical validation, domestic fermentation

|

Premium and medical-grade leadership

|

|

Netherlands

|

Bulk logistics, carbon efficiency, profitability

|

Scalable and low-emission supply hub

|

|

Norway

|

Algae-fed salmon, circular CO₂ utilization

|

Structural substitution of fish oil

|

|

China

|

Regulatory approvals, PBR transition

|

Rapid uptake with higher quality thresholds

|

|

Canada

|

Biorefinery R&D, clean-label vegan products

|

Innovation-led niche expansion

|

Algae Omega-3 Ingredients Market Report Scope

Algae Omega 3 Ingredients Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$3.5 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Ingredient Type (Docosahexaenoic Acid, Eicosapentaenoic Acid, DHA and EPA Blends, Omega Fatty Acid Complexes), By Source (Schizochytrium, Ulkenia, Crypthecodinium cohnii, Nannochloropsis), By Form (Bulk Oil, Powder, Suspension and Emulsion, Ethyl Esters), By Production Technology (Heterotrophic Fermentation, Phototrophic Cultivation, Hybrid Cultivation Systems), By End Use Industry (Dietary Supplements, Infant Nutrition, Aquaculture and Animal Feed, Functional Food and Beverages, Pharmaceuticals and Clinical Nutrition)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

dsm firmenich, Corbion NV, Veramaris, BASF SE, Polaris, Mara Renewables Corporation, Archer Daniels Midland Company, Cargill Incorporated, Fermentalg, CABIO Biotech, AlgiSys BioSciences, Cellana, Bioprocess Algae, Phytosolum, Skretting

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Algae Omega 3 Ingredients Market Segmentation

By Ingredient Type

- Docosahexaenoic Acid

- Eicosapentaenoic Acid

- DHA and EPA Blends

- Omega Fatty Acid Complexes

By Source

- Schizochytrium

- Ulkenia

- Crypthecodinium cohnii

- Nannochloropsis

By Form

- Bulk Oil

- Powder

- Suspension and Emulsion

- Ethyl Esters

By Production Technology

- Heterotrophic Fermentation

- Phototrophic Cultivation

- Hybrid Cultivation Systems

By End Use Industry

- Dietary Supplements

- Infant Nutrition

- Aquaculture and Animal Feed

- Functional Food and Beverages

- Pharmaceuticals and Clinical Nutrition

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Algae Omega 3 Ingredients Industry

- dsm firmenich

- Corbion NV

- Veramaris

- BASF SE

- Polaris

- Mara Renewables Corporation

- Archer Daniels Midland Company

- Cargill Incorporated

- Fermentalg

- CABIO Biotech

- AlgiSys BioSciences

- Cellana

- Bioprocess Algae

- Phytosolum

- Skretting

*- List not Exhaustive