Microencapsulation Market 2025–2034: Biopolymer Innovation, Regulatory-Driven Reformulation, and Controlled-Release Platforms Propel $38.7 Billion Opportunity

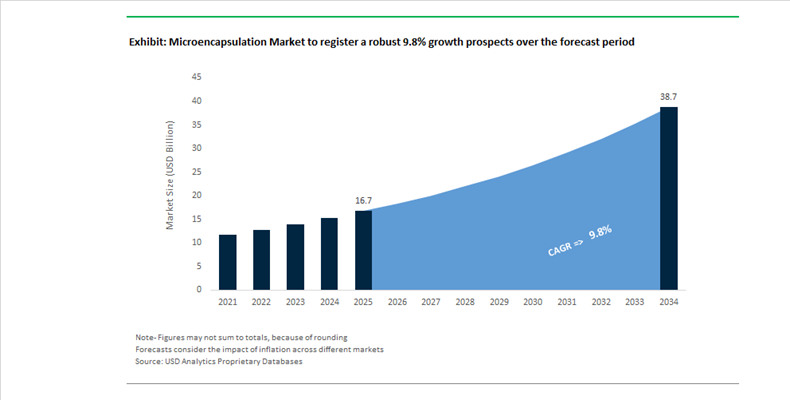

The Microencapsulation Market is projected to expand from $16.7 billion in 2025 to $38.7 billion by 2034, advancing at a CAGR of 9.8%. Growth is being accelerated by regulatory pressure on synthetic polymer microparticles, increasing demand for precision nutrient delivery, and the commercialization of biodegradable shell technologies. Microencapsulation has evolved into a core enabling platform across fabric care, personal care, pharmaceuticals, functional foods, agrochemicals, and nutraceuticals. The transition from traditional melamine-formaldehyde and polyacrylate shells toward plant-based and enzymatically engineered biopolymers represents one of the most significant structural shifts in the sector. Compliance with EU REACH restrictions and ECHA microplastic mandates is catalyzing rapid portfolio upgrades among global fragrance and ingredient leaders.

In July 2025, International Flavors & Fragrances introduced ENVIROCAP™, a biodegradable scent delivery system designed for fabric care applications. The biopolymer-based capsules provide controlled fragrance release during laundering while fully complying with EU synthetic polymer microparticle restrictions. In November 2025, Givaudan expanded its PlanetCaps™ microplastic-free fragrance system into hair and body care categories, enabling long-lasting scent retention in both rinse-off and leave-on products. To meet surging demand, Givaudan doubled encapsulation capacity at its Mexico site in late 2025 and announced further production expansion in Singapore for early 2026. These capacity expansions underscore how sustainability compliance is no longer optional but foundational to growth strategies in encapsulated fragrance technologies.

Nutritional and bioactive delivery systems are also advancing rapidly. In October 2025, BASF launched Lutavit® A/D3 1000/200 NXT, a microencapsulated beadlet combining vitamins A and D3 with enhanced oxidative stability and extended shelf life for feed premixes. In May 2024, Lubrizol unveiled LIPOFER™, engineered to encapsulate iron for food fortification while preventing metallic off-notes and reactive discoloration. Meanwhile, TopGum commercialized high-load microencapsulated caffeine gummies in early 2025, enabling sustained release and improved taste masking. In November 2024, Yili Group partnered with Xampla to deploy plant-protein-based capsules in dairy fortification, eliminating synthetic coatings entirely.

Strategic alliances and pharmaceutical innovation further reinforce the sector’s expansion. In October 2025, BASF and IFF entered a bio-innovation alliance to co-develop Designed Enzymatic Biomaterials™, leveraging advanced encapsulation to stabilize sensitive bio-actives. Symrise expanded its Holzminden mixing facility in partnership with GEA to increase capacity for microencapsulated liquid flavors by up to 50%, targeting clean-label markets. In November 2025, InnoCore Pharmaceuticals secured EU funding to develop biodegradable peptide-loaded microspheres for long-acting metabolic therapies. Following the integration of Encapsys, Milliken & Company scaled agricultural microencapsulation systems to enable controlled pesticide release and smart seed coatings. Collectively, these developments position microencapsulation as a high-growth, cross-sector technology platform underpinning sustainability, precision dosing, and next-generation functional materials.

Microencapsulation Market Trends and Opportunities

Trend: Strategic In-Housing and Captive R&D by Food and Beverage CPG Leaders

The microencapsulation market is witnessing a decisive shift as large Food and Beverage CPG companies internalize encapsulation capabilities to gain tighter control over functionality, intellectual property, and time-to-market. Rather than relying solely on third-party ingredient suppliers, brand owners are establishing captive microencapsulation platforms to differentiate fortified foods, beverages, and nutraceuticals through proprietary delivery systems. This transition is particularly visible in omega-3s, probiotics, minerals, and fat-soluble vitamins, where bioavailability, oxidative stability, and taste masking directly influence consumer acceptance and regulatory shelf-life claims.

In September 2024, dsm-firmenich expanded its Singapore innovation campus to pilot next-generation encapsulation architectures tailored to the Asian functional food market. The facility enables rapid prototyping of trigger-release mineral systems that remain stable under high-heat and high-humidity storage conditions common in tropical regions. From a performance standpoint, industrial benchmarks indicate that advanced encapsulation technologies can preserve up to 95% of active ingredient potency during thermal processes such as UHT pasteurization, compared to approximately 60% retention in non-encapsulated formats. This delta is driving dairy, bakery, and beverage OEMs to invest directly in spray-drying and complex coacervation lines.

Clean-label alignment further reinforces this trend. According to early 2025 insights from the Indian Council of Agricultural Research, spray-drying remains the preferred in-house encapsulation route due to its scalability and ability to mask off-notes without synthetic additives. As global consumers increasingly scrutinize ingredient lists, captive microencapsulation is becoming a strategic lever for CPGs to balance nutritional fortification with label simplicity, brand protection, and margin resilience.

Trend: Standardization of Encapsulated Phase Change Materials in Cold Chain Logistics

Microencapsulation is also becoming a standardized technology layer within cold chain logistics as pharmaceutical biologics, vaccines, and direct-to-consumer meal kits scale globally. Encapsulated Phase Change Materials function as thermal buffers, absorbing and releasing latent heat at defined temperatures to maintain narrow thermal windows during transport and storage. Between 2024 and 2025, deployment of PCM microcapsules across automotive and HVAC applications demonstrated energy efficiency improvements of roughly 15%, validating their economic and environmental value beyond niche use cases.

Infrastructure players are accelerating adoption. Armstrong World Industries has integrated PCM microcapsule technologies such as Templok into building panels and logistics systems to stabilize temperature fluctuations and reduce HVAC loads. Within cold chain operations, the Global Cold Chain Alliance estimates that nearly 20% of perishable food losses and a significant share of pharmaceutical efficacy degradation are linked to temperature excursions. This has driven logistics operators toward microencapsulated organic PCMs, particularly paraffin-based systems, which now account for approximately 44% of PCM form-factor usage due to their chemical stability, non-corrosive behavior, and predictable thermal performance.

Standardization is advancing through strategic partnerships. Collaborations between DIC Corporation and Phase Change Solutions are focused on commercializing BioPCM solutions for pharmaceutical warehouses and logistics hubs. These bio-based, microencapsulated PCMs are engineered to flatten peak temperature loads, reduce energy consumption, and meet increasingly strict GDP compliance requirements across global pharma distribution networks.

Opportunity: Targeted Flavor Release for Alternative Protein and Cultivated Meat

One of the most commercially attractive opportunities in the microencapsulation market lies in addressing the sensory limitations of plant-based and cultivated meat products. Flavor release, fat perception, and aroma evolution during cooking remain the primary barriers to mass adoption. Microencapsulation enables multi-stage flavor delivery, releasing savory and fatty notes only at specific temperatures or mechanical stresses such as chewing, closely replicating the behavior of animal fat.

In January 2024, Unilever, IFF, and Wageningen University launched a four-year research program to resolve bitterness and off-notes in plant proteins. The initiative centers on understanding how microencapsulated flavors interact with protein matrices to deliver sequential aroma release during grilling and mastication. Parallel innovation is emerging from precision fermentation. In November 2024, Nourish Ingredients partnered with Cabio to commercialize Tastilux, a fermented fat mimetic that uses solvent-free extraction and microencapsulation to survive extrusion and deliver authentic mouthfeel at point of consumption.

Regulatory momentum is amplifying demand. With cultivated meat approvals accelerating in 2025 across the United States and Asia, manufacturers are increasingly developing hybrid products where cultivated fats are microencapsulated and embedded within plant-based scaffolds. This creates realistic marbling, controlled fat release, and scalable pathways to regulatory-compliant, premium alternative proteins.

Opportunity: Autonomous Self-Healing Microcapsules for Industrial and Marine Coatings

The final high-impact opportunity for microencapsulation lies in autonomous self-healing systems for industrial, marine, and energy infrastructure coatings. These coatings embed microcapsules filled with healing agents that rupture upon mechanical damage, releasing corrosion inhibitors or polymerizable resins that seal defects before degradation accelerates. Rising maintenance costs for bridges, offshore wind assets, and naval vessels are making preventive, self-repairing coatings economically compelling.

By August 2025, U.S. infrastructure projects had begun deploying polymer-based self-healing coatings on steel bridges and load-bearing structures to mitigate sub-surface corrosion and extend maintenance cycles. In marine environments, adoption is accelerating even faster. In February 2025, major maritime operators implemented microcapsule-enabled coatings for ship hulls and offshore platforms, using linseed oil or epoxy-based agents to arrest saltwater corrosion immediately after impact or abrasion.

Microencapsulation Market Share and Segmentation Insights

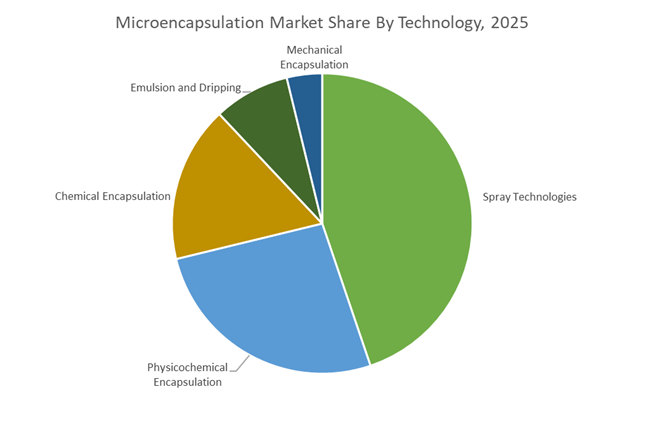

Spray Technologies Dominate Microencapsulation Market Through High-Volume Industrial Encapsulation Efficiency

Spray technologies accounted for 44.80% of the Microencapsulation Market share in 2025, making them the leading encapsulation method across pharmaceutical, food ingredient, and agrochemical industries. Techniques such as spray drying, spray cooling, spray chilling, and fluid bed coating enable large-scale production of microencapsulated materials with controlled particle size, uniform shell formation, and consistent release characteristics. Spray drying remains the most widely adopted technique due to its ability to convert liquid formulations into stable powder microcapsules suitable for large-volume industrial use. These systems are particularly valuable for encapsulating flavors, vitamins, active pharmaceutical ingredients, probiotics, fragrances, and crop protection chemicals, where protection of sensitive compounds and controlled release performance are critical. Spray technologies also support processing of heat-sensitive materials through rapid solvent evaporation and optimized drying conditions, preserving ingredient functionality. In 2025, engineering advancements including improved atomization nozzles, optimized drying chamber airflow design, and advanced digital process control systems have improved spray encapsulation efficiency by increasing product yield, reducing energy consumption, and enhancing particle uniformity across large-scale manufacturing operations.

Pharmaceuticals and Healthcare Sector Leads Demand for Microencapsulation Technologies

Pharmaceuticals and healthcare accounted for 36.80% of the Microencapsulation Market share in 2025, positioning the sector as the largest end-use industry for microencapsulation technologies. Microencapsulation is widely used in pharmaceutical formulations to achieve controlled drug release, protection of active pharmaceutical ingredients (APIs), improved bioavailability, and taste masking in oral medications. Encapsulation technologies enable pharmaceutical manufacturers to deliver drugs through extended-release tablets, injectable microspheres, topical drug carriers, and implantable delivery systems, improving therapeutic performance and patient compliance. Microencapsulation also protects drug compounds from oxidation, moisture exposure, and chemical degradation, extending product shelf life and ensuring consistent dosage performance. In 2025, rapid growth in biologic therapeutics, peptide drugs, and protein-based medicines has significantly increased the importance of microencapsulation technologies capable of stabilizing complex biomolecules. Advanced encapsulation polymers and carrier materials are being developed to support sustained-release biologic formulations and targeted delivery systems, enabling pharmaceutical manufacturers to protect fragile biologics while improving dosing efficiency and therapeutic outcomes in modern drug development pipelines.

Microencapsulation Market Competitive Landscape

The microencapsulation market in 2026 is driven by biodegradable shell materials, ECHA-compliant microplastic-free systems, and stimuli-responsive release technologies. Competitive leadership is defined by bio-based polymers, precision coacervation, and controlled-release systems that enhance stability, bioavailability, and targeted delivery across pharmaceutical, agrochemical, and personal care sectors.

BASF scales bio-based encapsulation with Verbund integration and high-stability nutrition solutions

BASF SE is leading the microencapsulation market through its vertically integrated Verbund model and focus on sustainable, high-performance formulations. Its Lutavit® A/D3 NXT microencapsulated vitamin blend delivers 18-month stability in mineral-rich premixes, addressing animal nutrition efficiency. The company’s €3.4 billion CAPEX strategy prioritizes specialty chemicals and resource-efficient encapsulation technologies. BASF is advancing decarbonized production at its Zhanjiang site, targeting over 10% reduction in polymer carbon footprint. Its ability to control the full value chain ensures consistent quality across pharma, personal care, and food applications. BASF’s regulatory-aligned innovation and industrial scale position it as a global leader in bio-based microencapsulation.

Givaudan accelerates biodegradable fragrance encapsulation with high-load PlanetCaps™ systems

Givaudan is redefining sustainable microencapsulation through its PlanetCaps™ platform, delivering microplastic-free, biodegradable fragrance systems. Expansion into personal care applications enables scalable deployment across body and hair products with over 20 scent profiles. Its IRRESISTIBLE Laundry Serum utilizes advanced capsules with a 40% fragrance load, delivering long-lasting scent performance up to one year. The company is expanding its Singapore production hub in 2026 to meet rising APAC demand. With over 60% of capsule shells certified biodegradable under OECD standards, Givaudan is aligning with ECHA mandates. Its focus on high-hedonic performance and sustainability strengthens its leadership in premium fragrance delivery systems.

IFF advances bioscience-driven encapsulation with plastic-free delivery systems and strategic partnerships

International Flavors & Fragrances (IFF) is strengthening its market position through ENVIROCAP, a plastic-free encapsulation platform designed for fabric care and volatile oil stabilization. Its collaboration with BASF integrates bioscience and polymer expertise to develop next-generation bio-based encapsulation matrices. With $10.89 billion in 2025 revenue, growth is driven by its Scent and Health & Biosciences segments. IFF’s portfolio reset strategy is reallocating capital toward high-margin encapsulated fragrance and enzyme technologies. Its Sensory Perception™ platform enables functional textiles with controlled release of actives like Vitamin E and Aloe Vera. IFF’s innovation in sustainable delivery systems positions it as a key player in advanced encapsulation technologies.

Syngenta integrates smart-release agrochemical microcapsules with AI-enabled precision agriculture platforms

Syngenta Group is a leader in agricultural microencapsulation, focusing on UV-stable, rainfast formulations that enhance crop protection efficiency. Its Vertento insecticide, powered by PLINAZOLIN® technology, delivers extended field activity through advanced encapsulation. The company is expanding its biologicals portfolio, using encapsulation to stabilize sensitive microbial and terpene-based solutions. Integration with the Cropwise® platform enables AI-driven application based on real-time environmental triggers across over 70 million hectares. Strategic collaborations with SALIC support food security initiatives in climate-stressed regions. Syngenta’s combination of digital agriculture and smart-release technologies positions it at the forefront of sustainable crop protection.

Lonza leads pharmaceutical microencapsulation with lipid nanoparticle systems and advanced CDMO capabilities

Lonza Group is the global benchmark for pharmaceutical microencapsulation, specializing in lipid nanoparticle (LNP) systems for mRNA and gene therapies. Its “One Lonza” model integrates bioconjugates and small molecule platforms to deliver end-to-end encapsulation services. The Cocoon® platform’s FDA AMT designation accelerates regulatory approval for cell and gene therapy manufacturing. The acquisition of Redberry enhances real-time microbiological validation for encapsulated biologics. Lonza is expanding its global footprint with a new capability center in Hyderabad, supporting its CDMO-focused strategy. Its expertise in targeted delivery and regulatory compliance positions it as a leader in high-value therapeutic encapsulation.

United States: Solvent Exit, Enclosed Automation, and Resilient Agrochemical Formulations

The United States microencapsulation market is undergoing a structural process transition driven by chemical regulation and occupational safety mandates. Following the April 2024 TSCA Section 6 final rule from the U.S. Environmental Protection Agency, most industrial uses of methylene chloride, a legacy solvent in capsule synthesis, are prohibited for non-exempt sectors after April 28, 2026. This has accelerated a shift toward aqueous-based systems and green-solvent encapsulation routes across consumer goods, food ingredients, and specialty formulations. For essential uses that remain permitted, the mandated Workplace Chemical Protection Program enforces an Existing Chemical Exposure Limit of 2 ppm, with initial exposure monitoring due by November 2026. These requirements are forcing capital deployment into fully enclosed, automated microencapsulation cells with in-line monitoring and minimal operator intervention.

Application demand is reinforcing this transition, particularly in agriculture. Corteva Agriscience introduced Resicore REV 3.26CS in January 2025, featuring an updated encapsulated acetochlor that improves crop safety and extends residual weed control in corn. Corteva’s Enversa 3CS, also launched in 2025, applies controlled-release encapsulation to enable surface persistence until rainfall activation, a performance attribute aligned with increasingly volatile weather patterns. In parallel, federal Bioeconomy funding has catalyzed biopolymer innovation, including a $125 million allocation in Pennsylvania during 2025 to develop starch- and cellulose-based capsule walls as replacements for synthetic polymers in functional foods.

Germany: Microplastic Compliance and Precision Encapsulation at GMP Scale

Germany’s microencapsulation market is anchored in regulatory alignment and high-precision delivery performance. With the European Chemicals Agency restriction on intentionally added microplastics entering force, German suppliers completed the phase-out of non-compliant capsule systems ahead of October 17, 2025, when new information obligations under Regulation (EU) 2023/2055 took effect. These requirements have pushed the market toward biodegradable shells and documented end-of-life guidance, elevating compliance from a material choice to a lifecycle obligation.

Pharmaceutical and agrochemical innovations illustrate this pivot. Evonik received the CPHI Excellence in Pharma Award in October 2025 for EUDRACAP® colon, the first ready-to-fill functional capsule designed to target the ileo-colonic region under GMP conditions. In crop protection, BASF reported Liberty ULTRA applications across 60 million acres in 2025, leveraging Liberty Lock encapsulation to protect the active ingredient until leaf contact and deliver materially higher weed control versus generic formulations. Evonik’s November 2025 partnership with InVitria further expands access to animal-component-free albumin coatings, supporting high-performance microencapsulation in biopharmaceuticals.

Switzerland: Corporate-Led Sustainability and High-Load Fragrance Delivery

Switzerland functions as a global innovation hub where sustainability-compliant microencapsulation platforms are commercialized and scaled internationally. In November 2025, Givaudan extended its PlanetCaps™ technology, a biodegradable and microplastic-free fragrance encapsulation, into personal care applications. To meet rising global demand, Givaudan confirmed capacity expansion at its Singapore site in Q1 2026, positioning Asia as a manufacturing backbone for compliant capsule systems.

Product innovation is emphasizing performance density alongside compliance. Givaudan’s patent-pending laundry serum launched in late 2025 delivers a 40% fragrance load within PlanetCaps™, targeting long-lasting scent release in fabric care. Complementing this, International Flavors & Fragrances introduced ENVIROCAP™ in July 2025, a vegan-suitable biopolymer system designed for controlled scent bursts while meeting 2026 biodegradability standards. Switzerland’s role is therefore defined by platform leadership and formulation science rather than bulk production.

China: Digitalized Scale and Cross-Sector Application Expansion

China is advancing microencapsulation through industrial digitalization and coordinated demand creation. The Ministry of Industry and Information Technology issued a 2025–2026 petrochemical growth plan prioritizing advanced fine chemicals and high-end polyolefins, both essential inputs for capsule wall materials. Under the AI plus petrochemicals initiative, chemical parks are deploying AI-driven precision dosing to standardize capsule size and release profiles, addressing variability challenges that previously constrained smaller producers.

Beyond process upgrades, policy support is widening application scope. MIIT-led supply-demand matchmaking is cultivating new use cases for microencapsulated materials in humanoid robotics and low-altitude economy sensors, while pharmaceutical approvals are being fast-tracked for smart formulations responsive to pH and enzymatic triggers. These measures position China to combine scale with improved technical consistency across industrial, medical, and emerging technology segments.

South Korea: Battery Safety and Encapsulated Energy Materials

South Korea’s microencapsulation trajectory is closely tied to next-generation energy storage. In November 2025, the Ministry of Trade, Industry, and Energy announced a multi-year investment program totaling 280 billion won to develop microencapsulated additives for all-solid-state and lithium-sulfur batteries. These capsules are engineered to enhance thermal stability and mitigate degradation under high-energy-density conditions.

Supply chain resilience is reinforcing R&D intensity. A 100 billion won stabilization fund is supporting domestic development of microencapsulated electrolytes that reduce thermal runaway risks in EV batteries, decreasing reliance on imported materials. This positions South Korea at the intersection of microencapsulation and battery safety, where controlled release and phase-change behavior are mission-critical.

Comparative Snapshot: Country-Level Positioning in the Microencapsulation Market

Microencapsulation Market County Level Snapshot

|

Country / Region

|

Primary Policy or Demand Driver

|

Technology Emphasis

|

Core End-Use Focus

|

Strategic Outcome

|

|

United States

|

TSCA solvent restrictions and WCPP

|

Enclosed, aqueous-based systems

|

Agrochemicals, functional foods

|

Process modernization with compliance

|

|

Germany

|

ECHA microplastic restriction

|

Biodegradable, GMP-grade capsules

|

Pharma, crop protection

|

Regulation-aligned precision

|

|

Switzerland

|

Corporate sustainability platforms

|

High-load fragrance encapsulation

|

Home and personal care

|

Global innovation leadership

|

|

China

|

MIIT digitalization and growth plans

|

AI-controlled capsule uniformity

|

Pharma, robotics, sensors

|

Scaled consistency across sectors

|

|

South Korea

|

Battery safety investments

|

Thermal and electrolyte microcapsules

|

EV and energy storage

|

High-value, safety-critical applications

|

Microencapsulation Market Report Scope

Microencapsulation Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.7 Billion

|

|

Market Size (2034)

|

$38.7 Billion

|

|

Market Growth Rate

|

9.8%

|

|

Segments

|

By Technology (Spray Technologies, Emulsion and Dripping, Physicochemical Encapsulation, Chemical Encapsulation, Mechanical Encapsulation), By Wall Material (Polymers, Gums and Resins, Lipids, Carbohydrates, Proteins), By Application (Pharmaceuticals and Healthcare, Food and Beverages, Home and Personal Care, Agrochemicals, Textiles, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Givaudan, International Flavors and Fragrances, Evonik Industries, Symrise, SABIC, Corteva Agriscience, Dow, LyondellBasell Industries, Ingredion, Lonza, Milliken and Company, Balchem, Mitsubishi Chemical, Shin-Etsu Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Microencapsulation Market Segmentation

By Technology

- Spray Technologies

- Emulsion and Dripping

- Physicochemical Encapsulation

- Chemical Encapsulation

- Mechanical Encapsulation

By Wall Material

- Polymers

- Gums and Resins

- Lipids

- Carbohydrates

- Proteins

By Application

- Pharmaceuticals and Healthcare

- Food and Beverages

- Home and Personal Care

- Agrochemicals

- Textiles

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Microencapsulation Market

- BASF

- Givaudan

- International Flavors and Fragrances

- Evonik Industries

- Symrise

- SABIC

- Corteva Agriscience

- Dow

- LyondellBasell Industries

- Ingredion

- Lonza

- Milliken and Company

- Balchem

- Mitsubishi Chemical

- Shin-Etsu Chemical

*- List not Exhaustive